- Summary

- Table Of Content

- Methodology

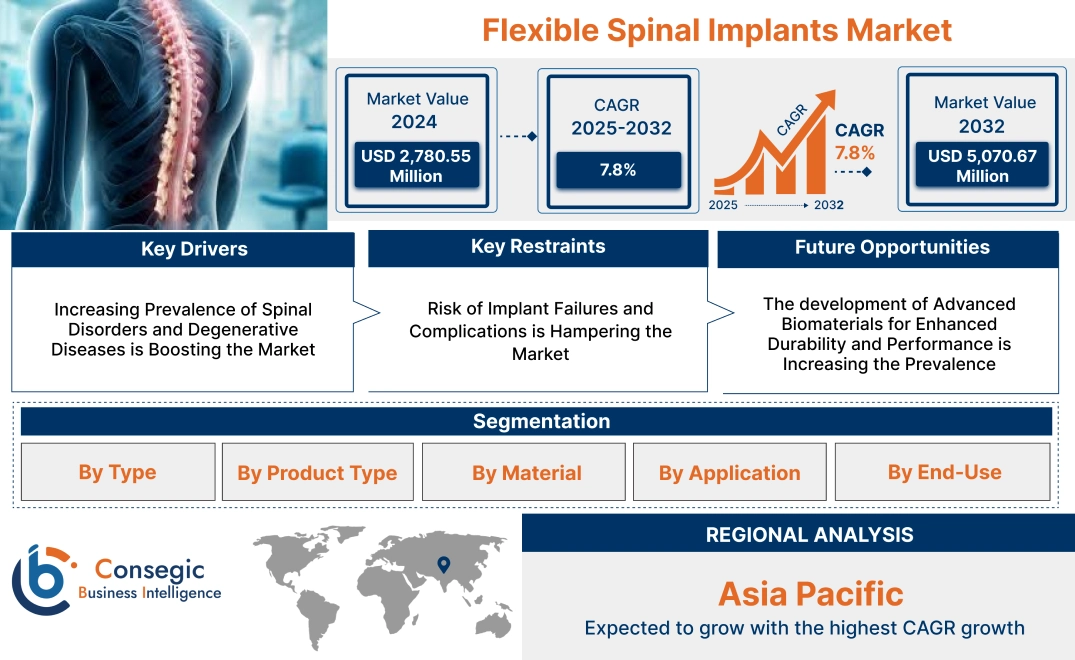

Flexible Spinal Implants Market Size:

Flexible Spinal Implants Market size is estimated to reach over USD 5,070.67 Million by 2032 from a value of USD 2,780.55 Million in 2024 and is projected to grow by USD 2,947.89 Million in 2025, growing at a CAGR of 7.8% from 2025 to 2032.

Flexible Spinal Implants Market Scope & Overview:

The flexible spinal implants are advanced implant systems designed to provide dynamic stabilization, maintain spinal flexibility, and address degenerative spinal conditions. These implants, which include rods, screws, and plates, are engineered with flexible materials to allow controlled movement while reducing the risk of adjacent segment degeneration. Key characteristics of flexible spinal implants include biomechanical stability, compatibility with minimally invasive surgical techniques, and long-term durability. The benefits include improved patient outcomes, reduced recovery times, and preservation of natural spinal motion compared to traditional fusion implants. Applications span degenerative disc disease, scoliosis, herniated discs, and spinal trauma cases. End-users include hospitals, specialty orthopedic clinics, and ambulatory surgical centers, driven by the increasing prevalence of spinal disorders, rising adoption of minimally invasive surgical techniques, and advancements in implant technology aimed at improving patient quality of life.

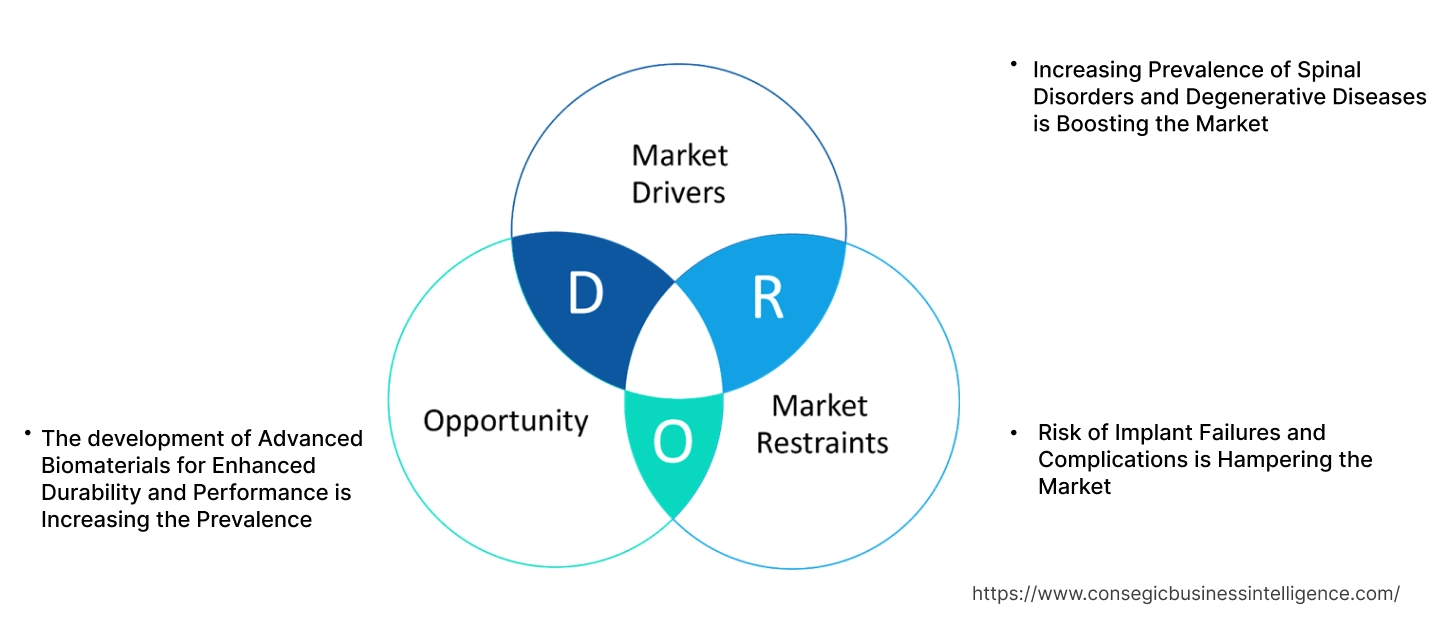

Flexible Spinal Implants Market Dynamics - (DRO) :

Key Drivers:

Increasing Prevalence of Spinal Disorders and Degenerative Diseases is Boosting the Market

The rising occurrence of spinal disorders, including herniated discs, scoliosis, and degenerative disc disease, is significantly driving the adoption of flexible spinal implants. These disorders are increasingly prevalent due to factors such as aging populations, sedentary lifestyles, and workplace ergonomics that strain spinal health. Flexible spinal implants provide an advanced solution by offering enhanced mobility, reduced stress on adjacent spinal segments, and better alignment than traditional rigid implants.

Trends in personalized healthcare and advancements in surgical techniques further support the integration of these implants into modern spinal surgeries. Analysis indicates that the growing emphasis on improving patient mobility and post-surgery recovery aligns with the increased utilization of flexible spinal implants, positioning them as a critical component of spinal care innovations.

Key Restraints:

Risk of Implant Failures and Complications is Hampering the Market

Despite their advantages, flexible spinal implants carry risks such as implant wear, failure, or complications like adjacent segment degeneration and loosening. These issues may result in additional surgical interventions, prolonging recovery and increasing healthcare costs. Factors such as improper implant positioning, material degradation, or patient-specific conditions can exacerbate these risks, creating reluctance among healthcare providers and patients to adopt these solutions in complex cases.

Trends in long-term implant performance and durability highlight the importance of addressing these challenges through material innovations and improved surgical protocols. The analysis underscores the need for continuous advancements in implant design and post-operative monitoring to minimize these complications and enhance patient trust.

Future Opportunities :

The development of Advanced Biomaterials for Enhanced Durability and Performance is Increasing the Prevalence

The advancement of biomaterials has opened new possibilities for enhancing the performance and longevity of flexible spinal implants. Innovative materials such as bioactive coatings, hybrid composites, and nanostructured polymers are being developed to improve biocompatibility, reduce wear, and promote better integration with natural bone. These advancements address key challenges such as implant-related complications and long-term durability, making flexible spinal implants more effective for diverse patient needs.

Trends in material science and nanotechnology are driving the creation of implants that mimic natural bone properties, enhancing their adaptability and minimizing the risk of rejection or loosening. Additionally, bioactive coatings can stimulate bone growth around the implant, ensuring better stabilization and reduced recovery time. Analysis highlights that these innovations are particularly relevant for applications requiring high-performance solutions, such as minimally invasive surgeries and complex spinal reconstructions.

The development of advanced biomaterials also aligns with the growing focus on personalized medicine, enabling the design of implants tailored to individual anatomical and biomechanical requirements. Manufacturers investing in research and development of cutting-edge materials are well-positioned to meet the increasing demand for reliable and efficient spinal care solutions, ensuring better patient outcomes and expanded market opportunities.

Flexible Spinal Implants Market Segmental Analysis :

By Type:

Based on type, the market is segmented into rods, hooks, pedicle screws, plates, cages, and others.

The pedicle screws segment accounted for the largest revenue in flexible spinal implants market share in 2024.

- Pedicle screws are widely utilized in spinal fusion surgeries due to their ability to provide strong anchorage and stability to the vertebrae.

- These screws are essential in treating conditions such as degenerative disc disease, scoliosis, and spinal fractures, making them indispensable in modern spinal surgeries.

- Advancements in screw design, including cannulated and fenestrated screws, have improved procedural outcomes, further driving their adoption.

- The increasing prevalence of spinal disorders and trauma cases globally has bolstered the trends for pedicle screws in hospitals and specialty clinics.

The rods segment is anticipated to register the fastest CAGR during the forecast period.

- Spinal rods are critical components of spinal implants, providing structural support and alignment during spinal fusion procedures.

- Innovations in rod materials, such as titanium and PEEK, have enhanced their flexibility, durability, and biocompatibility, making them increasingly popular.

- The growing adoption of minimally invasive spinal surgeries, where smaller and more flexible rods are required, is driving the flexible spinal implants market growth of this segment.

- Rising awareness about advanced treatment options for spinal deformities and trauma is further fueling the demand for rods in surgical procedures.

By Product Type:

Based on product type, the market is segmented into dynamic stabilization devices, motion preservation devices, and others.

The dynamic stabilization devices segment accounted for the largest revenue share in 2024.

- Dynamic stabilization devices, such as pedicle-based dynamic rod devices and interspinous process spacers, offer flexibility while stabilizing the spine, allowing for controlled motion.

- These devices are widely used in treating degenerative disc diseases, where preserving spinal mobility is critical.

- Advancements in dynamic stabilization technologies, including minimally invasive systems, have increased their adoption across hospitals and surgical centers.

- The rising flexible spinal implants market trends for alternative treatments to traditional spinal fusion surgeries have further boosted the adoption of dynamic stabilization devices.

The motion preservation devices segment is anticipated to register the fastest CAGR during the forecast period.

- Motion preservation devices, such as artificial discs and annulus repair devices, are increasingly used to treat spinal disorders while maintaining natural movement.

- The growing preference for less invasive procedures and shorter recovery times has driven the demand for these devices in spinal surgeries.

- Technological advancements in artificial disc designs, including biocompatible materials and enhanced durability, are contributing to their growth.

- The rising prevalence of spinal disorders and a shift toward motion-preserving procedures over traditional fusion surgeries are fueling this segment’s expansion.

By Material:

Based on material, the spinal implants and devices market is segmented into titanium, PEEK (polyether ether ketone), stainless steel, and others.

The titanium segment accounted for the largest revenue in the flexible spinal implants market share in 2024.

- Titanium is widely used in spinal implants due to its high strength, corrosion resistance, and biocompatibility, making it suitable for long-term use.

- Titanium implants are favored in spinal fusion surgeries and deformity corrections for their compatibility with imaging technologies like MRI and CT scans.

- The growing adoption of titanium-based expandable cages and rods has further bolstered this segment’s dominance.

- The increasing opportunities for durable and lightweight materials in advanced spinal procedures are driving the preference for titanium implants.

The PEEK segment is anticipated to register the fastest CAGR during the forecast period.

- PEEK is gaining traction as a material for spinal implants due to its excellent biocompatibility, radiolucency, and ability to mimic the flexibility of natural bone.

- The material’s use in interbody cages and motion-preserving devices is growing, particularly in minimally invasive spinal surgeries.

- Advancements in PEEK composite materials, such as carbon-reinforced PEEK, are enhancing implant performance and durability.

- The rising preference for implants that allow better post-operative imaging and reduced stress shielding is driving the adoption of PEEK-based implants.

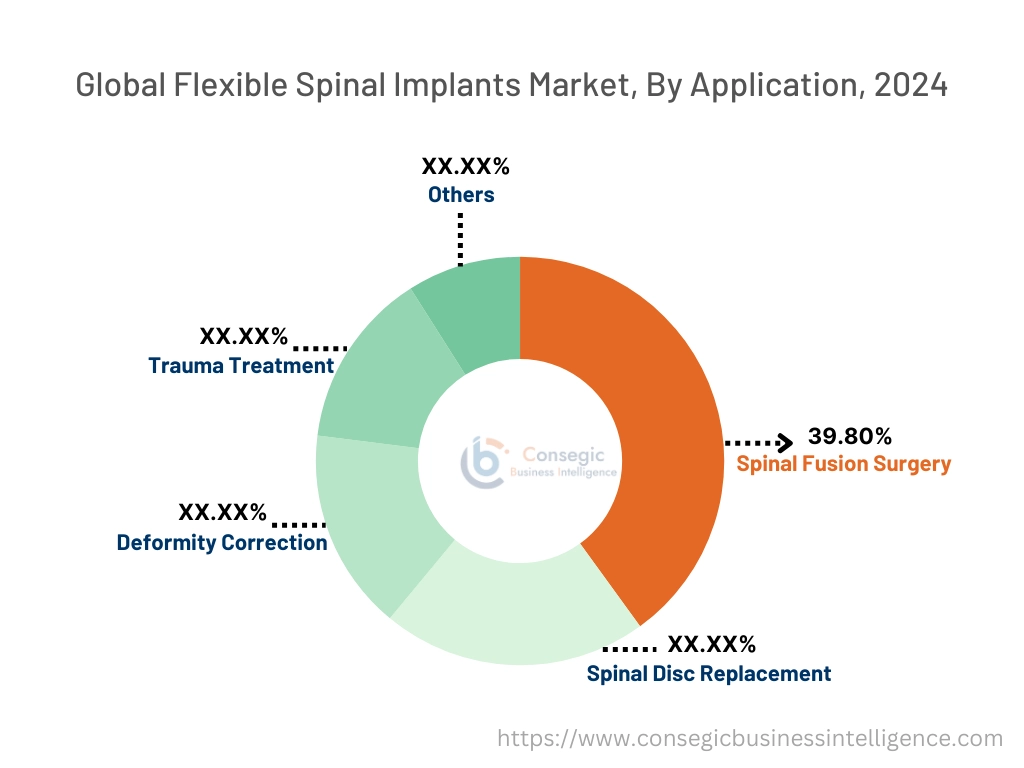

By Application:

Based on application, the spinal implants and devices market is segmented into spinal fusion surgery, spinal disc replacement, deformity correction, trauma treatment, and others.

The spinal fusion surgery segment accounted for the largest revenue of 39.80% share in 2024.

- Spinal fusion surgery remains the gold standard for treating conditions like degenerative disc diseases, spinal fractures, and scoliosis.

- The increasing prevalence of chronic back pain and spinal disorders globally has driven the flexible spinal implants market trends for fusion implants and devices.

- Technological advancements, including minimally invasive techniques and expandable fusion cages, have further enhanced procedural outcomes.

- The rising number of geriatric patients requiring spinal surgeries has also contributed to the flexible spinal implants market growth of this segment.

The spinal disc replacement segment is anticipated to register the fastest CAGR during the forecast period.

- Spinal disc replacement is gaining popularity as an alternative to fusion surgery, offering better mobility and reduced recovery times.

- The increasing adoption of artificial discs, designed with advanced materials like titanium and PEEK, is driving this segment’s growth.

- The growing prevalence of disc degenerative diseases among the working-age population is boosting the demand for disc replacement procedures.

- Rising awareness about motion-preserving surgical options and improved healthcare infrastructure in emerging economies are supporting the flexible spinal implants market expansion.

By End-Use:

Based on end-use, the market is segmented into hospitals, ambulatory surgical centers, specialty clinics, and others.

The hospitals segment accounted for the largest revenue share in 2024.

- Hospitals perform a majority of spinal surgeries due to their advanced infrastructure and access to skilled surgeons.

- The increasing prevalence of spinal disorders and trauma cases has driven the adoption of spinal implants and devices in hospital settings.

- Investments in robotic-assisted spinal surgeries and advanced imaging technologies have further strengthened hospitals’ dominance in this market.

- The availability of comprehensive post-operative care and rehabilitation services has contributed to the segment’s growth.

The ambulatory surgical centers segment is anticipated to register the fastest CAGR during the forecast period.

- Ambulatory surgical centers are gaining traction due to their cost-effectiveness and shorter patient stays compared to hospitals.

- These centers specialize in minimally invasive procedures, making them ideal for spinal implant surgeries such as disc replacements and deformity corrections.

- The growing trend of outpatient care and the establishment of advanced surgical centers in urban and rural areas are driving flexible spinal implants market opportunities in this segment.

- Technological advancements in portable and compact spinal surgical instruments are further fueling the adoption of spinal implants in ambulatory surgical centers.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

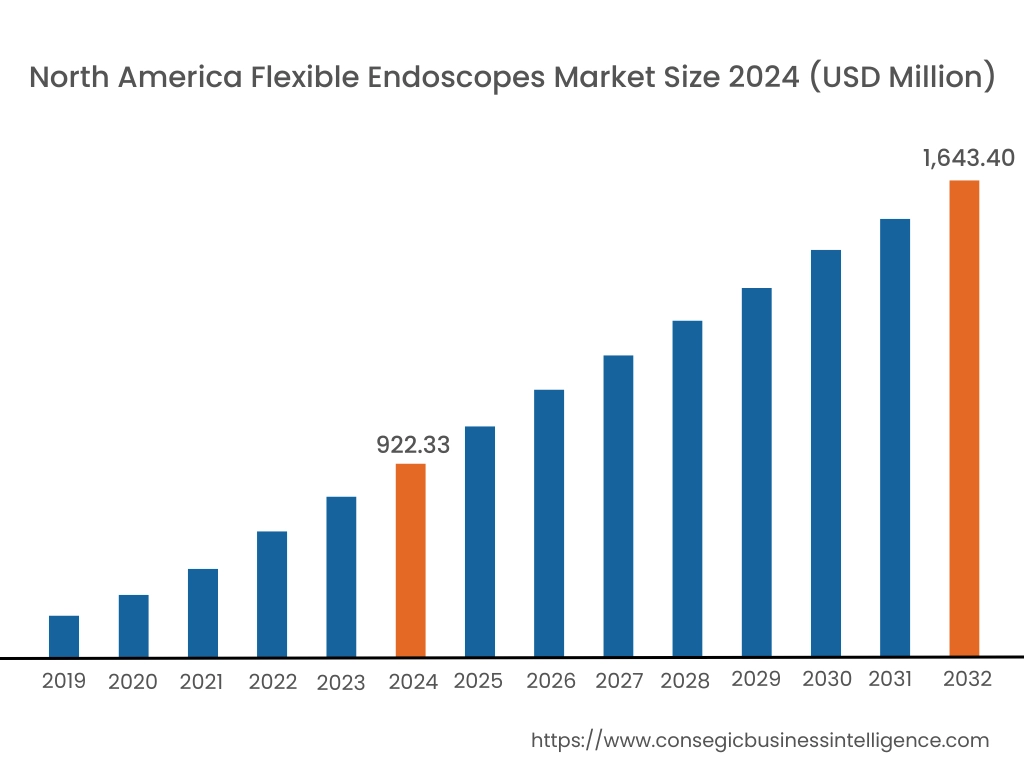

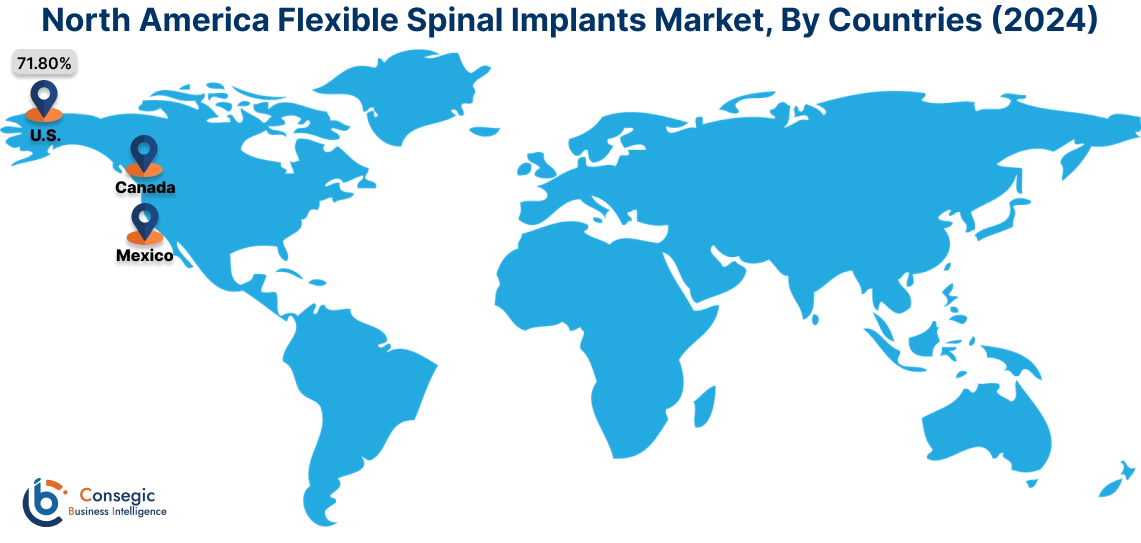

In 2024, North was valued at USD 922.33 Million and is expected to reach USD 1,643.40 Million in 2032. In North America, the U.S. accounted for the highest share of 71.80% during the base year of 2024. North America holds a significant share of the flexible spinal implants market, driven by the rising prevalence of spinal disorders, advancements in healthcare infrastructure, and high adoption of innovative surgical technologies. The U.S. leads the region due to a strong trend for minimally invasive spinal surgeries and the presence of key market players developing advanced flexible spinal implant systems. Canada contributes with increasing investments in orthopedic care and an aging population requiring spinal interventions. However, the high cost of spinal implant surgeries may limit accessibility for certain patient groups.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 8.3% over the forecast period. In the flexible spinal implants market analysis, fueled by rapid urbanization, increasing healthcare investments, and a rising prevalence of spinal disorders in China, India, and Japan. China dominates the region with a growing demand for advanced spinal implants to address an increasing number of spinal injuries and degenerative conditions. India’s expanding healthcare infrastructure supports the adoption of cost-effective spinal implants in hospitals and specialty clinics. Japan focuses on high-precision spinal implants, leveraging its strong medical technology industry and increasing the elderly population. However, limited awareness and affordability challenges in rural areas may hinder expansion in certain parts of the region.

Europe is a prominent market, supported by an aging population, increasing cases of degenerative spinal disorders, and strong government healthcare systems. Countries like Germany, France, and the UK are key contributors. As per the flexible spinal implants market analysis, Germany drives trends through its advanced orthopedic care facilities and focuses on innovative spinal surgery techniques. France emphasizes the use of flexible implants in addressing spinal deformities and degenerative conditions, while the UK focuses on adopting minimally invasive spinal procedures to improve patient outcomes. However, budget constraints in public healthcare systems may pose challenges to the adoption of advanced implants.

The Middle East & Africa region is witnessing steady development in the flexible spinal implants market, driven by increasing investments in healthcare infrastructure and a rising incidence of spinal injuries and disorders. In the Middle East, countries like Saudi Arabia and the UAE are adopting advanced spinal implant technologies in hospitals and specialty clinics, supported by government initiatives to improve orthopedic care. In Africa, South Africa is an emerging market, focusing on improving access to spinal care through partnerships with global flexible spinal implants market manufacturers. However, limited local manufacturing and reliance on imports may restrict market development in the region.

Latin America is an emerging market, with Brazil and Mexico leading the region. Brazil’s expanding healthcare sector and rising prevalence of spinal disorders drive trends for advanced implants in orthopedic surgeries. Mexico emphasizes the adoption of flexible spinal implants in hospitals and specialty clinics, supported by increasing awareness about minimally invasive spinal procedures. The regional analysis is also exploring collaborations with international medical device manufacturers to improve access to advanced spinal solutions. However, economic instability and inconsistent healthcare policies may pose challenges to market development in smaller economies.

Top Key Players and Market Share Insights:

The flexible spinal implants market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the flexible spinal implants market. Key players in the flexible spinal implants industry include -

- Medtronic plc (USA)

- Stryker Corporation (USA)

- Braun Melsungen AG (Germany)

- Abbott Spine Inc. (USA)

- K2M Group Holdings (USA)

- Zimmer Biomet Holdings Inc. (USA)

- NuVasive Inc. (USA)

- Globus Medical Inc. (USA)

- Alphatec Holdings Inc. (USA)

- Orthofix International N.V. (Netherlands)

Recent Industry Developments :

Advancements:

- In November 2024, Zimmer Biomet announced the CE Mark certification for its Persona Revision Knee System, expanding its portfolio in personalized knee solutions. Immer Biomet's first titanium spinal implant manufactured via a 3D printing process, the Zyston Strut Open System is designed to enhance the strength, graft capacity, and visualization of the interbody spacer in spinal fusion cases.

- In April 2024, Zimmer Biomet Holdings, Inc., a global leader in medical technology, announced the successful completion of the first-ever robotic-assisted shoulder replacement surgery using the ROSA Shoulder System. The groundbreaking procedure was performed at the Mayo Clinic by Dr. John W. Sperling, Professor of Orthopedic Surgery and a key member of the ROSA Shoulder development team, highlighting a significant advancement in robotic-assisted surgical technology.

Flexible Spinal Implants Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 5,070.67 Million |

| CAGR (2025-2032) | 7.8% |

| By Type |

|

| By Product Type |

|

| By Material |

|

| By Application |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected size of the Flexible Spinal Implants Market by 2032? +

Flexible Spinal Implants Market size is estimated to reach over USD 5,070.67 Million by 2032 from a value of USD 2,780.55 Million in 2024 and is projected to grow by USD 2,947.89 Million in 2025, growing at a CAGR of 7.8% from 2025 to 2032.

What factors are driving the growth of the Flexible Spinal Implants Market? +

The increasing prevalence of spinal disorders, advancements in implant technology, and rising adoption of minimally invasive surgical techniques are key drivers.

What challenges does the Flexible Spinal Implants Market face? +

The market faces challenges such as risks of implant failures, complications like adjacent segment degeneration, and material degradation. These issues necessitate advancements in implant design and post-operative monitoring to enhance reliability.

What are the emerging opportunities in the Flexible Spinal Implants Market? +

Advancements in biomaterials, such as bioactive coatings, nanostructured polymers, and hybrid composites, present significant opportunities. These materials improve durability, biocompatibility, and integration with bone, driving demand for high-performance implants tailored to patient needs.