- Summary

- Table Of Content

- Methodology

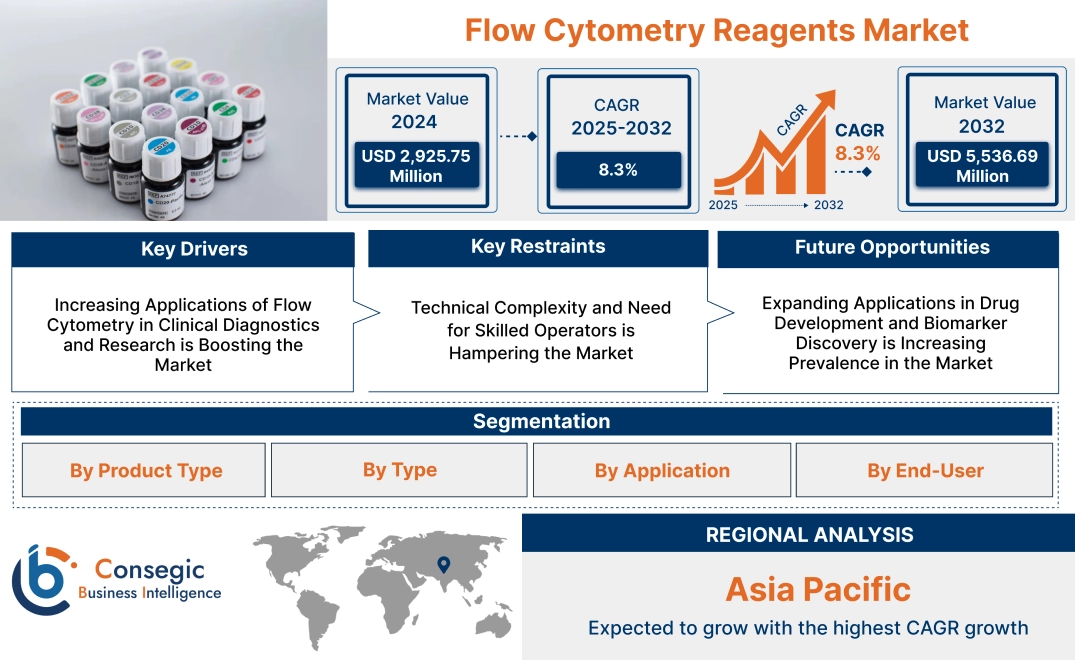

Flow Cytometry Reagents Market Size:

Flow Cytometry Reagents Market size is estimated to reach over USD 5,536.69 Million by 2032 from a value of USD 2,925.75 Million in 2024 and is projected to grow by USD 3,116.46 Million in 2025, growing at a CAGR of 8.3% from 2025 to 2032.

Flow Cytometry Reagents Market Scope & Overview:

The flow cytometry reagents produce specialized reagents used in flow cytometry to analyze, quantify, and sort cells and particles in research and clinical diagnostics. These reagents include fluorochrome-conjugated antibodies, viability dyes, buffers, and calibration beads, enabling precise detection of cellular properties and biomolecules. Key characteristics of flow cytometry reagents include high specificity, sensitivity, and compatibility with multi-parametric analysis, supporting advancements in cell biology and immunology. The benefits include enhanced diagnostic accuracy, improved workflow efficiency, and reliable results in complex analyses. Applications span immunophenotyping, cell viability and apoptosis studies, cancer diagnostics, and drug development. End-users include research laboratories, pharmaceutical companies, and clinical diagnostic centers, driven by the increasing prevalence of chronic diseases, advancements in immunotherapy research, and the growing adoption of flow cytometry in clinical and research settings.

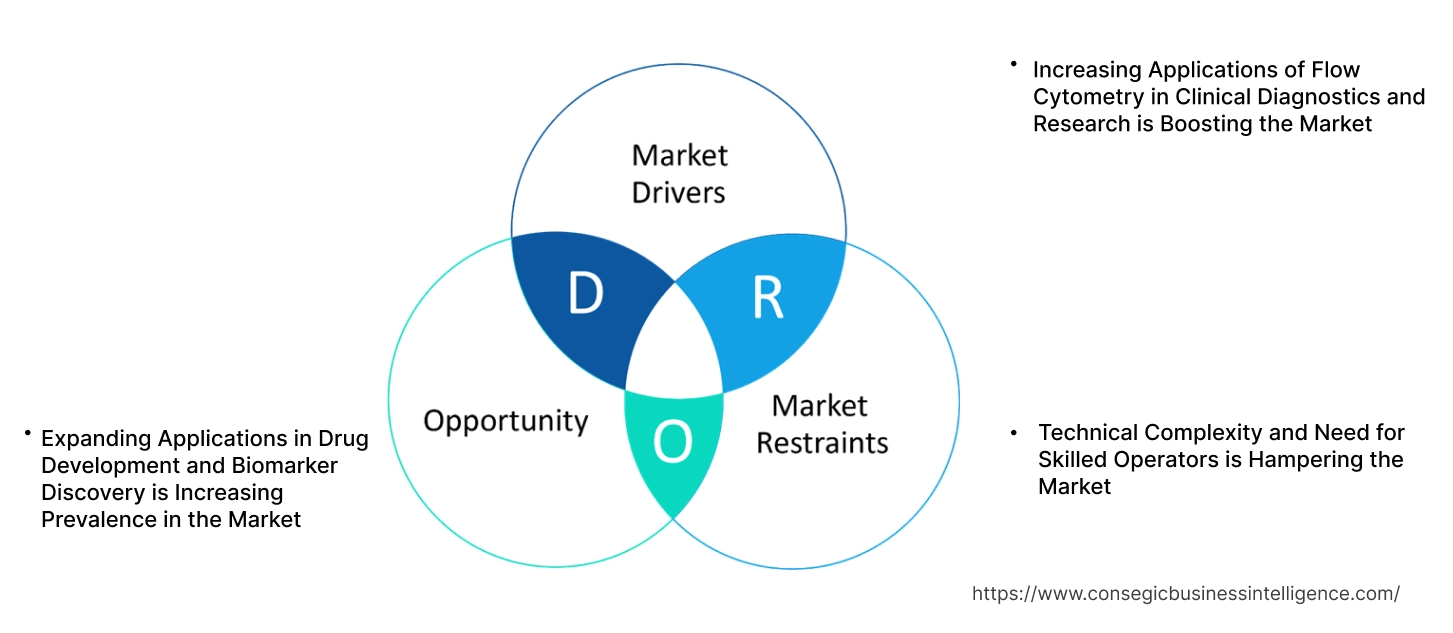

Flow Cytometry Reagents Market Dynamics - (DRO) :

Key Drivers:

Increasing Applications of Flow Cytometry in Clinical Diagnostics and Research is Boosting the Market

Flow cytometry has become a cornerstone in clinical diagnostics and research due to its ability to deliver precise and high-throughput analyses of cells and biomolecules. In clinical settings, it is extensively used for immunophenotyping, cancer detection, and infectious disease monitoring. In research, the technique supports advancements in immunology, molecular biology, and regenerative medicine by enabling detailed cellular analysis.

Trends in personalized medicine and disease-specific research have amplified the role of flow cytometry reagents in ensuring accurate and reproducible results. With the increasing emphasis on early diagnosis and targeted therapies, flow cytometry continues to expand its applications across healthcare and research domains. Analysis indicates that its versatility and precision make it a critical tool for advancing diagnostic and therapeutic strategies.

Key Restraints:

Technical Complexity and Need for Skilled Operators is Hampering the Market

The effective use of flow cytometry reagents and instruments requires specialized knowledge, including expertise in experimental design, operation, and data interpretation. The technical complexity of the systems can pose challenges for laboratories that lack adequately trained personnel. Misinterpretation of data or errors in reagent preparation may lead to inaccurate results, impacting clinical or research outcomes.

Trends in automation and user-friendly software are helping mitigate these challenges, but the steep learning curve and the need for continuous training remain significant barriers. The analysis highlights that addressing these issues through enhanced training programs and simplified system designs is essential for ensuring broader adoption and effective utilization of flow cytometry technologies.

Future Opportunities :

Expanding Applications in Drug Development and Biomarker Discovery is Increasing Prevalence in the Market

Flow cytometry is playing an increasingly important role in drug development and biomarker discovery. It supports the identification of therapeutic targets, monitors drug efficacy, and studies cellular responses. Flow cytometry reagents' ability to enable multiplex flow cytometry reagents market analysis and high-content screening makes them indispensable in pharmaceutical research and preclinical studies.

Trends in precision medicine and the development of targeted therapies are driving the integration of flow cytometry into drug discovery workflows. Analysis suggests that innovations in reagent formulations tailored for specific drug development processes offer significant flow cytometry reagents market opportunities for manufacturers to cater to the growing needs of the pharmaceutical and biotechnology sectors. As the focus on personalized treatments intensifies, flow cytometry reagents are expected to remain central to advancing therapeutic research and innovation.

Flow Cytometry Reagents Market Segmental Analysis :

By Product Type:

Based on product type, the market is segmented into antibodies, dyes & stains, beads, buffers, kits, and others.

The antibodies segment accounted for the largest revenue in flow cytometry reagents market share in 2024.

- Antibodies, including primary and secondary antibodies, are critical reagents in flow cytometry applications for identifying specific cellular markers and antigens.

- Primary antibodies are widely used for their ability to directly bind to antigens, while secondary antibodies enhance signal detection and amplification.

- The increasing use of antibodies in immunophenotyping and cancer diagnostics has driven trends in both research and clinical settings.

- Advancements in monoclonal antibody technology and the growing focus on targeted therapies are further propelling the adoption of antibody-based flow cytometry reagents.

The dyes & stains segment is anticipated to register the fastest CAGR during the forecast period.

- Dyes and stains are essential for fluorescent labeling in flow cytometry, enabling detailed analysis of cell populations.

- The rising global flow cytometry reagents market for multiplexing and high-throughput screening has driven the development of advanced fluorescent dyes with higher stability and sensitivity.

- The growing adoption of flow cytometry in clinical diagnostics, particularly for cancer and infectious disease screening, is boosting the use of dyes and stains.

- Increasing research activities in cell biology and immunology are expected to fuel segment growth, supported by innovations in dye chemistry for improved performance.

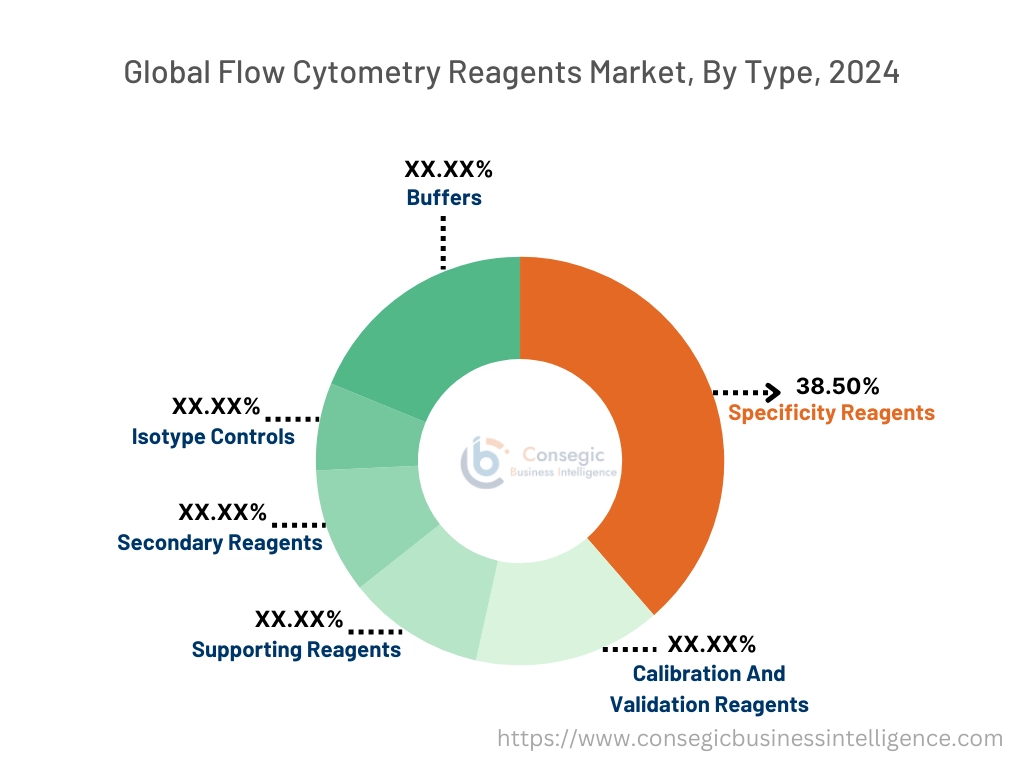

By Type:

Based on type, the market is segmented into supporting reagents, calibration and validation reagents, specificity reagents, secondary reagents, isotype controls, and buffers.

The specificity reagents segment accounted for the largest revenue of 38.50% share in 2024.

- Specificity reagents are critical for ensuring accurate and reliable flow cytometry results, making them indispensable in both research and clinical applications.

- These reagents enable precise detection and quantification of specific antigens, contributing to advancements in immunology and oncology research.

- The increasing adoption of targeted therapies and personalized medicine has driven trends for high-specificity reagents in diagnostic and drug discovery applications.

- Ongoing innovations in reagent formulations and quality assurance are further supporting the flow cytometry reagents market growth of this segment.

The calibration and validation reagents segment is anticipated to register the fastest CAGR during the forecast period.

- Calibration and validation reagents are essential for standardizing flow cytometry instruments, ensuring accuracy and reproducibility in experiments.

- The growing emphasis on compliance with regulatory standards in clinical diagnostics has increased the adoption of these reagents.

- Rising flow cytometry reagents market demand for flow cytometry in quality control applications across the pharmaceutical and biotechnology sectors is driving segment growth.

- Technological advancements in reagent development for enhanced instrument performance are expected to boost adoption during the forecast period.

By Application:

Based on application, the market is segmented into diagnostics and drug discovery.

The diagnostics segment accounted for the largest revenue in the flow cytometry reagents market share in 2024.

- Flow cytometry is extensively used in clinical diagnostics for identifying and characterizing cell populations in diseases such as cancer, HIV, and autoimmune disorders.

- The increasing prevalence of chronic and infectious diseases has driven demand for high-quality reagents in diagnostic workflows.

- Advancements in flow cytometry technologies, such as high-throughput systems and multiparametric analysis, have expanded its use in routine diagnostics.

- Regulatory mandates for precision diagnostics and the rising adoption of flow cytometry in hospital laboratories are further boosting segment growth.

The drug discovery segment is anticipated to register the fastest CAGR during the forecast period.

- Flow cytometry plays a pivotal role in drug discovery, enabling detailed flow cytometry reagents market analysis of cellular responses, target validation, and high-content screening.

- Pharmaceutical and biotechnology companies are increasingly using cytometry reagents to support the development of immunotherapies and biologics.

- The growing focus on cell-based assays and the use of flow cytometry in preclinical studies are driving the adoption of reagents in this segment.

- Rising investments in R&D activities, coupled with advancements in reagent technology for enhanced sensitivity and specificity, are expected to propel flow cytometry reagents market growth.

By End-User:

Based on end-user, the market is segmented into academic & research institutes, pharmaceutical & biotechnology companies, hospitals & clinical testing laboratories, contract research organizations (CROs), and others.

The academic & research institutes segment accounted for the largest revenue share in 2024.

- Academic and research institutes are major consumers of flow cytometry reagents for studying cellular mechanisms, immunology, and cancer biology.

- The growing number of research grants and funding for life sciences research has driven the adoption of advanced reagents in this sector.

- Innovations in reagent formulations tailored for academic workflows, including multicolor panels and high-sensitivity dyes, are further boosting flow cytometry reagents market trends.

- The expansion of research collaborations and partnerships between academic institutions and industry players is also contributing to segment growth.

The pharmaceutical & biotechnology companies segment is anticipated to register the fastest CAGR during the forecast period.

- These companies rely heavily on flow cytometry reagents for drug development, quality control, and clinical trials.

- The increasing adoption of immunotherapy and biologics has driven flow cytometry reagents market trends for specialized reagents in pharmaceutical R&D.

- Rising investments in personalized medicine and the development of novel therapeutics are fueling reagent adoption in this sector.

- The need for high-throughput screening and advanced cell analysis tools has further accelerated the use of flow cytometry reagents in pharmaceutical and biotech companies.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

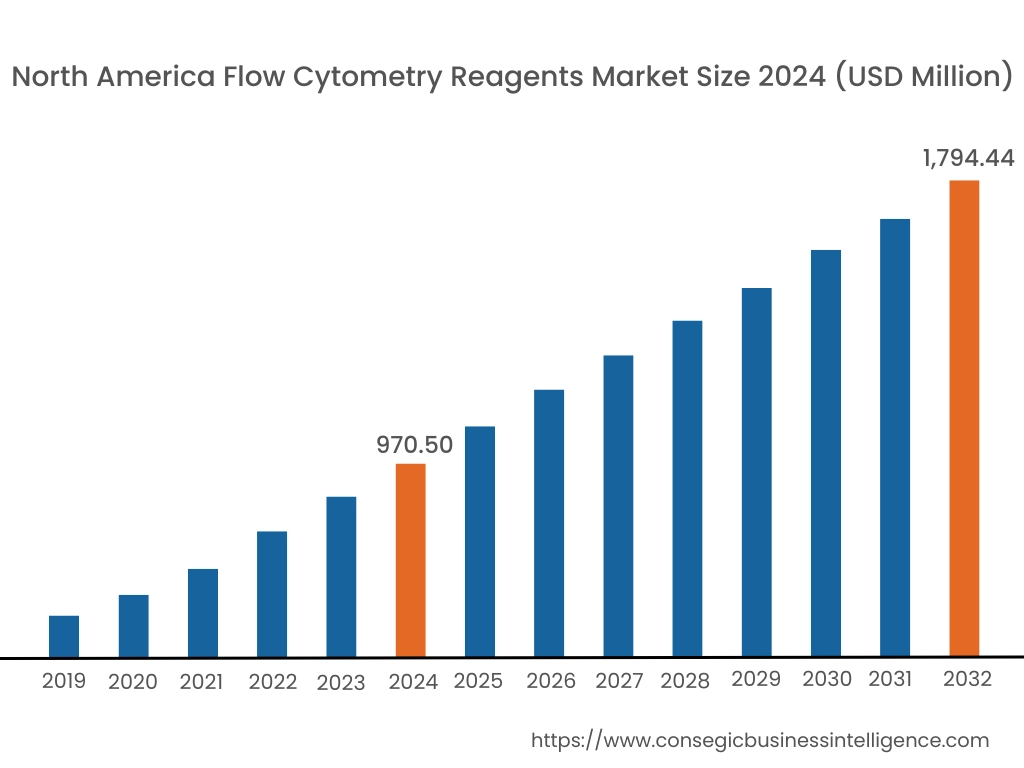

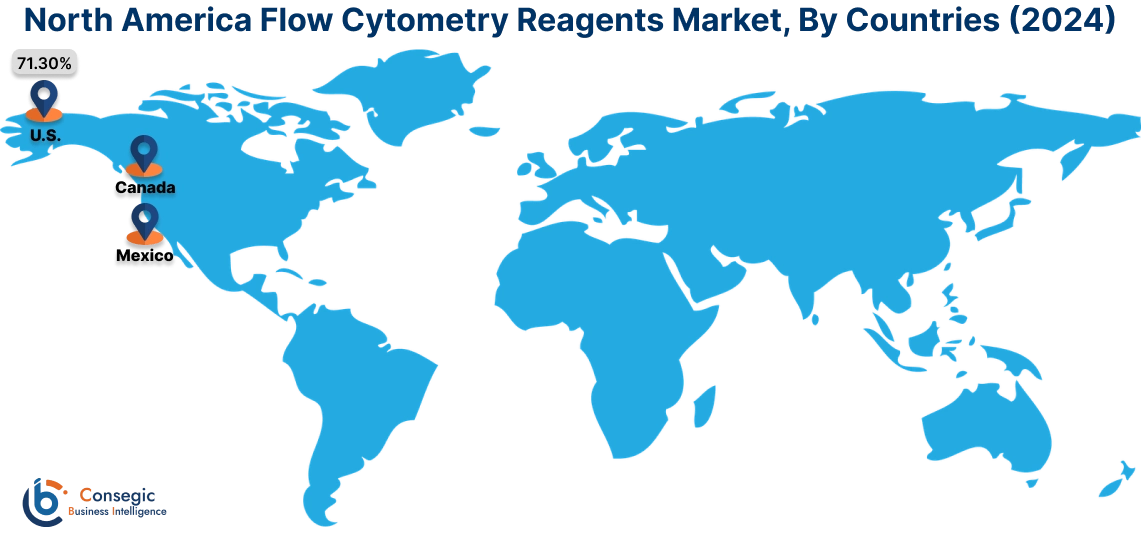

In 2024, North was valued at USD 970.50 Million and is expected to reach USD 1,794.44 Million in 2032. In North America, the U.S. accounted for the highest share of 71.30% during the base year of 2024. North America holds a significant share in the flow cytometry reagents market, driven by a strong focus on advanced research in life sciences, immunology, and oncology. The U.S. leads the region due to the presence of well-established research institutions, pharmaceutical companies, and advanced clinical laboratories. The increasing prevalence of chronic diseases and the need for precise diagnostic tools support the adoption of flow cytometry reagents. Canada contributes with growing investments in healthcare research and immunology studies. However, the high cost of reagents and flow cytometry systems may limit their use in smaller laboratories.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 8.8% over the forecast period. In the flow cytometry reagents market, fueled by rapid advancements in healthcare infrastructure, increasing prevalence of infectious diseases, and expanding biotechnology research in China, India, and Japan. China dominates the region with a growing demand for reagents in cancer research, immunology, and clinical diagnostics, supported by significant government funding for healthcare research. India’s expanding clinical diagnostics sector and increasing focus on vaccine research drive the adoption of flow cytometry reagents. Japan emphasizes high-precision applications in drug development and stem cell research. However, limited access to advanced technologies in rural areas and cost sensitivity may hinder advancement in some parts of the region.

Europe is a prominent market for flow cytometry reagents, supported by robust research activities in biotechnology, immunology, and clinical diagnostics. Countries like Germany, France, and the UK are key contributors. Germany drives trends through its strong pharmaceutical and biotechnology sectors, utilizing flow cytometry reagents for drug development and immunophenotyping. France emphasizes their use in cancer diagnostics and cell-based research, while the UK focuses on expanding clinical applications in hematology and infectious disease studies. However, stringent regulatory frameworks for diagnostic tools and reagents may create challenges for regional manufacturers.

The Middle East & Africa region is witnessing steady development in the flow cytometry reagents market, driven by increasing healthcare investments and rising demand for diagnostic tools in immunology and infectious disease research. In the Middle East, countries like Saudi Arabia and the UAE are adopting flow cytometry technologies in hospitals and research laboratories to enhance diagnostic capabilities. In Africa, South Africa is emerging as a market, leveraging reagents for HIV and tuberculosis research. However, limited local production capabilities and reliance on imports for reagents may restrict broader flow cytometry reagents market expansion in the region.

Latin America is an emerging market for flow cytometry reagents, with Brazil and Mexico leading the region. Brazil’s growing biotechnology and pharmaceutical sectors drive trends for reagents in cancer research, vaccine development, and immunophenotyping. Mexico emphasizes the use of flow cytometry reagents in clinical diagnostics and infectious disease studies. The region’s focus on improving healthcare infrastructure and expanding research capabilities further supports market rise. However, economic instability and inconsistent funding for healthcare research may pose challenges to market development in some countries.

Top Key Players and Market Share Insights:

The flow cytometry reagents market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the flow cytometry reagents market. Key players in the flow cytometry reagents industry include -

- Becton, Dickinson and Company (BD) (USA)

- Danaher Corporation (Beckman Coulter) (USA)

- Luminex Corporation (USA)

- Sysmex Corporation (Japan)

- Cytek Biosciences, Inc. (USA)

- Thermo Fisher Scientific Inc. (USA)

- Bio-Rad Laboratories, Inc. (USA)

- Miltenyi Biotec (Germany)

- Agilent Technologies, Inc. (USA)

- Sony Corporation (Japan)

Recent Industry Developments :

Product Launches:

- In October 2024, Bio-Rad Laboratories expanded its portfolio of flow cytometry reagents with the introduction of StarBright Dyes, a proprietary range of fluorescent nanoparticles designed to enhance panel design flexibility and data resolution in flow cytometry applications. Designed to integrate seamlessly with various flow cytometry platforms, including Bio-Rad's ZE5 Cell Analyzer, facilitating high-throughput and high-parameter cell analysis.

Flow Cytometry Reagents Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 5,070.67 Million |

| CAGR (2025-2032) | 8.3% |

| By Product Type |

|

| By Type |

|

| By Application |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected size of the Flow Cytometry Reagents Market by 2032? +

Flow Cytometry Reagents Market size is estimated to reach over USD 5,536.69 Million by 2032 from a value of USD 2,925.75 Million in 2024 and is projected to grow by USD 3,116.46 Million in 2025, growing at a CAGR of 8.3% from 2025 to 2032.

What factors are driving the growth of the Flow Cytometry Reagents Market? +

The increasing use of flow cytometry in clinical diagnostics, advancements in immunotherapy and drug discovery, and the growing focus on personalized medicine are key growth drivers.

What challenges does the Flow Cytometry Reagents Market face? +

The market faces challenges such as technical complexity, the need for skilled operators, and the high cost of reagents and instruments, which may limit adoption in resource-constrained laboratories.

What are the emerging opportunities in the Flow Cytometry Reagents Market? +

Opportunities include expanding applications in drug development, biomarker discovery, and precision medicine. Innovations in reagent formulations for multiplex analysis and high-content screening also present significant potential for market growth.

Which product type segment dominates the Flow Cytometry Reagents Market? +

The antibodies segment holds the largest market share due to their critical role in immunophenotyping and diagnostics. This segment benefits from advancements in monoclonal antibody technology and increasing adoption in cancer and infectious disease diagnostics.