- Summary

- Table Of Content

- Methodology

Full Service Carrier Market Size:

Full Service Carrier Market size is estimated to reach over USD 479.21 Billion by 2032 from a value of USD 310.85 Billion in 2024 and is projected to grow by USD 322.59 Billion in 2025, growing at a CAGR of 5.6% from 2025 to 2032.

Full Service Carrier Market Scope & Overview:

A full service carrier refers to an airline that offers a comprehensive range of services to passengers, including in-flight meals, entertainment, checked baggage, and premium seating options. These carriers operate on domestic and international routes, catering to both economy and premium-class travelers. The focus of these airlines is to provide a seamless and comfortable travel experience, with additional amenities and customer support throughout the journey.

Full service carriers often operate through hub-and-spoke models, connecting major cities and regional destinations. They provide multiple class options, such as economy, business, and first class, to meet the varying needs of passengers. These carriers also offer frequent flyer programs and lounge access to enhance passenger loyalty and convenience.

End-users of full service carriers include business travelers, leisure tourists, and individuals requiring long-haul or international travel options. These airlines play a vital role in the aviation industry by offering reliable and comprehensive services for diverse passenger needs.

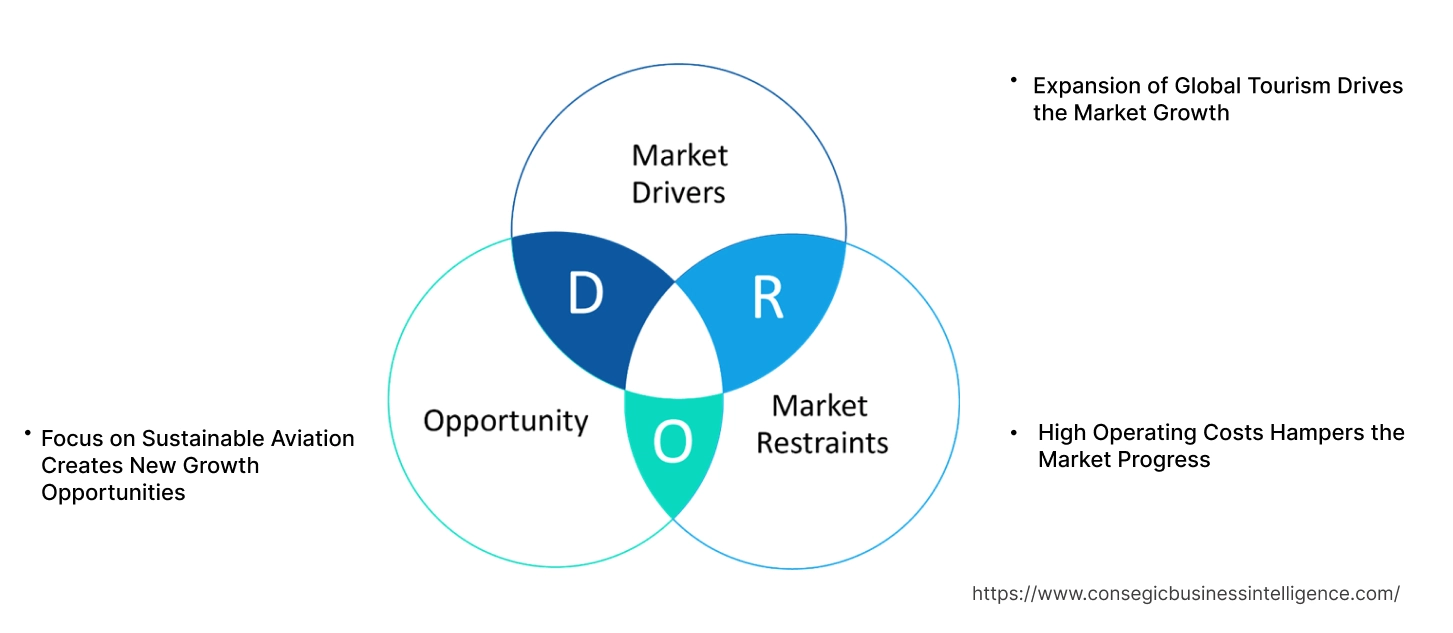

Full Service Carrier Market Dynamics - (DRO) :

Key Drivers:

Expansion of Global Tourism Drives the Market Growth

The rise in international tourism is significantly boosting the airline industry, with full-service carriers playing a crucial role in catering to this growing demand. Popular tourist destinations in regions such as Asia-Pacific, Europe, and the Middle East are experiencing a surge in traveler arrivals, driven by increased disposable incomes and relaxed travel restrictions.

Full-service airlines capitalize on this trend by offering seamless connectivity, comprehensive luggage handling, and premium travel perks like in-flight entertainment and gourmet meals. These features ensure a superior travel experience, making them the preferred choice for long-haul and international travelers. Additionally, the ability of full-service carriers to provide efficient connections across multiple destinations enhances convenience for tourists, further driving their appeal. As tourism continues to grow globally, full-service airlines are poised to benefit by aligning their offerings with the needs of leisure and business travelers, driving the full service carrier market growth.

Key Restraints:

High Operating Costs Hampers the Market Progress

The aviation industry operates under stringent safety regulations, which govern the design, testing, and

Operating a full-service airline involves substantial costs across various domains, including fuel, aircraft maintenance, staffing, and advanced technology integration. Aviation fuel, a major expense for airlines, is subject to price volatility, adding financial pressure. Additionally, full-service carriers must comply with stringent regulatory standards concerning safety, emissions, and operational procedures, which further increase expenditures.

The need for highly trained personnel, from pilots to cabin crew, alongside investments in premium in-flight amenities and ground services, drives up overall operating costs. These financial constraints are exacerbated by competition from low-cost carriers that attract price-sensitive passengers with budget-friendly fares. For full-service airlines, maintaining a balance between offering superior services and staying competitively priced is increasingly difficult. Rising operating costs not only strain profitability but also limit flexibility in pricing strategies, posing significant restraints in sustaining market share in the competitive aviation sector. Thus, the aforementioned factors limit the full service carrier market demand.

Future Opportunities :

Focus on Sustainable Aviation Creates New Growth Opportunities

The increasing awareness of climate change and environmental sustainability is prompting airlines to adopt greener practices. Full-service carriers are leveraging their resources to implement sustainable aviation fuels (SAFs), energy-efficient aircraft, and carbon offset programs. These initiatives align with the growing preference of eco-conscious travelers who prioritize environmentally responsible travel options. Moreover, stringent regulations on emissions and the push for achieving net-zero carbon goals further encourage carriers to invest in sustainable aviation practices.

By adopting SAFs and reducing their carbon footprint, airlines not only enhance their brand reputation but also comply with global environmental standards. These efforts position these carriers as leaders in sustainable aviation, creating significant full service carrier market opportunities to capture a loyal customer base while contributing to a more sustainable future for air travel.

Full Service Carrier Market Segmental Analysis :

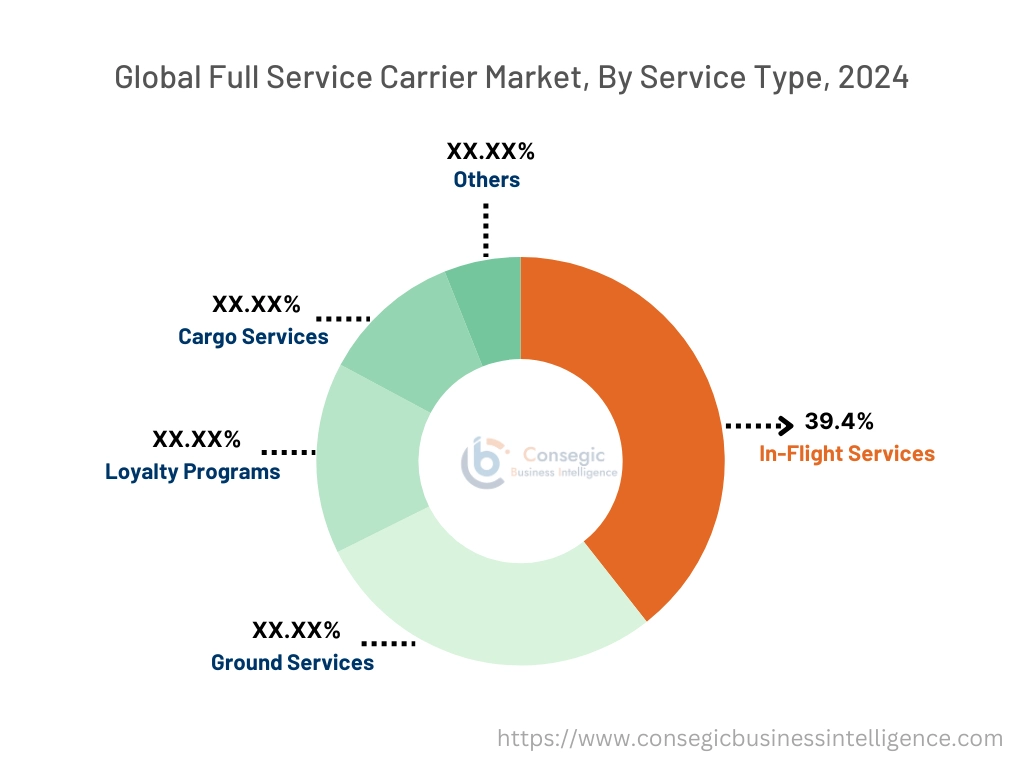

By Service Type:

Based on service type, the market is segmented into in-flight services, ground services, loyalty programs, cargo services, and others.

The in-flight services segment accounted for the largest revenue of 39.4% of the total full service carrier market share in 2024.

- Enhanced passenger experiences, including entertainment systems, meal services, and Wi-Fi connectivity, drive the prominence of in-flight services.

- Airlines are investing in premium in-flight amenities, such as personalized dining and seating comfort, to cater to diverse customer preferences.

- The dominance of this segment reflects the significant role of in-flight services in building brand loyalty and increasing customer retention.

- As per full service carrier market analysis, advancements in technology, including real-time flight tracking and connectivity, further boost the significance of in-flight services.

The loyalty programs segment is expected to register the fastest CAGR during the forecast period.

- Airlines are focusing on expanding loyalty program features, including partnership rewards and personalized benefits, to attract frequent travelers.

- Growth in competition among carriers encourages the introduction of innovative and flexible loyalty schemes tailored to customer preferences.

- The rising adoption of digital platforms for managing loyalty points enhances accessibility and transparency, boosting customer satisfaction.

- As per the full service carrier market trends, loyalty programs are evolving into essential tools for driving customer engagement and fostering long-term relationships.

By Aircraft Type:

Based on aircraft type, the market is segmented into fixed-wing aircraft and rotary-wing aircraft.

The fixed-wing aircraft segment held the largest revenue of the total full service carrier market share in 2024.

- Fixed-wing aircraft are widely used for long-haul and high-capacity routes, making them essential for full-service carriers.

- The dominance of this segment is attributed to the operational efficiency and range capabilities of fixed-wing aircraft.

- Airlines are increasingly incorporating advanced fixed-wing models to enhance fuel efficiency and passenger comfort.

- As per market analysis, the role of fixed-wing aircraft in connecting international and domestic destinations underpins its market leadership, contributing to the full service carrier market expansion.

The rotary-wing aircraft segment is projected to grow at the fastest CAGR during the forecast period.

- Rotary-wing aircraft are increasingly adopted for niche applications, including regional connectivity, cargo services, and emergency medical services.

- The flexibility and accessibility of rotary-wing aircraft make them suitable for operations in remote and challenging terrains.

- Rising demand for personalized and exclusive travel experiences contributes to the segment’s significant growth potential.

- Market trends indicate increasing investments in advanced rotary-wing models with enhanced safety and comfort features, which further fuels the full service carrier market growth.

By Route Type:

Based on route type, the market is segmented into domestic routes and international routes.

The domestic routes segment accounted for the largest revenue share in 2024.

- Domestic routes cater to a high volume of passengers, particularly in densely populated regions, ensuring consistent market demand.

- Airlines prioritize frequent and cost-effective domestic flights to enhance accessibility and convenience for travelers.

- The dominance of this segment is driven by regional connectivity initiatives and infrastructure development in emerging economies.

- As per industry analysis, the integration of smaller aircraft for domestic routes enhances efficiency and reduces operational costs, fueling the full service carrier market demand.

The international routes segment is expected to register the fastest CAGR during the forecast period.

- International routes benefit from rising global tourism and increasing business travel across continents.

- Enhanced service offerings, including luxury amenities and long-haul connectivity, attract premium travelers to international routes.

- Strategic alliances and codeshare agreements among carriers strengthen the network and accessibility of international routes.

- As per market trends, advancements in aircraft technology, including ultra-long-range models, further bolster the growth of international travel, creating significant full service carrier market opportunities.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

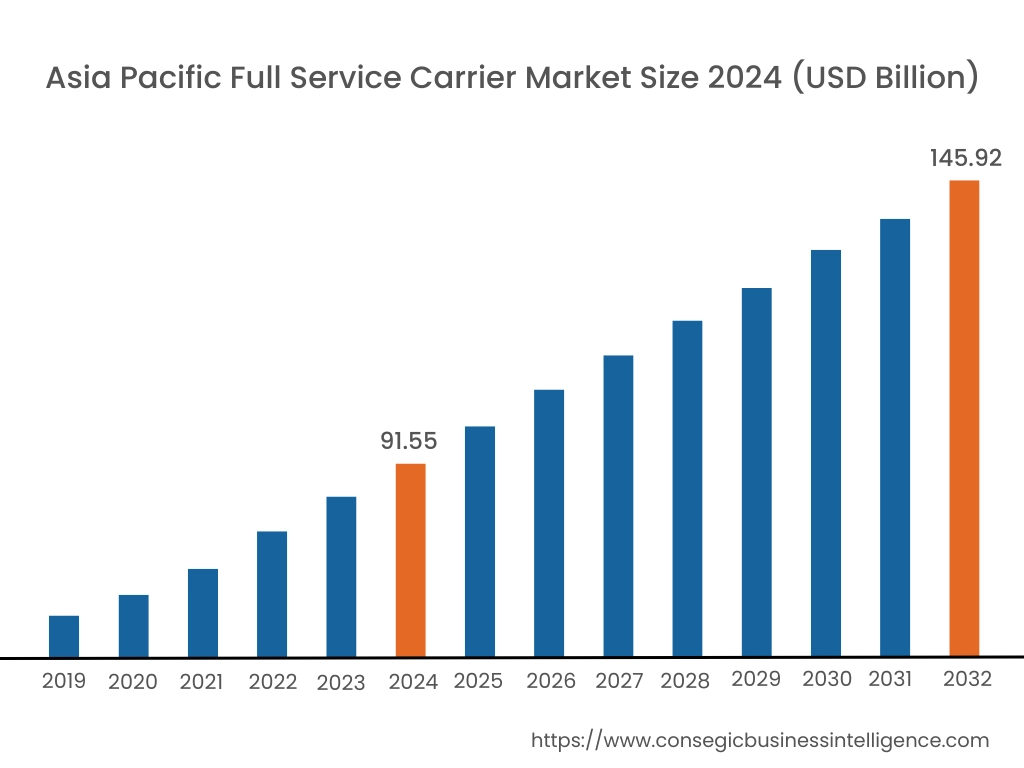

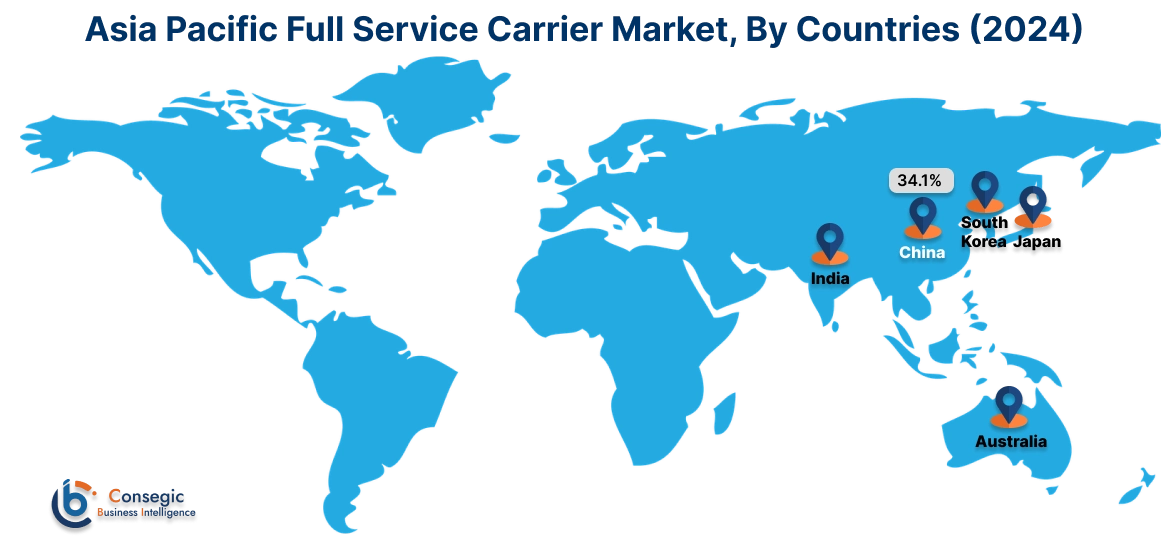

Asia Pacific region was valued at USD 91.55 Billion in 2024. Moreover, it is projected to grow by USD 95.28 Billion in 2025 and reach over USD 145.92 Billion by 2032. Out of this, China accounted for the maximum revenue share of 34.1%. Asia-Pacific is the fastest-evolving region, with significant activity from airlines like Singapore Airlines, Cathay Pacific, and ANA. Trends in expanding international networks and incorporating luxury services in business and first-class cabins are prominent in countries like China, Japan, and India. The analysis also points to increased competition among carriers to capture the rising number of passengers opting for full-service experiences, particularly on routes connecting Asia to Europe and North America.

North America is estimated to reach over USD 155.31 Billion by 2032 from a value of USD 103.11 Billion in 2024 and is projected to grow by USD 106.80 Billion in 2025. North America dominates the full service carrier market, with significant operational focus on enhancing passenger experience and integrating advanced digital technologies. The United States leads the region, emphasizing trends such as premium cabin upgrades, loyalty programs, and digital check-in processes. Canada also contributes through increased connectivity between domestic and international destinations. The analysis highlights how the competitive landscape is shaped by alliances like Oneworld and Star Alliance, offering seamless global connectivity and premium services, boosting the full service carrier market expansion.

Europe remains a key region for the full service carrier market, driven by the presence of legacy airlines such as Lufthansa, British Airways, and Air France. The region is focused on trends in eco-friendly initiatives, including fuel-efficient aircraft and carbon offset programs. The full service carrier market analysis indicates a strong push toward modernizing fleets and enhancing onboard amenities, particularly on long-haul routes. Additionally, government regulations around environmental sustainability are influencing operational strategies in this market.

The Middle East, led by carriers such as Emirates, Qatar Airways, and Etihad Airways, is a major hub for full service carriers, focusing on connecting global destinations via centralized hubs. The analysis highlights trends in offering ultra-long-haul flights and world-class in-flight services. In Africa, the market is gradually expanding, with airlines like Ethiopian Airlines adopting strategies to improve passenger experiences and connect key international destinations.

Latin America’s full service carrier market is influenced by key players like LATAM Airlines and Avianca, which are enhancing their offerings to compete on international routes. The analysis reveals trends in modernizing fleets and optimizing service quality to attract business and leisure travelers. As per the full service carrier market trends, partnerships with global alliances have strengthened connectivity across continents, enabling carriers to expand their customer base and improve service standards.

Top Key Players and Market Share Insights:

The Full Service Carrier market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Full Service Carrier market. Key players in the Full Service Carrier industry include -

- American Airlines Group (USA)

- Delta Air Lines (USA)

- Cathay Pacific Airways (Hong Kong)

- Singapore Airlines (Singapore)

- Qatar Airways (Qatar)

- United Airlines Holdings, Inc. (USA)

- Lufthansa Group (Germany)

- Air France-KLM (France)

- British Airways (International Airlines Group) (UK)

- Emirates (UAE)

Full Service Carrier Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 479.21 Billion |

| CAGR (2025-2032) | 5.6% |

| By Service Type |

|

| By Aircraft Type |

|

| By Route Type |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Full Service Carrier Market? +

The Full Service Carrier Market size is estimated to reach over USD 479.21 Billion by 2032 from a value of USD 310.85 Billion in 2024 and is projected to grow by USD 322.59 Billion in 2025, growing at a CAGR of 5.6% from 2025 to 2032.

What are the key segments in the Full Service Carrier Market? +

The market is segmented by service type (in-flight services, ground services, loyalty programs, cargo services, others), aircraft type (fixed-wing aircraft, rotary-wing aircraft), route type (domestic routes, international routes), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which segment is expected to grow the fastest in the Full Service Carrier Market? +

The loyalty programs segment is expected to register the fastest CAGR during the forecast period, driven by the growing competition among carriers and the rising importance of customer engagement and retention through flexible and innovative loyalty schemes.

Who are the major players in the Full Service Carrier Market? +

Major players in the Full Service Carrier market include American Airlines Group (USA), Delta Air Lines (USA), United Airlines Holdings, Inc. (USA), Lufthansa Group (Germany), Air France-KLM (France), British Airways (UK), Emirates (UAE), Cathay Pacific Airways (Hong Kong), Singapore Airlines (Singapore), and Qatar Airways (Qatar).