- Summary

- Table Of Content

- Methodology

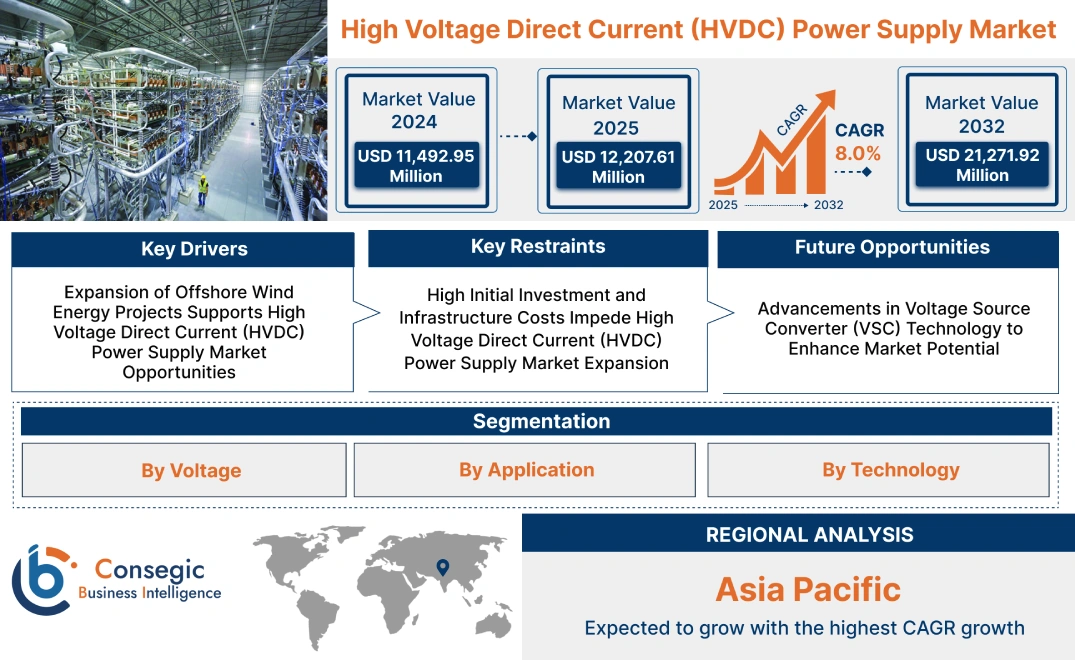

High Voltage Direct Current (HVDC) Power Supply Market Size:

High Voltage Direct Current (HVDC) Power Supply Market size is estimated to reach over USD 21,271.92 Million by 2032 from a value of USD 11,492.95 Million in 2024 and is projected to grow by USD 12,207.61 Million in 2025, growing at a CAGR of 8.0% from 2025 to 2032.

High Voltage Direct Current (HVDC) Power Supply Market Scope & Overview:

High Voltage Direct Current (HVDC) power supply systems transmit electricity over long distances with minimal losses, ensuring efficient and stable power distribution. These systems use converter stations, cables, and transformers to convert, transmit, and regulate high-voltage power. Key features include low transmission losses, enhanced grid stability, and compatibility with renewable energy sources. HVDC power supplies support bidirectional power flow, voltage control, and reduced environmental impact compared to conventional alternating current (AC) systems.

The benefits include efficient long-distance power transmission, improved system reliability, and enhanced integration of renewable energy sources. HVDC technology supports grid interconnections, ensuring seamless electricity distribution across regions. Applications include power generation, industrial operations, and utility-scale transmission networks. End-use industries include energy, manufacturing, transportation, and telecommunication sectors. HVDC power supply systems play a crucial role in ensuring stable and efficient electricity distribution in these industries.

High Voltage Direct Current (HVDC) Power Supply Market Dynamics - (DRO):

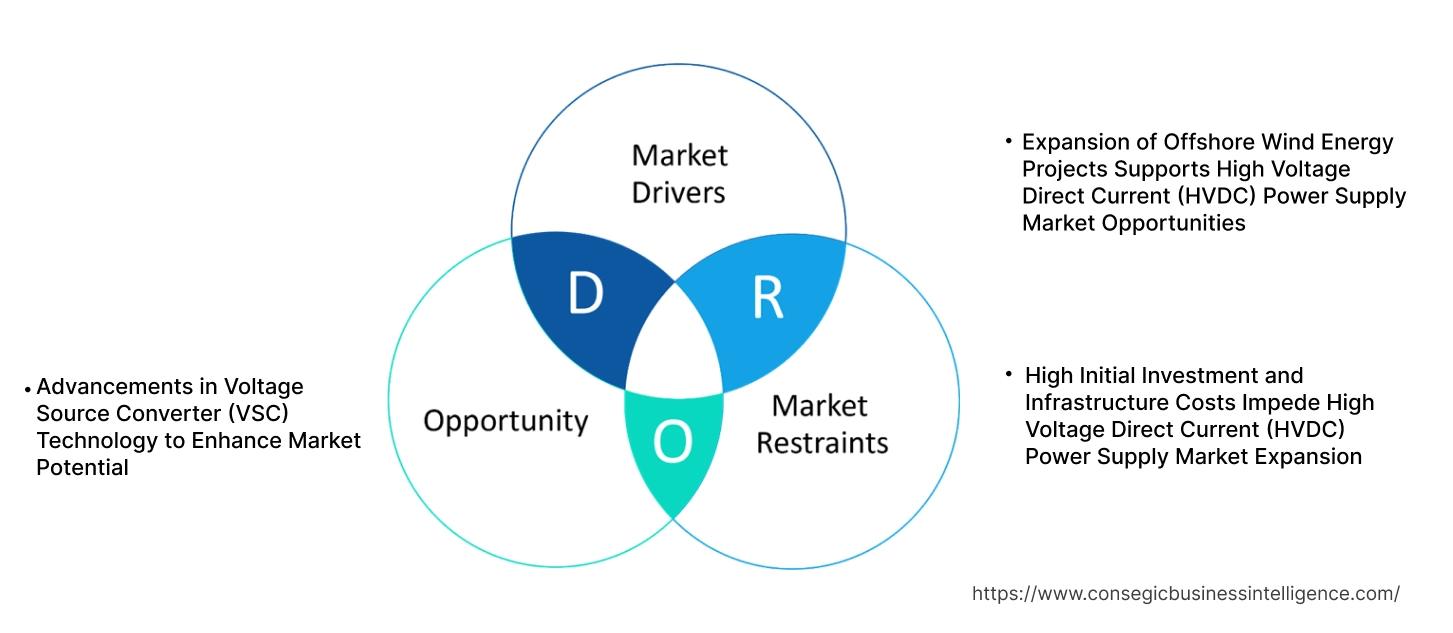

Key Drivers:

Expansion of Offshore Wind Energy Projects Supports High Voltage Direct Current (HVDC) Power Supply Market Opportunities

Offshore wind energy projects require efficient power transmission solutions to transport electricity from wind farms to onshore grids. HVDC power supply is an ideal solution as it minimizes power losses over long distances and ensures stable energy transmission. Unlike conventional alternating current (AC) systems, HVDC technology offers enhanced grid stability and facilitates the integration of renewable energy sources into national grids. For instance, projects like the North Sea Link, a subsea HVDC interconnector, demonstrate the effectiveness of HVDC in offshore energy transmission.

Therefore, the increasing deployment of offshore wind energy projects contributes to the expansion of the HVDC power supply market.

Key Restraints:

High Initial Investment and Infrastructure Costs Impede High Voltage Direct Current (HVDC) Power Supply Market Expansion

The deployment of HVDC power supply systems requires substantial capital investment for infrastructure development, including converter stations, transmission lines, and grid integration components. These systems involve complex engineering and advanced technologies, leading to higher installation costs compared to traditional AC transmission. Additionally, the cost of upgrading existing power grids to support HVDC technology adds to financial constraints. For instance, the development of large-scale HVDC interconnectors requires government support and long-term financial commitments.

These significant investment requirements act as a barrier to widespread adoption, restraining the market's expansion.

Future Opportunities:

Advancements in Voltage Source Converter (VSC) Technology to Enhance Market Potential

Future advancements in Voltage Source Converter (VSC) technology are expected to improve the efficiency and flexibility of HVDC power supply systems. VSC-HVDC technology enables better control over power flow, enhances grid stability, and allows for the seamless integration of renewable energy sources. Innovations in modular multilevel converters (MMC) are expected to reduce power losses and increase the reliability of HVDC transmission. For instance, research on next-generation VSC-based systems is focused on reducing costs and expanding application possibilities in urban and industrial settings.

Thus, technological advancements in VSC are anticipated to create significant opportunities for the HVDC power supply market.

High Voltage Direct Current (HVDC) Power Supply Market Segmental Analysis :

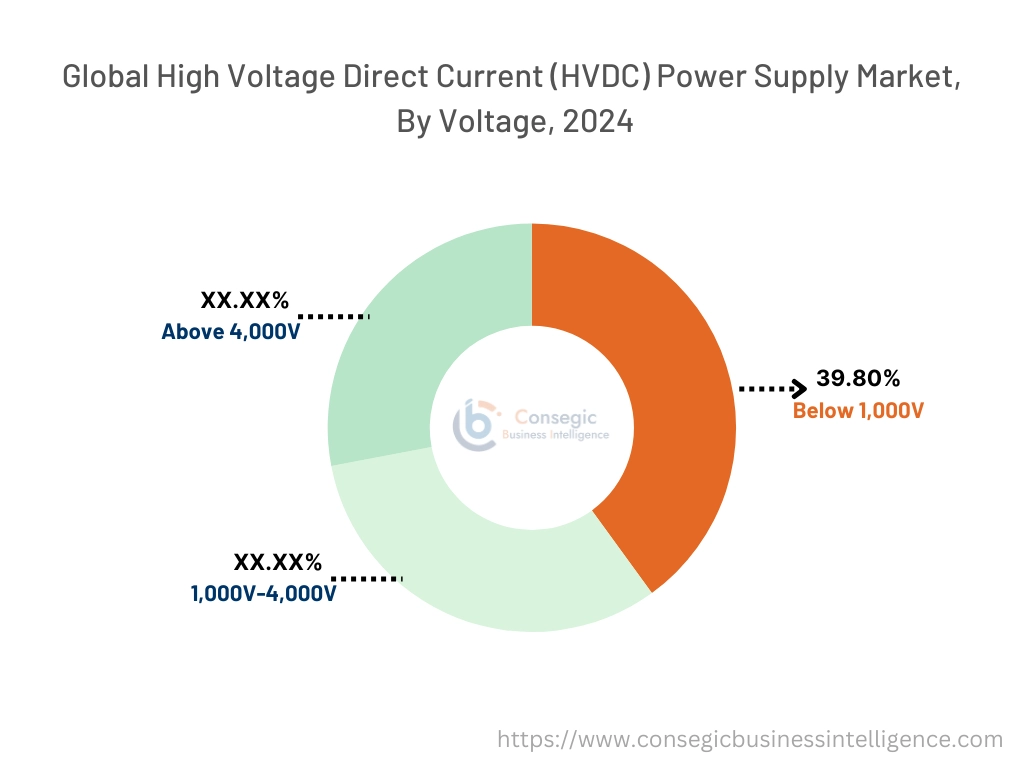

By Voltage:

Based on voltage, the High Voltage Direct Current (HVDC) power supply market is segmented into three categories: below 1,000V, 1,000V-4,000V, and above 4,000V.

The below 1,000V sector accounted for the largest revenue in high voltage direct current (HVDC) power supply market share by 39.80% in 2024.

- This voltage range is widely used for short-distance transmission and in applications that require moderate power supply.

- The below 1,000V HVDC systems are cost-effective and suitable for industrial, residential, and telecommunication infrastructure.

- These systems provide stable and reliable power transmission in urban areas and smaller industrial setups.

- The increasing high voltage direct current (HVDC) power supply market trend for power in dense urban areas and small-scale renewable energy systems has contributed to the prominence of this voltage segment.

- Furthermore, their ability to reduce energy loss and improve efficiency in long-distance power transmission enhances the high voltage direct current (HVDC) power supply market trend.

- The below 1,000V sector is crucial for stable power distribution, especially in areas where high-voltage transmission systems are impractical.

- Therefore, according to high voltage direct current (HVDC) power supply market analysis, the below 1,000V voltage segment is a key player in the HVDC power supply market, thanks to its widespread application in urban and small-scale industries and its role in maintaining energy efficiency.

The 1,000V-4,000V sector is anticipated to register the fastest CAGR during the forecast period.

- This voltage range is commonly used in medium-distance transmission, typically for industrial plants and telecommunication networks.

- Its flexibility in handling moderate power supply needs, combined with cost efficiency, makes it an attractive option for expanding industrial applications.

- The segment is poised to grow due to increasing industrialization, technological advancements, and the rising adoption of renewable energy systems.

- HVDC systems in this voltage range help enhance the integration of wind and solar energy by minimizing transmission losses.

- As industries strive for more sustainable energy solutions, the trend for 1,000V - 4,000V HVDC systems is expected to increase significantly.

- Thus, according to high voltage direct current (HVDC) power supply market analysis, with the growing industrial and renewable energy demands, the 1,000V-4,000V segment is expected to experience robust growth, driven by its scalability and efficiency in medium-distance power supply.

By Application:

Based on application, the HVDC power supply market is segmented into industrial, oil & gas, telecommunication, medical, and others.

The industrial sector accounted for the largest revenue in high voltage direct current (HVDC) power supply market share in 2024.

- HVDC systems in industrial applications are used for providing stable and uninterrupted power to manufacturing plants, data centers, and heavy industries.

- These systems help reduce transmission losses, improve operational efficiency, and ensure a reliable power supply for continuous industrial processes.

- The growing industrial automation and the need for high-performance machinery contribute to the increasing trend for HVDC systems in this sector.

- HVDC systems also facilitate the integration of renewable energy sources in industrial plants, supporting sustainability goals.

- Furthermore, industrial sectors benefit from the enhanced stability and control provided by HVDC power supply systems.

- Therefore, according to the market analysis, the industrial application segment dominates the HVDC power supply market, driven by its need for reliable, efficient, and sustainable power solutions.

The telecommunication sector is anticipated to register the fastest CAGR during the forecast period.

- HVDC systems are increasingly used in telecommunications to ensure stable power supply for network infrastructure, including data centers and base stations.

- As the global trend for data services grows, the need for efficient and uninterrupted power becomes critical in telecommunication systems.

- HVDC systems help telecom providers reduce energy losses and manage large-scale infrastructure with greater efficiency.

- The continuous growth in 5G network installations and high-speed data transmission requirements will further fuel the high voltage direct current (HVDC) power supply market demand for HVDC solutions in the telecommunication industry.

- Moreover, as telecom companies strive for sustainability, HVDC offers an environmentally friendly alternative to traditional power supply methods.

- Thus, according to the market analysis, the telecommunication segment is expected to witness rapid growth as the trend for high-capacity and reliable power systems increases with advancements in telecommunications technology.

By Technology:

Based on technology, the market is segmented into Line Commutated Converters (LCC), Voltage Source Converters (VSC), and Capacitor Commutated Converters (CCC).

The Line Commutated Converters (LCC) sector accounted for the largest revenue share in 2024.

- LCC technology is widely used for high-capacity, long-distance power transmission, especially for large-scale applications like interconnecting power grids.

- LCCs are known for their reliability, cost-effectiveness, and high efficiency in transmitting power over vast distances.

- Their widespread use in high-voltage direct current transmission projects, especially in regions with large energy needs, makes them a dominant player in the market.

- Additionally, LCCs are well-suited for integrating renewable energy sources into the power grid, further boosting their adoption.

- The sector benefits from the large infrastructure projects worldwide, particularly in renewable energy integration.

- Therefore, according to the market analysis, the LCC technology segment remains the market leader due to its proven reliability, cost-effectiveness, and high performance in long-distance and large-scale applications.

The Voltage Source Converters (VSC) sector is anticipated to register the fastest CAGR during the forecast period.

- VSC technology is gaining traction due to its ability to provide flexible and efficient power transmission over medium distances, making it ideal for urban and offshore wind power connections.

- VSCs enable the use of underground and underwater HVDC lines, offering more versatility in terms of infrastructure deployment.

- This technology also allows for more stable and reliable integration of renewable energy sources such as wind and solar power.

- VSC technology is increasingly used in grid interconnections and back-to-back HVDC links, where its ability to offer quick response times is highly valued.

- The growing need for sustainable energy solutions and more flexible power transmission systems will drive the growth of this sector.

- Thus, according to the market analysis, as the trend for flexible, efficient, and renewable energy integration grows, the VSC segment is set to experience rapid growth, offering a promising future for HVDC technology.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

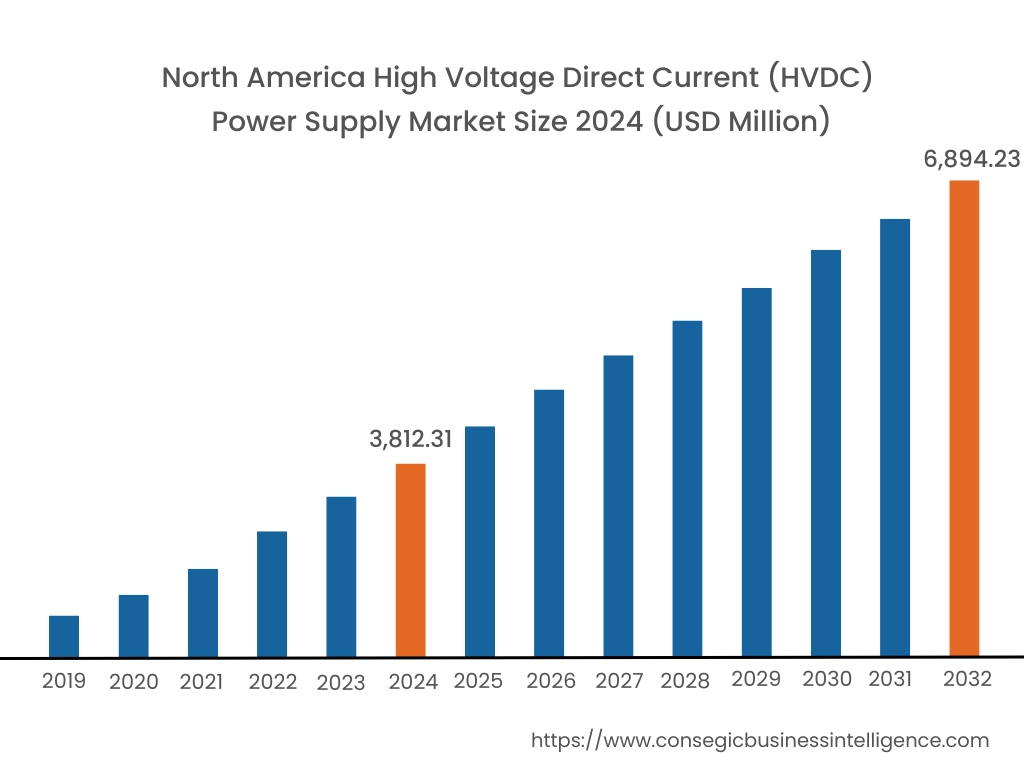

In 2024, North America was valued at USD 3,812.31 Million and is expected to reach USD 6,894.23 Million in 2032. In North America, the U.S. accounted for the highest share of 75.05% during the base year of 2024. In North America, the HVDC power supply market is expanding due to increasing investments in renewable energy integration and power transmission infrastructure. The United States leads in HVDC projects, focusing on enhancing grid stability and improving energy efficiency. The adoption of HVDC technology is further supported by the aging power grid infrastructure and the need for long-distance power transmission. The government's push for clean energy solutions also bolsters high voltage direct current (HVDC) power supply market demand, as HVDC systems facilitate the integration of renewable energy sources.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 8.5% over the forecast period. Asia-Pacific is a key region for HVDC power supply systems, with significant market activity driven by the rapid expansion of power generation and transmission networks. China is a major player, with large-scale HVDC projects focusing on long-distance transmission from remote renewable energy sources. India and other Southeast Asian countries are also investing in HVDC infrastructure to support urbanization, industrialization, and the growing demand for reliable power. The region’s commitment to energy transition initiatives and grid modernization further supports HVDC market development.

Europe’s HVDC power supply market remains strong, driven by the region’s focus on renewable energy integration and cross-border electricity transmission. Countries like Germany, Sweden, and the United Kingdom are leading the implementation of HVDC technology to connect offshore wind farms and stabilize the grid. Europe’s ambitious green energy targets and the European Union's commitment to reducing carbon emissions contribute to the growing adoption of HVDC systems. Additionally, Europe’s well-developed infrastructure and strong regulatory support create a favorable environment for HVDC growth.

The Middle East and Africa region is experiencing a steady increase in HVDC power supply system demand, fueled by expanding energy infrastructure and a focus on renewable energy. Countries like the UAE and Saudi Arabia are investing in HVDC technology to enhance energy distribution efficiency and support large-scale solar and wind energy projects. Additionally, the region's increasing energy demand and the need for reliable power distribution networks contribute to the adoption of HVDC systems. However, economic fluctuations and political instability may pose challenges to high voltage direct current (HVDC) power supply market growth in certain areas.

In Latin America, the HVDC power supply market is in its early stages but is gaining traction, especially in countries like Brazil and Argentina. The rising demand for electricity, coupled with the need to modernize aging infrastructure, supports the adoption of HVDC technology. Moreover, large-scale renewable energy projects in the region, particularly in Brazil, are increasing the need for efficient long-distance power transmission. Despite these factors, challenges such as budget constraints and the need for regulatory clarity may slow market development in some areas.

Top Key Players & Market Share Insights:

The Global High Voltage Direct Current (HVDC) Power Supply Market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the Global High Voltage Direct Current (HVDC) Power Supply Market. Key players in the High Voltage Direct Current (HVDC) Power Supply industry include-

- Siemens AG (Germany)

- ABB Ltd. (Switzerland)

- Hyosung Heavy Industries (South Korea)

- Power Grid Corporation of India Limited (PGCIL) (India)

- Dongfang Electric Corporation (China)

- General Electric (GE) (United States)

- Schneider Electric (France)

- Mitsubishi Electric Corporation (Japan)

- Hitachi Ltd. (Japan)

- Toshiba Corporation (Japan)

Recent Industry Developments :

Partnerships & Collaborations:

- In January 2025, GE Vernova and 50Hertz joined forces for the Ostwind 4 renewable energy project. GE Vernova's role in the partnership is to supply essential HVDC technology. Ostwind 4 is a significant infrastructure project aimed at strengthening Germany's grid and accelerating the energy transition. The initiative combines advanced technology, strategic procurement, and shared expertise to enhance the country's power transmission capabilities.

- In December 2024, Hitachi Energy and Samsung C&T expanded their strategic collaboration to advance HVDC projects globally. This non-exclusive partnership leverages the growing demand for electrification and clean energy solutions. Hitachi Energy provides its advanced HVDC technology, while Samsung C&T contributes its engineering, procurement, and construction (EPC) expertise. The collaboration focuses on key regions, including the Middle East, Southeast Asia, and South Korea.

- In August 2023, Southwire entered into a partnership with NKT to supply underground cables for the Champlain Hudson Power Express (CHPE) project. This project involves delivering clean, renewable hydroelectricity via a 339-mile fully buried HVDC transmission system using a combination of submarine and underground cables. Southwire serves as the turnkey cable system provider, combining its manufacturing expertise with NKT's HVDC cable system technology and design.

Industry Development:

- In January 2025, a £2 billion factory is set to be developed in North Ayrshire, Scotland, on a former coal-handling port site. This facility will manufacture subsea cables for renewable energy transmission, focusing on high-voltage direct current (HVDC) cables. The project aims to stimulate growth in one of Scotland's most deprived regions and build local supply chain capacity for floating offshore wind projects. The initiative is co-funded by the Scottish National Investment Bank (SNIB) and is expected to create 900 long-term jobs.

Mergers and Acquisitions:

- In January 2025, Prysmian, a Milan-based provider of undersea infrastructure, is planning a dual listing in New York and focusing on further U.S. acquisitions to build on its rapid expansion. This follows the $4 billion acquisition of Texas-based Encore Wire in the previous year. Prysmian is targeting expansion in the U.S., particularly seeking acquisitions in the telecoms sector to enhance its data center capabilities.

- In December 2024, ABB agreed to acquire the power electronics unit of Gamesa Electric from Siemens Gamesa. This acquisition aims to strengthen ABB's position in the renewable power conversion technology market. The transaction is expected to close in the second half of 2025, with financial terms not disclosed. The deal will add over 100 specialized engineers and converter factories in Madrid and Valencia to ABB's workforce, extending its presence to include employees in India, China, the United States, and Australia.

High Voltage Direct Current (HVDC) Power Supply Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 21,271.92 Million |

| CAGR (2025-2032) | 8.0% |

| By Voltage |

|

| By Application |

|

| By Technology |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the High Voltage Direct Current (HVDC) Power Supply Market? +

In 2024, the High Voltage Direct Current (HVDC) Power Supply Market was USD 11,492.95 million.

What will be the potential market valuation for the High Voltage Direct Current (HVDC) Power Supply Market by 2032? +

In 2032, the market size of High Voltage Direct Current (HVDC) Power Supply Market is expected to reach USD 21,271.92 million.

What are the segments covered in the High Voltage Direct Current (HVDC) Power Supply Market report? +

The voltage, application, and technology are the segments covered in this report.

Who are the major players in the High Voltage Direct Current (HVDC) Power Supply Market? +

Siemens AG (Germany), ABB Ltd. (Switzerland), General Electric (GE) (United States), Schneider Electric (France), Mitsubishi Electric Corporation (Japan), Hitachi Ltd. (Japan), Toshiba Corporation (Japan), Hyosung Heavy Industries (South Korea), Power Grid Corporation of India Limited (PGCIL) (India), Dongfang Electric Corporation (China) are the major players in the High Voltage Direct Current (HVDC) Power Supply market.