- Summary

- Table Of Content

- Methodology

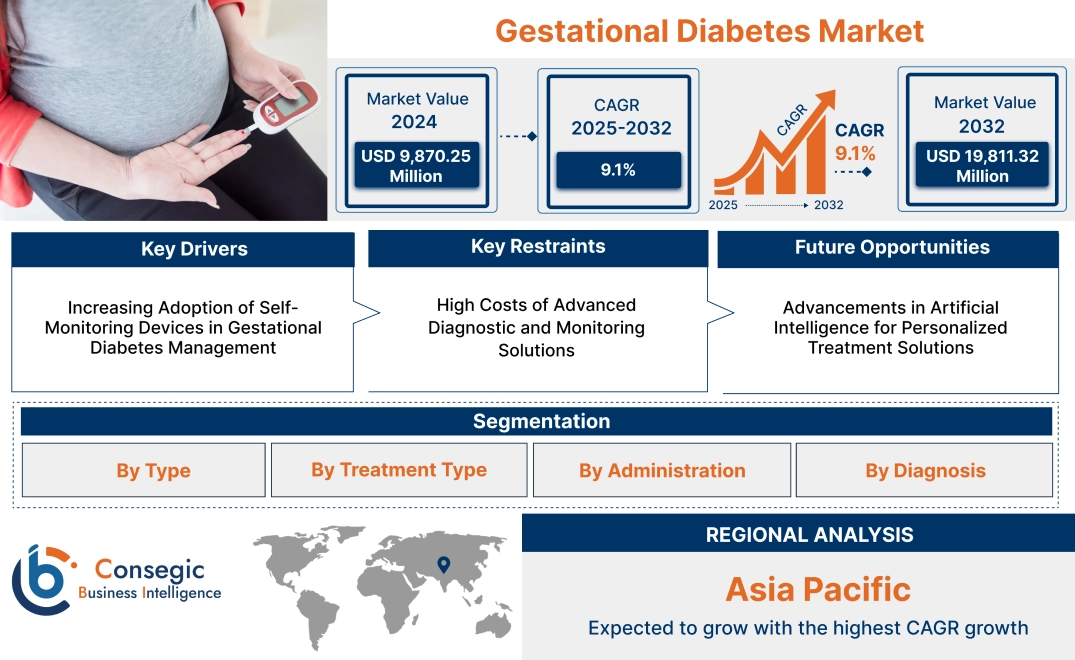

Gestational Diabetes Market Size:

Gestational Diabetes Market size is estimated to reach over USD 19,811.32 Million by 2032 from a value of USD 9,870.25 Million in 2024 and is projected to grow by USD 10,592.57 Million in 2025, growing at a CAGR of 9.1 % from 2025 to 2032.

Gestational Diabetes Market Scope & Overview:

Gestational diabetes is a condition characterized by elevated blood glucose levels during pregnancy, typically affecting women with no prior history of diabetes. It occurs due to hormonal changes that impair insulin function, requiring effective diagnosis, monitoring, and management. Products in this market include diagnostic tools, insulin delivery devices, and glucose monitoring systems. These products offer features such as accurate glucose measurement, real-time data tracking, and enhanced patient convenience. Advanced technologies also support remote monitoring and personalized treatment plans.

The benefits of these solutions include improved maternal and fetal health, reduced pregnancy complications, and better glycemic control. Early detection and management play a crucial role in preventing long-term health risks. Applications span across prenatal care, hospital settings, and home healthcare. End-use industries include hospitals, clinics, diagnostic centers, and healthcare technology providers focused on advancing maternal and neonatal care solutions.

Gestational Diabetes Market Dynamics - (DRO) :

Key Drivers:

Increasing Adoption of Self-Monitoring Devices in Gestational Diabetes Management

The adoption of self-monitoring devices, including continuous glucose monitoring (CGM) systems, has significantly improved the management of gestational diabetes. These devices empower pregnant women to track their glucose levels in real time, ensuring better glycemic control and reducing risks for both mother and child. For example, CGM systems provide alerts for abnormal glucose levels, enabling timely intervention and improved health outcomes.

The rising preference for self-monitoring devices among healthcare professionals and patients is accelerating the gestational diabetes market growth.

Key Restraints:

High Costs of Advanced Diagnostic and Monitoring Solutions

The costs associated with advanced diagnostic tools and monitoring devices limit their accessibility, particularly in low-income regions. These expenses include the purchase price, maintenance, and periodic sensor replacement for devices like CGM systems. For instance, continuous glucose monitors require frequent sensor updates, which can be expensive and are often not covered by insurance.

The financial burden associated with these solutions hampers widespread adoption, restraining the gestational diabetes market growth.

Future Opportunities :

Advancements in Artificial Intelligence for Personalized Treatment Solutions

Artificial intelligence (AI) is expected to revolutionize gestational diabetes management by providing personalized treatment plans based on individual patient data. AI algorithms will analyze glucose patterns, dietary habits, and physical activity levels to recommend tailored interventions. For example, AI-powered applications could suggest specific dietary changes to maintain optimal glucose levels during pregnancy.

The integration of AI into gestational diabetes care is anticipated to create significant opportunities for gestational diabetes market trend, offering innovative and efficient solutions for patients and healthcare providers.

Gestational Diabetes Market Segmental Analysis :

By Type:

Based on type, the gestational diabetes market is segmented into Type A1, Type A2, and Others.

Type A1 accounted for the largest revenue in gestational diabetes market share in 2023.

- Type A1 refers to gestational diabetes that is controlled by diet alone and does not require insulin therapy.

- This category is commonly diagnosed in women whose blood sugar levels can be managed through lifestyle modifications such as diet and exercise.

- The rising awareness and education around lifestyle changes that can help control blood sugar levels are driving the gestational diabetes market demand for Type A1 management.

- The non-invasive approach to managing Type A1 gestational diabetes contributes to its widespread preference, especially among pregnant women.

- Additionally, the growing prevalence of gestational diabetes is further supporting the adoption of Type A1 management as a common treatment approach.

- Therefore, according to gestational diabetes market analysis, the Type A1 segment is expected to maintain its dominance due to its widespread adoption, as it is often managed with diet and exercise modifications, offering a non-invasive option for pregnant women.

Type A2 is anticipated to register the fastest CAGR during the forecast period.

- Type A2 gestational diabetes requires insulin therapy or oral medications in addition to lifestyle management.

- The rise in insulin resistance and metabolic changes during pregnancy contributes to the higher incidence of Type A2 among women with gestational diabetes.

- As healthcare systems become more advanced in managing diabetes, there is an increasing shift toward using insulin and oral anti-diabetic drugs for better control of blood glucose levels in Type A2 cases.

- The use of advanced treatments and the growing understanding of gestational diabetes are key factors driving the rapid trend of Type A2.

- Thus, according to gestational diabetes market analysis, the Type A2 segment is experiencing significant growth, driven by the increasing adoption of insulin therapy and other pharmaceutical treatments for better glucose control in pregnant women.

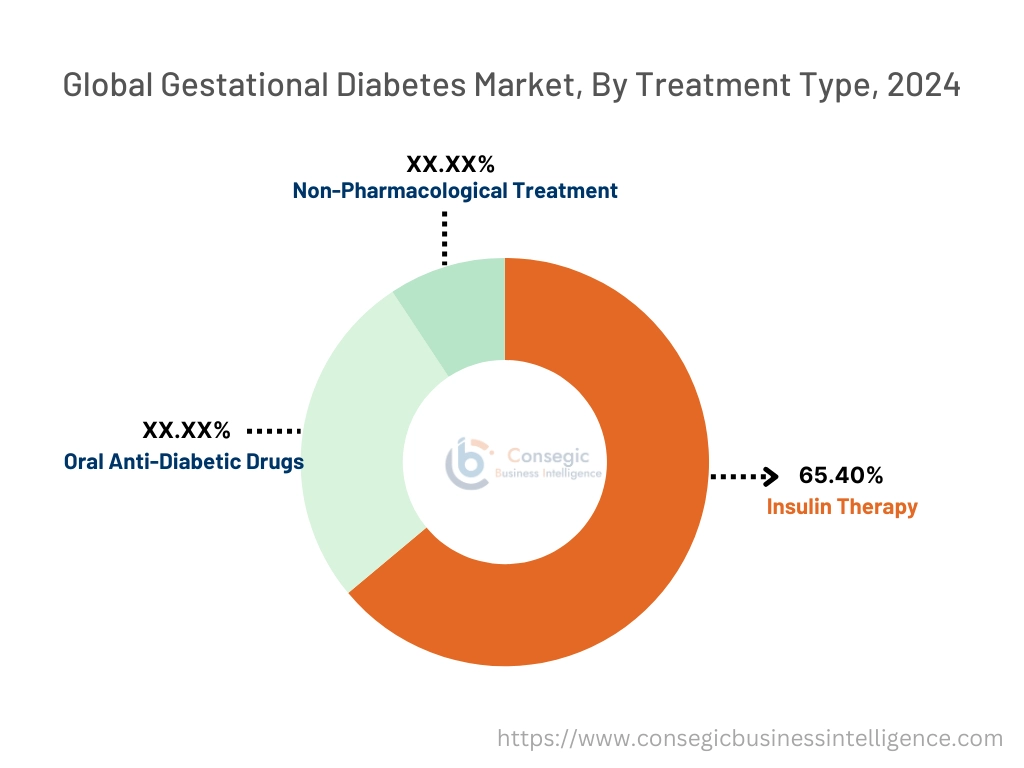

By Treatment Type:

Based on treatment type, the market is segmented into Insulin Therapy, Oral Anti-Diabetic Drugs, and Non-Pharmacological Treatment.

Insulin therapy accounted for the largest revenue of 65.40% in gestational diabetes market share in 2023.

- Insulin therapy involves administering insulin to manage blood sugar levels in women with gestational diabetes who cannot control it through diet or oral medications.

- Insulin is often considered the most effective way to control blood glucose levels, making it a preferred choice for managing more severe cases of gestational diabetes.

- The rising prevalence of gestational diabetes, combined with the effectiveness of insulin therapy in maintaining blood glucose control, is a major factor contributing to its high revenue share in the market.

- Technological advancements in insulin delivery methods, such as insulin pumps and continuous glucose monitoring, are further supporting the trend of this treatment type.

- Therefore, according to market analysis, insulin therapy remains the most widely used treatment for gestational diabetes, owing to its effectiveness in controlling blood sugar in more severe cases.

Oral anti-diabetic drugs are anticipated to register the fastest CAGR during the forecast period.

- Oral anti-diabetic drugs, such as metformin, are increasingly used as a first-line treatment for managing blood sugar levels in women with gestational diabetes.

- These drugs help improve insulin sensitivity and reduce glucose production in the liver, making them an attractive treatment option for those who do not require insulin injections.

- As research advances in non-insulin-based therapies for gestational diabetes, oral anti-diabetic drugs are expected to become a more prominent treatment option.

- Thus, according to market analysis, the increasing adoption of oral anti-diabetic drugs, due to their convenience and efficacy, is driving rapid trend in this segment.

By Administration:

Based on administration, the market is segmented into Oral, Intravenous, and Others.

Oral administration accounted for the largest revenue share in 2023.

- Oral administration involves the use of oral anti-diabetic drugs such as metformin to manage blood glucose levels in gestational diabetes.

- The convenience of oral administration compared to injectable therapies is a significant factor driving the preference for this method among patients.

- As more oral medication options become available for managing gestational diabetes, oral administration is expected to maintain its leading position in the market.

- Therefore, according to market analysis, the oral administration segment holds the largest share due to the ease of use and growing availability of oral medications for managing gestational diabetes.

Intravenous administration is anticipated to register the fastest CAGR during the forecast period.

- Intravenous administration is often used for more severe cases of gestational diabetes where insulin therapy is required for rapid glucose control.

- The growing availability of advanced intravenous insulin therapy methods is contributing to the increased gestational diabetes market demand for this treatment approach in hospitals and clinical settings.

- As healthcare providers focus on more precise and faster control of blood glucose levels during labor and delivery, intravenous insulin therapy is expected to gain traction.

- Thus, according to market analysis, the intravenous administration segment is seeing rapid trend, driven by the need for more immediate and precise glucose control in high-risk gestational diabetes cases.

By Diagnosis:

Based on diagnosis, the market is segmented into Oral Glucose Tolerance Test (OGTT), Fasting Blood Sugar Test, Random Blood Sugar Test, and Hemoglobin A1C Test.

The Oral Glucose Tolerance Test (OGTT) accounted for the largest revenue share in 2023.

- The OGTT is considered the gold standard for diagnosing gestational diabetes, as it provides a clear indication of how well the body processes glucose.

- It involves drinking a glucose solution and measuring blood glucose levels at intervals to determine how the body responds.

- As it remains the most reliable diagnostic test, the demand for the OGTT is expected to remain high, particularly among pregnant women at risk of developing gestational diabetes.

- Therefore, according to market analysis, the Oral Glucose Tolerance Test (OGTT) remains the most commonly used and trusted diagnostic tool for gestational diabetes, ensuring its leading position in the market.

The Hemoglobin A1C Test is anticipated to register the fastest CAGR during the forecast period.

- The Hemoglobin A1C test is used to measure the average blood sugar levels over the past two to three months.

- It is becoming increasingly popular as a diagnostic tool for gestational diabetes due to its ability to assess long-term glucose control, providing a broader picture of blood sugar patterns.

- With growing awareness of diabetes management and early detection, the demand for the A1C test is projected to rise, making it the fastest-growing diagnostic test for gestational diabetes.

- Thus, according to market analysis, the Hemoglobin A1C test is gaining popularity for its ability to measure long-term blood sugar control, driving its rapid adoption in the diagnosis of gestational diabetes.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

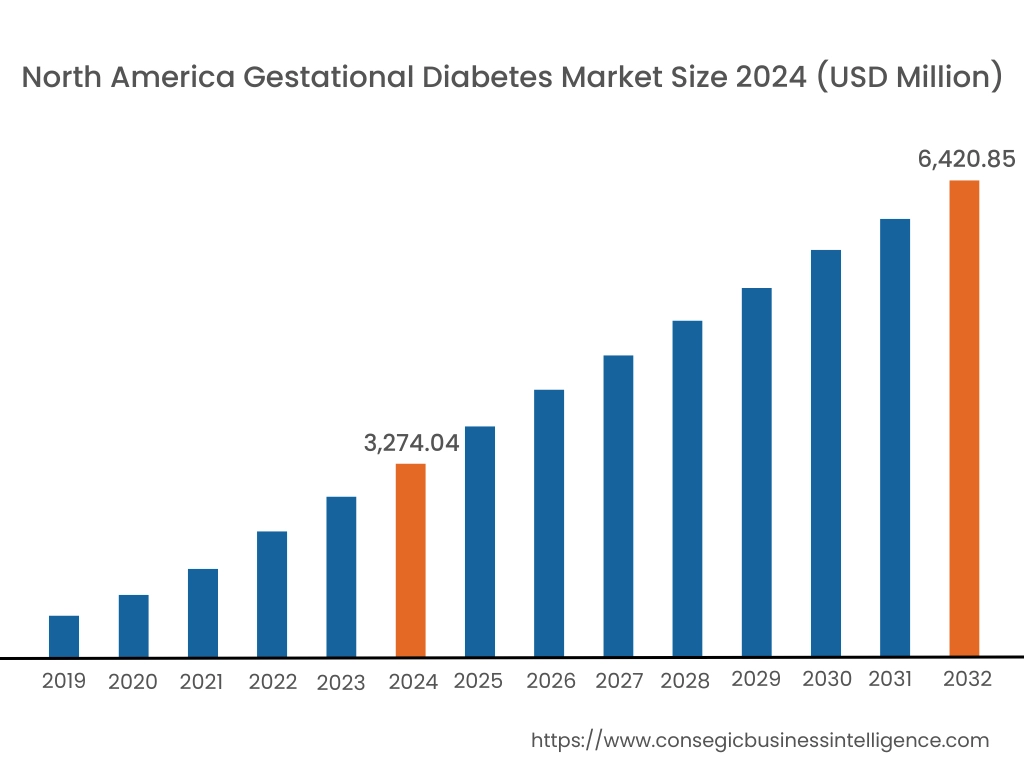

In 2024, North America was valued at USD 3,274.04 Million and is expected to reach USD 6,420.85 Million in 2032. In North America, the U.S. accounted for the highest share of 73.10% during the base year of 2024. The increasing prevalence of gestational diabetes in pregnant women, along with rising awareness of its health implications, has led to a high demand for diagnostic and therapeutic products in the US and Canada. Government initiatives promoting maternal health and the availability of advanced healthcare infrastructure support gestational diabetes market expansion. Furthermore, the growing adoption of personalized healthcare and telemedicine solutions for managing gestational diabetes positively influences market dynamics.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 9.6% over the forecast period. In Asia-Pacific, the gestational diabetes market expansion is notable, driven by rapid urbanization, changes in lifestyle, and a rise in maternal age. Countries like China, India, and Japan contribute significantly to market trend. Increasing awareness about gestational diabetes and its complications has led to higher demand for testing and management solutions. However, the market faces challenges in some developing regions due to limited healthcare infrastructure and lower awareness. Still, the region’s large population and increasing healthcare investments support a positive market outlook.

Europe is a key market for gestational diabetes, with countries such as Germany, France, the UK, and Italy showing strong demand. The region's established healthcare systems and rising awareness about gestational diabetes are crucial factors for market performance. Additionally, the prevalence of obesity and delayed pregnancies in European countries contributes to an increase in gestational diabetes cases. Europe also benefits from stringent healthcare regulations that ensure high-quality diagnostic and therapeutic solutions, further enhancing market growth. The growing gestational diabetes market trend of preventive care and health monitoring among expectant mothers adds to market momentum.

The Middle East and Africa present a mixed performance in the gestational diabetes market. In the Gulf Cooperation Council (GCC) countries like the UAE and Saudi Arabia, rising healthcare access and a focus on maternal health contribute to market growth. However, challenges exist in sub-Saharan Africa due to limited healthcare resources and lower awareness of gestational diabetes. Increasing cases of obesity, especially in the Middle East, further elevate the risk of gestational diabetes, creating a gestational diabetes market opportunity for market expansion. International healthcare organizations are also increasing their focus on improving healthcare access in Africa, which may positively affect the market in the future.

Latin America shows moderate growth in the gestational diabetes market, with Brazil and Mexico leading in demand. The rising incidence of gestational diabetes due to lifestyle changes, increasing obesity rates, and delayed pregnancies has resulted in higher healthcare spending on maternal health. However, disparities in healthcare infrastructure and awareness across countries hinder market development in certain areas. Despite these challenges, the growing adoption of advanced diagnostic methods and healthcare reforms in countries like Brazil support steady market growth.

Top Key Players and Market Share Insights:

The Global Gestational Diabetes Market is highly competitive with major players providing FWA to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the Global Gestational Diabetes Market. Key players in the Gestational Diabetes industry include-

- Novo Nordisk A/S (Denmark)

- Sanofi S.A. (France)

- Merck & Co., Inc. (United States)

- Johnson & Johnson (United States)

- Medtronic PLC (Ireland)

- Bristol-Myers Squibb (United States)

- Eli Lilly and Co. (United States)

- Bayer AG (Germany)

- GlaxoSmithKline plc (United Kingdom)

- Abbott Laboratories (United States)

Gestational Diabetes Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 19,811.32 Million |

| CAGR (2025-2032) | 9.1% |

| By Type |

|

| By Treatment Type |

|

| By Administration |

|

| By Diagnosis |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Gestational Diabetes Market? +

In 2024, the Gestational Diabetes Market was USD 9,870.25 million.

What will be the potential market valuation for the Gestational Diabetes Market by 2032? +

In 2032, the market size of Gestational Diabetes Market is expected to reach USD 19,811.32 million.

What are the segments covered in the Gestational Diabetes Market report? +

The treatment type, diagnosis, product type, distribution channel, and end-user industry are the segments covered in this report.

Who are the major players in the Gestational Diabetes Market? +

Novo Nordisk A/S (Denmark), Sanofi S.A. (France), Bristol-Myers Squibb (United States), Eli Lilly and Co. (United States), Bayer AG (Germany), GlaxoSmithKline plc (United Kingdom), Abbott Laboratories (United States), Merck & Co., Inc. (United States), Johnson & Johnson (United States), Medtronic PLC (Ireland) are the major players in the Gestational Diabetes market.