- Summary

- Table Of Content

- Methodology

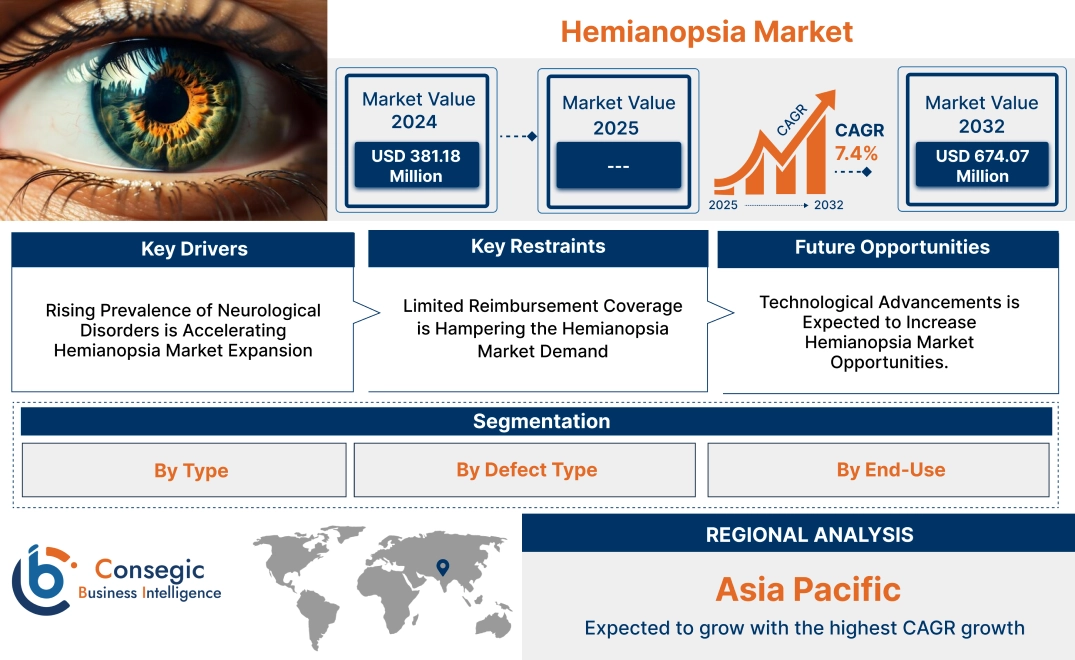

Hemianopsia Market Size:

Hemianopsia Market size is growing with a CAGR of 7.4% during the forecast period (2025-2032), and the market is projected to be valued at USD 674.07 Million by 2032 from USD 381.18 Million in 2024.

Hemianopsia Market Scope & Overview:

Hemianopsia is a condition where a person loses half of their visual field in one or both eyes. It is not an eye disease, but it results from damage to the brain’s visual pathways. This defect has various causes such as strokes being the leading cause, traumatic brain injuries, brain tumors, infections such as meningitis, or degenerative neurological diseases. The condition is categorized into two main types. In homonymous, the same side of visual field is lost in both eyes, and in heteronymous, the opposite side of visual field is lost.

The condition leads to symptoms such as difficulty in seeing objects or people on one side, frequent collisions with obstacles, challenges with reading, and disorientation. All these factors negatively affect individuals’ mobility and independence, impacting overall quality of life. The treatment options for this condition include vision restoration therapy, and vision field expanding devices which help patients adapt their daily activities.

Hemianopsia Market Dynamics - (DRO) :

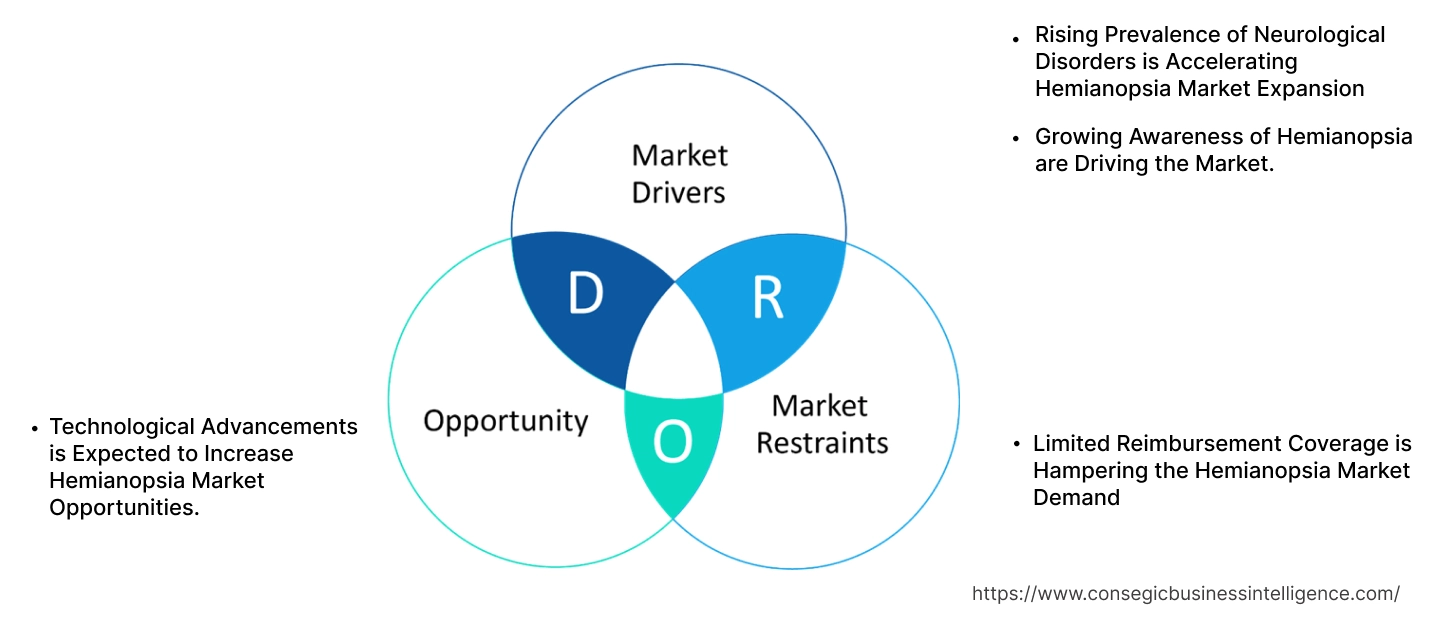

Key Drivers:

Rising Prevalence of Neurological Disorders is Accelerating Hemianopsia Market Expansion

Stroke, a leading cause of disability, frequently damages brain regions responsible for visual processing, leading to vision loss. Similarly, brain tumors, depending on their location and mass exert pressure on critical visual pathways, resulting in vision loss. Additionally, traumatic brain injuries from accidents also disrupt neural connections, which leads to visual field deficits. The rising prevalence of these disorders has led to an increase in cases of vision loss in half of the visual field.

For instance,

- According to an article published by the Eyewire+, in 2024, an average of 500,000 to 1 million individuals in U.S. are affected by this vision loss condition. These incidences have led to a need for diagnostic and treatment solutions, positively influencing hemianopsia market trends.

Overall, the rising prevalence of neurological disorders is significantly boosting the hemianopsia market expansion.

Growing Awareness of Hemianopsia are Driving the Market.

Many individuals with this vision loss remain undiagnosed or unaware of available therapies. Educational campaigns and initiatives by healthcare organizations and non-profits are helping patients and caregivers understand the conditions and seek appropriate treatments. Advancements in communication platforms, including social media, and digital healthcare tools have made it easier to disseminate information about this condition.

For instance,

- In 2023, Emianopsia published an article providing information on what is hemianopsia, its key symptoms, risk factors, underlying causes, diagnostic methods, and potential treatment options available. This has increased visits regarding this vision loss condition, positively influencing hemianopsia market trends.

Thus, growing awareness of this vision loss condition is accelerating the global hemianopsia market growth.

Key Restraints:

Limited Reimbursement Coverage is Hampering the Hemianopsia Market Demand

Many treatments for this condition are expensive for patients without adequate financial support. For example, vision loss therapy (VRT) and similar neuroplasticity-based treatments fall outside of traditional insurance plans. This is due to insufficient clinical evidence or regulatory approval in some countries. Moreover, these insurance plans do not cover the costs for assistive technology, or low-visions aids.

The high financial cost affects patients in low and middle-income countries where expenses dominate healthcare spending. Additionally, the lack of reimbursement reduces patient access to necessary treatments. It also discourages healthcare industry providers from adopting advanced therapies. As a result, it slows down the development of innovative solutions in the market. Henceforth, limited reimbursement coverage is hampering the hemianopsia market demand.

Future Opportunities :

Technological Advancements is Expected to Increase Hemianopsia Market Opportunities.

Innovative diagnostic tools are a significant potential factor that is expected to drive in the forecast period. A few of the innovative diagnostic tools are optical coherence tomography (OCT), magnetic resonance imaging (MRI), amongst others. These have led to enhancement of accuracy and speed of detecting the vision defect. Additionally, there is the development of advanced prism glasses and field expanding devices to help patients regain their mobility and independence more effectively.

For instance,

- Ocutech, Inc., in 2024, announced the launch of its limited ultrasonic sensor device SideSight. This device will help patients with vision loss walk safely without any obstacles. These innovative launches will improve patient outcomes, creating potential for market growth.

Overall, advancements in diagnostic tools and development of innovative technologies to improve patient outcomes are expected to increase hemianopsia market opportunities.

Hemianopsia Market Segmental Analysis :

By Type:

Based on type, the market is categorized into diagnosis and treatment.

Trends in Type:

- AI algorithms are being integrated into imaging systems (MRI, CT) to improve accuracy and speed of detection.

- Emerging therapies like brain stimulation techniques (e.g., transcranial magnetic stimulation) are being explored for potential benefits in treatment.

The treatment segment accounted for the largest market share in 2024 and is expected to grow at the fastest CAGR over the forecast period.

- The treatment dominates the market due to the significant focus on improving patients’ quality of life and restoring visual function.

- Treatment options, including vision restoration therapy. This helps the brain adapt to vision loss and improves visual scanning and attention.

- Devices such as screen readers and specialized computer programs enhance accessibility and independence. Visual aids such as prism glasses help expand the visual field.

- Increased reimbursement coverage for vision rehabilitation services or devices is driving the segment.

- For instance, Ocutech, Inc., in 2025, announced a Medicare coverage for its assistive mobility device designed to help patients with hemianopsia.

- Overall, as per the market analysis, expanding reimbursement coverage is driving a segment in hemianopsia market growth.

By Defect Type:

Based on defect type, the market is categorized into homonymous and heteronymous.

Trends in the Defect Type:

- Increased focus on understanding the underlying causes of homonymous forms of vision loss.

- Emerging research on the potential for neurorehabilitation to improve visual function in both homonymous and heteronymous vision loss types.

The homonymous segment accounted for the largest market share in 2024.

- Homonymous type is a condition where a person loses the same side of visual field in both eyes. It typically results from damage to the brains pathways, caused by neurological disease.

- The impact of this condition on daily life activities is substantial. It affects activities such as reading, driving, and others. This in turn is driving the demand for effective treatment and support service.

- Additionally, there is a growing prevalence of strokes, leading to an increase in number of vision loss cases in half of the visual field.

- For instance, according to global stroke statistics, in 2021, there are 93.8 million stroke survivors and 1.9 million new stroke cases were reported worldwide. Homonymous type of vision loss affects 20–57% of stroke victims.

- Overall, as per the market analysis, the high prevalence of strokes, resulting in homonymous type of vision loss, is driving the segmental growth in the hemianopsia industry.

The heteronymous segment is expected to grow at the fastest CAGR over the forecast period.

- Heteronymous is a type of visual impairment where a person loses opposite visual fields in both eyes. This condition typically affects the peripheral vision, with the loss occurring in the nasal field of one eye and the temporal field of the other.

- The condition is emerging as a growing concern due to the increasing incidence of pituitary tumors and other conditions that affect the optic chiasm.

- Pituitary tumors, though rare, are becoming more frequently diagnosed, due to advances in medical imaging and improved awareness.

- As medical technology improves, more people are being diagnosed with tumors that affect the optic chiasm, leading to heteronymous types of vision loss.

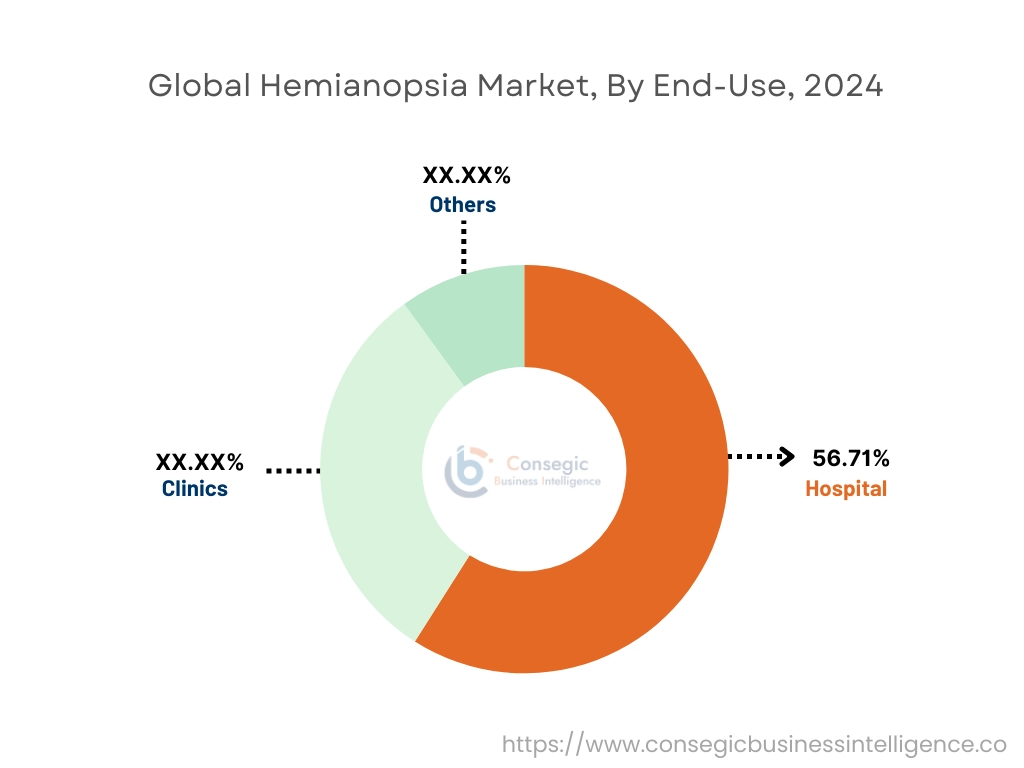

By End Use:

Based on end-use, the market is categorized into hospitals, clinics and others.

Trends in End-Use:

- Growing role of home healthcare providers in delivering vision rehabilitation services.

- Increased collaboration between hospitals, clinics, and community-based organizations.

The hospitals segment accounted for the largest market share of 56.71% in 2024

- Hospitals are equipped with state-of-the-art imaging technologies such as MRI, CT scans, and optical coherence tomography (OCT). These technologies are crucial for accurately diagnosing vision loss and identifying its causes, such as strokes, tumors, or brain injuries.

- Additionally, hospitals have multidisciplinary teams, including neurologists, ophthalmologists, and rehabilitation specialists, to provide holistic care for patients.

- Hospitals are increasingly adopting new diagnostic technologies, such as advanced imaging techniques and AI-powered analysis tools, to improve accuracy and speed in diagnosing various conditions.

- For instance, in 2024, Baptist Health in Arkansas became the first hospital system in the state to implement AI technology to assist with MRI scan interpretation. This has allowed for accurate detection and better patient outcomes, positively driving the segment.

- Overall, as per the market analysis, the adoption of new technologies for accurate diagnosis and better patient outcomes is driving segmental growth.

The clinics segment is expected to grow at the fastest CAGR over the forecast period.

- Clinics are emerging in the market due to their accessibility, affordability, and growing focus on outpatient care.

- Unlike hospitals, clinics provide personalized care in less formal settings, which appeals to patients seeking follow-up treatments or non-invasive therapies.

- With the rising demand for outpatient services, many clinics now offer specialized care, such as neuro-ophthalmology consultations and rehabilitation programs.

- Furthermore, clinics operate in underserved or rural areas, addressing the growing demand for accessible healthcare services.

- Their ability to offer cost-effective treatments makes them a preferred option for patients with limited resources or those seeking convenience, contributing to their growing prominence in the market.

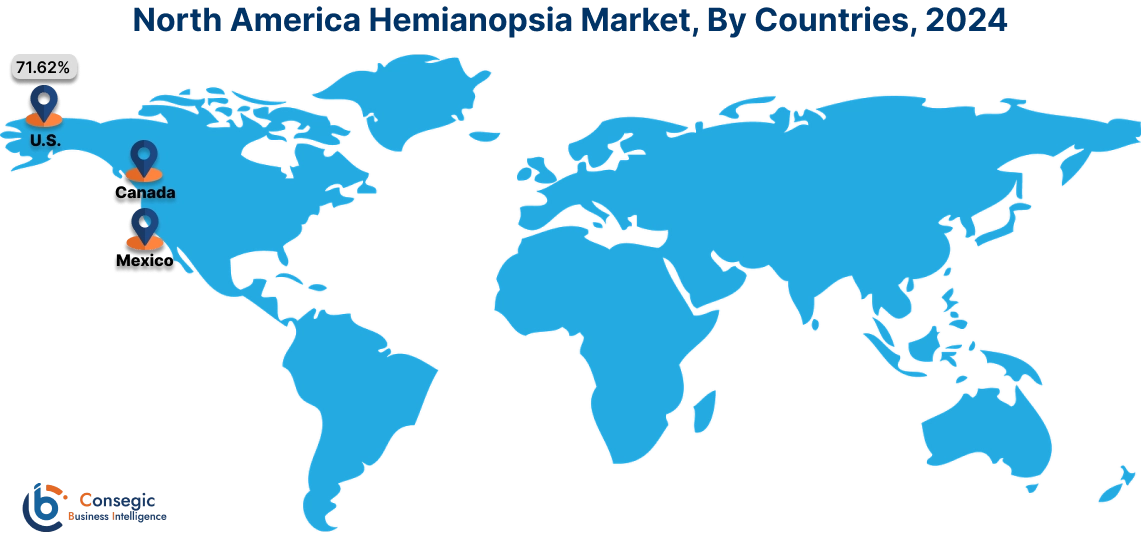

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

In 2024, North America accounted for the highest hemianopsia market share at 40.78% and was valued at USD 155.45 Million and is expected to reach USD 259.64 Million in 2032. In North America, the U.S. accounted for the hemianopsia market share of 71.62% during the base year of 2024. The region reports a significant number of stroke and traumatic brain injury cases annually.

- For instance, according to the Centers for Disease Control and Prevention (CDC), nearly 795,000 people experience a stroke each year in the United States,

This has underscored the substantial patient pool for hemianopsia diagnosis and treatment, positively driving market in region. Moreover, trend such as continuous innovation in assistive technologies, such as advanced prism glasses, wearable devices that provide visual cues, and AI-powered software for visual field training, offer new avenues for improving patient outcomes. The development of more sophisticated and user-friendly devices enhances independence and quality of life for individuals with this vision loss, driving the market. Thus, the rising prevalence of neurological disorder and technological advancements in treatment are driving the market in the region.

In Asia Pacific, the hemianopsia market is experiencing the fastest growth with a CAGR of 8.8% over the forecast period. The region is experiencing significant growth in healthcare spending. This increased investment enables greater access to diagnostic tools, advanced therapies, and rehabilitation services, thus driving the market in the region. Moreover, the region is also witnessing a surge in the establishment of specialized rehabilitation centers. These centers focus on neuro-ophthalmology and post-stroke care, offering therapies such as vision restoration therapy, prism adaptation, and occupational rehabilitation. Governments and private organizations in APAC countries are investing in expanding facilities, particularly in urban and semi-urban areas, to meet the growing demand for rehabilitation services.

Europe's hemianopsia market analysis states that several trends are responsible for the progress of the market in the region. Countries such as Germany, the UK, and France are equipped with state-of-the-art diagnostic technologies, including MRI and optical coherence tomography (OCT), ensuring accurate and early detection of visual impairments. Moreover, insurance coverage and reimbursement policies across Europe play a significant role in reducing the financial burden on patients, facilitating access to treatment. These policies are particularly strong in Western European countries, where healthcare systems are well-funded. Additionally, public and private healthcare providers focus on supporting neurological rehabilitation programs, which include treatment for loss of half of a visual field.

The Middle East and Africa (MEA) hemianopsia market analysis states that the region is also witnessing a notable surge. Trends such as public health campaigns and educational initiatives enhance the understanding of conditions such as strokes and their link to loss of a visual field, encouraging early diagnosis and treatment. Moreover, the region is also witnessing a shift toward outpatient care, with clinics and specialized centers offering affordable diagnostic and therapeutic services. These facilities provide accessibility for patients who do not require hospitalization, catering to the demand for cost-effective treatments. Countries such as the UAE and South Africa are emerging as regional hubs for advanced healthcare, further boosting the market.

Latin America's hemianopsia market size is also emerging and limited retail penetration in rural areas pose challenges. The market is expanding due to increasing healthcare investments and collaborations between public and private sectors. Governments in countries such as Brazil, Mexico, and Argentina are prioritizing healthcare infrastructure development, leading to better access to diagnostic tools and treatment options for hemianopsia. Moreover, collaboration between private healthcare providers and international organizations has brought advanced technologies and therapies to the region. These partnerships enable training programs for medical professionals and the integration of cutting-edge diagnostic equipment, improving patient outcomes.

Top Key Players and Market Share Insights:

The Hemianopsia market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D) and product innovation to hold a strong position in the global Hemianopsia market. Key players in The Hemianopsia industry include-

- Ocutech, Inc. (U.S.)

- Vycor Medical (U.S.)

- EssilorLuxottica (France)

- Edmund Optics (U.S.)

- Chadwick Optical (U.S.)

- Carl Zeiss AG (Germany)

- Haag-Streit Holding (Germany)

- Heidelberg Engineering (Germany)

Recent Industry Developments :

Product Launch:

- In August 2024, Ocutech launched a new device called SideSight designed to assist people with loss of vision in half of the visual field. It is an ultrasonic sensor that attaches to eyeglasses and alerts the wearer with a vibration when an obstacle is detected on their blind side, essentially providing awareness of their peripheral vision where they cannot see.

Hemianopsia Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 674.07 Million |

| CAGR (2025-2032) | 7.4% |

| By Type |

|

| By Defect Type |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Hemianopsia market? +

In 2024, the Hemianopsia market is USD 381.18 Million.

Which is the fastest-growing region in the Hemianopsia market? +

Asia Pacific is the fastest-growing region in the Hemianopsia market.

What specific segmentation details are covered in the Hemianopsia market? +

Type, Defect Type and End-Use segmentation details are covered in the Hemianopsia market

Who are the major players in the Hemianopsia market? +

Ocutech, Inc. (U.S.), Vycor Medical (U.S.), Chadwick Optical (U.S.), Carl Zeiss AG (Germany), Haag-Streit Holding (Germany), Heidelberg Engineering (Germany), EssilorLuxottica (France), and Edmund Optics (U.S.)