- Summary

- Table Of Content

- Methodology

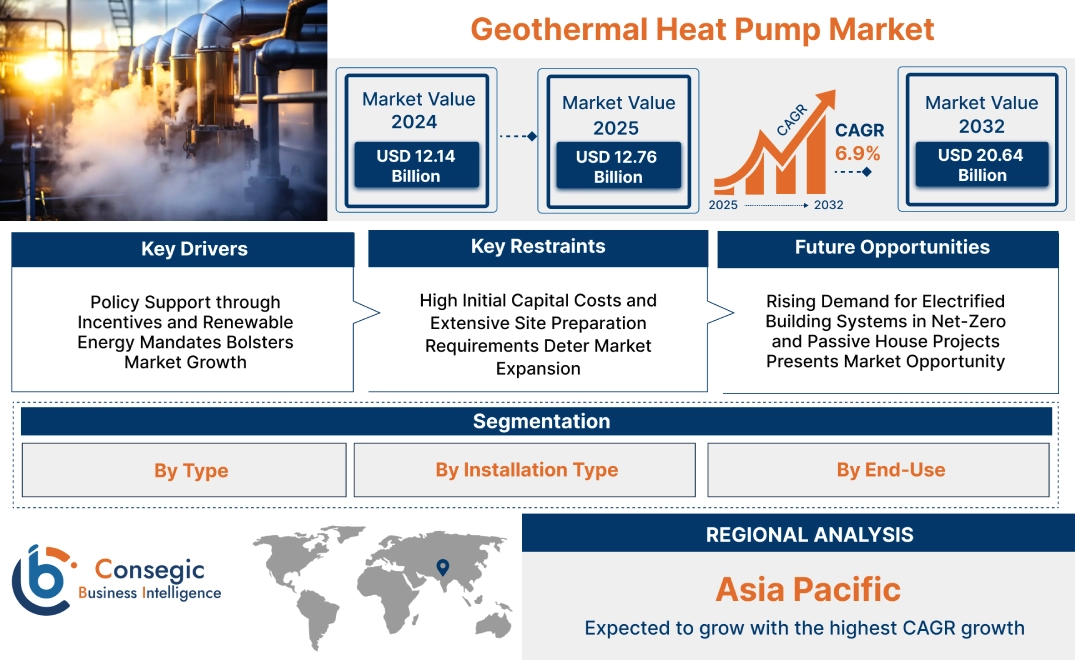

Geothermal Heat Pump Market Size:

Geothermal Heat Pump Market size is estimated to reach over USD 20.64 Billion by 2032 from a value of USD 12.14 Billion in 2024 and is projected to grow by USD 12.76 Billion in 2025, growing at a CAGR of 6.9% from 2025 to 2032.

Geothermal Heat Pump Market Scope & Overview:

A geothermal heat pump is a ground-source heating and air conditioning system that exploits the planet's reliable subsurface temperature to provide energy-efficient heating and cooling for buildings. It works by passing fluid in underground loops, transferring thermal energy to or from interior spaces based on seasonal requirements.

Major features encompass high operational efficiency, low maintenance needs, and low emissions during operation. The system comprises ground heat exchangers, heat pumps, and distribution units, with long life and stable temperature control. Compatibility with radiant floor systems or forced-air ducts enables wide application in residential, commercial, and institutional settings.

Geothermal heat pump systems achieve cost savings over the long term, lower energy consumption, and enhanced indoor comfort. Their adaptability in new building applications and retrofits accommodates various architectural requirements, and hence, they are an efficient and environmentally friendly option for today's climate control systems. Their closed-loop or open-loop design offers site-specific requirements adaptability.

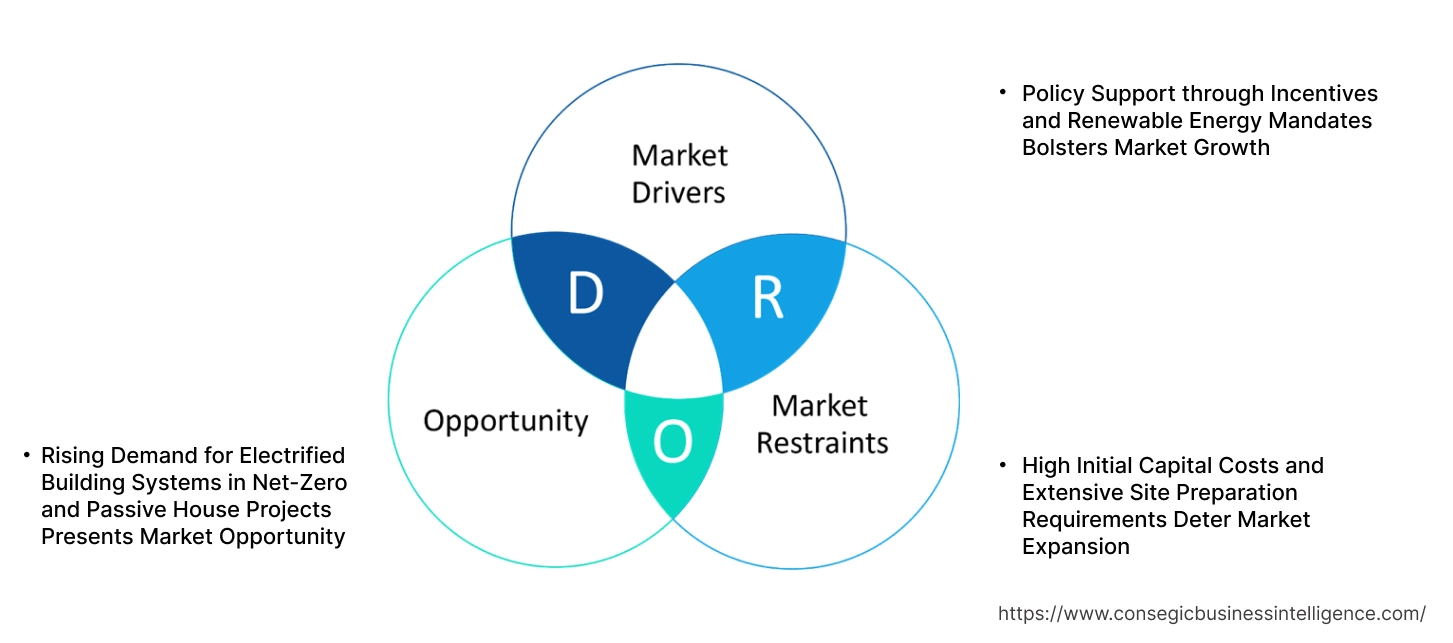

Geothermal Heat Pump Market Dynamics - (DRO):

Key Drivers:

Policy Support through Incentives and Renewable Energy Mandates Bolsters Market Growth

Tax credits, low-interest loans, and rebates lower upfront costs, accelerating adoption in green developments. U.S., Canadian, and European building codes are changing to include requirements for enhanced energy performance and carbon neutrality, where geothermal systems are seen as a compliant solution. Municipalities are also encouraging ground-source installations in public buildings and low-income housing initiatives to achieve decarbonization objectives. Such financial instruments and regulatory requirements enhance market visibility and investment returns, particularly in long-lifecycle projects. With institutional developers and private builders reacting to such changing norms, demand for low-emission thermal systems is picking up pace in new builds and large-scale retrofit projects. These government-sponsored programs are proving to be an important facilitator of the geothermal heat pump market expansion.

Key Restraints:

High Initial Capital Costs and Extensive Site Preparation Requirements Deter Market Expansion

The capital cost of installation for geothermal systems is still a key limitation to wider uptake. Deep drilling for boreholes, trenching for horizontal loops, and geotechnical surveys all significantly increase the cost of a system relative to air-source or conventional HVAC options. Rocky ground conditions or elevated water tables add technical difficulty and prolong project schedules. Small-scale builders and individual property owners tend to find these costs difficult to absorb without incentives. Even in commercial building, the additional design coordination and space allocation needs are hindrances. Growing need for green HVAC solutions is met by frequently being undercut by cost limitations that slow up adoption. All these factors combine to limit deployment in cost-sensitive markets and hinder conversion from traditional heating systems. Therefore, high upfront cost and land preparation needs continue to be central restraints to geothermal heat pump market growth.

Future Opportunities:

Rising Demand for Electrified Building Systems in Net-Zero and Passive House Projects Presents Market Opportunity

The shift to net-zero and all-electric buildings is placing geothermal heat pumps at the forefront of foundation technologies in next-generation HVAC strategies. The systems support high-efficiency space conditioning and domestic hot water supply while conforming to Passive House and LEED certification standards. Developers and architects are increasingly specifying ground-source systems for high-performance buildings to meet operational carbon neutrality and qualify for financing tied to sustainability. Inclusion of geothermal technology with solar PV and energy storage also promotes system resilience and energy independence. Expansion in green real estate, carbon-neutral procurement of infrastructure through public procurement, and ESG-driven investments is driving adoption among multifamily apartments, university campuses, and institutional buildings. As electrification enters the mainstream of climate policy, geothermal options are becoming strategic in building planning and mechanical engineer specifications. These circumstances are creating long-term geothermal heat pump market opportunities stimulated by regulatory convergence and sustainable growth-oriented activities.

Geothermal Heat Pump Market Segmental Analysis :

By Type:

Based on type, the market is divided into closed-loop systems and open-loop systems.

The closed-loop systems segment accounted for the largest geothermal heat pump market share in 2024.

- Closed-loop systems dominate due to their lower maintenance and long-term reliability, particularly in residential and commercial applications.

- Vertical closed-loop systems are preferred in urban settings with limited land availability, offering higher energy efficiency through deep boreholes.

- Horizontal closed-loop systems are widely used in suburban and rural installations, given their relatively low installation cost and ease of deployment.

- According to geothermal heat pump market analysis, the pond/lake loops are leveraged in regions with accessible water bodies to reduce drilling costs and improve heat exchange efficiency.

The open-loop systems segment is projected to grow at the fastest CAGR during the forecast period.

- Open-loop systems offer higher thermal efficiency due to direct exchange with groundwater, minimizing the need for extensive piping or ground excavation.

- These systems are gaining traction in agricultural and industrial facilities where water sources are readily available and regulations permit discharge.

- Open-loop configurations enable substantial cost savings over time due to reduced pumping and circulation energy requirements.

- The rising need for high-performance HVAC solutions in large commercial facilities is expected to support open-loop adoption, driving geothermal heat pump market expansion.

By Installation Type:

Based on installation type, the market is bifurcated into new installations and retrofits.

New installations captured the largest revenue share in 2024.

- New constructions in energy-efficient residential and commercial buildings integrate geothermal systems as part of green building codes and incentives.

- Builders are increasingly incorporating geothermal designs into HVAC planning due to lower lifecycle costs and LEED certification benefits.

- Regions with supportive government rebates and tax incentives, such as the U.S. and parts of Europe, are witnessing higher need for new geothermal system installations.

- According to geothermal heat pump market trends, public infrastructure projects focused on sustainability are propelling this segment forward.

The retrofit segment is anticipated to witness the highest growth rate during the forecast period.

- Aging HVAC infrastructure in developed regions is driving retrofit installations of geothermal systems to improve energy efficiency and lower emissions.

- Commercial buildings seeking to upgrade to low-carbon heating and cooling solutions contribute to rising retrofit activity.

- Technological advancements in drilling, modular loop systems, and compact heat exchangers are making retrofits more feasible in space-constrained areas.

- As per geothermal heat pump market analysis, retrofitting aligns with global decarbonization goals, encouraging funding and regulatory support.

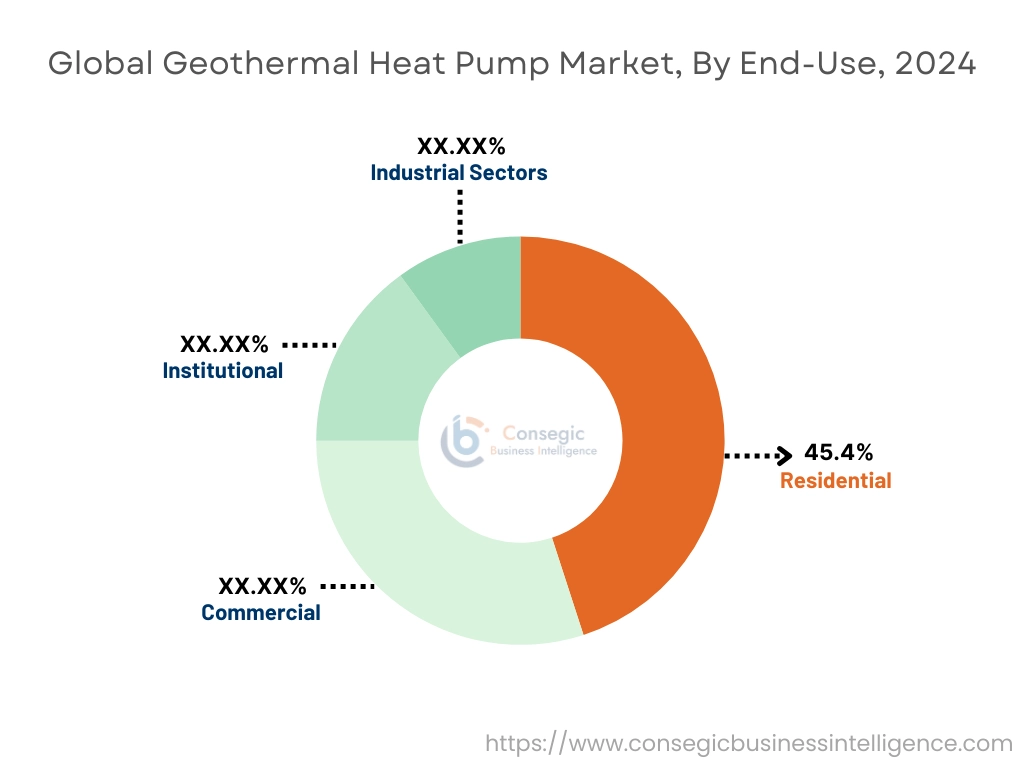

By End-Use:

Based on end-use, the market is segmented into residential, commercial, institutional, and industrial sectors.

The residential segment held the largest geothermal heat pump market share of 45.4% in 2024.

- Residential adoption is driven by rising energy costs, homeowner awareness of geothermal efficiency, and long-term cost savings.

- Incentives for home energy upgrades, including tax credits and rebates, are fueling the installation of geothermal heat pumps in single and multi-family homes.

- Demand is further supported by developments in noise-reduced and compact systems tailored for residential usage.

- The proliferation of net-zero and passive housing standards in residential settings is driving the geothermal heat pump market growth.

The commercial segment is projected to register the fastest CAGR over the forecast period.

- Large-scale HVAC requirements in office spaces, hotels, and retail complexes are leading to higher penetration of geothermal technologies.

- System scalability, load-sharing capabilities, and low operating costs make geothermal heat pumps suitable for high-occupancy commercial buildings.

- Integration with building automation systems and IoT-based controls is enhancing operational efficiency and occupant comfort.

- This heating system is being increasingly incorporated into university campuses, resulting in cost savings for the colleges and universities, which are then able to offer lower tuition fees and more student scholarships.

- According to geothermal heat pump market trends, the commercial sector is increasingly adopting sustainable heating and cooling, contributing to robust market growth.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

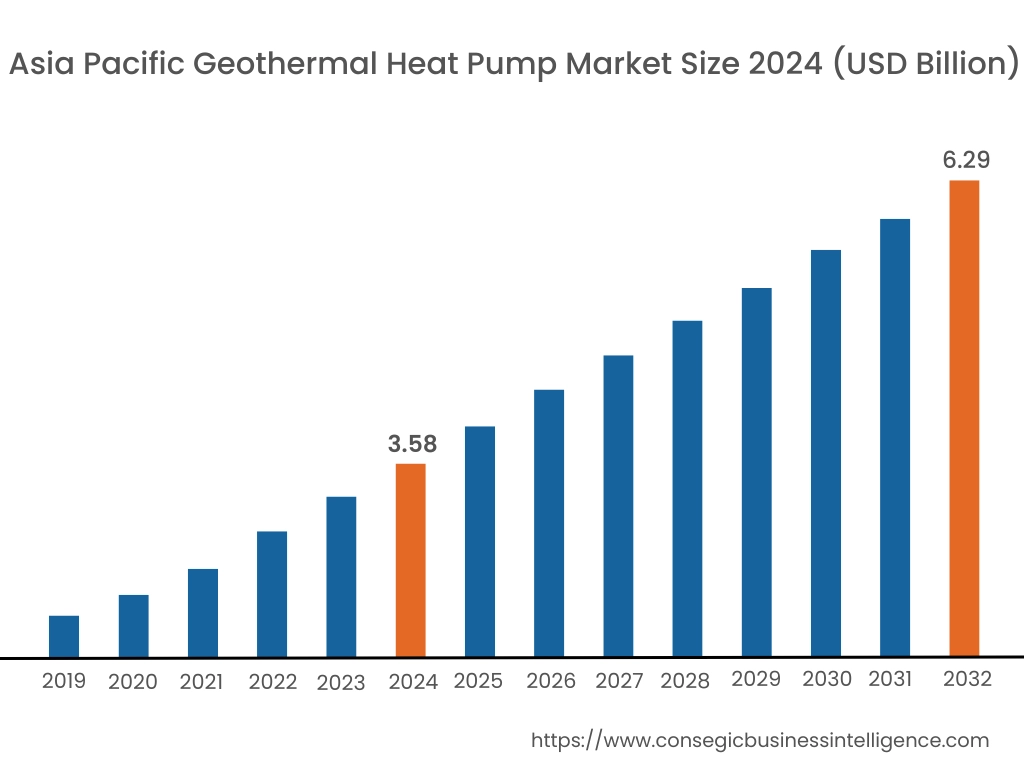

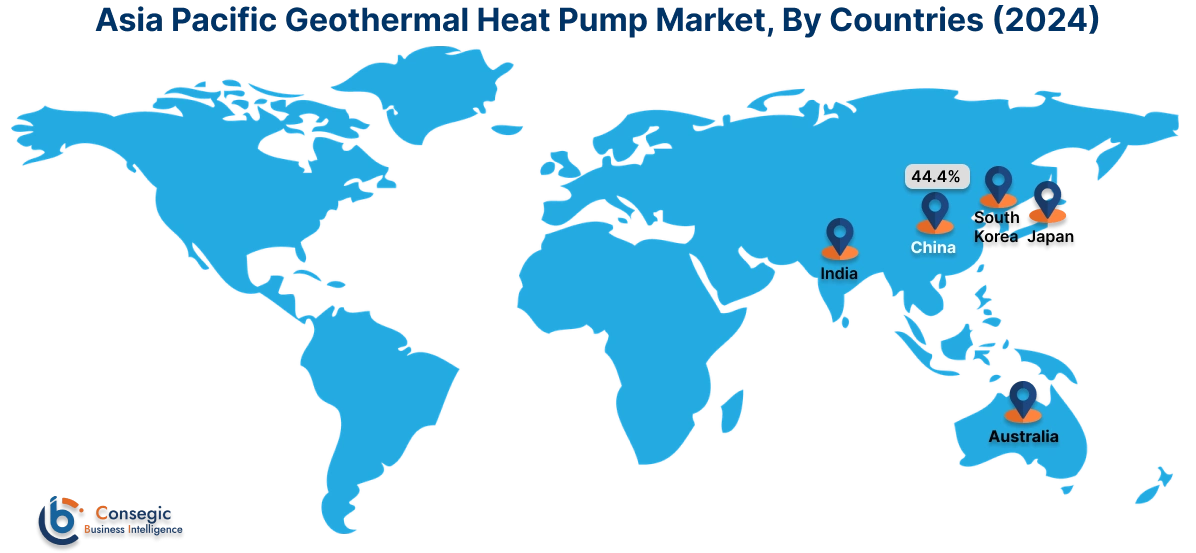

Asia Pacific region was valued at USD 3.58 Billion in 2024. Moreover, it is projected to grow by USD 3.77 Billion in 2025 and reach over USD 6.29 Billion by 2032. Out of this, China accounted for the maximum revenue share of 44.4%. Asia-Pacific is experiencing rapid growth, led by an increase in urbanization, concerns regarding energy security, and state-supported programs aimed at encouraging clean heating technologies. China, South Korea, Japan, and Australia are witnessing high installations, especially in commercial complexes, smart cities, and schools. Analysis of the region identifies growing demand for district-based systems as well as pilot programs linking geothermal with solar-supported technologies. While high initial cost and geologic mapping pose challenges, policy-driven requirement and emphasis on diminishing air pollution drive adoption. The region's increasing real estate presence and good investment in renewable infrastructure provide solid potential for future deployment.

North America is estimated to reach over USD 6.69 Billion by 2032 from a value of USD 4.03 Billion in 2024 and is projected to grow by USD 4.22 Billion in 2025. The region represents a mature market supported by strong environmental regulation and federal and state-level subsidies for sustainable building practices. The United States and Canada are at the forefront of system installations in residential subdivisions, commercial campuses, and public infrastructure projects. Analysis indicates that increasing electrification of heating, particularly in cold-weather zones, is driving interest in geothermal systems as a long-term solution to lower fossil fuel reliance. Moreover, the presence of established drilling expertise and heat pump manufacturers has enabled cost-effective deployment of such technologies. Rising awareness of lifetime savings and indoor comfort benefits continues to enhance the geothermal heat pump market demand across the nations.

Europe is a global leader in the geothermal heat pump industry, driven by ambitious decarbonization goals, climate-conscious building regulations, and high energy costs. Germany, Sweden, Switzerland, and the Netherlands have integrated ground-source systems into residential, commercial, and municipal developments. Detailed analysis reveals a strong shift toward low-temperature heating networks, where geothermal systems are combined with radiant floor heating and thermal storage. Incentive schemes supporting the retrofitting of older buildings and the preference for renewable heat in social housing projects contribute to long-term growth. The region’s emphasis on lowering operational emissions is a significant geothermal heat pump market opportunity for technology providers offering hybrid and high-efficiency solutions.

The geothermal heat pump adoption in Latin America remains at the nascent stage but is expanding in certain areas with suitable geothermal prospects and policy interest. Chile and Mexico have begun geothermal development zones for more general energy uses, with spillover value potential for building-scale heating and cooling systems. It is considered by analysis that healthcare, tourism, and government facilities are expected to be among the early adopters in temperate climates. Growing green building certifications and public-private partnerships could become crucial to meeting demand. But sustainable growth will depend on growing investment in ground-source feasibility studies and worker training programs.

The Middle East and Africa market offers a niche but developing geothermal heat pump market, especially in high-altitude or seasonally cold areas in Turkey, Iran, and South Africa. Although air-based systems are the prevalent option because of cost and ease, increasing electricity prices and the desire for off-grid applications are gradually drawing attention to geothermal solutions. Analysis identifies pilot installations in institutional and research-based facilities where steady heating and cooling are essential. With global partnerships and knowledge transfer, the demand for geothermal heat pumps can increase in line with overall renewable energy adoption strategies.

Top Key Players & Market Share Insights:

The geothermal heat pump market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global geothermal heat pump market. Key players in the geothermal heat pump industry include –

- Bosch Thermotechnology (Germany)

- Viessmann Group (Germany)

- NIBE Industrier AB (Sweden)

- Vaillant Group (Germany)

- Groupe Atlantic (France)

- OCHSNER Wärmepumpen GmbH (Austria)

- Trane Technologies plc (Ireland)

- Carrier Global Corporation (USA)

- Mitsubishi Electric Corporation (Japan)

- Stiebel Eltron GmbH & Co. KG (Germany)

Recent Industry Developments :

Acquisitions:

- In February 2025, Swegon acquired American Geothermal, a USA heat pump and chiller manufacturer. This acquisition enables the entry of the Swedish company into the North American market and expands their manufacturing capabilities and expertise.

Brand Consolidation:

- In January 2025, Enertech Global, a leading manufacturer of geothermal heating and cooling solutions, announced a strategic brand consolidation where its four brands, Enertech, GeoComfort, Hydron Module, and TETCO, will be consolidated into two unified brands of Enertech and GeoComfort by Enertech.

Partnerships:

- In April 2025, Dandelion Energy, a leading home geothermal heating and cooling company, announced a partnership with Lennar Corporation, a leading homebuilder company. This collaboration aims to establish the framework to make geothermal heating and cooling the standard in new home constructions. Dandelion Energy developed a streamlined installation process to improve the affordability and accessibility of geothermal heat pumps.

Geothermal Heat Pump Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 20.64 Billion |

| CAGR (2025-2032) | 6.9% |

| By Type |

|

| By Installation Type |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Geothermal Heat Pump Market? +

Geothermal Heat Pump Market size is estimated to reach over USD 20.64 Billion by 2032 from a value of USD 12.14 Billion in 2024 and is projected to grow by USD 12.76 Billion in 2025, growing at a CAGR of 6.9% from 2025 to 2032.

What specific segmentation details are covered in the Geothermal Heat Pump Market report? +

The Geothermal Heat Pump market report includes specific segmentation details for type, installation type and end-use.

What are the end-use of the Geothermal Heat Pump ? +

The end-use of Geothermal Heat Pump are residential, commercial, industrial and institutional.

Who are the major players in the Geothermal Heat Pump Market? +

The key participants in the Geothermal Heat Pump market are Bosch Thermotechnology (Germany), Viessmann Group (Germany), OCHSNER Wärmepumpen GmbH (Austria), Trane Technologies plc (Ireland), Carrier Global Corporation (USA), Mitsubishi Electric Corporation (Japan), Stiebel Eltron GmbH & Co. KG (Germany), NIBE Industrier AB (Sweden), Vaillant Group (Germany) and Groupe Atlantic (France).