- Summary

- Table Of Content

- Methodology

Fault Circuit Indicator Market Size:

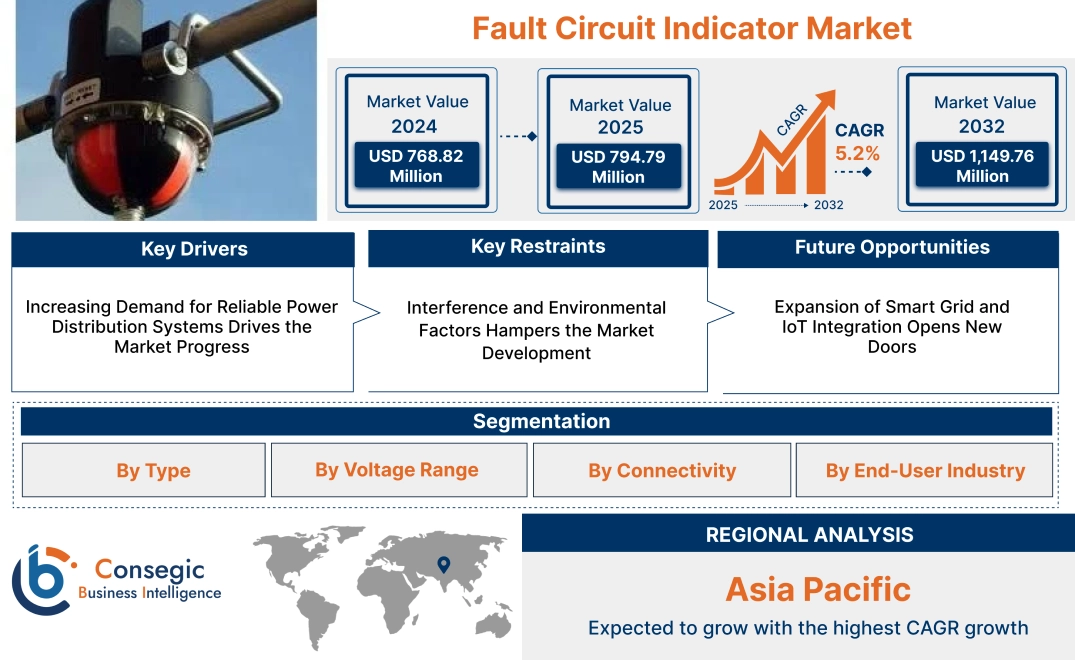

Fault Circuit Indicator Market size is estimated to reach over USD 1,149.76 Million by 2032 from a value of USD 768.82 Million in 2024 and is projected to grow by USD 794.79 Million in 2025, growing at a CAGR of 5.2% from 2025 to 2032.

Fault Circuit Indicator Market Scope & Overview:

A fault circuit indicator (FCI) is a device used in electrical power distribution systems to detect and indicate faults such as short circuits and ground faults. These devices are critical for identifying fault locations in underground and overhead power lines, enabling quicker response times for maintenance and repair teams. FCIs help minimize power outages and improve the reliability and safety of electrical distribution networks.

These indicators are available in various types, including overhead line indicators, underground line indicators, and resettable models, designed to meet specific operational requirements. They are equipped with advanced sensing technologies that detect fault currents and provide visual or remote alerts. Some models also feature wireless communication capabilities, allowing integration with grid monitoring systems for real-time fault detection and analysis.

End-users of these indicators include utility companies, industrial facilities, and commercial infrastructure operators who rely on efficient fault detection to maintain continuous and safe power supply. FCIs play a vital role in modernizing electrical grid infrastructure and improving operational efficiency.

Fault Circuit Indicator Market Dynamics - (DRO) :

Key Drivers:

Increasing Demand for Reliable Power Distribution Systems Drives the Market Progress

The increasing demand for reliable power distribution systems, particularly in urban areas, is a key driver for the market. As urbanization and population growth continue, the need for a stable and uninterrupted power supply becomes even more critical. Fault detection technologies, including advanced fault circuit indicators, play a crucial role in maintaining the reliability of power distribution networks. These systems quickly detect faults, enabling prompt identification and isolation of problems, reducing downtime, and minimizing service interruptions. This ensures a more consistent power supply for densely populated areas, where the consequences of power outages are more disruptive. As cities grow and requirement for electricity increases, utilities are adopting advanced fault detection solutions to enhance operational efficiency, improve customer satisfaction, and reduce maintenance costs, making these indicators an essential component of modern power infrastructure. Thus, the aforementioned factors are fueling the fault circuit indicator market growth.

Key Restraints:

Interference and Environmental Factors Hampers the Market Development

Interference and environmental factors pose a significant restraint to the effectiveness of fault circuit indicators. These systems rely on accurate detection of faults in power lines, but their performance are compromised by external interference, such as electromagnetic noise or signal congestion in densely populated areas. Environmental conditions, such as extreme weather, temperature fluctuations, and humidity, also affect the sensitivity and reliability of the indicators. For instance, storms, heavy rain, or snow causes physical damage to the power infrastructure, leading to false readings or missed fault detection. Additionally, harsh environmental conditions like extreme heat or cold degrade the components of fault circuit indicators, reducing their lifespan and accuracy. Such factors make it challenging to maintain optimal performance and increase maintenance requirements, which impacts the overall efficiency of power distribution systems and hinder the fault circuit indicator market demand.

Future Opportunities :

Expansion of Smart Grid and IoT Integration Opens New Doors

The transition to smart grids and the growing integration of the Internet of Things (IoT) in energy management present a significant opportunity for fault circuit indicators. Smart grids, which rely on advanced communication and control systems, benefit from the real-time data provided by IoT-enabled devices, including fault circuit indicators. These devices instantly detect and report faults, allowing for faster response times and more accurate fault localization. Predictive maintenance capabilities, supported by IoT data analytics, further enhance the efficiency of power distribution systems by identifying potential issues before they cause disruptions. The seamless communication between devices within smart grids enables improved coordination, optimized grid performance, and reduced downtime. This integration helps utilities proactively address system failures, maintain grid stability, and reduce operational costs, making these indicators essential components in the development of more efficient, resilient, and intelligent power networks. Therefore, the above mentioned factors are boosting the fault circuit indicator market opportunities.

Fault Circuit Indicator Market Segmental Analysis :

By Type:

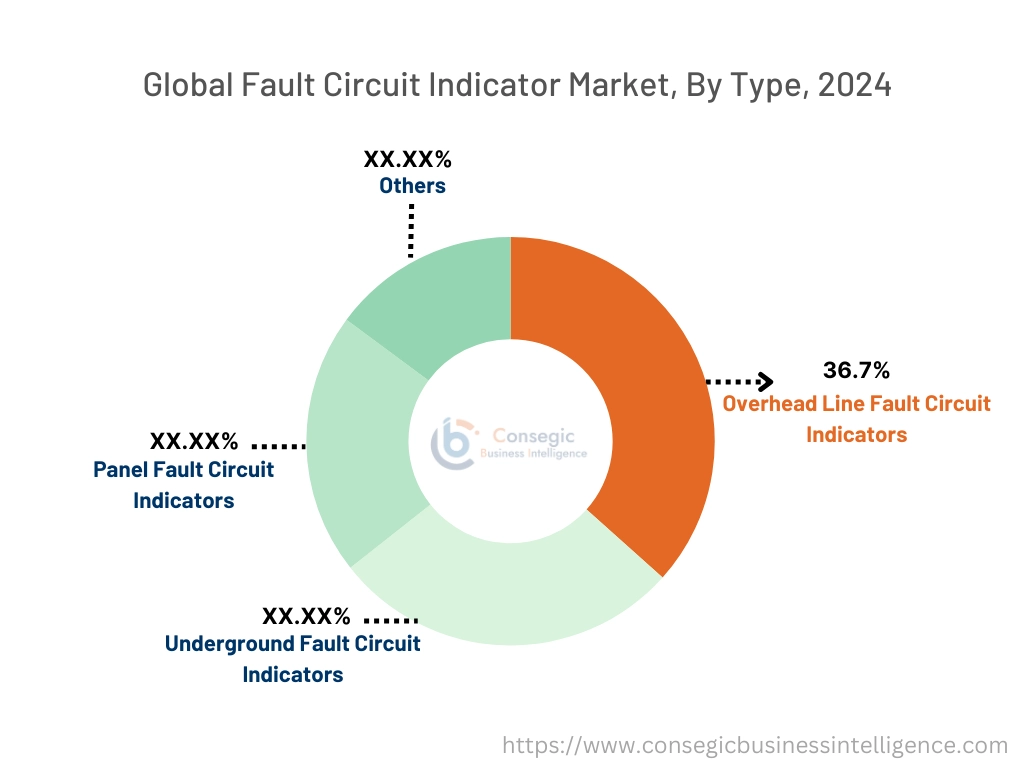

Based on type, the market is segmented into overhead line fault circuit indicators, underground fault circuit indicators, panel fault circuit indicators, and others.

The overhead line fault circuit indicators segment accounted for the largest revenue of 36.7% of the total fault circuit indicator market share in 2024.

- This dominance is attributed to their widespread use in power distribution networks to detect and isolate faults promptly.

- Increasing investments in upgrading power infrastructure in developing economies have driven requirement for overhead line fault indicators.

- Their reliability in extreme weather conditions makes them a preferred choice for utilities, ensuring minimal service disruption.

- The segment's progress is further supported by advancements in real-time fault monitoring technologies, contributing to the fault circuit indicator market expansion.

The underground fault circuit indicators segment is projected to grow at the fastest CAGR during the forecast period.

- Rising urbanization has led to the enlargement of underground electrical networks, boosting the need for efficient fault detection systems.

- Underground fault indicators offer high accuracy in pinpointing fault locations, reducing downtime.

- Their deployment is increasing in densely populated areas where overhead lines are impractical.

- As per the fault circuit indicator market analysis, growing investments in smart grid infrastructure are further accelerating the adoption of underground fault indicators.

By Voltage Range:

Based on voltage range, the market is segmented into low voltage (up to 1kV), medium voltage (1kV - 69kV), and high voltage (above 69kV).

The medium voltage segment held the largest revenue of the total fault circuit indicator market share in 2024.

- This is due to the extensive deployment of medium voltage grids in industrial and commercial sectors.

- Increased investments in renewable energy integration into medium voltage grids have driven segment growth.

- Medium voltage systems are critical for power distribution, supporting the segment’s dominance.

- As per the fault circuit indicator market trends, utilities are increasingly adopting medium voltage fault indicators to enhance grid reliability.

The high voltage segment is expected to grow at the fastest CAGR during the forecast period.

- Growing energy demand and the extension of long-distance power transmission networks are driving segment progress.

- High voltage fault indicators are essential for managing grid stability and preventing large-scale outages.

- Ongoing grid modernization projects are accelerating the adoption of high voltage fault detection solutions.

- The rise in renewable energy generation requires efficient high-voltage transmission, boosting this segment, further fueling the fault circuit indicator market growth.

By Connectivity:

Based on connectivity, the market is bifurcated into wired and wireless.

The wired segment accounted for the largest revenue share in 2024.

- Wired fault circuit indicators are widely used due to their reliability and cost-effectiveness in established grid systems.

- They offer consistent performance with minimal maintenance requirements.

- Wired systems are preferred in critical infrastructure for their high data security and stability.

- Therefore, as per the market trends, the segment benefits from ongoing upgrades in conventional power grids.

The wireless segment is projected to grow at the fastest CAGR during the forecast period.

- Increasing adoption of IoT and smart grid technologies is driving need for wireless fault indicators.

- Wireless systems offer real-time fault detection and remote monitoring capabilities.

- Their flexible installation and scalability make them ideal for remote and hard-to-access areas.

- As per the fault circuit indicator market analysis, utilities are embracing wireless solutions to improve operational efficiency and reduce outage times.

By End-User Industry:

Based on end-user industry, the market is segmented into utilities, manufacturing, transportation, and others.

The utilities segment accounted for the largest revenue share in 2024.

- Rising global electricity consumption and the need for uninterrupted power supply are fueling demand for fault detection solutions.

- Utilities are investing in advanced fault indicators to enhance grid resilience and reliability.

- Regulatory mandates for grid modernization are driving the adoption of fault detection systems in utilities.

- As per the fault circuit indicator market trends, the integration of renewable energy sources into utility grids has increased the need for real-time fault monitoring.

The manufacturing segment is anticipated to grow at the fastest CAGR during the forecast period.

- The increasing focus on operational efficiency and safety in manufacturing facilities is driving demand.

- Fault indicators help prevent downtime by enabling early fault detection and maintenance.

- Automation and smart manufacturing trends are boosting the adoption of fault monitoring solutions.

- Thus, energy-intensive industries are prioritizing grid stability, supporting segment progress, which contributes to the fault circuit indicator market expansion.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

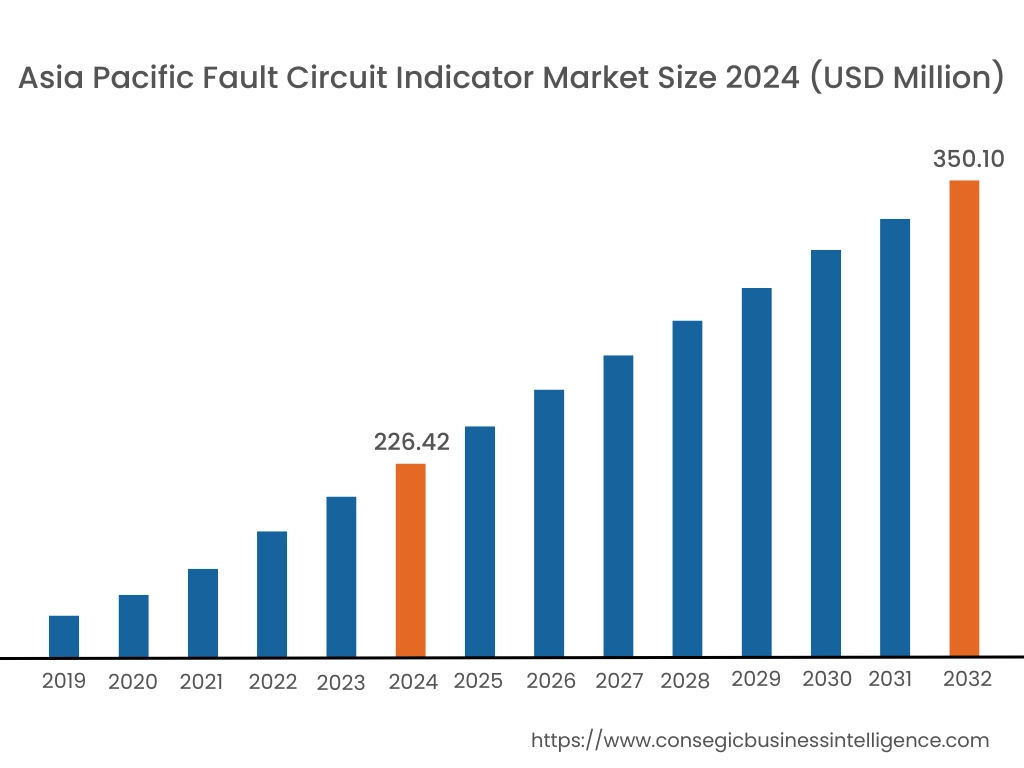

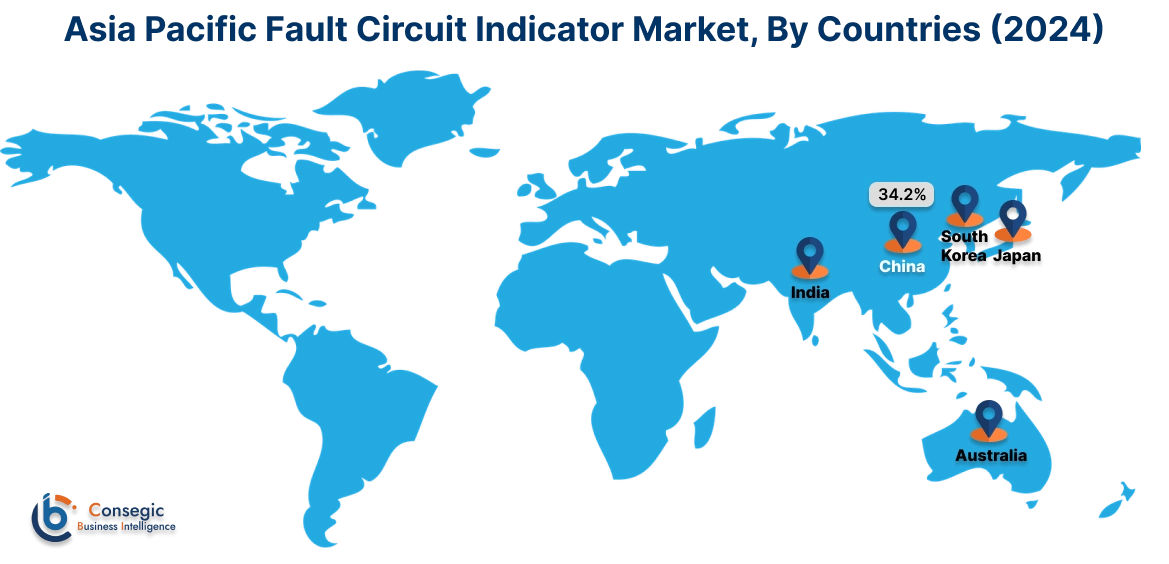

Asia Pacific region was valued at USD 226.42 Million in 2024. Moreover, it is projected to grow by USD 234.73 Million in 2025 and reach over USD 350.10 Million by 2032. Out of this, China accounted for the maximum revenue share of 34.2%. The Asia-Pacific region leads the FCI market in terms of value, attributed to rapid industrialization and urbanization. A prominent trend is the deployment of FCIs in expanding electrical grids to ensure reliable power distribution. Analysis indicates that countries like China and India are investing in modern faulted circuit indicators to meet the increasing need for electricity and to support the extension and reinforcement of grid infrastructure.

North America is estimated to reach over USD 372.64 Million by 2032 from a value of USD 255.02 Million in 2024 and is projected to grow by USD 263.14 Million in 2025. This region holds a substantial share of the FCI market, driven by the modernization of aging electrical infrastructure and the integration of smart grid technologies. A notable trend is the adoption of advanced sensor technologies that provide real-time data, enhancing the ability to detect faults swiftly and accurately. Analysis indicates that investments in smart grid initiatives are acting as vital growth drivers, improving fault detection and response times, and contributing to overall operational efficiency.

European countries are key players in the FCI market, with a strong emphasis on enhancing the reliability of power distribution systems. A significant trend is the increasing adoption of digital fault circuit indicators that offer enhanced accuracy and improved data logging. Analysis suggests that the shift towards more advanced fault detection technologies and rising investments in automation across various sectors are propelling the fault circuit indicator market opportunities in this region.

In the Middle East and Africa, the FCI market is expected to witness strong growth, driven by the development of off-grid power systems and the need for reliable electrical distribution in remote areas. The focus is on implementing FCIs to enhance the reliability of power distribution and to support the integration of renewable energy sources. Analysis suggests that the push for modernization of grid infrastructure presents significant growth opportunities within the FCI market in these regions.

Latin American countries are increasingly recognizing the importance of FCIs in improving grid stability and reducing downtime. A notable trend is the adoption of IoT-based platforms to develop smart grids, facilitating advanced monitoring and management of electrical systems. Analysis indicates that modernization of aging electrical infrastructure and grid expansion are driving the fault circuit indicator market demand in this region.

Top Key Players and Market Share Insights:

The Fault Circuit Indicator market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Fault Circuit Indicator market. Key players in the Fault Circuit Indicator industry include -

- Schweitzer Engineering Laboratories (SEL) (USA)

- Eaton Corporation (Ireland)

- Chaobo Automation Technology Co., Ltd. (China)

- Four-Faith Smart Power Technology Co., Ltd. (China)

- Sentient Energy, Inc. (USA)

- ABB Ltd. (Switzerland)

- Smart Grid Solutions (USA)

- Horstmann GmbH (Germany)

- Littelfuse, Inc. (USA)

Recent Industry Developments :

- In October 2024, ATRIY introduced the Lodestar PT2, a short-circuit and earth fault indicator designed for 6-35 kV power distribution lines. Suitable for networks with insulated, grounded, or resistance-grounded neutrals, this device enhances fault localization in overhead and cable lines. The Lodestar PT2 is compact and can be installed on switchgear control panels or wall-mounted, ensuring efficient operation and monitoring.

Fault Circuit Indicator Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 1,149.76 Million |

| CAGR (2025-2032) | 5.2% |

| By Type |

|

| By Voltage Range |

|

| By Connectivity |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Fault Circuit Indicator Market? +

The Fault Circuit Indicator Market size is estimated to reach over USD 1,149.76 Million by 2032 from a value of USD 768.82 Million in 2024 and is projected to grow by USD 794.79 Million in 2025, growing at a CAGR of 5.2% from 2025 to 2032.

What are the key segments in the Fault Circuit Indicator Market? +

The market is segmented by type (overhead line fault circuit indicators, underground fault circuit indicators, panel fault circuit indicators, others), voltage range (low voltage, medium voltage, high voltage), connectivity (wired, wireless), and end-user industry (utilities, manufacturing, transportation, others).

Which segment is expected to grow the fastest in the Fault Circuit Indicator Market? +

The underground fault circuit indicators segment is projected to grow at the fastest CAGR during the forecast period, driven by the increasing urbanization and demand for efficient fault detection in underground electrical networks.

Who are the major players in the Fault Circuit Indicator Market? +

Key players in the Fault Circuit Indicator market include Schweitzer Engineering Laboratories (USA), Eaton Corporation (Ireland), ABB Ltd. (Switzerland), Smart Grid Solutions (USA), Horstmann GmbH (Germany), Littelfuse, Inc. (USA), Chaobo Automation Technology Co., Ltd. (China), Four-Faith Smart Power Technology Co., Ltd. (China), Sentient Energy, Inc. (USA).