- Summary

- Table Of Content

- Methodology

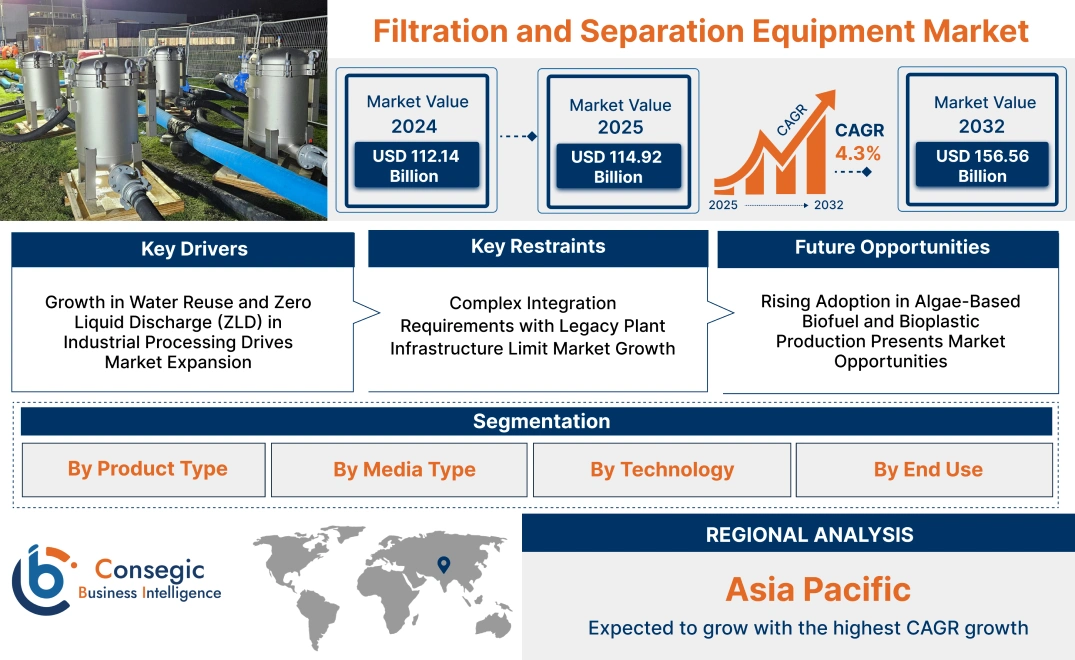

Filtration and Separation Equipment Market Size:

Filtration and Separation Equipment Market size is estimated to reach over USD 156.56 Billion by 2032 from a value of USD 112.14 Billion in 2024 and is projected to grow by USD 114.92 Billion in 2025, growing at a CAGR of 4.3% from 2025 to 2032.

Filtration and Separation Equipment Market Scope & Overview:

Filtration and separation equipment is a general term for a wide variety of systems designed to eliminate solids, liquids, or gases from a mixture, as well as ensure process purity and operational integrity. The units are used across various industries like water treatment, pharmaceuticals, food processing, oil and gas, and chemical manufacturing, where material separation is crucial.

Major system designs involve membrane filters, centrifuges, vacuum filters, cartridge units, and magnetic separators, all suited for certain throughput, particle size, and fluid compatibility. State-of-the-art features consist of automated control, corrosion-resistant materials, and modular integration into existing process lines.

The application of separation and filtration equipment makes a contribution to better product quality, lower process downtime, as well as regulations adhering to strict regulatory standards. With the ability to accommodate batch and continuous processes, these systems offer scalable and fault-tolerant solutions adjusted for sophisticated industrial environments to enable consistent production and peak process performance in high-demand applications.

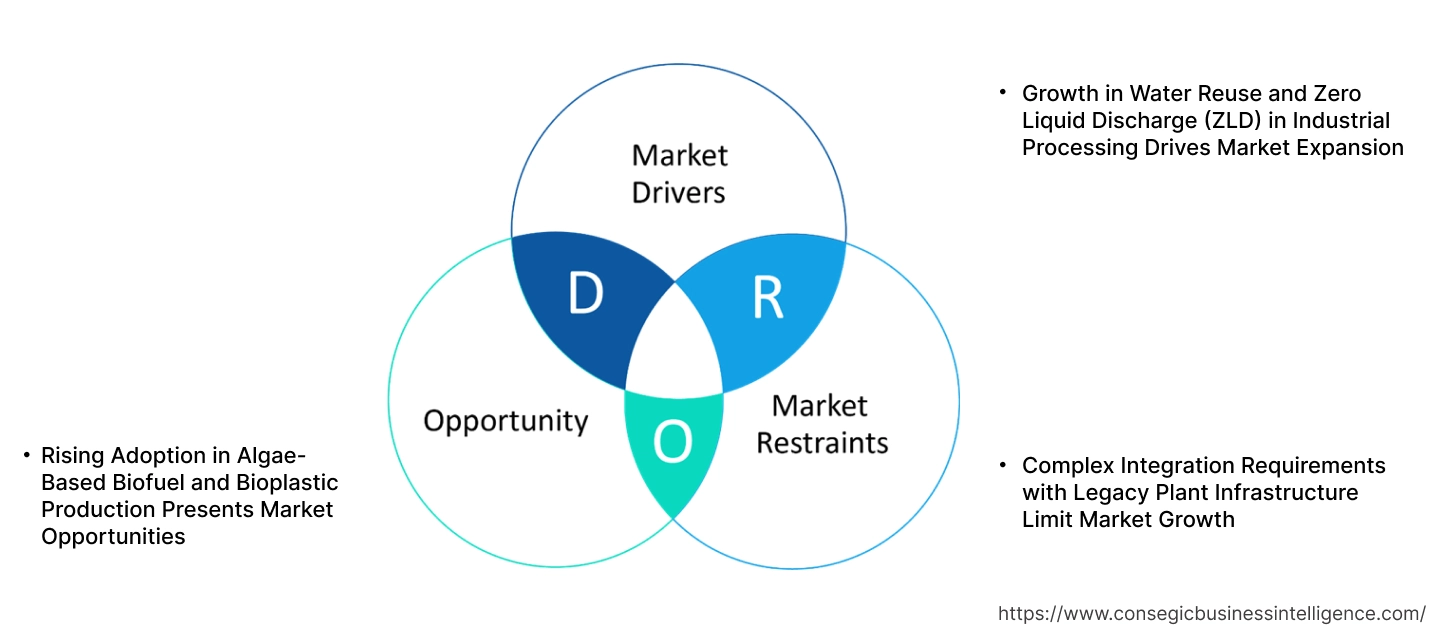

Filtration and Separation Equipment Market Dynamics - (DRO) :

Key Drivers:

Growth in Water Reuse and Zero Liquid Discharge (ZLD) in Industrial Processing Drives Market Expansion

The drive toward water sustainability and compliance with regulation is driving the adoption of separation and filtration equipment for industrial water reuse and ZLD applications. The textile, power generation, petrochemical, and pharmaceutical industries are faced with the imperative of minimizing freshwater use and disposing of liquid wastes. Multi-stage treatment systems utilizing ultrafiltration (UF), reverse osmosis (RO), and evaporative crystallizers are dependent on high-performance filtration for process reliability and regulatory discharge limits. Next-generation separation technologies eliminate suspended solids, organics, and dissolved salts with high recovery rates and uniform water quality for recycling and reuse. With tightening environmental regulations and water scarcity growing in industrial belts, closed-loop water treatment systems are increasingly in demand. The capability of filtration platforms to facilitate circularity of water while reducing environmental impact is making them indispensable assets, fueling the filtration and separation equipment market expansion.

Key Restraints:

Complex Integration Requirements with Legacy Plant Infrastructure Limit Market Growth

Most industrial plants have legacy process systems with dated piping configurations, non-uniform interfaces, and low spatial flexibility. Adding contemporary filtration and separation units to such systems poses structural compatibility, instrumentation coordination, and control system synchronization challenges. In chemical, refinery, and pulp & paper industries, filter retrofits involve extensive reengineering of process loops or bypass paths to meet flow rates, pressure drop allowances, and redundancy schemes. These changes raise capital expenses, prolong installation times, and interfere with operations. In plants with low downtime acceptability, these integration obstacles postpone equipment upgrade, even when performance improvements are apparent. The absence of plug-and-play capability among older facilities limits the flexibility of adoption and the length of innovation cycles, inhibiting overall filtration and separation equipment market growth despite robust end-user demand.

Future Opportunities :

Rising Adoption in Algae-Based Biofuel and Bioplastic Production Presents Market Opportunities

Algae biofuel and bioplastic production need accurate and efficient separation processes throughout biomass harvesting, cell disruption, and lipid or polymer recovery. Separation equipment and filtration gear like membrane modules, disc-stack centrifuges, and vacuum filters play a crucial role in separating high-value compounds while maintaining product purity and conserving energy consumption. As the world interest speeds up for alternative feedstocks and carbon-neutral processes, algae-derived materials are picking up pace in energy, packaging, and biochemical sectors. These production routes depend on continuous, hygienic, and scalable separation technologies with high solid handling and variable feedstock tolerance. Needs for sustainable manufacturing and bioprocessing technology are driving new technical specifications for filtration manufacturers. As applications of algae move from research scale to commercial use, expert system configurations are becoming increasingly significant—fueling long-term filtration and separation equipment market opportunities based on development and necessity in bio-based applications.

Filtration and Separation Equipment Market Segmental Analysis :

By Product Type:

Based on product type, the market is segmented into filters (cartridge filters, bag filters, panel filters, etc.), centrifuges, membrane modules, magnetic separators, cyclones & hydrocyclones, filter press, and vacuum belt filters.

Filters accounted for the largest market share in 2024.

- Filters are widely used across industries due to their simplicity, cost-effectiveness, and availability in multiple configurations such as cartridge, bag, and panel types.

- The adaptability of filters to both solid and liquid separation needs supports consistent requirements across diverse applications.

- Their high utility in HVAC, pharmaceuticals, and food & beverage industries reinforces their strong market position.

- For instance, in April 2024, Abatement Technologies launched the ATL Filtration™ brand to expand into filter replacement supply and service. The company, with 39 years of experience in the indoor air quality industry, unveiled the new service to provide affordable, comprehensive air filtration solutions and exceptional service for commercial buildings in the United States and Canada.

- exceptional service for commercial buildings in the United States and Canada

- The continued expansion of industrial infrastructure globally is expected to drive filtration and separation equipment market demand in this category.

Membrane modules are projected to exhibit the fastest CAGR during the forecast period.

- The rising adoption of advanced membrane technologies for water treatment and ultrapure processing enhances the appeal of membrane modules.

- These modules offer selective separation capabilities critical for chemical, electronics, and biotech sectors.

- Advancements in membrane durability and efficiency, particularly in reverse osmosis and ultrafiltration, are key market trends.

- According to filtration and separation equipment market analysis, membrane modules benefit from increasing environmental regulations and water reuse mandates.

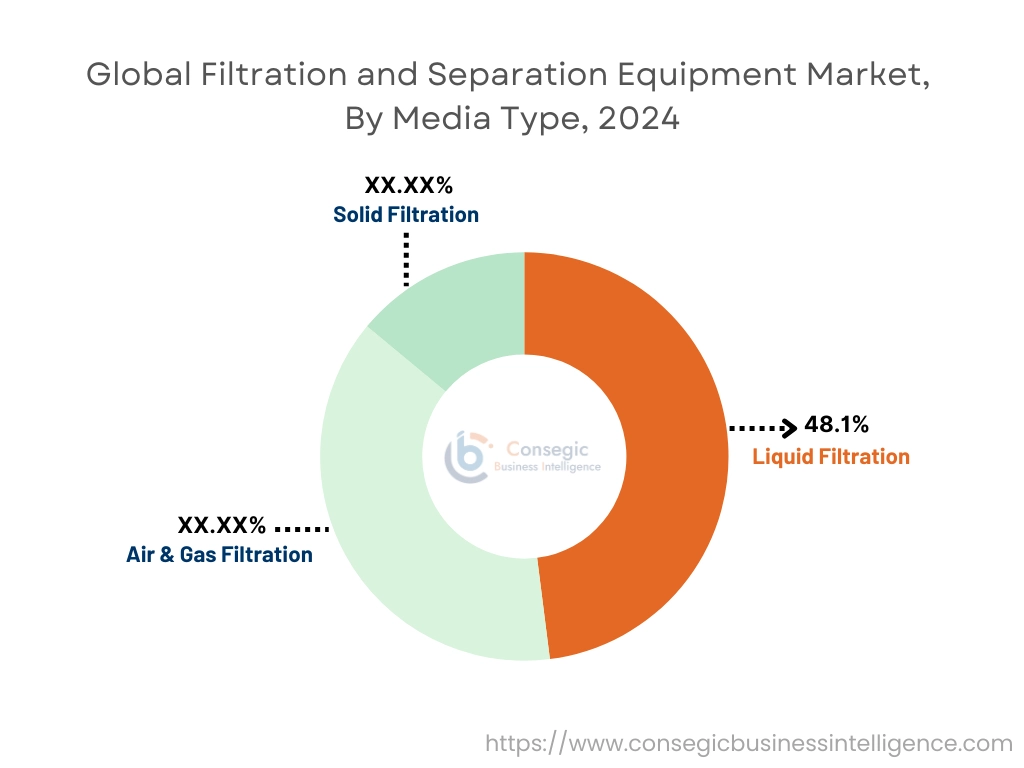

By Media Type:

Based on media type, the market is divided into liquid filtration, air & gas filtration, and solid filtration.

Liquid filtration held the dominant filtration and separation equipment market share of 48.1% in 2024.

- The widespread use of liquid filtration systems in food processing, chemical manufacturing, and water treatment drives segment growth.

- The need for regulatory-compliant wastewater treatment technologies continues to rise, supporting liquid filtration dominance.

- Product innovations such as self-cleaning filters and high-capacity filtration media are shaping liquid filtration trends.

- The filtration and separation equipment market analysis shows increasing investments in infrastructure for safe water management.

Air & gas filtration is expected to register a robust CAGR during the forecast period.

- Stricter air quality standards in industrial zones and rising awareness of indoor air quality fuel the need for air filtration solutions.

- Applications across cleanrooms, semiconductor fabs, and gas processing plants contribute to the segment's growth.

- High-efficiency particulate air (HEPA) and ULPA technologies are advancing rapidly to meet evolving industry needs.

- As per filtration and separation equipment market trends, air & gas filtration systems are critical for protecting sensitive manufacturing environments.

By Technology:

Based on technology, the market includes mechanical filtration, membrane filtration, centrifugal separation, magnetic separation, gravity separation, electrostatic separation, vacuum filtration, and pressure filtration.

Mechanical filtration held the largest share in 2024.

- Mechanical filtration technologies like screens, cartridges, and bags are simple, scalable, and cost-effective for general-purpose use.

- Their applicability across air, liquid, and particulate separation provides operational flexibility.

- These systems offer ease of maintenance and integration into legacy processing systems.

- According to the filtration and separation equipment market trends, the continued use in food processing and industrial manufacturing supports market stability.

Membrane filtration is projected to grow at the fastest CAGR during the forecast timeline.

- The increasing need for precise separation and high-quality output in biotech, pharmaceuticals, and desalination is driving adoption.

- The expanding use of ultrafiltration, nanofiltration, and reverse osmosis is a major market growth trend.

- Rising concerns over water scarcity and contamination elevate membrane technology relevance.

- As per the segmental analysis, the need for energy-efficient and high-recovery membranes will propel this segment.

By End-Use:

Based on end-use, the market is categorized into chemicals, oil & gas, pharmaceuticals & biotechnology, food & beverage, water & wastewater treatment utilities, power generation, mining, electronics & semiconductors, pulp & paper, automotive, aerospace & defense, and others.

Water & wastewater treatment utilities held the largest filtration and separation equipment market share in 2024.

- Municipal and industrial water treatment requirements continue to rise globally, especially in Asia-Pacific and the Middle East.

- Public sector investments and tightening environmental laws fuel demand for high-performance filtration equipment.

- Adoption of modular filtration solutions and mobile treatment units is an emerging trend.

- The water & wastewater treatment utilities benefit from continued infrastructure development and urbanization, bolstering filtration and separation equipment market expansion.

Pharmaceuticals & biotechnology segment is anticipated to experience the fastest CAGR.

- The growing production of injectable drugs, vaccines, and biopharmaceuticals requires stringent filtration standards.

- Advancements in single-use technologies and cleanroom filtration solutions are boosting adoption.

- Regulations from agencies like the FDA and EMA drive innovation in sterile filtration and process integrity.

- For instance, in December 2024, Amazon Filters launched a high-temperature vent filter for the pharmaceuticals & biotechnology sector. SupaPore TMB, an improved high-temperature-resistant membrane product, is created for hot operating conditions in processes like sterile air venting and large-scale fermentation. Its key attributes include polyphenylene sulphide membrane support and drainage layers, that provide robust resistance to oxidative and ozonated environments.

- The filtration and separation equipment market growth is driven by the rapid expansion of global pharmaceutical manufacturing capacity.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

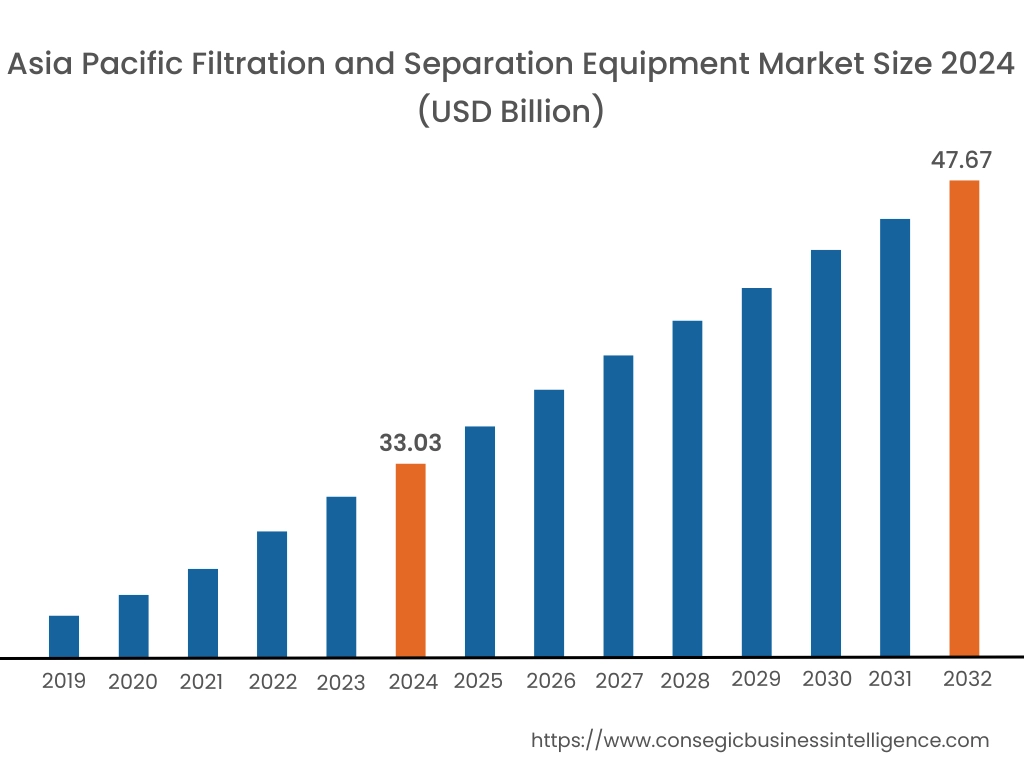

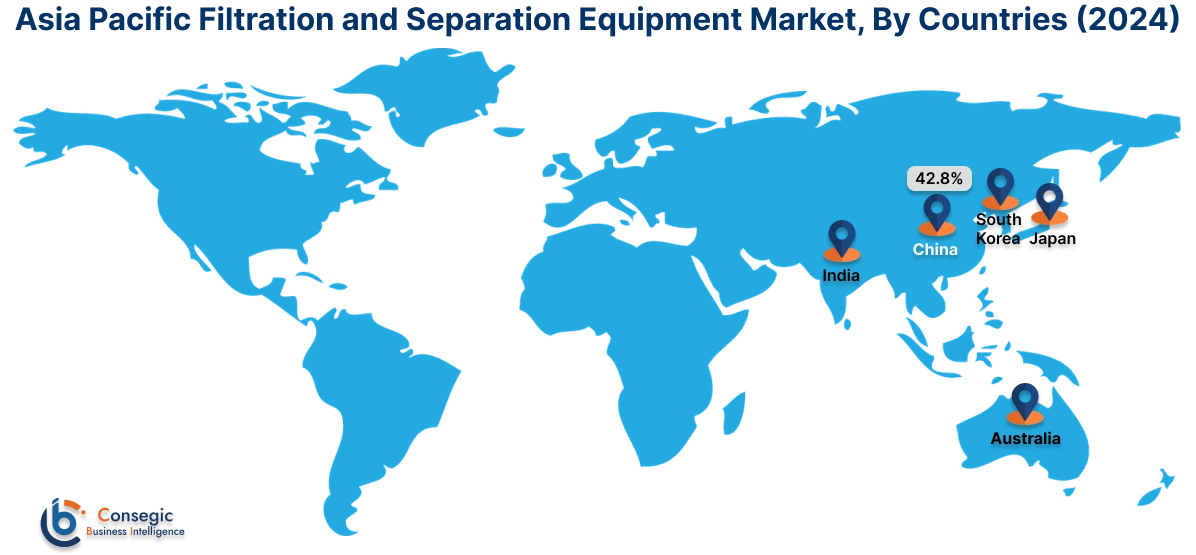

Asia Pacific region was valued at USD 33.03 Billion in 2024. Moreover, it is projected to grow by USD 33.94 Billion in 2025 and reach over USD 47.67 Billion by 2032. Out of this, China accounted for the maximum revenue share of 42.8%. Asia-Pacific is the most rapidly growing market in the filtration and separation equipment industry, fueled by rapid industrial growth, urban infrastructure development, and increasing environmental enforcement. China, India, Japan, and South Korea are prominent adopters, especially in the petrochemical, textile, and semiconductor industries, where accurate filtration is essential to functional quality.

- In June 2024, Pall Corporation opened a US$150 million manufacturing facility in Singapore to support the global semiconductor industry. The company, a leader in filtration, separation and purification technologies, inaugurated the new state-of-the-art manufacturing facility to better serve regional and global customers. The facility aims to provide lithography and wet-etch filtration, purification and separation solutions to support the production of semiconductor chips.

Analysis indicates that public sector projects designed to enhance air and water quality, together with private investment in manufacturing modernization, are driving substantial growth in equipment sales. Local production capacities are being enhanced to address cost-conscious market segments, while high-end systems are also finding traction in urban water recycling and cleanroom applications.

North America is estimated to reach over USD 50.74 Billion by 2032 from a value of USD 37.20 Billion in 2024 and is projected to grow by USD 38.05 Billion in 2025. North America remains the center for high-performance filtration technologies with extensive application in chemical processing, the pharmaceutical industry, water treatment, and the food & beverage sector. The United States and Canada lead the innovation in sophisticated particulate and liquid separation systems due to stringent EPA and FDA regulations. Market analysis indicates strong replacement cycles and increasing requirements for automated and energy-saving systems. The trend towards closed-loop production and zero-liquid discharge systems has added to the need for specialized equipment. Investment in renewable energy initiatives and data center growth also drives high equipment demand for process air and water purity.

Europe has a regulation-intensive and innovation-led market, where environmental directives, decarbonization goals for industry, and stringent operational standards drive equipment uptake. Regional coverage includes Germany, France, the UK, and the Netherlands, with filtration solutions spread across bioprocessing, electricity generation, and municipal infrastructure. Regional analysis further shows steady expansion underpinned by the EU's Green Deal framework and reusing wastewater policy. Growing emphasis on circular handling of resources through filtration of industrial effluents and air pollution propels ongoing equipment upgrades. Furthermore, a mature manufacturing infrastructure and the requirement to meet REACH and ISO standards make Europe a long-term, stable consumer of both standard and custom-designed systems.

Latin America represents a steadily expanding market, with Brazil, Mexico, and Chile exhibiting growing usage in mining, oil refining, and beverage production. The requirement in the region is bolstered by rising industrial safety needs, concern for water availability, and upgrading of public water utilities. Market data indicate that cost-effective, low-maintenance systems are favored, especially among industries with cost and manpower limitations. Furthermore, regional development initiatives supporting environmental compliance and border investment in process industries are driving long-term filtration and separation equipment market demand.

The Middle East and Africa region exhibits increasing demand for industrial-size and mobile filtration systems, particularly in water-stressed and oil-producing economies. Some nations, such as the UAE, Saudi Arabia, and South Africa, are investing in desalination, natural gas processing, and clean energy production—all fields with high equipment needs. Regional reports state that the requirement for low-maintenance, climate-resilient filtration units is on the rise, particularly in infrastructure-intensive surroundings. Although local equipment production is still small-scale, collaborations with international suppliers are improving availability and service provision. The filtration and separation equipment market opportunity in this region remains to realign solutions to long-term sustainability objectives and support industrial diversification initiatives.

Top Key Players and Market Share Insights:

The filtration and separation equipment market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global filtration and separation equipment market. Key players in the filtration and separation equipment industry include -

- Alfa Laval AB (Sweden)

- MANN+HUMMEL Group (Germany)

- Porvair Filtration Group (United Kingdom)

- SPX Flow, Inc. (USA)

- Graver Technologies (USA)

- Eaton Corporation plc (Ireland)

- GEA Group AG (Germany)

- Suez Water Technologies & Solutions (France)

- HYDAC International GmbH (Germany)

- Pentair plc (Ireland)

Recent Industry Developments :

Acquisitions:

- In November 2024, Lifco acquired Kögel Filter in Germany. Kögel Filter was consolidated in the Business Area Systems Solutions, division Special Products.

- In January 2024, Rensa Filtration completed acquisitions of multiple companies that ensure the distribution, sales and service of air filters to commercial and industrial customers and end-users in California, Illinois, New York and Arizona. Air Filter Supply, Air Filter Engineers, R.P. Fedder and Dave Downing & Associates are the companies joining Rensa.

Filtration and Separation Equipment Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 156.56 Billion |

| CAGR (2025-2032) | 4.3% |

| By Product Type |

|

| By Media Type |

|

| By Technology |

|

| By End Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Filtration and Separation Equipment Market? +

Filtration and Separation Equipment Market size is estimated to reach over USD 156.56 Billion by 2032 from a value of USD 112.14 Billion in 2024 and is projected to grow by USD 114.92 Billion in 2025, growing at a CAGR of 4.3% from 2025 to 2032.

What specific segmentation details are covered in the Filtration and Separation Equipment Market report? +

The Filtration and Separation Equipment market report includes specific segmentation details for product type, media type, technology and end-use.

What are the end-uses of the Filtration and Separation Equipment Market? +

The end-use of the Filtration and Separation Equipment Market is chemicals, oil & gas, pharmaceuticals & biotechnology, food & beverage, water & wastewater treatment utilities, power generation, mining, electronics & semiconductors, pulp & paper, automotive, aerospace & defense and others (textiles, marine, etc.).

Who are the major players in the Filtration and Separation Equipment Market? +

The key participants in the Filtration and Separation Equipment market are Alfa Laval AB (Sweden), MANN+HUMMEL Group (Germany), Eaton Corporation plc (Ireland), GEA Group AG (Germany), Suez Water Technologies & Solutions (France), HYDAC International GmbH (Germany), Pentair plc (Ireland), Porvair Filtration Group (United Kingdom), SPX Flow, Inc. (USA) and Graver Technologies (USA).