- Summary

- Table Of Content

- Methodology

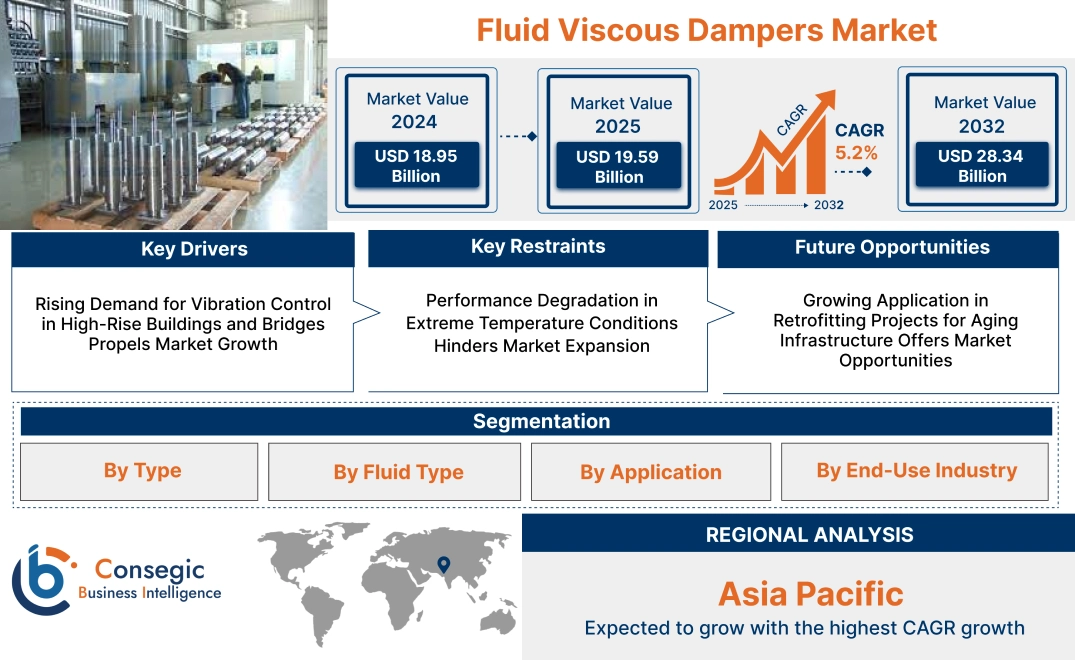

Fluid Viscous Dampers Market Size:

Fluid Viscous Dampers Market size is estimated to reach over USD 28.34 Billion by 2032 from a value of USD 18.95 Billion in 2024 and is projected to grow by USD 19.59 Billion in 2025, growing at a CAGR of 5.2% from 2025 to 2032.

Fluid Viscous Dampers Market Scope & Overview:

Fluid viscous dampers are high-performance energy dissipation devices designed to control structural motion by converting kinetic energy into heat through viscous fluid movement. Used in buildings, bridges, and industrial structures, they help mitigate vibrations caused by seismic events, wind loads, or mechanical disturbances.

These dampers consist of a piston-cylinder assembly filled with a silicone or mineral-based fluid. As the piston moves in response to structural motion, the fluid resists flow, providing consistent damping across a wide range of frequencies and amplitudes.

Its key features include durability, temperature stability, and performance uniformity under dynamic loading. Fluid viscous dampers improve structural safety, reduce acceleration, and enhance occupant comfort without altering the natural stiffness or mass of the system. Their integration supports both new construction and retrofit applications, making them an essential solution for improving structural resilience and operational continuity in critical infrastructure.

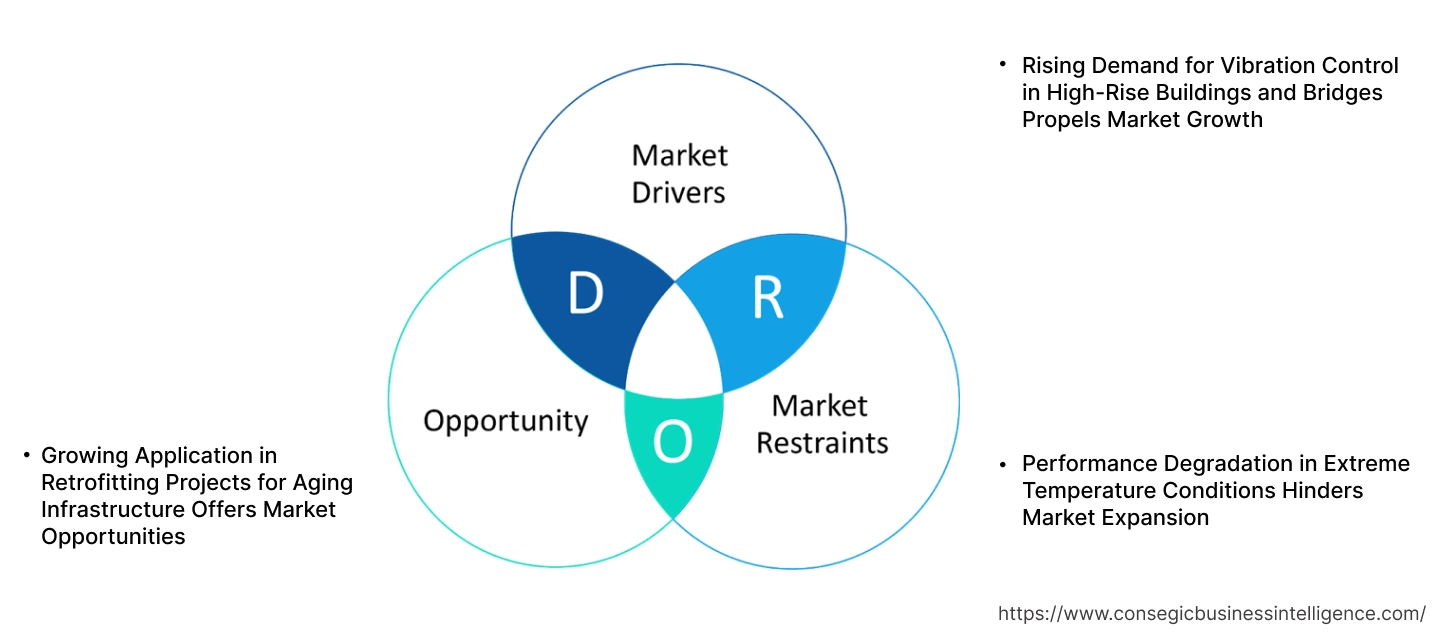

Fluid Viscous Dampers Market Dynamics - (DRO) :

Key Drivers:

Rising Demand for Vibration Control in High-Rise Buildings and Bridges Propels Market Growth

The increasing verticality of modern buildings and the expansion of bridge infrastructure in seismic and high-wind regions have led to an escalating need for effective vibration control systems. Fluid viscous dampers are essential in providing enhanced damping performance for large structures subjected to wind loads, traffic-induced vibrations, and seismic activity. By minimizing lateral movement and reducing structural fatigue, these dampers ensure the safety, comfort, and durability of high-rise buildings and bridges. Their ability to absorb and dissipate energy efficiently in diverse structural environments, including skyscrapers and long-span bridges, makes them a preferred choice for engineers and architects. With urbanization and infrastructure development pushing the need for resilient building solutions, they are becoming integral in protecting critical assets.

- For instance, the Mumbai Trans Harbour Link (MTHL) bridge, inaugurated in January 2024, was designed with numerous bearings and dampers to minimize vibrations resulting from the lightweight construction of the 1.75-kilometer-long steel bridge section with a wide span of 100 to 180 meters. The hydraulic dampers, manufactured in Germany, were designed to be frictionless and wear-free to withstand ongoing wind force, reducing bridge vibration for 50 years and longer.

As a result, the requirement for vibration control technologies continues to rise, driving fluid viscous dampers market expansion.

Key Restraints:

Performance Degradation in Extreme Temperature Conditions Hinders Market Expansion

While fluid viscous dampers offer excellent performance under normal operating conditions, their efficiency can be affected by extreme temperatures, both high and low. At low temperatures, the damping fluid within the system may become more viscous, limiting its ability to dissipate energy effectively. In contrast, high temperatures can lead to fluid degradation, reducing the overall performance and lifespan of the damper. These temperature-related issues are particularly challenging in regions with extreme climatic conditions, such as arctic or desert environments. The demand for dampers in these locations may be hindered unless specialized materials or fluid compounds are used, which increases cost and complexity. As such, these temperature limitations present challenges for its widespread adoption in harsh climates, ultimately restricting the fluid viscous dampers market growth.

Future Opportunities :

Growing Application in Retrofitting Projects for Aging Infrastructure Offers Market Opportunities

With aging infrastructure becoming a major concern in many regions, the need for cost-effective solutions to enhance structural resilience is increasing. Fluid viscous dampers are widely being adopted in retrofitting projects to upgrade bridges, highways, and high-rise buildings to meet modern seismic and vibration control standards. These dampers offer a non-invasive and efficient way to improve the dynamic performance of existing structures without the need for extensive rebuilding. As infrastructure owners seek to extend the lifespan of their assets while adhering to updated safety regulations, the demand in retrofitting applications is on the rise. This trend is particularly prominent in earthquake-prone and high-wind areas. With continued growth in the renovation and reinforcement of older structures, the fluid viscous dampers market opportunities are expanding in the retrofit sector, providing valuable solutions for modernizing infrastructure.

Fluid Viscous Dampers Market Segmental Analysis :

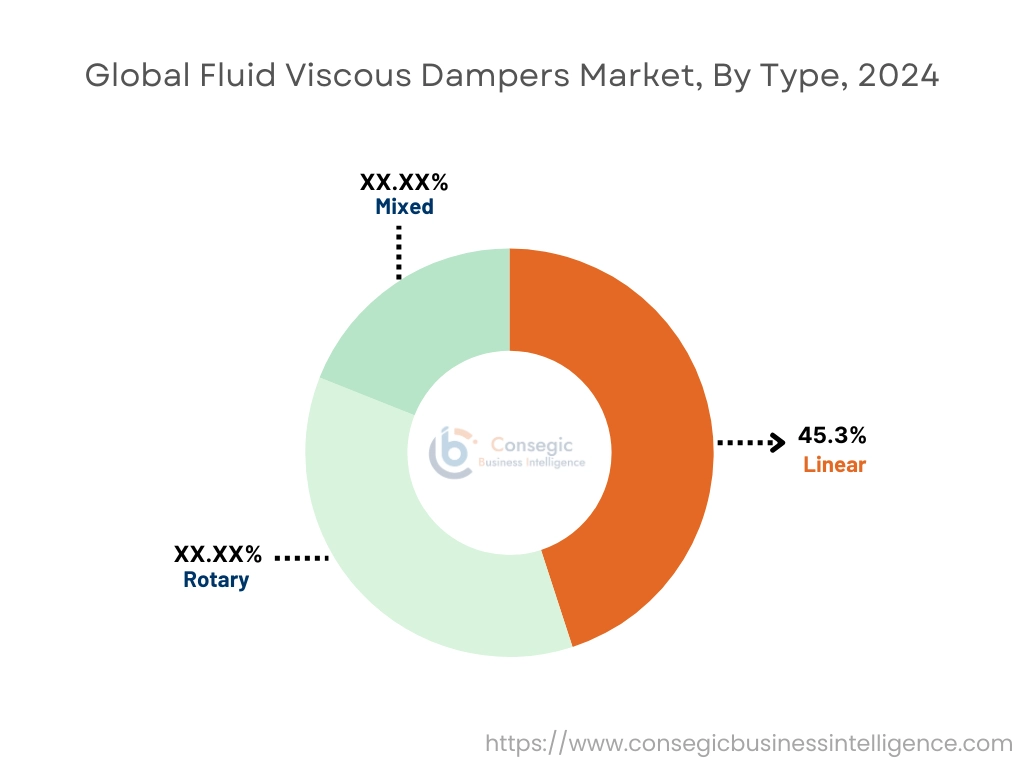

By Type:

Based on type, the fluid viscous dampers market is segmented into linear, rotary, and mixed.

The linear fluid viscous dampers segment held the largest revenue share of 45.3% in 2024.

- Linear dampers are designed to provide constant resistance across a wide range of motion, making them ideal for seismic protection and vibration control in structures like bridges and high-rise buildings.

- These dampers operate by converting kinetic energy into heat energy through viscous shear, offering efficient performance in applications that require steady damping.

- Their widespread use in both construction and industrial sectors is supported by their simplicity and durability in absorbing shock and vibrations.

- As per fluid viscous dampers market analysis, linear dampers continue to dominate due to their proven efficiency in mitigating seismic activity and protecting buildings and infrastructure.

The rotary segment is expected to grow at the fastest CAGR during the forecast period.

- Rotary dampers are highly effective in controlling rotational movements, which makes them suitable for applications like automotive suspension systems and machinery vibration control.

- Their ability to provide consistent damping in rotating mechanisms, such as turbines or moving equipment, is driving their adoption in energy & power and aerospace sectors.

- The increasing use of rotary dampers in high-performance applications, particularly where rotational movements need precise control, is fueling growth in this segment.

- According to fluid viscous dampers market trends, rotary dampers are gaining popularity due to their superior performance in complex, rotating mechanical systems.

By Fluid Type:

Based on fluid type, the market is segmented into hydraulic fluid and magnetorheological fluid.

The hydraulic fluid segment accounted for the largest fluid viscous dampers market share in 2024.

- Hydraulic fluid dampers are commonly used in industries that require high force damping, such as in construction, automotive, and energy & power sectors.

- These dampers offer efficient energy dissipation and are well-suited for large-scale infrastructure projects that experience high vibrations or shock loads.

- Hydraulic fluid dampers are preferred for their reliability, ease of maintenance, and ability to operate across a broad range of temperatures and pressures.

- For instance, in January 2024, KYB launched a new environmentally friendly hydraulic fluid called SustainaLub™ for shock absorption. The fluid achieves carbon neutrality by replacing petroleum-derived base oil with naturally derived base oil. Furthermore, it improves manoeuvrability and stability in automobiles.

- As per the fluid viscous dampers market demand, the hydraulic fluid segment remains dominant due to its broad applicability and durability in heavy-duty applications.

The magnetorheological fluid segment is projected to register the fastest CAGR during the forecast period.

- Magnetorheological fluids are smart fluids that change their viscosity when exposed to a magnetic field, offering adjustable damping characteristics.

- These dampers are used in applications where variable damping is required, such as in advanced automotive suspension systems, military vehicles, and high-tech industrial machinery.

- The ability to fine-tune damping behavior in real-time makes magnetorheological dampers increasingly attractive for industries looking to enhance performance and control.

- According to fluid viscous dampers market trends, the adoption of magnetorheological fluid dampers is growing due to their ability to respond to changing conditions, offering improved safety and adaptability.

By Application:

Based on application, the market is segmented into seismic protection, vibration control, noise reduction, energy dissipation, and others.

The seismic protection segment held the largest fluid viscous dampers market share in 2024.

- Seismic protection systems using these dampers helps prevent structural damage during earthquakes by absorbing seismic energy and reducing the forces transmitted to buildings.

- These systems are commonly integrated into bridges, high-rise buildings, and critical infrastructure in earthquake-prone regions.

- The need for seismic protection is rising as more urban areas in seismic zones implement regulations to safeguard buildings and ensure public safety during natural disasters.

- As per the fluid viscous dampers market analysis, seismic protection remains the dominant application, driven by the increasing frequency of earthquakes and heightened safety awareness in construction.

The vibration control segment is expected to witness the fastest CAGR during the forecast period.

- Vibration control using such dampers is essential in industries like manufacturing, automotive, and energy, where machinery and equipment generate continuous vibrations.

- These dampers help protect sensitive equipment, reduce wear and tear, and improve overall operational efficiency.

- The growing trend toward automation and precision manufacturing is driving the adoption of vibration control systems to maintain product quality and reduce downtime.

- According to segmental trends, the increasing need for noise and vibration control in industrial applications is accelerating the fluid viscous dampers market growth.

By End-Use Industry:

Based on end-use industry, the market is segmented into construction, aerospace, automotive, energy & power, oil & gas, and others.

The construction segment accounted for the largest revenue share in 2024.

- These dampers are extensively used in the construction industry for seismic protection and vibration control in buildings, bridges, and other critical infrastructure.

- As urbanization increases and new infrastructure projects are developed, the demand for advanced damping systems to enhance the safety and longevity of structures is growing.

- The construction industry's need for energy-efficient and low-maintenance damping solutions is further driving their adoption.

- Hence, the construction sector remains the largest end-user due to the critical need for seismic protection in modern infrastructure projects, driving the fluid viscous dampers market expansion.

The automotive segment is projected to witness the fastest CAGR during the forecast period.

- In the automotive industry, they are increasingly used in suspension systems to improve ride comfort, reduce noise, and enhance vehicle stability.

- These dampers help reduce vibrations caused by road irregularities, ensuring smoother driving experiences.

- The rise in necessity for electric vehicles (EVs) and advancements in automotive suspension technologies are driving their adoption in the automotive sector.

- According to market trends, the automotive sector is poised for rapid expansion as the fluid viscous dampers market demand, especially for smart, adjustable suspension systems, increases.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

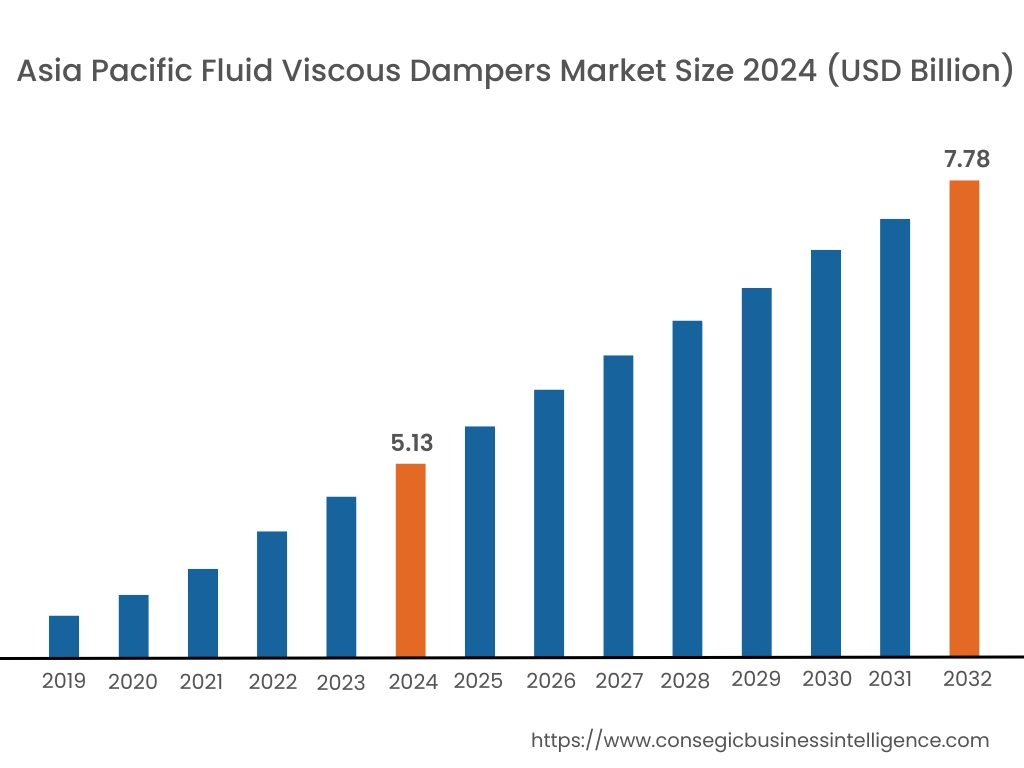

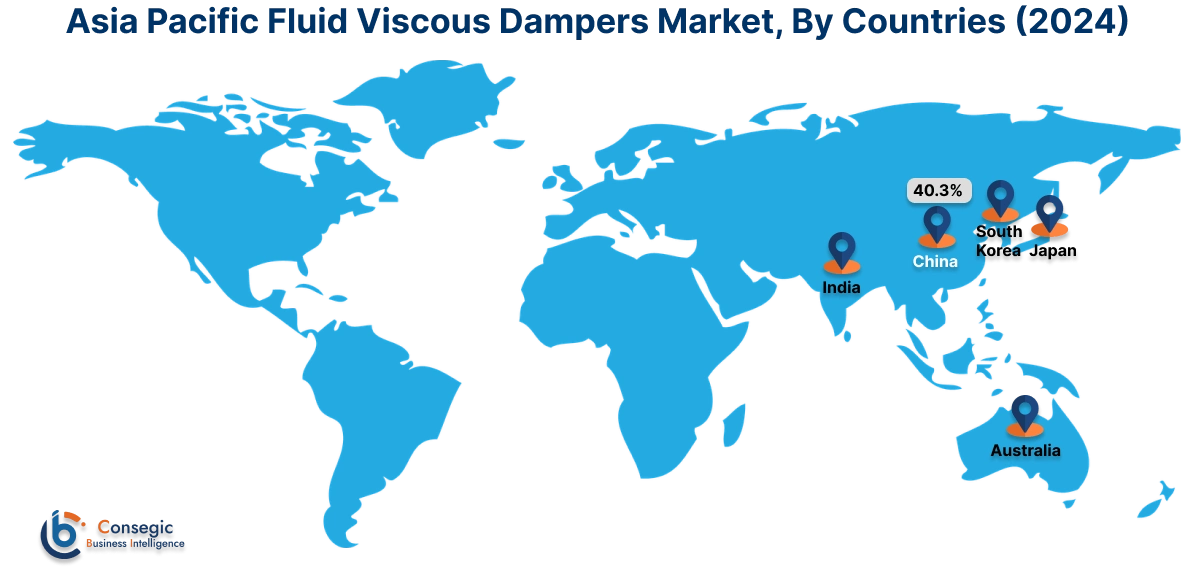

Asia Pacific region was valued at USD 5.13 Billion in 2024. Moreover, it is projected to grow by USD 5.31 Billion in 2025 and reach over USD 7.78 Billion by 2032. Out of this, China accounted for the maximum revenue share of 40.3%. Asia-Pacific is witnessing rapid expansion in the fluid viscous dampers industry due to high seismic exposure, dense urban populations, and rapid construction cycles. Countries like Japan, China, South Korea, and Taiwan have institutionalized their use in both commercial and public buildings. Market analysis highlights significant demand from transport infrastructure, including metro systems, high-speed rail bridges, and airport terminals. In developing economies such as India and Indonesia, adoption is expanding as urban safety frameworks evolve, and awareness of damping technologies grows. Continued growth is fueled by government mandates, engineering innovation, and increasing investment in disaster-resilient infrastructure.

North America is estimated to reach over USD 9.44 Billion by 2032 from a value of USD 6.30 Billion in 2024 and is projected to grow by USD 6.51 Billion in 2025. North America represents a mature and steadily advancing market for damping systems, with its widespread use in high-rise buildings, transportation infrastructure, and retrofitting of seismic-prone structures. In the United States and Canada, market analysis reveals strong integration of dampers in bridge expansion projects, hospitals, and skyscrapers to enhance dynamic load resistance. Growth in this region is supported by updated seismic building codes, government incentives for seismic upgrades, and strong institutional expertise in structural engineering. Additionally, public infrastructure resilience plans continue to prioritize energy dissipation technologies for long-term structural protection.

Europe exhibits stable adoption, especially in countries such as Italy, Turkey, and Greece, where seismic vulnerability is a key concern. Market analysis shows that fluid viscous dampers are frequently employed in heritage building retrofits, viaducts, and critical infrastructure requiring energy dissipation without structural alteration. Northern and western Europe are applying dampers more in wind-sensitive applications such as offshore platforms, tall buildings, and data centers. The market opportunity in Europe is driven by evolving structural safety regulations, lifecycle durability priorities, and integration into EU-funded civil resilience initiatives focused on climate adaptation and seismic risk mitigation.

Latin America is witnessing increasing use of damping systems in earthquake-prone countries like Mexico, Chile, and Peru. Market analysis shows the dampers being deployed in hospitals, public buildings, and high-density housing developments, particularly in seismic zones with limited emergency access. Although cost sensitivity remains a challenge, the growing focus on structural preservation and disaster preparedness is leading to gradual market penetration. The fluid viscous dampers market opportunity in Latin America lies in technical training, regional partnerships with engineering consultancies, and incorporation into local building standards for both new construction and retrofitting.

The Middle East and Africa are at an early stage of adoption, though notable demand is emerging in countries such as the UAE, Saudi Arabia, and South Africa. Market analysis indicates that fluid viscous dampers are being considered in mega-infrastructure and smart city projects where structural control and longevity are strategic priorities. In seismic or wind-exposed zones of North and East Africa, pilot applications in commercial and transportation infrastructure are gaining attention. Growth in this region is supported by increasing awareness of resilient design, interest in performance-based engineering, and the need for adaptable damping solutions in variable climate and terrain conditions.

Top Key Players and Market Share Insights:

The fluid viscous dampers market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global fluid viscous dampers market. Key players in the fluid viscous dampers industry include -

- Taylor Devices, Inc. (USA)

- Maurer SE (Germany)

- FIP Industriale S.p.A. (Italy)

- Sumitomo Riko Company Limited (Japan)

- GERB Vibration Control Systems (Germany)

- Dynamic Isolation Systems, Inc. (USA)

- Toyo Tire Corporation (Japan)

- Kawakin Core-Tech Co., Ltd. (Japan)

- Mageba SA (Switzerland)

- Bridgestone Corporation (Japan)

Recent Industry Developments :

Acquisitions:

- In March 2025, Wabtec Corporation announced the acquisition of Dellner Couplers, a global leader in highly engineered safety-critical train connection systems and services for passenger rail rolling stock.

- In December 2024, the global supplier of components, systems, and engineering services to the automotive industry, Multimatic, acquired PKM Consulting, a leading supplier of advanced racing dampers. This enables PKM Consulting to gain responsibility for all racing damper operations of the company.

Partnerships:

- In September 2022, Constec Engi, Co. partnered with Taylor Devices, Inc. to represent them in Japan.

Fluid Viscous Dampers Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 28.34 Billion |

| CAGR (2025-2032) | 5.2% |

| By Type |

|

| By Fluid Type |

|

| By Application |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Fluid Viscous Dampers Market? +

Fluid Viscous Dampers Market size is estimated to reach over USD 28.34 Billion by 2032 from a value of USD 18.95 Billion in 2024 and is projected to grow by USD 19.59 Billion in 2025, growing at a CAGR of 5.2% from 2025 to 2032.

What specific segmentation details are covered in the Fluid Viscous Dampers Market report? +

The Fluid Viscous Dampers market report includes specific segmentation details for type, fluid type, application and end-use industry.

What are the end-use industries of the Fluid Viscous Dampers Market? +

The end-use industries of the Fluid Viscous Dampers Market are construction, aerospace, automotive, energy & power, oil & gas, and others.

Who are the major players in the Fluid Viscous Dampers Market? +

The key participants in the Fluid Viscous Dampers market are Taylor Devices, Inc. (USA), Maurer SE (Germany), FIP Industriale S.p.A. (Italy), Sumitomo Riko Company Limited (Japan), GERB Vibration Control Systems (Germany), Dynamic Isolation Systems, Inc. (USA), Toyo Tire Corporation (Japan), Kawakin Core-Tech Co., Ltd. (Japan), Mageba SA (Switzerland) and Bridgestone Corporation (Japan).