- Summary

- Table Of Content

- Methodology

Heavy Duty Construction Equipment Market Size:

Heavy Duty Construction Equipment Market size is estimated to reach over USD 264.15 Billion by 2031 from a value of USD 185.36 Billion in 2023 and is projected to grow by USD 190.45 Billion in 2024, growing at a CAGR of 4.5% from 2024 to 2031.

Heavy Duty Construction Equipment Market Scope & Overview:

The heavy-duty construction equipment focuses on machinery designed for large-scale construction projects, including earthmoving, material handling, and road-building activities. This market encompasses equipment such as excavators, loaders, bulldozers, cranes, and dump trucks, which are engineered to handle heavy loads and operate in demanding environments. Key characteristics of heavy-duty construction equipment include high durability, advanced hydraulics, enhanced fuel efficiency, and integration with telematics for real-time monitoring. The benefits of these machines include improved productivity, reduced labor costs, and precision in large-scale construction operations. Applications span infrastructure development, mining, oil and gas, and urban construction. End-users include construction contractors, mining operators, and government agencies, driven by rising investments in infrastructure projects, urbanization trends, and advancements in equipment automation and electrification.

Heavy Duty Construction Equipment MarketDynamics - (DRO) :

Key Drivers:

Increasing Investments in Infrastructure Development Drive Market Growth

The surge in infrastructure development projects globally is a key driver for the heavy-duty construction equipment market. Governments and private investors are prioritizing large-scale construction projects such as highways, railways, airports, bridges, and urban housing developments to support economic development and address urbanization challenges. For example, initiatives like China's Belt and Road Initiative (BRI) and India's Smart Cities Mission are generating a significant rise in robust construction machinery capable of handling large-scale operations efficiently.

Additionally, developed regions like North America and Europe are investing heavily in modernizing aging infrastructure, including the repair and upgrade of existing roadways, bridges, and public utilities. These projects require advanced heavy-duty equipment such as excavators, loaders, cranes, and bulldozers to ensure timely and efficient completion. The rising need for advanced construction machinery that can handle complex tasks while reducing labor dependency is fueling the adoption of heavy-duty construction equipment across both developed and emerging markets.

Key Restraints :

High Initial Costs of Heavy-Duty Equipment Limit Market Penetration

The high upfront costs associated with heavy-duty construction equipment are a significant restraint for the market, particularly for small and medium-sized enterprises (SMEs) in the construction sectors. Modern machinery equipped with advanced technologies, such as telematics, GPS-based monitoring, and autonomous features, is expensive to purchase, making it less accessible for smaller contractors. Moreover, the cost of routine maintenance, repairs, and spare parts further adds to the financial burden, increasing the total cost of ownership.

In price-sensitive markets, the limited availability of financing and leasing options exacerbates this issue, restricting the ability of smaller firms to acquire the latest equipment. Additionally, fluctuations in raw material prices, particularly steel and other components, contribute to the high production costs of construction machinery, making it more expensive for end-users. These financial constraints hinder the widespread adoption of heavy-duty construction equipment, particularly in developing regions where budget limitations are a common challenge.

Future Opportunities :

Rising Demand for Rental Services Creates Growth Opportunities

The growing advancement for construction equipment rental services is creating significant heavy-duty construction equipment market opportunities. Contractors and construction firms are increasingly opting for rental solutions to reduce the financial burden of purchasing high-cost equipment and managing associated operational risks. Rental services allow businesses to access advanced machinery on a short-term or project-specific basis, ensuring flexibility and cost-effectiveness.

The expansion of organized rental markets, supported by digital platforms and online marketplaces, has made it easier for contractors to find and rent heavy-duty equipment as per their requirements. These platforms offer features such as real-time availability, price comparison, and remote equipment monitoring, enhancing user convenience. Additionally, the adoption of subscription-based models in the rental service is enabling smaller firms to utilize cutting-edge equipment without significant capital investments. As the heavy-duty construction equipment market demand for construction equipment rental services continues to grow, it is expected to drive heavy-duty construction equipment market expansion and provide manufacturers with new revenue streams through partnerships with rental companies.

Heavy Duty Construction Equipment Market Segmental Analysis :

By Equipment Type:

Based on equipment type, the heavy-duty construction equipment market is segmented into earthmoving equipment, material handling equipment, heavy construction vehicles, and others.

The earthmoving equipment segment accounted for the largest revenue in heavy duty construction equipment market share in 2023.

- Earthmoving equipment, including excavators, loaders, bulldozers, and motor graders, is widely used in construction and infrastructure development projects due to its versatility and efficiency.

- Excavators and loaders are particularly critical for activities such as excavation, material loading, and site preparation.

- The increasing number of large-scale infrastructure projects, particularly in emerging economies, is driving the surge for earthmoving equipment.

- Moreover, advancements in automation and smart technology integration in these machines are further boosting their adoption across the construction industry.

- Therefore, earthmoving equipment analysis leads the heavy-duty construction equipment market trends due to its essential role in construction projects, driven by the advancement of efficient, versatile, and technologically advanced machines.

The material handling equipment segment is anticipated to register the fastest CAGR during the forecast period.

- Material handling equipment, such as cranes, forklifts, and conveyors, is essential for moving, lifting, and transporting heavy materials across construction sites.

- The growing adoption of cranes for high-rise building construction and the rising applications for forklifts in warehouse management are key factors driving this segment's advancements.

- Additionally, advancements in electric and automated material handling equipment are increasing their efficiency and appeal across various industries.

- Hence, material handling equipment analysis depicts it is expected to grow rapidly, fueled by the increasing adoption of efficient lifting and transportation solutions, particularly in high-rise construction and warehouse management.

By Application:

Based on application, the heavy-duty construction equipment market is segmented into excavation & demolition, heavy lifting, material handling, tunneling, transportation, and recycling & waste management.

The excavation & demolition segment accounted for the largest revenue share in 2023.

- Excavation and demolition activities form the backbone of construction and infrastructure development, driving appeal for heavy-duty equipment such as excavators, bulldozers, and tippers.

- These activities are critical for site preparation, foundation work, and dismantling structures, making them integral to almost every construction project.

- The increasing number of urban redevelopment projects and the expansion of infrastructure in emerging economies contribute to the dominance of this segment.

- Hence, excavation & demolition analysis lead the market due to their fundamental role in construction projects and the growing number of infrastructure and redevelopment activities all over.

The recycling & waste management segment is anticipated to register the fastest CAGR during the forecast period.

- Recycling and waste management are gaining prominence as industries and governments emphasize sustainable construction practices.

- Heavy-duty equipment, such as compactors and conveyors, is increasingly used for managing construction waste and recycling materials for reuse.

- The implementation of stricter environmental regulations and the rising focus on reducing construction waste are driving the applications for specialized equipment in this segment.

- Thus, recycling & waste management is expected to grow rapidly, driven by the increasing adoption of sustainable practices and the heavy-duty construction equipment market demand for efficient waste management solutions in construction.

By Propulsion Type:

Based on propulsion type, the market is segmented into diesel, electric, hybrid, and CNG/LNG/RNG.

The diesel segment accounted for the largest revenue in heavy duty construction equipment market share in 2023.

- Diesel-powered construction equipment remains the most widely used due to its reliability, efficiency, and ability to handle heavy workloads.

- Diesel engines provide the power required for large-scale construction activities, making them the preferred choice for heavy-duty equipment.

- The established infrastructure for diesel fuel distribution and the availability of advanced, fuel-efficient diesel engines further support the dominance of this segment.

- Thus, diesel-powered equipment heavy-duty construction equipment market analysis leads the market trends due to its reliability, efficiency, and widespread availability, making it the preferred choice for heavy-duty applications.

The electric segment is anticipated to register the fastest CAGR during the forecast period.

- Electric-powered construction equipment is gaining traction as industries transition toward sustainable and eco-friendly solutions.

- These machines offer significant advantages, including reduced emissions, lower operating costs, and quieter operations.

- The increasing adoption of electric equipment, particularly in urban construction projects with strict emission regulations, is driving this segment's advancement.

- Additionally, advancements in battery technology and the availability of charging infrastructure are further accelerating the adoption of electric construction equipment.

- Hence, electric-powered equipment trends are expected to grow rapidly, driven by the growing applications for sustainable solutions and advancements in battery technology.

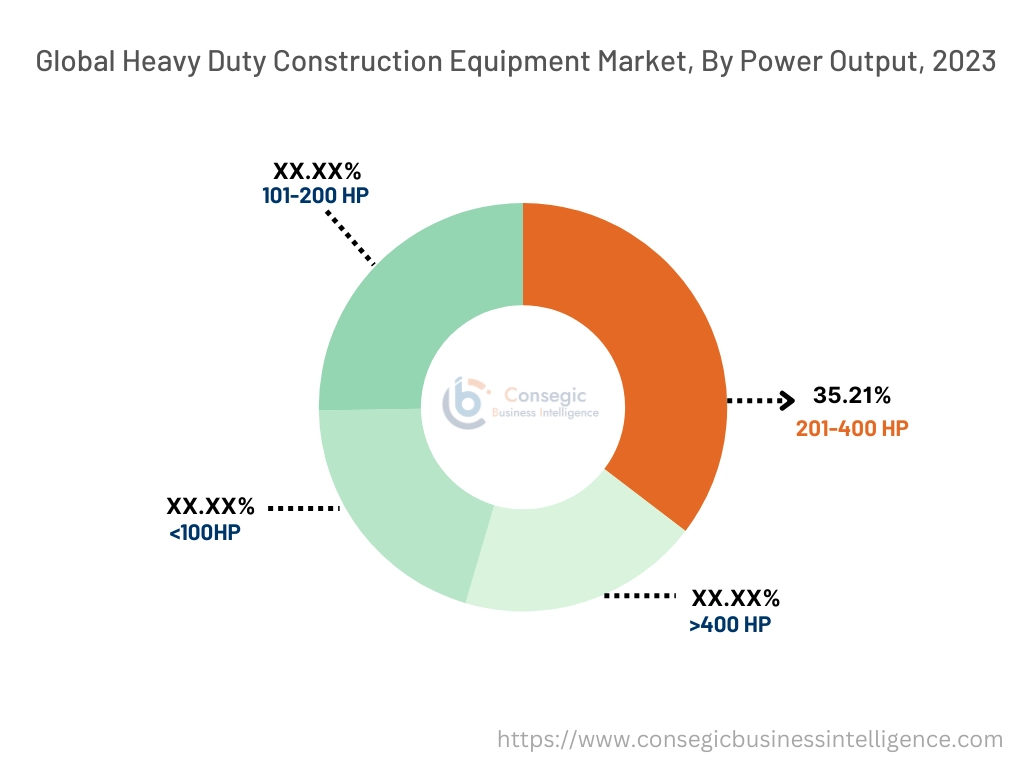

By Power Output:

Based on power output, the market is segmented into <100 HP, 101-200 HP, 201-400 HP, and >400 HP.

The 201-400 HP segment accounted for the largest revenue of 35.21% share in 2023.

- Construction equipment with a power output of 201-400 HP is widely used in medium to large-scale infrastructure projects due to its ability to handle a variety of tasks efficiently.

- This range of power output is ideal for earthmoving, material handling, and heavy lifting applications, making it the most versatile category.

- The increasing number of infrastructure projects, particularly in emerging economies, is driving the application for equipment in this power range.

- Thus, the 201-400 HP segment leads the market trends due to its versatility and suitability for a wide range of medium to large-scale construction activities.

The >400 HP segment is anticipated to register the fastest CAGR during the forecast period.

- High-power construction equipment with >400 HP output is essential for large-scale projects such as mining, tunneling, and heavy-duty infrastructure development.

- The growing advancements for robust machinery capable of handling extreme workloads and harsh environments are driving the adoption of equipment in this category.

- Technological advancements in high-power engines and the increasing scale of infrastructure projects globally further support the rapid development of this segment.

- Thus, the >400 HP segment trend is expected to grow rapidly, driven by the rising factor for robust machinery in large-scale and heavy-duty construction projects.

By Engine Capacity:

Based on engine capacity, the market is segmented into <5L, 5-10L, and >10L.

The 5-10L segment accounted for the largest revenue share in 2023.

- Engines with a capacity of 5-10L are commonly used in medium-duty construction equipment, offering a balance between power and fuel efficiency.

- This engine capacity is ideal for a wide range of construction activities, including excavation, material handling, and transportation.

- The increasing adoption of medium-duty equipment in construction projects globally supports the dominance of this segment.

- Thus, the 5-10L engine capacity segment leads the market trends due to its widespread use in medium-duty equipment and its balance of power and efficiency.

The >10L segment is anticipated to register the fastest CAGR during the forecast period.

- Engines with a capacity of >10L are essential for heavy-duty construction equipment used in large-scale projects such as mining, tunneling, and heavy infrastructure development.

- The appeal for high-capacity engines is growing as the scale and complexity of construction projects increase.

- Additionally, advancements in engine technology to improve efficiency and reduce emissions are further driving growth in this segment.

- The >10L segment analysis trends are expected to grow rapidly, driven by the increasing appeals for high-capacity engines in large-scale and heavy-duty construction projects.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

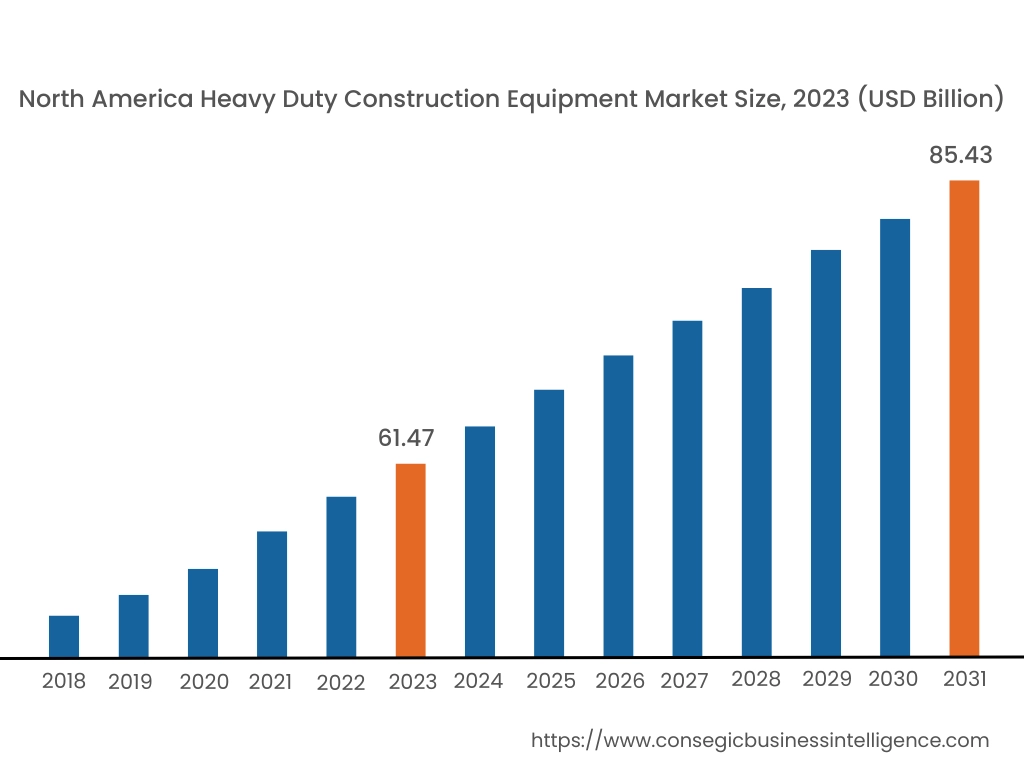

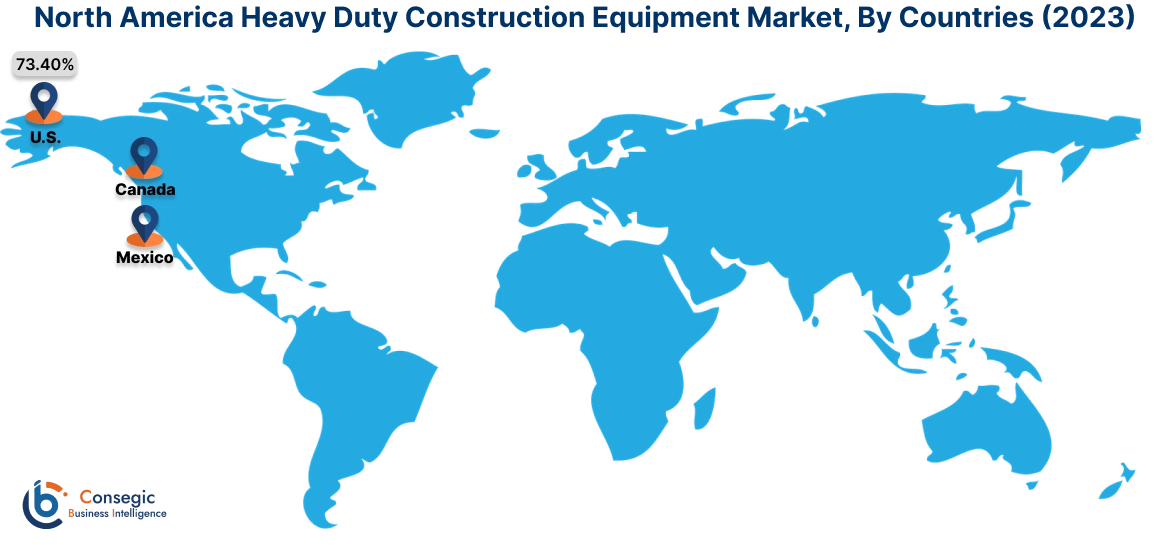

In 2023, North America was valued at USD 61.47 Billion and is expected to reach USD 85.43 Billion in 2031. In North America, the U.S. accounted for the highest share of 73.40% during the base year of 2023. North America remains a prominent market for heavy-duty construction equipment, driven by substantial investments in infrastructure modernization and housing developments. The U.S. leads the region, benefiting from large-scale projects such as highway upgrades, airport expansions, and renewable energy installations supported by the Infrastructure Investment and Jobs Act. Canada contributes to the market surge through increasing applications in the mining and oil and gas sectors, particularly for excavators and loaders. However, the market faces challenges from stringent emission regulations, pushing manufacturers to adopt eco-friendly technologies such as electric and hybrid equipment.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 4.9% over the forecast period. Asia-Pacific is the largest and fastest-growing region for heavy-duty construction equipment analysis, fueled by rapid urbanization, industrialization, and infrastructure development in China, India, and Southeast Asia. China dominates the market with massive government-led infrastructure projects under its Belt and Road Initiative and rising applications from the real estate sector. India is experiencing a strong surge, driven by initiatives like Smart Cities Mission and Pradhan Mantri Gram Sadak Yojana, which require advanced construction machinery. Southeast Asian countries such as Indonesia and Vietnam are witnessing increased demand for heavy equipment due to expanding transportation and energy projects. However, challenges such as fluctuating raw material costs and inconsistent regulatory frameworks across countries persist.

Europe is a key market for heavy-duty construction equipment, with a focus on sustainable construction practices and technological advancements. Germany, the UK, and France dominate, driven by ongoing infrastructure projects such as railway expansions and green building initiatives. Germany leads in the adoption of automated and hybrid machinery to align with the EU’s stringent environmental regulations. The UK’s increased housing requirements and urban renewal projects further support heavy-duty construction equipment market growth. However, rising energy costs and compliance with emissions standards remain significant challenges for manufacturers and end-users in the region.

The Middle East & Africa region is experiencing steady development in the heavy-duty construction equipment market analysis, led by large-scale infrastructure projects in Saudi Arabia, the UAE, and South Africa. Saudi Arabia’s Vision 2030 initiative and the UAE’s focus on developing mega infrastructure projects such as Expo City Dubai are key drivers. In Africa, South Africa is a significant market, with increasing demand for equipment in mining, energy, and urban development projects. However, the limited availability of skilled labor and dependency on imports for advanced machinery are challenges that impact heavy-duty construction equipment market growth in certain parts of the region.

Latin America is an emerging market for heavy-duty construction equipment, with Brazil and Mexico at the forefront. Brazil’s investments in road and port infrastructure, along with urban housing projects, are driving advancements for construction machinery. Mexico is witnessing increased adoption of heavy-duty equipment in transportation and energy infrastructure projects. Additionally, mining activities in countries like Chile and Peru contribute to the surge for excavators, dump trucks, and loaders. However, economic instability and fluctuating exchange rates pose challenges to the region's development, affecting the purchasing power of contractors and developers.

Top Key Players & Market Share Insights:

The Heavy Duty Construction Equipment market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Heavy Duty Construction Equipment market. Key players in the Heavy Duty Construction Equipment industry include -

- Caterpillar Inc. (United States)

- Komatsu Ltd. (Japan)

- Sany Heavy Industry Co., Ltd. (China)

- J C Bamford Excavators Ltd. (United Kingdom)

- Doosan Infracore Co., Ltd. (South Korea)

- Hitachi Construction Machinery Co., Ltd. (Japan)

- Volvo Construction Equipment (Sweden)

- Liebherr Group (Germany)

- Deere & Company (United States)

- CNH Industrial N.V. (United Kingdom)

Recent Industry Developments :

Acquistions:

- In December 2022, Komatsu acquired GHH Group GmbH, a German manufacturer specializing in underground mining and tunneling equipment. This strategic move aims to enhance Komatsu's offerings in the heavy-duty construction sector.

Heavy Duty Construction Equipment Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 264.15 Billion |

| CAGR (2024-2031) | 4.5% |

| By Equipment Type |

|

| By Application |

|

| By Propulsion Type |

|

| By Power Output |

|

| By Engine Capacity |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected market size for the Heavy Duty Construction Equipment Market by 2031? +

Heavy Duty Construction Equipment Market size is estimated to reach over USD 264.15 Billion by 2031 from a value of USD 185.36 Billion in 2023 and is projected to grow by USD 190.45 Billion in 2024, growing at a CAGR of 4.5% from 2024 to 2031.

What are the primary drivers of growth in the heavy-duty construction equipment market? +

Increasing investments in infrastructure development, urbanization trends, and advancements in automation and electrification of construction equipment are driving the market.

Which equipment type holds the largest share in the market? +

The Earthmoving Equipment segment, including excavators, loaders, and bulldozers, leads the market due to its versatility and widespread use in construction and infrastructure projects.

Which equipment type is expected to grow at the fastest rate? +

The Material Handling Equipment segment, driven by the increasing adoption of cranes and forklifts in construction and warehouse management, is projected to grow at the fastest CAGR.

What are the major restraints affecting the market? +

High initial costs of heavy-duty equipment, along with maintenance expenses and limited financing options, are significant barriers to market growth.