- Summary

- Table Of Content

- Methodology

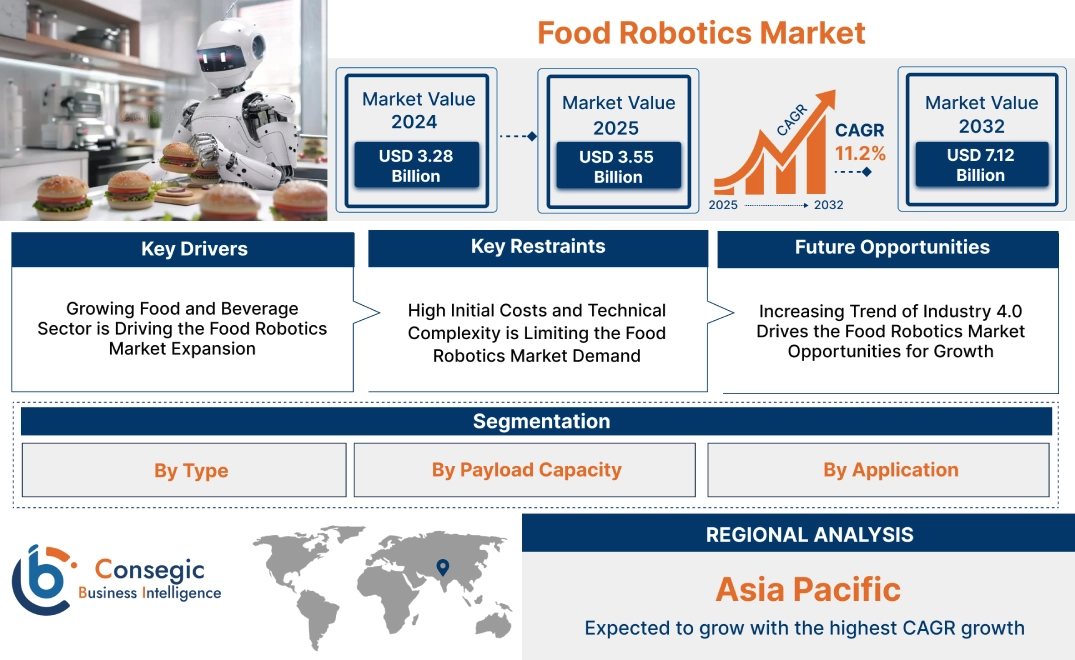

Food Robotics Market Size:

Food Robotics Market is estimated to reach over USD 7.12 Billion by 2032 from a value of USD 3.28 Billion in 2024 and is projected to grow by USD 3.55 Billion in 2025, growing at a CAGR of 11.2% from 2025 to 2032.

Food Robotics Market Scope & Overview:

Food robotics involves the design, development, and deployment of robotic systems to automate various processes within the food and beverage sector. The robots are engineered to perform tasks ranging from basic handling and packaging to complex food preparation and processing. Benefits including increased efficiency and productivity, improved food safety and hygiene, reduced labor costs, and improved workplace safety are driving the food robotics market demand. Further robotics are used for a wide range of applications including packaging, repackaging, palletizing, picking, processing, and others. Furthermore, key market trends driving food robotics include the increasing need for automation and rapid advancement in AI and vision systems. Additionally, the growing adoption of collaborative robots and the push for sustainable, customized food production are significantly influencing the food robotics industry.

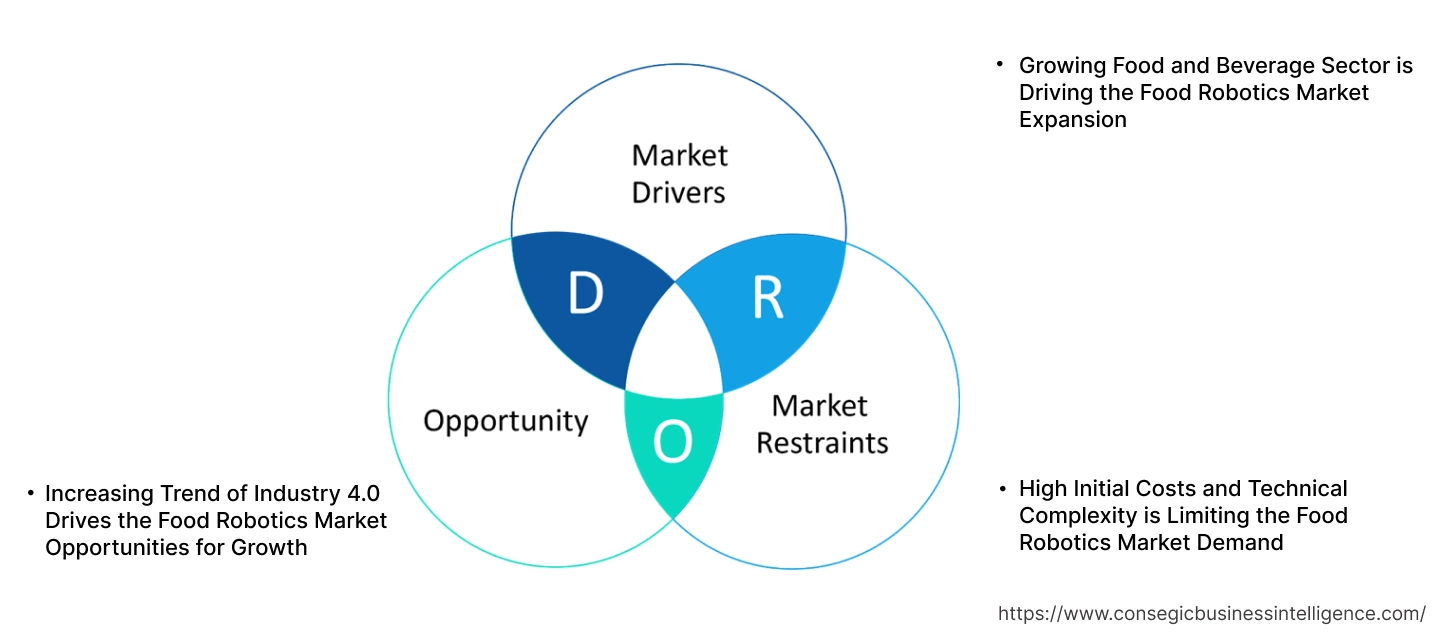

Food Robotics Market Dynamics - (DRO) :

Key Drivers:

Growing Food and Beverage Sector is Driving the Food Robotics Market Expansion

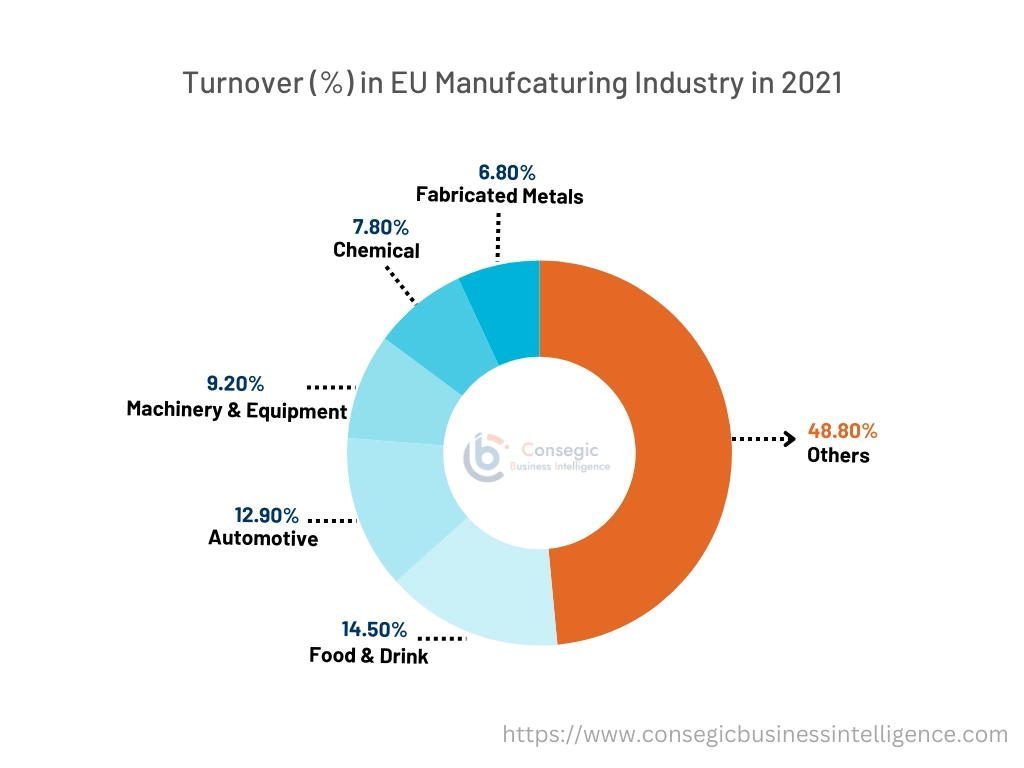

The growth in global food and beverage sector serves as a major catalyst for the food robotics market. The rise in population results in evolving consumer needs which drives the need for efficient and high-volume food production capabilities. The need for improved efficiency and productivity encourages manufacturers to adopt robotic solutions to automate. Further, robots enhance productivity by reducing downtime and minimizing human error. Moreover, stringent regulation and focus on food safety and hygiene necessitates the need for automated systems that minimize human contact. Furthermore, the growing complexity of food processing, with varied packaging and handling requirements, further fuels the adoption of versatile robotic systems.

- For instance, according to FoodDrinkEurope, EU accounted for 14.5% of the overall turnover of the EU manufacturing sector. Further, the food and drink sector employ around 4.7 million people and generates a turnover of USD 1.3 trillion.

Thus, sector’s growth, coupled with the need for efficiency and quality, propels the food robotics market expansion.

Key Restraints:

High Initial Costs and Technical Complexity is Limiting the Food Robotics Market Demand

The high initial costs associated with food robotics present a significant barrier in the market. The implementation of robotic systems involves substantial investments in hardware, software, and integration services, which often exceed the budgets of many businesses. The financial hurdle is aggravated by the technical complexity of integrating robots into existing production lines. Further, food processing environments are diverse and require customized solutions that are challenging to design and implement. The integration of robots with existing systems such as conveyors and packaging machines requires specialized expertise which in turn leads to potential downtime and increased costs.

Furthermore, the need for ongoing maintenance, software updates, and specialized training adds to the overall expense, making the transition to automation a complex and costly undertaking.

Future Opportunities :

Increasing Trend of Industry 4.0 Drives the Food Robotics Market Opportunities for Growth

The rising trend of Industry 4.0 significantly boosts the food robotics industry by fostering smart, interconnected manufacturing environments. Industry 4.0 integrates technologies like IoT, AI, and cloud computing, enabling real-time data collection and analysis. The automation allows food processors to optimize production, predict maintenance needs, and enhance traceability. Further, robots, equipped with advanced sensors and connectivity, seamlessly integrate into smart factories which leads to increased automation, improved efficiency, and enhanced food safety. Moreover, Industry 4.0 facilitates customized production and agile responses to changing consumer demands. Thus, the increasing trend of Industry 4.0 drives the food robotics market opportunities.

Food Robotics Market Segmental Analysis :

By Type:

Based on the type, the market is segmented into articulated robots, SCARA robots, parallel robots, cylindrical robots, collaborative robots, and others.

Trends in the Type:

- Increasing trend in the adoption of SCARA robots for high-volume packaging and picking applications which, in turn, drives the global food robotics market.

- Increasing requirement of parallel robots for high-speed picking and placing of lightweight items, making them ideal for packaging small food products.

Articulated Robots accounted for the largest revenue share in the year 2024.

- The advancements in sensor technology and AI are enabling articulated robots to perform complex tasks which, in turn, drive the food robotics market growth.

- Further, growing use of AI-powered articulated robots for real-time quality inspection and identification & removal of defective products.

- Furthermore, growing integration of 3D vision system is significantly contributing to driving the market.

- For instance, ABB offers IRB 1200 Hygienic articulated robot which is designed for applications in food and beverage sector. The robot offers two cleaning options including a simple wipe-down for low-risk packaging areas and a more thorough wash-down with a protective cover for high-risk food processing.

- Thus, food robotics market analysis, advancements in sensor technology and integration of AI are driving the adoption of articulated robots.

Collaborative Robots are anticipated to register the fastest CAGR during the forecast period.

- Integration of safety sensors and software is driving the demand for the collaborative robot.

- Further, cobots are programmed to perform different tasks and provide greater flexibility in food production which, in turn, drives the food robotics market growth.

- For instance, Dobot offers collaborative robots in food and beverage sector for applications including picking, packaging, and palletizing among others.

- Therefore, based on food robotics market analysis, safety features and flexibility are anticipated to boost the market during the forecast period.

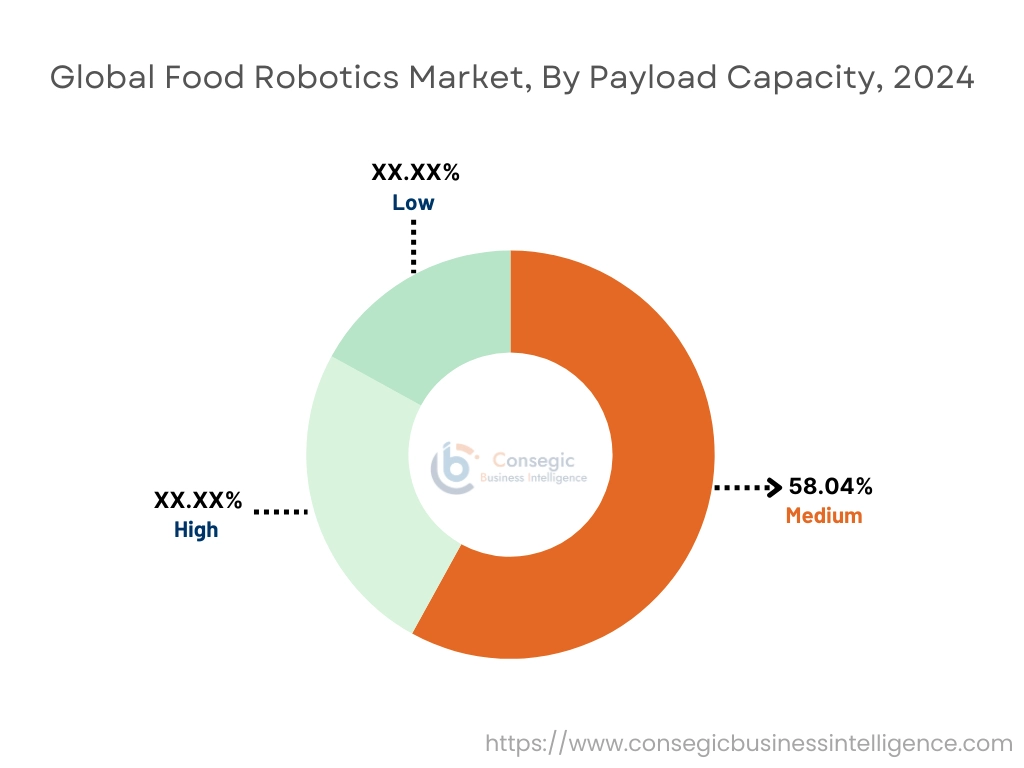

By Payload Capacity:

Based on the payload capacity, the market is segmented into low, medium, and high.

Trends in Payload Capacity:

- Increasing integration of advanced vision systems and soft grippers for low payload capacity is driving the

- The rise in e-commerce is driving the demand for low-payload robots for efficiently picking and packing the items.

Medium accounted for the largest revenue share of 58.04% in the year 2024.

- Integration of advanced sensors including 3D vision sensors, force sensors, and tactile sensors to handle variations in product dimension, shape, and weight.

- Further, manufacturers are developing robots that can handle a wider range of tasks and product dimensions which, in turn, drive the market.

- Thus, based on analysis, flexibility of robots and integration of advanced is driving the food robotics market share.

High is anticipated to register the fastest CAGR during the forecast period.

- There is a growing adoption of high-payload robots to handle large containers of raw materials and finished products.

- Further, increasing integration of high-payload robots with automated guided vehicles in food production and distribution facilities for creating fully automated material handling systems.

- Therefore, aforementioned factors are anticipated to boost the market during the forecast period.

By Application:

Based on the application, the market is segmented into packaging, repackaging, palletizing, picking, processing and others.

Trends in the Application:

- Robots are increasingly being used to automate the repackaging of returned goods which, in turn, increases the speed of return items processing.

- Picking robots are being integrated with warehouse management system to optimize picking routes and improve efficiency.

Palletizing accounted for the largest revenue share in the year 2024.

- Benefits including accuracy, safety, and traceability are driving the adoption of food robotics for palletizing applications.

- Further, robots are using AI to optimize pallet patterns for maximum efficiency and stability.

- Thus, based on analysis, aforementioned factors are driving the market growth during forecast period.

Processing is anticipated to register the fastest CAGR during the forecast period.

- Growing use of robots to automate food preparation and cooking tasks, such as cutting, slicing, and frying.

- Further, increasing use of artificial intelligence in robots to sort and grade food items based on quality and shape.

- Therefore, as per analysis, the growth of AI and IoT as well as rise of hybrid and remote work model are anticipated to boost the market during the forecast period.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

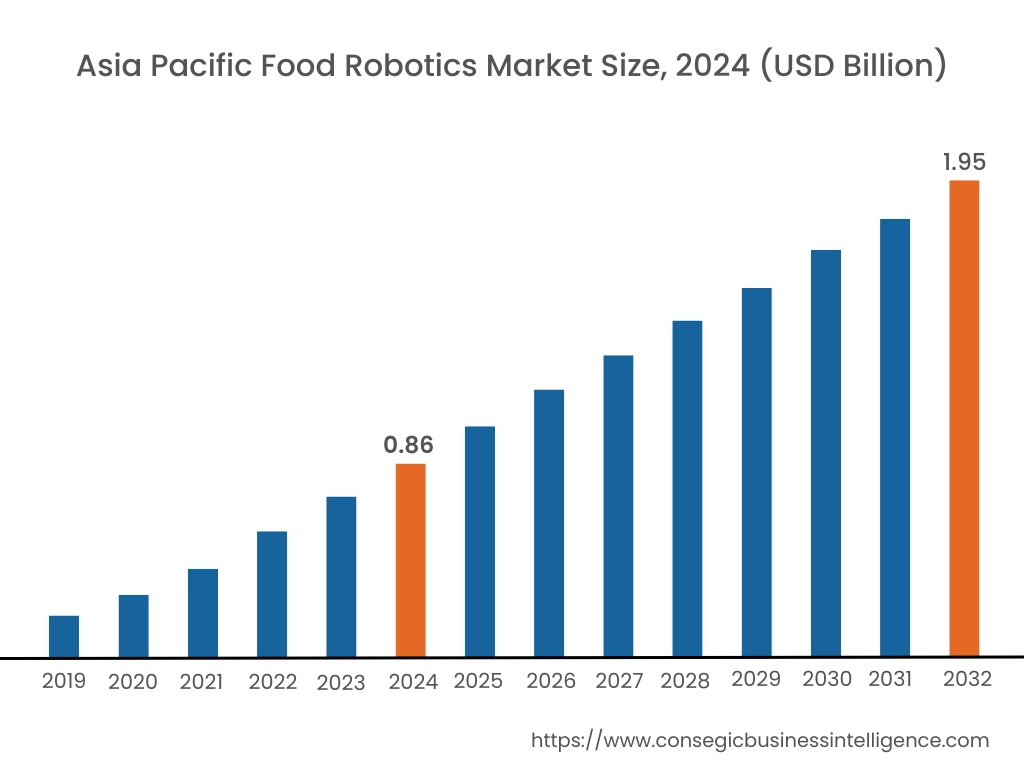

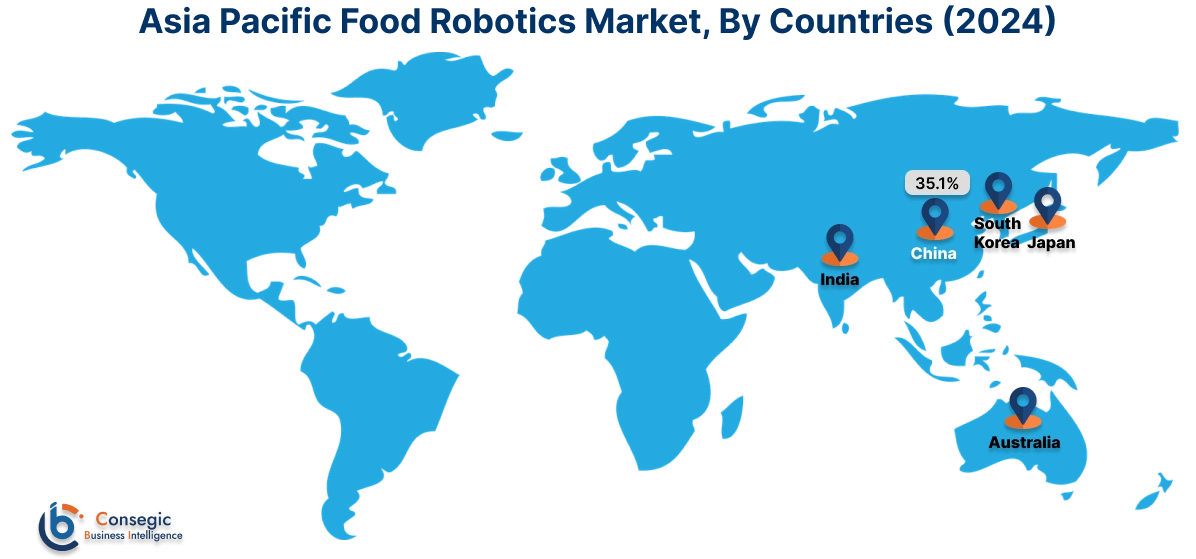

Asia Pacific region was valued at USD 0.86 Billion in 2024. Moreover, it is projected to grow by USD 0.94 Billion in 2025 and reach over USD 1.95 Billion by 2032. Out of this, China accounted for the maximum revenue share of 35.1%. The food robotics market size is mainly driven by surge in requirement of processed and packaged foods which, in turn, drives the need for robotics to meet production volumes and maintain quality standards. Additionally, focus on improving food safety is prompting food manufacturers to invest in robotic solutions which, in turn, drives the market growth.

- For instance, in April 2023, Doosan Robotics launched E-SERIES, a new line of NSF-certified collaborative robots designed specifically for the food and beverage sector. These robots offer hygienic design, competitive pricing, and flexibility for various food preparation tasks.

North America is estimated to reach over USD 2.44 Billion by 2032 from a value of USD 1.13 Billion in 2024 and is projected to grow by USD 1.23 Billion in 2025. North American food robotics market share is driven by strong focus on advanced automation and the growth of food and beverage sector. Furthermore, increasing consumer demand for consistent quality & food safety and stringent regulations in the region are driving the food robotics market trends.

- In April 2023, Doosan Robotics and Rockwell Automation agreed to collaborate through a Memorandum of Understanding signed in Washington, D.C. This partnership aims to combine Doosan's collaborative robot technology with Rockwell's expertise in industrial automation and digital transformation.

The regional analysis depicts that the stringent food safety regulations and a strong emphasis on automation to enhance production efficiency in Europe is driving the food robotics market size. Additionally, the factors driving the market in the Middle East and African region are increasing need for automation in food processing and growing investments in food security. Further, increased demand for processed foods, and improved food safety standards are paving the way for the progress of food robotics market trends in Latin America region.

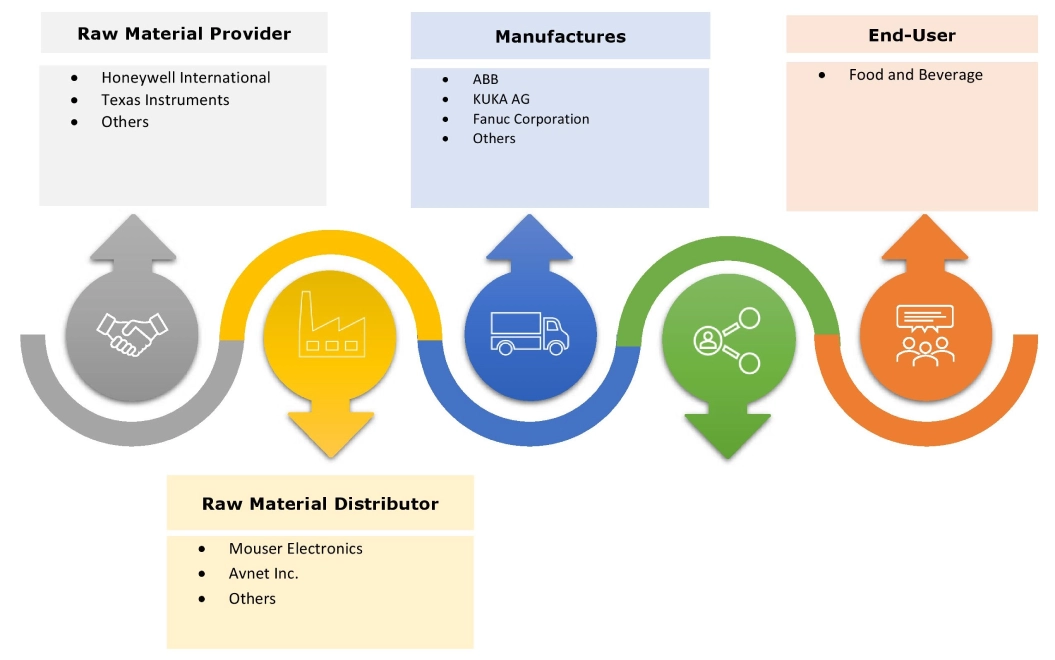

Top Key Players and Market Share Insights:

The global food robotics market is highly competitive with major players providing solutions to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the food robotics sector. Key players in the food robotics market include-

- ABB (Switzerland)

- Fanuc Corporation (Japan)

- Mitsubishi Electric Corporation (Japan)

- Denso Corporation (Japan)

- Universal Robots A/S (Denmark)

- OMRON Corporation (Japan)

- KUKA AG (Germany)

- Yasakawa Electric Corporation (Japan)

- Kawasaki Heavy Industries Ltd. (Japan)

- Rockwell Automation Inc. (U.S.)

- Staubli International AG (Switzerland)

Recent Industry Developments :

Partnerships and Collaborations:

- In May 2024, ABB Robotics and Pulmuone announced a partnership to automate the production of lab-grown seafood. Both companies have signed an agreement to develop robotic solutions for cell cultivation, aiming to improve efficiency, reduce contamination, and address labor shortages. ABB will provide its robotics, AI, and automation expertise, including collaborative robots (cobots), to help Pulmuone scale up production of its innovative seafood products.

Food Robotics Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 7.12 Billion |

| CAGR (2025-2032) | 11.2% |

| By Type |

|

| By Payload Capacity |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Food Robotics market? +

The Food Robotics Market is estimated to reach over USD 7.12 Billion by 2032 from a value of USD 3.28 Billion in 2024 and is projected to grow by USD 3.55 Billion in 2025, growing at a CAGR of 11.2% from 2025 to 2032.

What specific segmentation details are covered in the Food Robotics report? +

The food robotics report includes specific segmentation details for type, payload capacity, application, and regions.

Which is the fastest segment anticipated to impact the market growth? +

In the Food Robotics market, the high payload capacity is the fastest-growing segment during the forecast period due to the increasing automation of tasks such as palletizing and large container handling.

Who are the major players in the Food Robotics market? +

The key participants in the Food Robotics market are ABB (Switzerland), Fanuc Corporation (Japan), KUKA AG (Germany), Yasakawa Electric Corporation (Japan), Kawasaki Heavy Industries Ltd. (Japan), Rockwell Automation Inc. (U.S.), Staubli International AG (Switzerland), Mitsubishi Electric Corporation (Japan), Denso Corporation (Japan), Universal Robots A/S (Denmark), and OMRON Corporation (Japan) and others.

What are the key trends in the Food Robotics market? +

The food robotics market is being shaped by several key trends including increasing automation for enhanced efficiency and hygiene, the rise of collaborative robots, and advancements in AI and vision systems.