- Summary

- Table Of Content

- Methodology

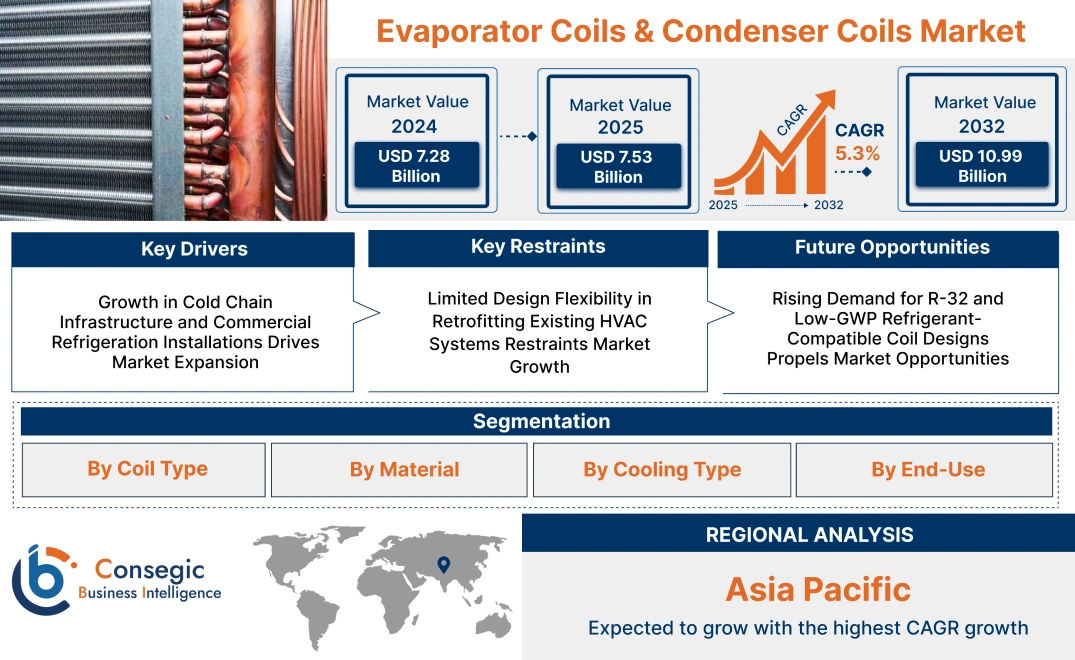

Evaporator Coils & Condenser Coils Market Size:

Evaporator Coils & Condenser Coils Market size is estimated to reach over USD 10.99 Billion by 2032 from a value of USD 7.28 Billion in 2024 and is projected to grow by USD 7.53 Billion in 2025, growing at a CAGR of 5.3% from 2025 to 2032.

Evaporator Coils & Condenser Coils Market Scope & Overview:

Evaporator coils & condenser coils are crucial components of the heat exchange systems employed in air conditioning, refrigeration, and industrial cooling processes. The coils allow thermal energy transfer, with evaporator coils picking up heat from the surroundings and condenser coils discharging it, regulating desired temperature levels in different systems.

Made of materials such as copper or aluminum, they are designed for maximum conductivity, corrosion resistance, and longevity. Design configurations—such as finned, microchannel, or tube-and-shell designs—facilitate efficient airflow, fast heat exchange, and compact integration into HVAC or refrigeration equipment.

Their major benefits are enhanced energy efficiency, uniform thermal control, and minimal maintenance needs. Their versatility in residential, commercial, and industrial applications guarantees broad usage in climate control and cold chain solutions. Through the provision of reliable performance under different environmental conditions, evaporator coils & condenser coils ensure long-term system reliability and increased equipment longevity.

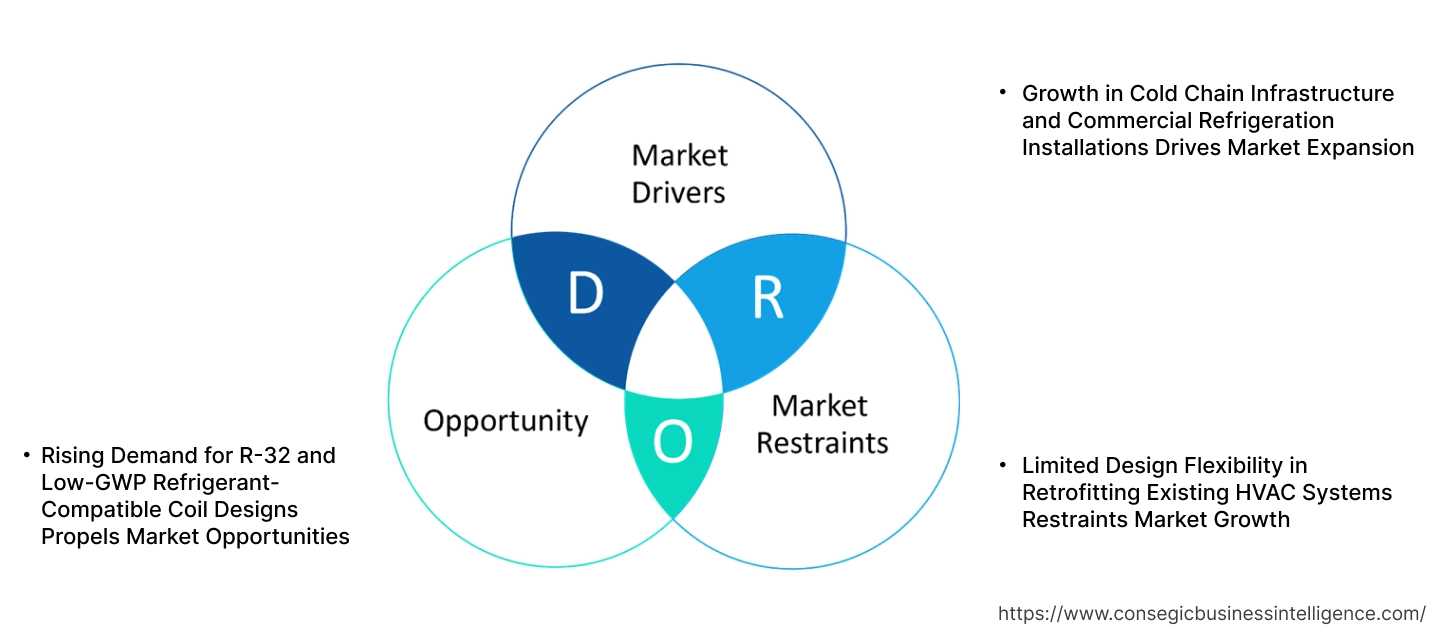

Evaporator Coils & Condenser Coils Market Dynamics - (DRO):

Key Drivers:

Growth in Cold Chain Infrastructure and Commercial Refrigeration Installations Drives Market Expansion

Mass development of cold chain logistics and refrigerated storage capacity is sharply fueling demand for high-performance thermal exchange components. Evaporator coils & condenser coils are necessary to maintain stable temperatures within walk-in freezers, refrigerated display cabinets, cold storage warehouses, and transport refrigeration units. Increased consumption of perishable items, growth in organized retailing, and vaccine supply chains are encouraging system designers to emphasize energy efficiency and rugged coil designs. These sub-components are designed for accurate thermal management, corrosion resistance, and extended operating cycles, such that performance under varying climate and load conditions is ensured. The food and pharmaceutical industries specifically need to have strong, low-maintenance refrigeration systems that ensure temperature compliance and product integrity. With increased investment in cold storage and refrigerated logistics becoming a trend across the world, need for maximized coil solutions is increasing—directly impacting evaporator coils & condenser coils market expansion.

Key Restraints:

Limited Design Flexibility in Retrofitting Existing HVAC Systems Restraints Market Growth

Replacement of evaporator and condenser coil assemblies in older HVAC systems poses immense challenges because coil sizes, refrigerant requirements, and airflow behaviors are not standardized across older equipment. Structural issues, irregular ductwork, and fixed housing sizes frequently require the use of unique coil configurations or full system rebuilding. Such complexities extend installation lead times and enhance project expense, especially in commercial facilities with full-time occupancy constraints. Apart from that, old infrastructure does not have spatial flexibility to host newer high-efficiency coils, whose geometry is typically different or who need extra clearance for proper functionality. Such retrofitting limitations reduce the potential of contractors to adopt efficient system upgrades without making a high amount of capital investment. Though demand for system modernization continues to be strong, these physical and design-related constraints still remain a limitation to mass adoption—ultimately holding back evaporator coils & condenser coils market growth.

Future Opportunities:

Rising Demand for R-32 and Low-GWP Refrigerant-Compatible Coil Designs Propels Market Opportunities

The move worldwide toward climate-friendly refrigerants under Kigali Amendment obligations and domestic F-gas phase-down plans is compelling coil component design innovation. Evaporator and condenser coils are being redesigned to support the thermodynamic and pressure characteristics of low-GWP refrigerants like R-32, R-290, and R-454B. Next-generation refrigerants require coil geometries that provide optimized heat exchange, chemical resistance, and high-pressure ratings without trading energy efficiency. Producers who supply refrigerant-ready coil packages are gaining competitive ground among OEMs and retrofit contractors looking ahead to future regulatory enforcement. This shift is most notable in Europe, Japan, and North America, where refrigerant policy systems are moving fast. Because HVAC equipment increasingly needs to be compatible with sustainable refrigerant alternatives, the need for flexible and future-proof coil solutions is on the increase.

- For instance, in April 2024, Johnson Controls launched a new suite of redesigned, innovative and environmentally friendly residential products optimized for use with the low-GWP refrigerant R-454B. This product line includes heat pumps, air conditioners, air handler units and indoor evaporator coils. The portfolio was redesigned with a new color scheme and enhanced features that provide increased efficiency, improved serviceability and installation to enhance ratings among customers incentivized by federal rebates and tax credits.

This transition for refrigerant is opening long-term evaporator coils & condenser coils market opportunities fueled by both compliance and development in green HVAC technologies.

Evaporator Coils & Condenser Coils Market Segmental Analysis :

By Coil Type:

Based on coil type, the market is segmented into evaporator coils and condenser coils.

The evaporator coils segment accounted for the largest revenue share in 2024.

- Evaporator coils are essential for absorbing heat from indoor air, making them critical in HVAC and refrigeration applications across residential, commercial, and industrial settings.

- Technological improvements, such as enhanced fin designs and microchannel coils, are contributing to improved energy efficiency and performance.

- The increasing installation of air conditioning systems in developing regions has significantly driven the evaporator coils market demand.

- According to the evaporator coils & condenser coils market analysis, evaporator coils dominate due to their widespread utility in both cooling and dehumidification processes.

The condenser coils segment is projected to register the fastest CAGR during the forecast period.

- Condenser coils play a vital role in dissipating heat and are widely adopted in outdoor condensing units of cooling systems.

- Trends indicate a rise in the necessity for high-efficiency coils in commercial refrigeration and industrial heat exchange systems.

- The shift toward low-GWP refrigerants and sustainable cooling has spurred innovation in condenser coil configurations and materials.

- For instance, in June 2023, Johnson Controls launched a new FRICK® Freezer Penthouse Evaporator-Retrofit (FPHE-R) model with design updates to improve ease of installation and service for contractors while maintaining product efficiency. One such feature is the removable cooling coil, accessible through a panel in the enclosure for easy maintenance.

- As per the evaporator coils & condenser coils market trends, the rising focus on green HVAC systems is accelerating adoption across various sectors.

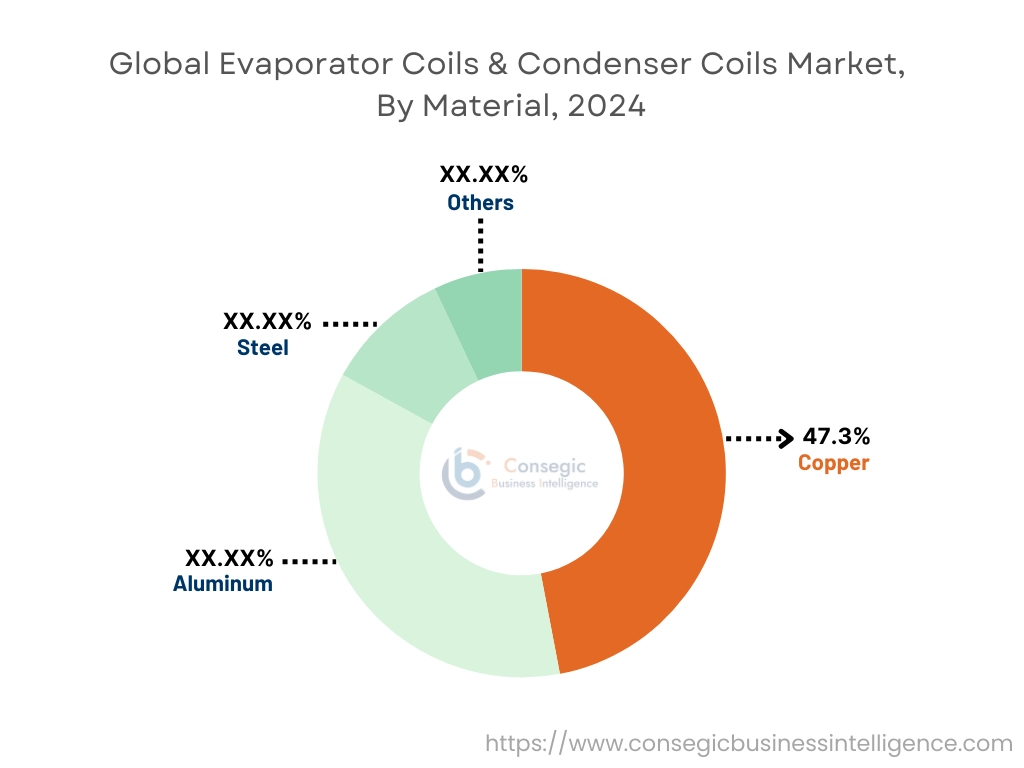

By Material:

Based on material, the market is segmented into copper, aluminum, steel, and others.

Copper held the dominant evaporator coils & condenser coils market share of 47.3% in 2024.

- Copper offers excellent thermal conductivity and corrosion resistance, making it ideal for HVAC and refrigeration coils.

- Due to its durability and ease of fabrication, copper continues to be the preferred material in both retrofits and new installations.

- The increasing replacement of older coils with high-performance copper units boosts segment growth.

- Copper's recyclability further supports sustainability goals, contributing to evaporator coils & condenser coils market trends.

The aluminum segment is anticipated to grow at the fastest CAGR.

- Aluminum coils are gaining traction due to their lightweight, cost-effectiveness, and increasing compatibility with advanced coil geometries.

- Aluminum's resistance to galvanic corrosion when coated has improved its viability in outdoor applications.

- As per trends, aluminum coils are increasingly used in compact systems such as residential split ACs and portable refrigeration units.

- The growing utilization of aluminum in HVAC components due to its attractive features supports the evaporator coils & condenser coils market demand.

By Cooling Type:

Based on cooling type, the market is divided into air-cooled, water-cooled, and evaporative-cooled systems.

The air-cooled segment dominated the market in 2024.

- Air-cooled systems are widely used across residential and light commercial environments due to their lower installation and maintenance costs.

- These coils require less infrastructure and are more suitable for applications without ready access to water sources.

- Trends in portable and ductless cooling units continue to favor air-cooled coil adoption.

- Their growing use in HVAC retrofitting projects is a significant factor fueling evaporator coils & condenser coils market demand.

The evaporative-cooled segment is projected to witness the fastest CAGR.

- These systems use water to pre-cool the air, enhancing energy efficiency in large-scale applications such as data centers and industrial cooling.

- Increasing regulatory pressure for energy conservation is driving the transition to evaporative technologies.

- Innovations in hybrid evaporative cooling systems further support this segment’s appeal.

- According to the evaporator coils & condenser coils market analysis, this category is seeing strong uptake in arid climates and high-load environments.

By End-Use:

Based on end-use, the market is segmented into residential, commercial (including data centers and cold storage), industrial (including automotive, food & beverage, pharmaceuticals, power generation), and others.

The commercial segment held the largest evaporator coils & condenser coils market share in 2024.

- The growing number of supermarkets, shopping malls, and data centers has increased the need for high-performance, reliable cooling solutions.

- The emphasis on maintaining temperature-sensitive environments in logistics and storage facilities drives this need.

- Commercial building retrofits focused on energy efficiency also boost this segment.

- These dynamics support strong evaporator coils & condenser coils market expansion in the commercial sector.

The industrial segment is anticipated to grow at the fastest CAGR.

- Manufacturing plants require robust cooling systems for process integrity, equipment protection, and compliance with environmental standards.

- Food and beverage, pharmaceuticals, and metal processing are witnessing high adoption of efficient coil systems.

- Industrial automation trends require precision cooling in production environments.

- The rising investments in industrial infrastructure globally are propelling the evaporator coils & condenser coils market growth.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

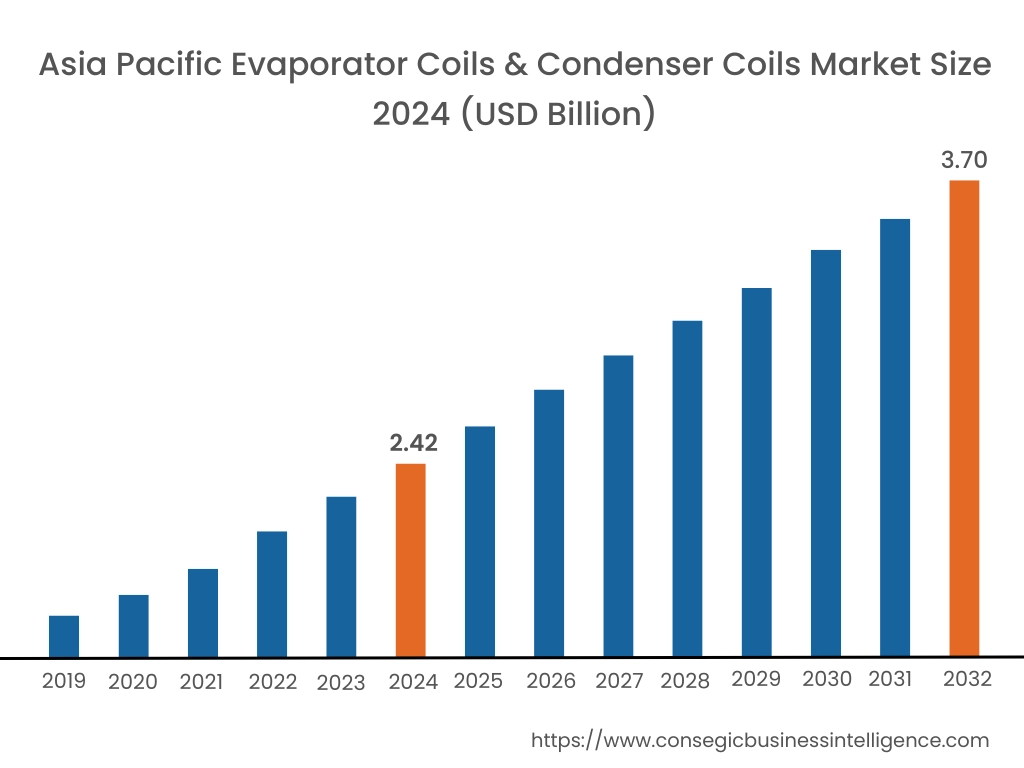

Asia Pacific region was valued at USD 2.42 Billion in 2024. Moreover, it is projected to grow by USD 2.51 Billion in 2025 and reach over USD 3.70 Billion by 2032. Out of this, China accounted for the maximum revenue share of 45.7%. Asia-Pacific is the region with the highest growth rate in the evaporator coils & condenser coils market, driven by urbanization, industrialization, and increasing requirement for cooling equipment. China, India, Japan, and Southeast Asia are experiencing the rapid growth in residential and commercial air conditioning system installations and cold chain infrastructure building. Market insights point out that OEMs and developers in these regions are placing a focus on cost-effectiveness, energy saving, and longevity—resulting in a higher demand for aluminum and coated copper coils. Mass development of high-rise buildings and smart cities also fosters integration of modular coil systems with high levels of control capabilities, offering a major evaporator coils & condenser coils market opportunity.

North America is estimated to reach over USD 3.24 Billion by 2032 from a value of USD 2.14 Billion in 2024 and is projected to grow by USD 2.21 Billion in 2025. North America holds a strong market position based on extensive HVACR installations in residential, commercial, and industrial applications. The U.S. and Canada persistently spend on high-performance air conditioning and refrigeration equipment, where coil technology plays the pivotal role. Market reports show increased focus on eco-friendly refrigerants and corrosion-free coil materials, particularly on the coastlines and in high-humidity areas. Furthermore, public incentives for retrofitting old HVAC equipment are fueling the upgrade to new coil designs with higher thermal transfer capabilities and lower energy usage. Aftermarket services as well as repeated product innovation in the region also contribute to favorable conditions.

Europe represents a regulation-driven market where sustainability targets and building decarbonization policies directly influence demand. Countries such as Germany, France, Italy, and the UK prioritize thermal efficiency, making advanced coil systems critical in retrofitting old structures and upgrading district cooling networks. Detailed analysis reveals that the region’s focus on low-emission heat pump adoption and the phasing out of older refrigerants is accelerating the need for optimized heat exchangers. Moreover, initiatives in green construction and eco-label certifications continue to promote the use of microchannel coils and compact units designed to reduce refrigerant volume and improve energy ratings.

Latin America is slowly increasing its market presence, most notably in Brazil, Mexico, and Argentina. With the rise in temperatures, electrification, and expansion of food and beverage processing industries, the need for effective thermal management systems is expanding. Analysis indicates that although cost-saving solutions dominate the market, regional distributors and producers are launching corrosion-resistant and energy-efficient coil models to satisfy shifting customer demands. Adoption is also being prompted by retail growth and the emergence of urban cooling infrastructure, albeit economic uncertainty and sparse policy incentives might represent short-term limitations.

The Middle East and Africa is a developing region with requirement primarily linked to commercial development, tourism infrastructure, and industrial operation in high-temperature environments. In the UAE, Saudi Arabia, and South Africa, evaporator and condenser coils form an essential component of HVAC equipment used in hotels, malls, and data centers. Market research points toward a demand for large-capacity, low-maintenance coil arrangements that can stand up to extreme ambient temperatures and dust exposure. At the same time, energy conservation efforts and regulatory changes toward high-efficiency apparatuses are starting to transform procurement norms. Yet adoption rates differ owing to lopsided infrastructure spending within the larger region.

Top Key Players & Market Share Insights:

The evaporator coils & condenser coils market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global evaporator coils & condenser coils market. Key players in the evaporator coils & condenser coils industry include -

- Johnson Controls (Ireland)

- Modine Manufacturing Company (USA)

- Winteco Industrial Co., Limited (China)

- Colmac Coil Manufacturing, Inc. (USA)

- Thermocoil (Pty) Ltd (South Africa)

- Bosch Thermotechnology (Germany)

- Coilmaster Corporation (USA)

- Goodman Manufacturing Company, L.P. (USA)

- Mortex Products, Inc. (USA)

- Shanghai Shenglin M&E Technology Co., Ltd (China)

Recent Industry Developments :

Acquisitions:

- In February 2024, Modine, a global leader in innovative thermal management and ventilation solutions, acquired Scott Springfield Manufacturing, a leading manufacturer of air handling units (AHUs). This decision enabled Modine to gain access to complementary product portfolio and a blue-chip customer base in several strategic end markets, including hyperscale and colocation data centers, telecommunications, healthcare and aerospace.

Evaporator Coils & Condenser Coils Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 10.99 Billion |

| CAGR (2025-2032) | 5.3% |

| By Coil Type |

|

| By Material |

|

| By Cooling Type |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Evaporator Coils & Condenser Coils Market? +

Evaporator Coils & Condenser Coils Market size is estimated to reach over USD 10.99 Billion by 2032 from a value of USD 7.28 Billion in 2024 and is projected to grow by USD 7.53 Billion in 2025, growing at a CAGR of 5.3% from 2025 to 2032.

What specific segmentation details are covered in the Evaporator Coils & Condenser Coils Market report? +

The Evaporator Coils & Condenser Coils market report includes specific segmentation details for coil type, material, cooling type and end-use.

What are the end-use of the Evaporator Coils & Condenser Coils Market? +

The end-use of the Evaporator Coils & Condenser Coils Market are residential, commercial, industrial and others.

Who are the major players in the Evaporator Coils & Condenser Coils Market? +

The key participants in the Evaporator Coils & Condenser Coils market are Johnson Controls (Ireland), Modine Manufacturing Company (USA), Bosch Thermotechnology (Germany), Coilmaster Corporation (USA), Goodman Manufacturing Company, L.P. (USA), Mortex Products, Inc. (USA), Shanghai Shenglin M&E Technology Co., Ltd (China), Winteco Industrial Co., Limited (China), Colmac Coil Manufacturing, Inc. (USA) and Thermocoil (Pty) Ltd (South Africa).