- Summary

- Table Of Content

- Methodology

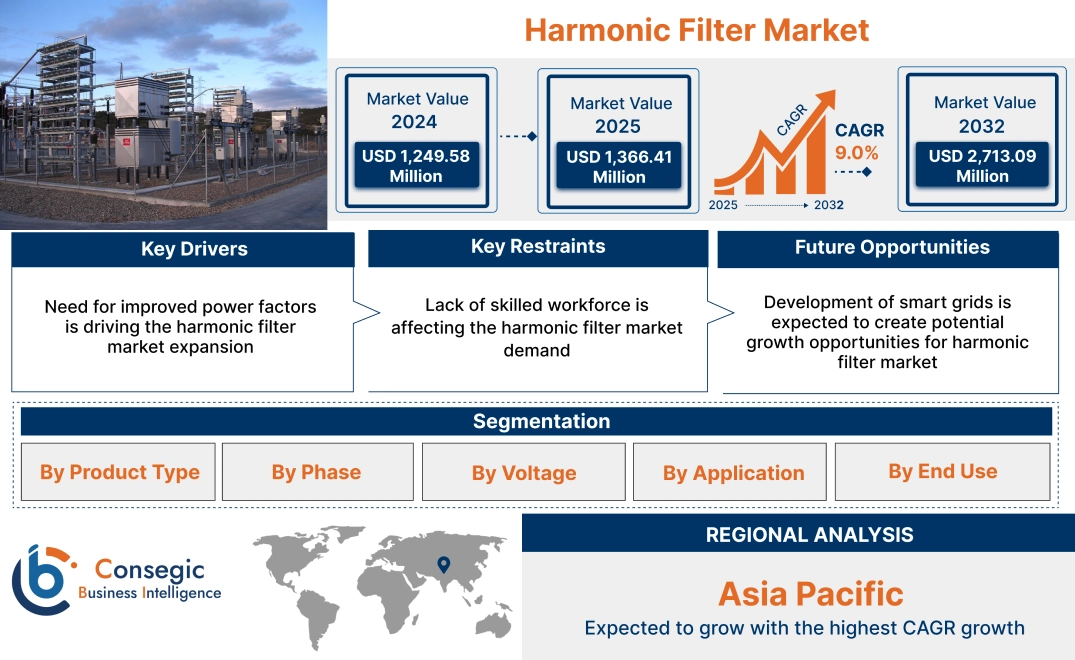

Harmonic Filter Market Size:

Harmonic Filter Market Size is estimated to reach over USD 2,713.09 Million by 2032 from a value of USD 1,249.58 Million in 2024 and is projected to grow by USD 1,366.41 Million in 2025, growing at a CAGR of 9.0% from 2025 to 2032.

Harmonic Filter Market Scope & Overview:

Harmonic filter plays a crucial role in minimizing harmonic distortions in electrical systems, which helps maintain effective power transmission and distribution. As non-linear loads such as variable frequency drives (VFDs) and power converters become more prevalent in industrial and commercial settings, the demand for solutions to mitigate harmonics has surged. Furthermore, strict government regulations regarding power quality and energy efficiency have accelerated market expansion. Moreover, technological advancements such as the development of active harmonic mitigation solutions with real-time monitoring and control capabilities have enhanced the market attractiveness. These sophisticated filters provide superior harmonic suppression efficiency and adaptability to dynamic load changes, effectively meeting the shifting demands of contemporary electrical systems. Furthermore, the rise of automation and digitization across various sectors has accelerated the integration of power quality solutions, consequently boosting the adoption of such type of solutions simultaneously.

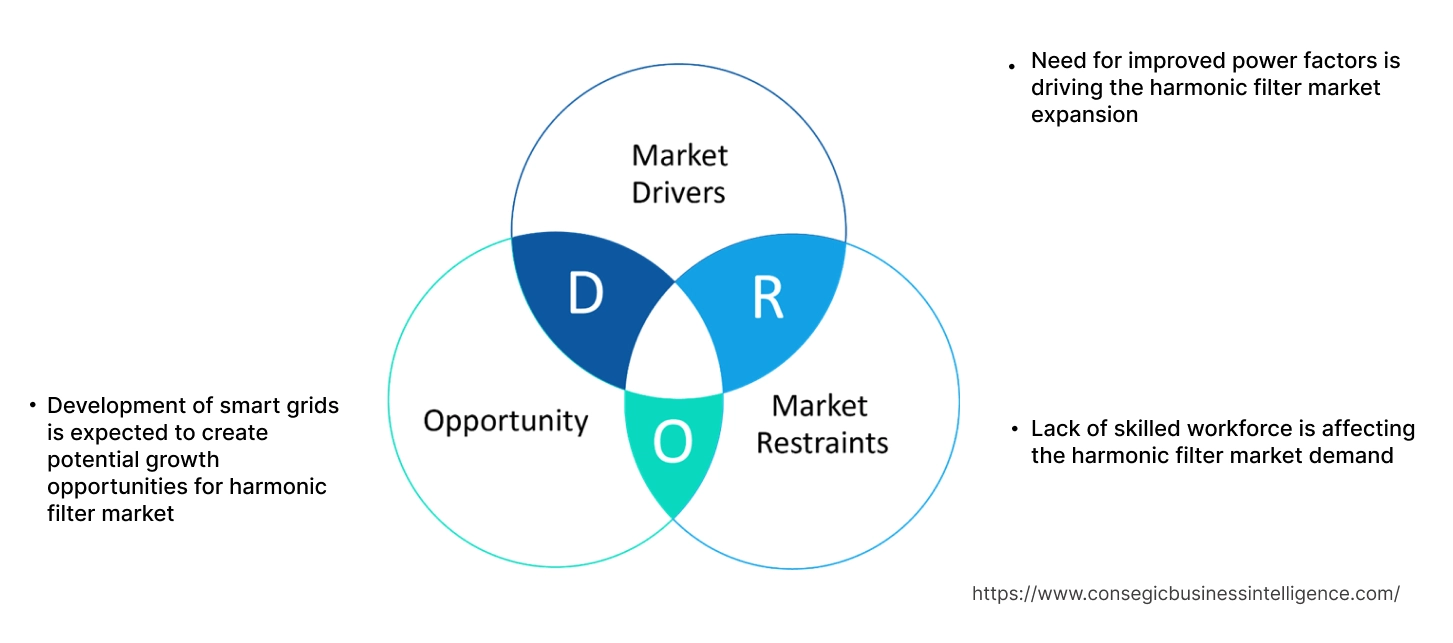

Harmonic Filter Market Dynamics - (DRO) :

Key Drivers:

Need for improved power factors is driving the harmonic filter market expansion

The global market is experiencing significant growth due to the escalating demand for improved power factor correction across various industries. The growing use of non-linear loads, including variable frequency drives (VFDs), computers, and LED lighting systems, has made power systems susceptible to harmonic distortions. These distortions compromise power quality and create inefficiencies within the power distribution network. Consequently, there is a crucial need for harmonic mitigation solutions to address these distortions and improve power factor correction. Further, the growing use of renewable energy sources, including solar and wind power, introduces new challenges to power networks, resulting in heightened harmonic distortions. Since these energy sources frequently produce electricity in an inconsistent and unpredictable manner, their incorporation into the grid requires sophisticated power conditioning technologies such as harmonic mitigation solutions. Moreover, the surge in electric vehicles (EVs) and their associated charging infrastructure further intensifies harmonic problems, especially in both commercial and residential environments.

- For instance, in January 2023, Danfoss A/S launched an active filter AAF 007 for harmonic mitigation, that cuts filter power losses by 60%. This system delivers harmonic mitigation, imbalance compensation, and power factor correction, adhering to the most current regulatory standards. It identifies harmonic distortion in the system and generates a counteracting current to eradicate electrical noise.

Thus, according to the harmonic filter market analysis, the growing need for improved power factors is driving the harmonic filter market size and trends.

Key Restraints:

Lack of skilled workforce is affecting the harmonic filter market demand

A significant hurdle confronting this market is the shortage of a proficient workforce. With the escalating complexity of harmonic mitigating solutions and the advent of novel technologies, there is an increasing need for experts possessing specialized expertise in power electronics, electrical engineering, and associated disciplines. Further, the availability of skilled professionals has not matched the surging need, resulting in a deficit of qualified individuals within the harmonic mitigation solutions. The deficit of qualified professionals in the market presents numerous challenges to its progression and advancement. In the absence of sufficient expertise, organizations might find it difficult to efficiently design, produce, and install harmonic mitigating solutions, resulting in delays, budget overruns, and possible safety hazards.

Additionally, the shortage of skilled workers stifles innovation and restricts the market capacity to create cutting-edge solutions that cater to the changing needs of clients. Bridging this skills gap necessitates coordinated efforts from stakeholders in both the public and private sectors to invest in educational initiatives, training, and workforce development programs specifically aligned with the unique needs of the harmonic filter market size.

Future Opportunities:

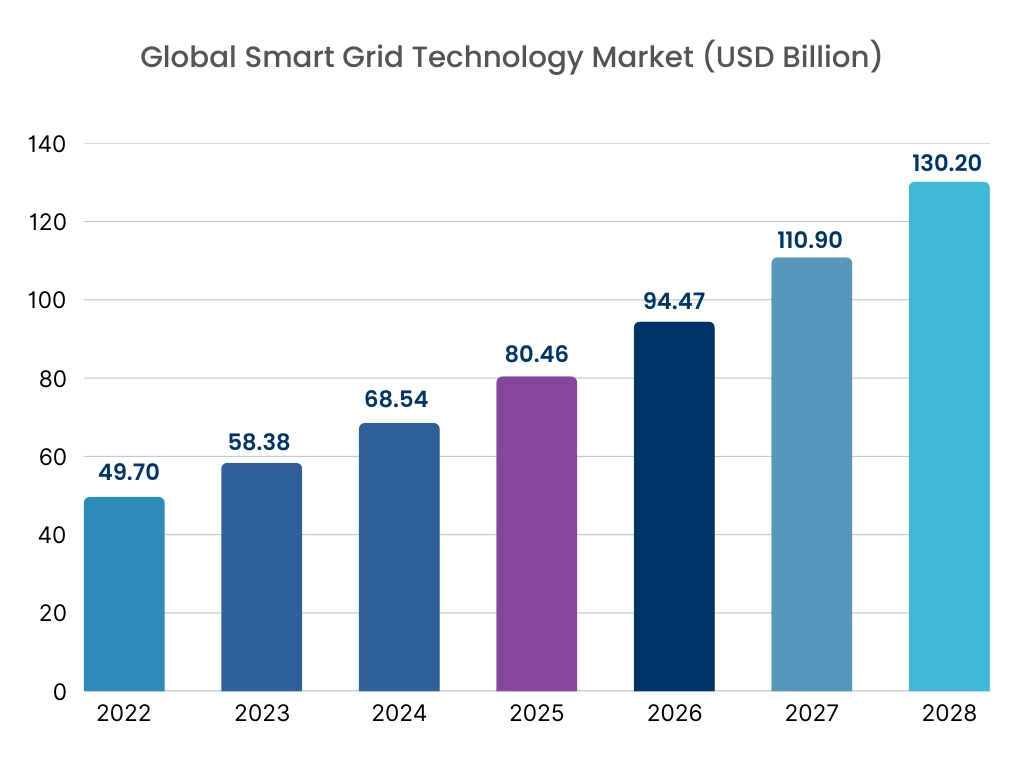

Development of smart grids is expected to create potential growth opportunities for harmonic filter market

Smart grids combine cutting-edge communication, sensing, and control technologies with the existing power grid framework, allowing for an efficient exchange of electricity and data between energy providers and consumers. By utilizing intelligent devices like sensors, smart meters, and automated switching systems, these grids improve reliability, optimize energy distribution, and support the integration of renewable energy sources. These filters are crucial in smart grid systems, as they help maintain power quality, minimize losses, and enhance system efficiency. With the ongoing global development of smart grid technologies, the need for these filters is anticipated to rise considerably, especially in areas prioritizing the modernization of their energy infrastructure.

Further, the rising embrace of renewable energy sources, including solar and wind, brings forth a mix of opportunities and hurdles for the market. Although these renewable technologies provide significant environmental advantages and aid in lowering greenhouse gas emissions, they bring forth challenges due to their intermittent and fluctuating power generation, which can affect grid reliability and power quality. These filters play a crucial role in tackling these issues by alleviating the negative impacts of harmonics and voltage variations linked to the integration of renewable energy. As governments around the globe continue to support clean energy initiatives and invest in renewable infrastructure, the need for such filters in renewable energy contexts is set to increase, further propelling the harmonic filter market trends.

- For instance, in October 2023, Powerside, a worldwide leader in power grid technology, introduced two innovative solutions, the PowerAct Hybrid Harmonic Mitigation Solution and the PQ Edge Power Analyzer, aimed at enhancing power quality optimization across various sectors. The latest innovation in power analysis, the PQ Edge, offers insights into grid edge power supply for the performance of delicate electronics in essential applications. This enhanced visibility enables companies to proactively detect performance challenges, improve operational efficiency, and optimize uptime. Accompanying this solution is the free monitoring software, QubeScan, which grants comprehensive visibility across fleets and notifies users of power supply irregularities that could lead to downtime or damage to equipment.

Thus, based on the above factors, the development of smart grids is expected to play a crucial role in shaping the future of the harmonic filter market opportunities.

Harmonic Filter Market Segmental Analysis :

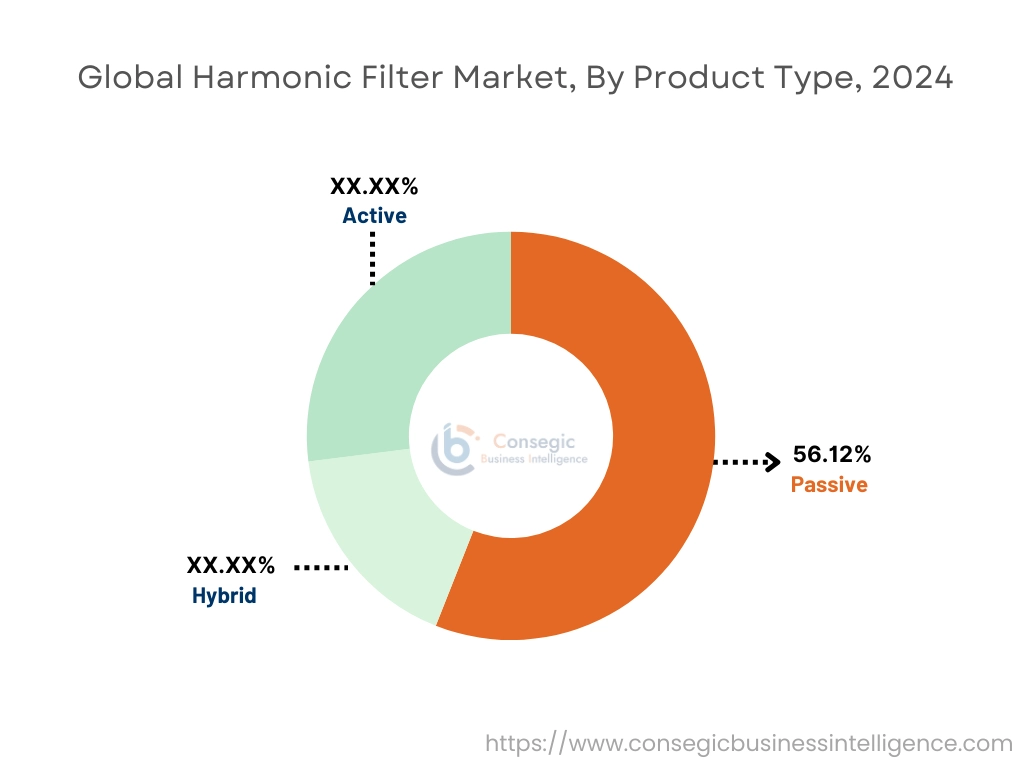

By Product Type:

Based on product type, the market is segmented into active, passive, and hybrid.

Trends in the product type:

- The advancements in power electronics, digital signal processing, and control algorithms are resulting in more efficient and economical solutions for harmonic solutions.

- An ongoing increase in the need for power quality, a heightened reliance on equipment, the growing automation of industrial processes, and data-driven decision-making facilitated by the use of sensitive electronic devices are anticipated to drive significant growth in the global market throughout the forecast period.

The passive segment accounted for the largest revenue share of 56.12% in the year 2024.

- The segment growth can be attributed by the widespread use of uninterruptible power supply (UPS) devices, variable frequency drives (VFDs) for motors, transformers, rectifiers, and other related technologies.

- The affordability offered by passive harmonic mitigating solutions, particularly for fixed-frequency harmonic mitigation, coupled with their increasing application in medium to high voltage scenarios, is anticipated to further boost need in this segment.

- In the equipment framework of the IT sector, front-end power supply units and VFDs are recognized for drawing harmonic currents, necessitating the use of passive filters to keep current and voltage distortion within safer thresholds.

- Manufacturers prefer passive solutions because they entail lower initial expenses and require little maintenance. Sectors such as manufacturing, oil and gas, and commercial real estate play a major role in driving the need for such type of solutions, as they emphasize the importance of stable power quality to prevent equipment damage and improve operational efficiency.

- In May 2020, Schaffner introduced its latest ecosine max passive harmonic mitigation solution series. These innovative filters are crafted to effectively reduce excessive harmonics in highly demanding applications. The new ecosine max filter series, including models FN3472/73, FN3480/81, FN3470/71, and FN3482/83, is available for both 400 VAC and 480 VAC, accommodating 50 Hz and 60 Hz networks, and is built on the company's ecosine platform. This series serves as the essential passive power quality solution for higher power ranges (250KW-500KW) found in challenging drive applications.

- Thus, factors and developments, such as growing adoption of uninterruptible power supply (UPS) devices would further drive the future of harmonic filter market growth.

The active segment is anticipated to register the fastest CAGR during the forecast period.

- The active segment is projected to expand significantly in the upcoming years, driven by the rising intricacy of electrical systems and the need for flexible solutions.

- Active filters offer instantaneous harmonic compensation, adjusting dynamically to fluctuating load conditions while adeptly handling a broader spectrum of harmonic frequencies. The increasing incorporation of cutting-edge technologies, including automation and renewable energy sources, fuels the need for these smart systems.

- Moreover, their capacity to lower overall energy expenses by reducing losses places them in a strong position within markets that prioritize sustainability and efficiency.

- For instance, in September 2023, Quality Energy, a manufacturer of power quality and energy efficiency solutions based in Australia, has unveiled a new series of active filters. These filters feature high input impedance and remarkably low output impedance. The filters exhibit a high input impedance coupled with an extremely low output impedance.

- These factors and analysis would further drive the harmonic filter market demand during the forecast period.

By Phase:

Based on phase, the market is segmented into single phase and three phase.

Trends in the phase:

- Three-phase filters are the most utilized, primarily in industrial and commercial sectors, owing to their effectiveness in handling the power produced by three-phase electrical systems. They play a vital role in large-scale operations, including manufacturing facilities and power grids, to facilitate seamless and efficient power distribution.

- Further, single-phase filters remain significant for applications with lower power demands, such as residential neighbourhoods or smaller commercial environments.

The three phase segment accounted for the largest revenue share in the year 2024.

- In 2024, the three-phase segment dominated the market, largely owing to its widespread application in industrial and commercial sectors.

- Three-phase systems offer enhanced power distribution efficiency and are particularly suited for powering large motors and heavy equipment. Sectors like manufacturing, mining, and energy generation depend on these systems to ensure operational effectiveness and reduce downtime.

- The dependable nature and stability of three-phase setups, along with their capacity to manage greater loads without considerable voltage loss, render them the favoured option for extensive operations.

- Thus, factors and developments, such as growing dependency on power quality and electronic devices for attaining operational efficiencies, and advancements in filter technology are driving the harmonic filter market growth.

The single phase segment is anticipated to register the fastest CAGR during the forecast period.

- The single-phase segment is expected to expand swiftly throughout the forecast period, fuelled by its growing use in residential and light commercial settings, where efficient power management is essential for smaller loads.

- The rise of smart homes and IoT devices is boosting the requirement for single-phase solutions, as these systems easily blend into compact infrastructures.

- Additionally, the continuing transition to renewable energy sources, including solar panels and wind turbines, typically supports single-phase setups, thereby increasing their attractiveness in the market.

- These factors and analysis in the single phase segment would further create the need for harmonic mitigating solutions during the forecast period.

By Voltage:

Based on voltage, the market is segmented into low, medium, and high.

Trends in the voltage:

- The growing need for superior power quality, fuelled by the sensitivity of contemporary electronic devices, is compelling sectors such as data centers, healthcare, and advanced manufacturing to implement filters for dependable operations.

- Moreover, the swift rise of renewable energy sources, especially solar and wind, which rely on power electronic converters, is generating a significant need for harmonic mitigation challenges to tackle challenges related to grid integration.

The low segment accounted for the largest revenue share in the year 2024 and it is expected to register the highest CAGR during the forecast period.

- Data centers, manufacturing facilities, commercial structures, and industrial equipment are key sectors where low-voltage filters are utilized to safeguard delicate electronics from voltage irregularities induced by harmonics.

- In both commercial and residential settings, low-voltage filters play a crucial role in maintaining the stability of electrical systems and protecting equipment from damage. As the use of renewable energy sources increases and the number of electronic devices grows, the need for low-voltage filters is projected to stay strong.

- These factors and analysis in the low voltage segment would further drive the harmonic filter market trends during the forecast period.

By Application:

Based on application, the market is segmented into data centers, ship propulsion, wind turbines, tunnel ventilation, motor drives, factory automation equipment, HVAC installations, offices and commercial buildings, medical equipment, water and wastewater treatment facilities, fan and pump applications, and others.

Trends in the application:

- The commercial sector includes a diverse array of establishments like office complexes, retail outlets, healthcare facilities, and schools. As reliance on electronic devices and delicate machinery continues to grow in these settings, the need for harmonic mitigation solutions is increasing. These filters play a crucial role in reducing harmonic distortions produced by nonlinear loads, thereby ensuring the efficient functioning of equipment and safeguarding electrical systems from potential damage.

- Within the industrial realm, harmonic distortion presents a considerable obstacle, primarily stemming from heavy machinery, motor drives, and automated systems. Industrial operations frequently rely on nonlinear loads, which can generate harmonics within the electrical network, causing voltage variations and potential equipment failures. Consequently, industries are progressively allocating resources toward harmonic mitigation strategies to ensure operational efficiency and adhere to regulatory standards.

The data centers segment accounted for the largest revenue in the year 2024 and it is expected to register the highest CAGR during the forecast period.

- Harmonic mitigating solutions are increasingly being incorporated into data center monitoring and control systems, enabling real-time analysis and optimization.

- Operators of data centers are focusing on harmonic mitigation solutions that not only enhance power quality but also lead to significant energy savings.

- By efficiently addressing harmonics, they play a crucial role in preserving the integrity of power systems, ensuring dependable and effective operations. Their function goes beyond merely improving power quality; they also aid in energy conservation by optimizing the performance of electrical equipment. As data centers embrace more advanced technologies, the need for harmonic mitigation solutions is anticipated to rise, fuelled by the necessity for improved power quality and operational efficiency.

- For instance, HPS Centurion passive filters are designed for data centers to mitigate harmonic currents created by non-linear loads. It improves power quality by concurrently reducing harmonics and upgrading true power factor.

- Thus, growing advanced monitoring control and integration with power management systems in data centers, would further drive the global market during the forecast period.

By End Use:

Based on the end use, the market is segmented into manufacturing, energy & utilities, metal & mining, healthcare, paper & pulp, construction, marine, IT & telecom, and others.

Trends in the end use:

- The increasing automation of industrial processes and the digitalization of various sectors are driving the need for harmonic mitigation solutions.

- The growing adoption of renewable energy sources is creating need harmonic mitigation solutions in various end use industries.

The manufacturing segment accounted for the largest revenue in the year 2024 and it is expected to register the highest CAGR during the forecast period.

- Heavy equipment such as stamping presses, rolling mills, and extruders frequently utilize rectifiers that generate harmonics. To alleviate these harmonics and avoid power quality challenges, these filters are employed in the large manufacturing units.

- For a comprehensive solution to harmonic challenges throughout the manufacturing plant, harmonic filters can be positioned at the main power distribution panel, enhancing the power supply for all linked devices.

- These filters are becoming increasingly favoured due to their capacity to dynamically react to fluctuating harmonic levels by actively injecting harmonic currents to negate the distortions, thus providing improved adaptability to different loads.

- These developments are anticipated to further drive the need for harmonic mitigation solutions in the global market during the forecast period.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

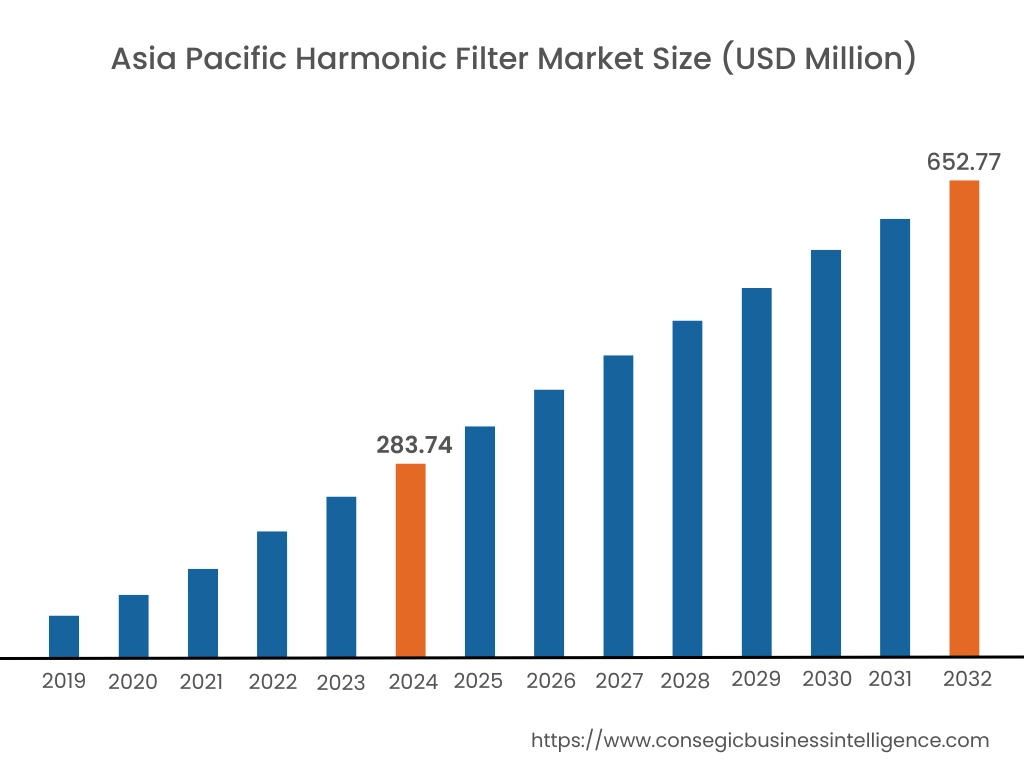

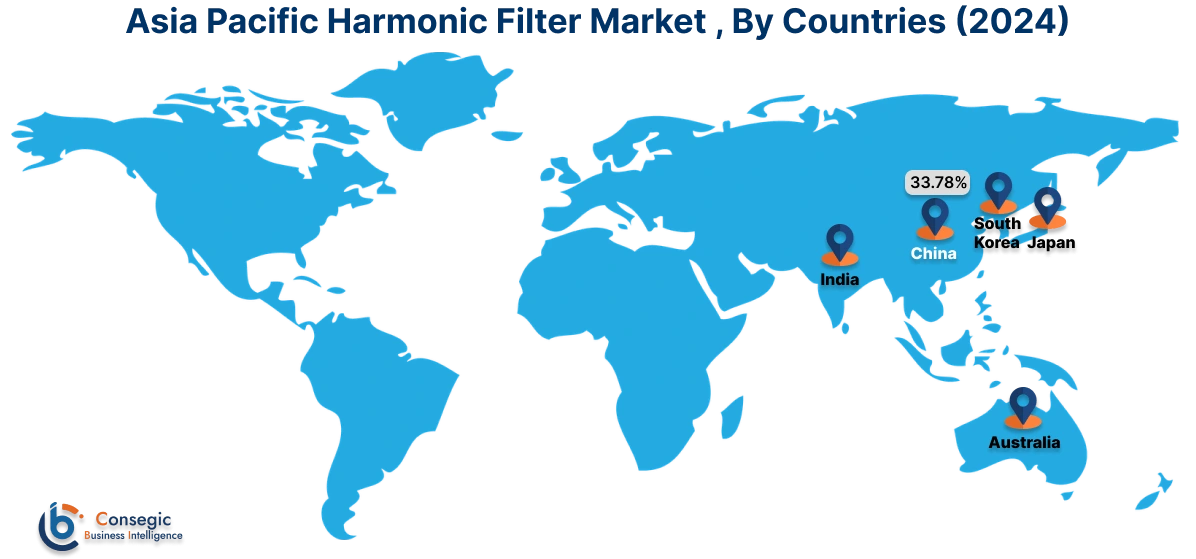

Asia Pacific harmonic filter market expansion is estimated to reach over USD 652.77 million by 2032 from a value of USD 283.74 million in 2024 and is projected to grow by USD 311.81 million in 2025. Out of this, the China market accounted for the maximum revenue split of 33.78%. The regional market is propelled by several factors, such as the presence of major players in the IT and IT services sectors, an uptick in the use of electronic devices across the area, particularly in economies such as China and India, growing application of harmonic filters in industrial settings, and the tightening of regulations regarding the installation of harmonic filters to maintain power quality.

Further, the proactive initiatives by government bodies in India and China aimed at enhancing digital ecosystems and improving the efficiency of digitally supported infrastructures are anticipated to drive need for harmonic mitigation solutions in the region. Additionally, the regional market in China accounted for the largest revenue of the regional industry in 2024. This market's progression is significantly driven by factors such as the rising adoption of sensitive electronic devices like plasma TVs and computers in both commercial and residential spaces, a strong manufacturing sector, and the ongoing trend of urbanization. These factors would further drive the regional harmonic filter market share during the forecast period.

- For instance, in February 2024, ABB India launched next-generation compact drive, ACH180, for HVACR equipment, a harmonic mitigation solution to mitigate the negative effects of harmonic currents generated by VFDs. The ACH180 provides precise management of high-efficiency motors, featuring a compact design that offers space savings, reduced capital costs, and simplified commissioning.

North America market is estimated to reach over USD 1,125.93 million by 2032 from a value of USD 507.55 million in 2024 and is projected to grow by USD 556.01 million in 2025. A large number of data centers in the region escalating utilization within industrial settings, a swift pace of digital transformation across various industries, and the expanding global presence of enterprises leading to heightened reliance on sophisticated technologies and power quality are pivotal factors propelling the regional market. Additionally, stringent regulations concerning power quality and a rising consciousness about energy efficiency are driving a consistent increase in the need for harmonic mitigation solutions in the region. Furthermore, the existence of prominent market players and continuous technological innovations significantly enhance the market's development in North America. These factors and developments would further drive the regional harmonic filter market share during the forecast period.

- For instance, in June 2021, HPS introduced the HPS Centurion P Passive Harmonic Filter, an advanced solution aimed at mitigating harmonic currents produced by non-linear loads. With initial options spanning from 5 to 500 horsepower, this filter improves power quality by reducing harmonics and boosting the true power factor. This integration provides a reliable and effective solution.

According to the industry analysis, the European market has experienced significant development during the forecast period. The regional market is being propelled by a heightened focus on renewable energy and a rising imperative to cut carbon emissions. Countries such as Germany, France, and the UK are making significant investments to enhance their power infrastructure for the integration of renewable energy. This progress has led to an increased need for harmonic mitigation solutions, which are essential for maintaining grid stability and facilitating efficient power transmission. Furthermore, favorable government initiatives and regulations designed to enhance power quality are contributing to the market's development across Europe.

Additionally, Latin America stands out as a vibrant market for harmonic filters, fueled by the escalating industrialization and urban progression in nations such as Brazil, Mexico, and Argentina. Moreover, the rising integration of renewable energy sources alongside the necessity to adhere to global power quality standards is propelling the uptake of harmonic mitigation solutions throughout the region. Additionally, countries across the Middle East are channeling investments into renewable energy initiatives and modernizing their power grids to accommodate the increasing need for electricity. Consequently, there is an escalating recognition of the detrimental impacts of harmonics on power quality, which is fueling the need for harmonic filters in the area. Further, in Africa, initiatives aimed at expanding electricity access and strengthening power infrastructure are anticipated to open up promising prospects for manufacturers and suppliers of harmonic filters. Thus, on the above harmonic filter market analysis, these factors would further drive the regional market during the forecast period.

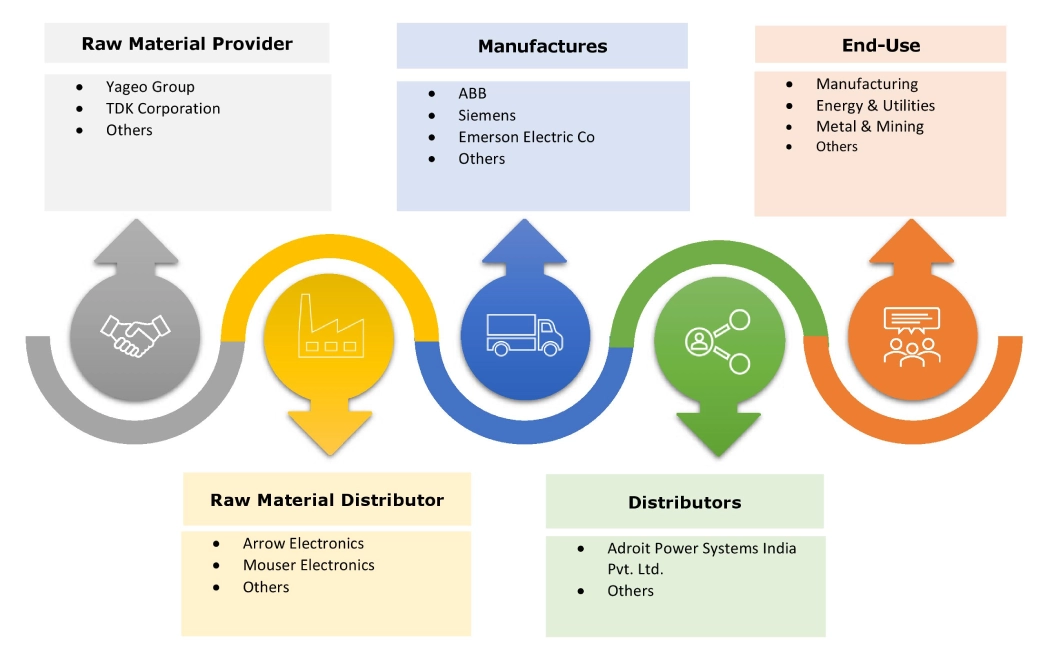

Top Key Players and Market Share Insights:

The global harmonic filter market is highly competitive with major players providing harmonic mitigating solutions to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the market. Key players in the harmonic filter industry include-

- ABB (Switzerland)

- Schneider Electric (France)

- Siemens (Germany)

- Emerson Electric Co (U.S.)

- Danfoss A/S (Denmark)

- Schaffner Holding AG (Germany)

- TDK Corporation (Japan)

- Eaton (Ireland)

- Comsys AB (Sweden)

- Baron Power (India)

Harmonic Filter Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 2,713.09 Million |

| CAGR (2025-2032) | 9.0% |

| By Type |

|

| By Phase |

|

| By Voltage |

|

| By Application |

|

| By End Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Harmonic Filter market? +

Harmonic Filter Market Size is estimated to reach over USD 2,713.09 Million by 2032 from a value of USD 1,249.58 Million in 2024 and is projected to grow by USD 1,366.41 Million in 2025, growing at a CAGR of 9.0% from 2025 to 2032.

Which is the fastest-growing region in the Harmonic Filter market? +

Asia-Pacific is the region experiencing the most rapid growth in the market. Key industry leaders prioritize exceptional production standards, frequently highlighting sustainability and energy efficiency. These firms command a significant presence in both local and global markets by engaging in ongoing product innovation, strategic collaborations, and advanced research initiatives. Top manufacturers place a strong emphasis on consumer preferences and shifting market trends, ensuring adherence to regulatory requirements. Their competitive advantage is frequently upheld through substantial investments in research and development, coupled with a dedicated effort to export high-quality products worldwide.

What specific segmentation details are covered in the Harmonic Filter report? +

The harmonic filter report includes specific segmentation details for product type, phase, voltage, application, and end use, and region.

Who are the major players in the Harmonic Filter market? +

The key participants in the market are ABB (Switzerland), Schneider Electric (France), Siemens (Germany), Emerson Electric Co (U.S.), Danfoss A/S (Denmark), Schaffner Holding AG (Germany), TDK Corporation (Japan), Eaton (Ireland), Comsys AB (Sweden), Baron Power (India), and others.