- Summary

- Table Of Content

- Methodology

High Purity Alumina Market Size:

High Purity Alumina Market size is estimated to reach over USD 28.77 Billion by 2032 from a value of USD 3.68 Billion in 2024 and is projected to grow by USD 4.70 Billion in 2025, growing at a CAGR of 29.3% from 2025 to 2032.

High Purity Alumina Market Scope & Overview:

The high purity alumina (HPA) focuses on the production and application of alumina with a purity level of 99.99% or higher. HPA is a critical material in industries requiring exceptional thermal, electrical, and chemical stability. It is widely used in manufacturing LED substrates, lithium-ion battery separators, sapphire glass, and optical lenses. Key types of HPA include 4N (99.99%), 5N (99.999%), and 6N (99.9999%) purity grades, each tailored to specific high-performance applications.

Key characteristics of high purity alumina include superior corrosion resistance, excellent hardness, and high thermal conductivity. The benefits include improved product performance, extended lifespan, and enhanced efficiency in advanced manufacturing processes.

Applications span across several industries including electronics (LEDs and semiconductors), automotive (battery components), and aerospace (optical and structural materials). End-users include LED manufacturers, battery producers, and specialty glass developers, driven by increasing demand for energy-efficient lighting solutions, advancements in electric vehicle technologies, and the growing use of high-performance materials in industrial and consumer applications.

High Purity Alumina Market Dynamics - (DRO) :

Key Drivers:

Rising Demand for LED Applications and Advanced Electronics is Boosting the Market

The increasing adoption of light-emitting diodes (LEDs) in various industries is a primary driver of the high purity alumina (HPA) market. HPA, known for its exceptional thermal stability, corrosion resistance, and optical clarity, is a critical material used in the production of sapphire substrates for LEDs. With the global push for energy efficiency and the phasing out of traditional incandescent lighting, LEDs have gained significant traction in residential, commercial, and industrial applications. The expanding demand for HPA in advanced electronics, such as semiconductors, lithium-ion batteries, and optical lenses, further drives high purity alumina market growth. The transition toward 5G technology and the increasing adoption of electric vehicles (EVs) have also created new avenues for HPA usage in ceramic separators for lithium-ion batteries, ensuring their safety and performance.

Key Restraints:

High Production Costs and Environmental Concerns is Hampering the Market

The high production cost is a significant barrier to high purity alumina market growth. The manufacturing process for HPA, particularly the hydrolysis of aluminum alkoxide or acid leaching of kaolin, involves energy-intensive steps, leading to elevated production costs. Additionally, the reliance on premium raw materials, such as high-grade aluminum or kaolin, further contributes to cost challenges. Environmental concerns associated with HPA production, including high energy consumption and the generation of industrial waste, have also attracted regulatory scrutiny, compelling manufacturers to adopt more sustainable and cost-effective processes. These factors limit the accessibility of HPA in cost-sensitive regions and restrict its broader adoption.

Future Opportunities :

Advancements in Sustainable Production Technologies are Increasing Prevalence in the Market

The development of sustainable and cost-efficient production technologies presents significant rising opportunities for the HPA market. Manufacturers are increasingly adopting alternative production methods, such as the use of recycled aluminum or innovative processes like the plasma synthesis method, to reduce energy consumption and production costs. Additionally, the rising focus on green manufacturing has encouraged the use of renewable energy sources in HPA production facilities, aligning with global sustainability goals. The rising expansion of high-purity alumina market trends in emerging applications, such as next-generation displays (OLEDs and micro-LEDs) and solid-state batteries, also provides significant developing potential. Companies investing in R&D to develop high-quality, environmentally friendly HPA solutions are well-positioned to capture opportunities in these high-growing sectors.

These dynamics highlight the increasing importance of HPA in advanced technologies, particularly in LEDs and EVs. While production costs and environmental challenges persist, innovations in sustainable production and expanding applications in cutting-edge technologies present promising avenues for market trends and innovation.

High Purity Alumina Market Segmental Analysis :

By Purity Level:

Based on purity level, the market is segmented into 4N (99.99%), 5N (99.999%), and 6N (99.9999%).

The 4N segment accounted for the largest revenue of high purity alumina market share in 2024.

- 4N purity alumina is widely used in applications such as LEDs, lithium-ion batteries, and sapphire substrates due to its cost-effectiveness and performance reliability.

- Increasing adoption in mass-market applications like phosphor coatings and industrial ceramics supports its dominance.

- Growing trends from the electronics industry for high-quality materials in display and lighting applications further propels the market as highlighted in this segmental analysis.

- Advancements in manufacturing processes for 4N alumina enhance scalability and affordability.

The 5N segment is anticipated to register the fastest CAGR during the forecast period.

- 5N purity alumina is gaining traction for high-end applications in semiconductors, medical devices, and optical lenses due to its superior purity and performance characteristics.

- Increasing use in advanced sapphire substrates for high-performance electronics drives trends.

- Rising high purity alumina market demand for next-generation LED technologies, where higher purity alumina is critical, supports growth in this segment.

- Technological advancements enabling cost-effective production of 5N alumina boost its market potential.

By Product Type:

Based on product type, the market is segmented into powder, pellets, and granules.

The powder segment accounted for the largest revenue share in 2024.

- Powdered high purity alumina is extensively used in the production of LEDs, phosphors, and lithium-ion batteries due to its fine particle size and superior dispersion properties.

- Increasing high purity alumina market demand for powdered alumina in advanced ceramics and optical applications supports its dominance.

- Growing R&D activities in developing nano-powdered alumina for enhanced material performance to propel market trends.

- Rising adoption of sapphire substrates and thin-film applications contributes to this segment's prominence.

The pellets segment is anticipated to register the fastest CAGR during the forecast period.

- Pellets are increasingly used in high-precision manufacturing processes such as semiconductor production and high-performance optical lenses.

- Their ease of handling, consistent composition, and minimal wastage make them ideal for advanced industrial applications.

- Expanding use of alumina pellets in aerospace and defense sectors for critical component manufacturing supports trends in the market.

- Technological innovations in pelletizing processes enhance quality and reduce production costs, boosting demand.

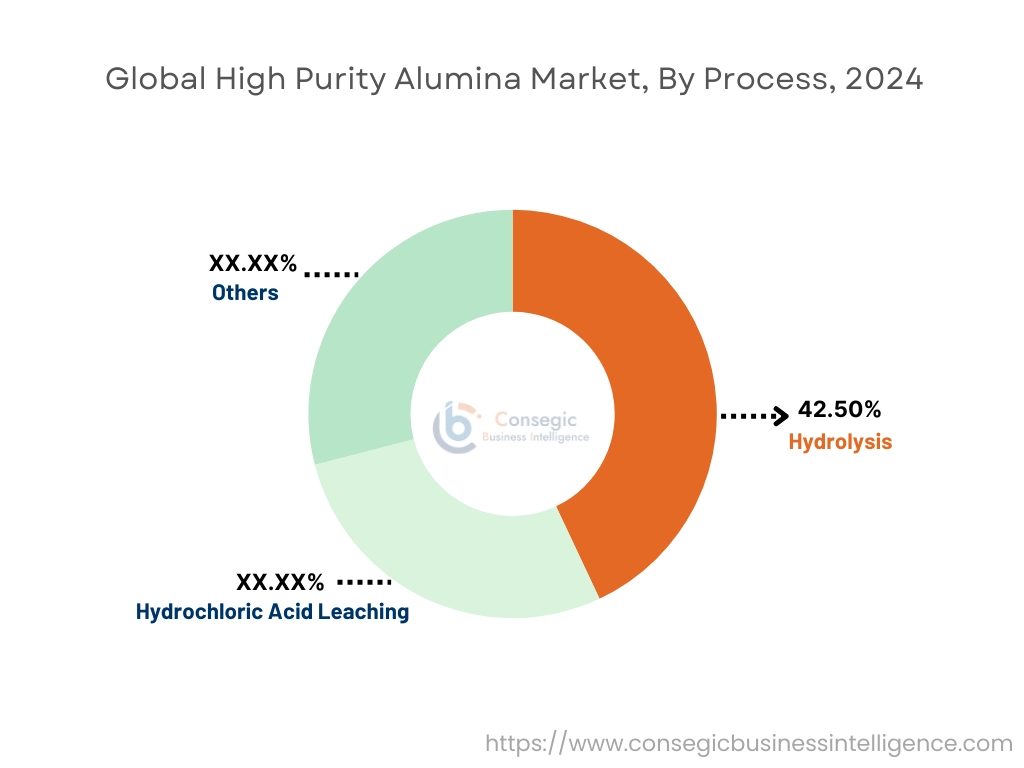

By Process:

Based on the process, the market is segmented into hydrolysis, hydrochloric acid leaching, and others.

The hydrolysis segment accounted for the largest revenue of high purity alumina market share of 42.50% in 2024.

- Hydrolysis is the most commonly used method for producing high purity alumina due to its cost-effectiveness and scalability.

- Increasing adoption of hydrolysis in manufacturing 4N and 5N alumina supports its dominance in the market.

- Rising focus on environmentally friendly and efficient production methods drives technological advancements in hydrolysis.

- The widespread availability of aluminum alkoxide feedstock enhances the adoption of this technology.

The hydrochloric acid leaching segment is anticipated to register the fastest CAGR during the forecast period.

- Hydrochloric acid leaching enables the production of ultra-high-purity alumina (6N) for advanced applications in semiconductors and optics.

- Increasing advancement for 6N alumina in high-performance electronics and aerospace applications supports growth in this segment.

- Advancements in leaching processes, improving yield, and reducing waste, enhance its market potential.

- Expanding R&D activities focused on cost reduction and process optimization further drive this segment.

By Application:

Based on application, the market is segmented into LEDs, semiconductors, phosphor applications, sapphire substrates, lithium-ion batteries, optical lenses, medical devices, and others.

The LEDs segment accounted for the largest revenue share in 2024.

- High purity alumina is a critical material for phosphor coatings in LEDs, enhancing brightness, energy efficiency, and durability.

- Increasing high purity alumina market opportunities for energy-efficient lighting solutions globally supports the growth of the LED segment.

- Growing adoption of LED technology in residential, commercial, and industrial sectors propels alumina consumption.

- Government initiatives promoting energy-efficient technologies further boost demand for HPA in LED applications.

The sapphire substrates segment is anticipated to register the fastest CAGR during the forecast period.

- Sapphire substrates, made using high purity alumina, are essential for advanced electronic devices and high-performance LEDs.

- Increasing demand for sapphire-based components in semiconductors and wearables drives rapid trends in the market.

- Expanding production of high-end consumer electronics requiring sapphire substrates supports this segment.

- Rising focus on durable and scratch-resistant materials in optical and display technologies propels market growth.

By End-User Industry:

Based on the end-user industry, the market is segmented into electronics, energy and power industry, aerospace & defense, automotive, healthcare, and industrial manufacturing.

The electronics segment accounted for the largest revenue share in 2024.

- High purity alumina is widely used in the electronics industry for applications such as semiconductors, LEDs, and display technologies.

- Increasing production of smartphones, tablets, and advanced displays drives high purity alumina market trends in this segment.

- Rising adoption of high-performance materials in microelectronics and wearables supports market dominance.

- Advancements in nanotechnology and material science further expand HPA applications in electronics.

The energy storage segment is anticipated to register the fastest CAGR during the forecast period.

- Lithium-ion batteries, which use HPA as a separator coating material, are in high demand due to the growing adoption of electric vehicles (EVs).

- Expanding investments in renewable energy projects and energy storage systems boost HPA usage.

- Increasing production of EVs and consumer electronics requiring long-lasting and efficient batteries drives surge.

- Advancements in battery technologies focused on enhancing safety and performance support high purity alumina market expansion.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

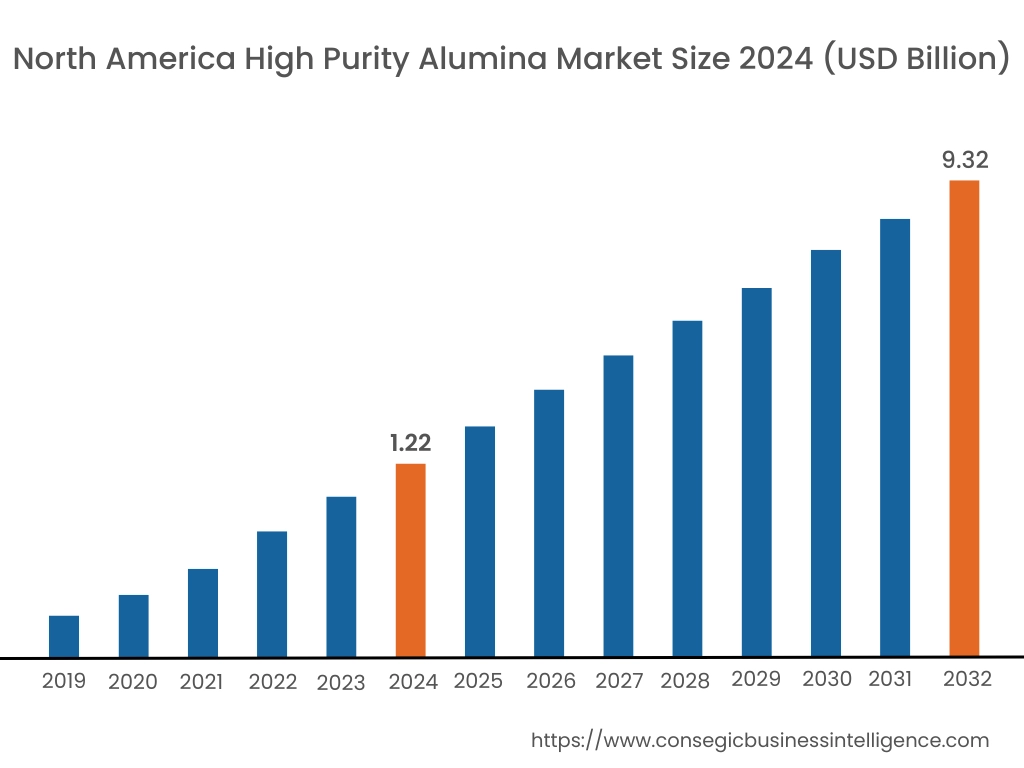

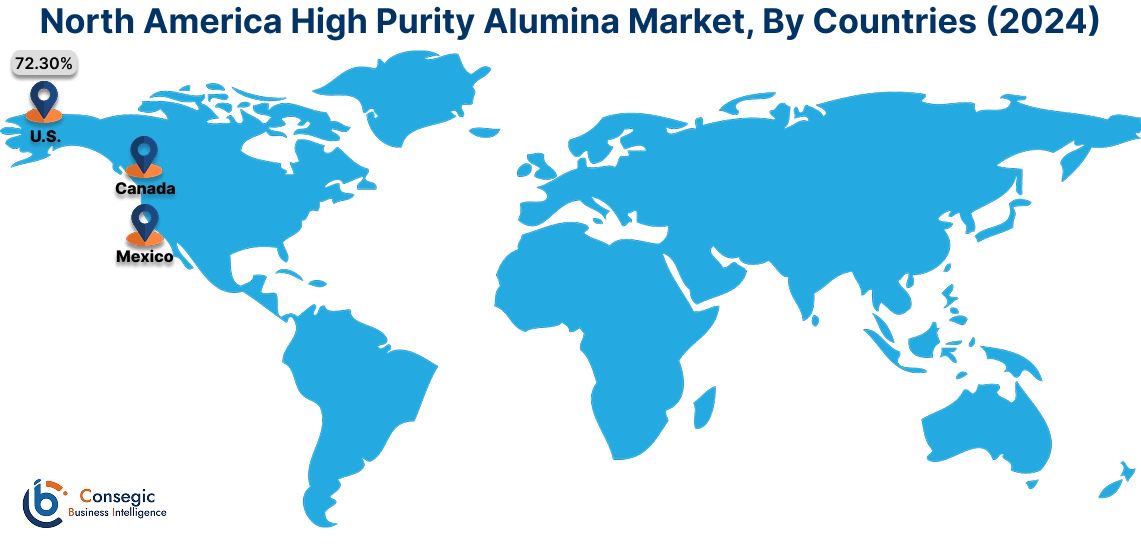

In 2024, North America was valued at USD 1.22 Billion and is expected to reach USD 9.32 Billion in 2032. In North America, the U.S. accounted for the highest share of 72.30% during the base year of 2024. North America holds a significant share in the high purity alumina market, driven by increasing demand from the LED and electronics industries. The U.S. leads the region with substantial investments in advanced manufacturing technologies, particularly for high-performance semiconductors and lithium-ion battery separators. Canada contributes with its focus on sustainable and efficient production methods, aligning with its stringent environmental policies. Analysis highlights the rising adoption of HPA in automotive applications, especially in electric vehicles, further propelling market hikes across the region.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 29.8% over the forecast period. Asia-Pacific is the fastest-growing region in the alumina market, which is fueled by rapid industrialization, expanding electronics manufacturing, and growing adoption of LEDs in China, Japan, and South Korea. China dominates the region with large-scale production of LEDs and lithium-ion batteries, supported by government-led initiatives to promote energy-efficient technologies. Japan focuses on high-grade HPA for advanced applications in optics and electronics, leveraging its strong R&D capabilities. South Korea emphasizes the use of HPA in battery separators for electric vehicles, aligning with its leadership in EV and battery technologies. The high purity alumina market analysis suggests that the availability of cost-effective raw materials and rising domestic consumption contribute significantly to regional market expansion.

Europe is a prominent market for high purity alumina, supported by stringent environmental regulations, advancements in green technologies, and increasing adoption of energy-efficient LEDs. Countries like Germany, France, and the UK are key contributors. Germany drives progress with its robust automotive and electronics sectors, focusing on the use of HPA in battery technologies for electric vehicles. The UK emphasizes its application in the production of high-quality sapphire substrates for LEDs, while France promotes R&D initiatives to enhance HPA production processes. Analysis indicates that the regional market benefits from a strong push toward sustainable manufacturing and renewable energy applications.

The Middle East & Africa region is witnessing steady growth in the global high-purity alumina market, driven by increasing investments in renewable energy projects and growing advancement for LEDs. Countries like Saudi Arabia and the UAE are adopting energy-efficient lighting solutions as part of their sustainability initiatives, boosting the need for HPA. In Africa, South Africa is emerging as a key market, focusing on the adoption of HPA in industrial and energy applications. Regional high purity alumina market analysis highlights challenges such as limited local production facilities and reliance on imports, which can affect pricing and availability.

Latin America is an emerging market for high-purity alumina, with Brazil and Mexico leading the region. Brazil’s growing focus on renewable energy and advanced industrial applications supports the high purity alumina market trends, particularly in solar panels and LEDs. Mexico emphasizes the use of HPA in electronics manufacturing, benefiting from its proximity to North American markets and global supply chains. Analysis indicates that increasing government initiatives to adopt energy-efficient technologies and develop local production capabilities are key factors driving regional high-purity alumina market expansion, despite economic instability in smaller countries.

Top Key Players & Market Share Insights:

The high purity alumina market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global high purity alumina market. Key players in the high purity alumina industry include -

- Alcoa Corporation (USA)

- Sumitomo Chemical Co., Ltd. (Japan)

- Xinfa Group (China)

- Altech Chemicals Ltd. (Australia)

- Bosai Minerals Group Co., Ltd. (China)

- Sibelco Group (Belgium)

- FYI Resources Ltd. (Australia)

- Auer Lighting (Germany)

- China Northern Rare Earth Group High-Tech Co., Ltd. (China)

- Norsk Hydro ASA (Norway)

Recent Industry Developments :

Innovations:

- In 2024, Sumitomo Chemical advanced its high purity alumina (HPA) production by refining its aluminum alkoxide hydrolysis method. The company improved production conditions to create ultra-fine and uniform particles, addressing the increasing demand for industries like displays, energy, and semiconductors. By enhancing particle control and developing a chemical vapor deposition method, Sumitomo produced high-quality single crystal α-Al2O3 particles. This innovation supports applications such as high-pressure sodium lamps and magnetic tapes, positioning Sumitomo to meet the growing demand for eco-friendly, high-performance materials in advanced technologies.

High Purity Alumina Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 28.77 Billion |

| CAGR (2025-2032) | 29.3% |

| By Purity Level |

|

| By Product Type |

|

| By Process |

|

| By Application |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the High Purity Alumina (HPA) Market? +

High Purity Alumina Market size is estimated to reach over USD 28.77 Billion by 2032 from a value of USD 3.68 Billion in 2024 and is projected to grow by USD 4.70 Billion in 2025, growing at a CAGR of 29.3% from 2025 to 2032.

What are the key drivers of the High Purity Alumina Market? +

The market is driven by rising demand for LED applications, advancements in lithium-ion battery technologies, and the increasing adoption of HPA in high-performance electronics. The shift towards 5G infrastructure and electric vehicles (EVs) is further boosting demand for HPA.

Which industries use High Purity Alumina the most? +

HPA is widely used in electronics, energy and power, aerospace & defense, automotive, healthcare, and industrial manufacturing. Major applications include LED lighting, sapphire substrates for semiconductors, and lithium-ion battery components.

What are the challenges in the High Purity Alumina Market? +

High production costs and environmental concerns are key challenges. The energy-intensive manufacturing processes and reliance on premium raw materials increase costs. Additionally, sustainability concerns have led to regulatory scrutiny, pushing manufacturers towards greener production methods.