- Summary

- Table Of Content

- Methodology

Endovascular Aneurysm Repair Devices Market Size:

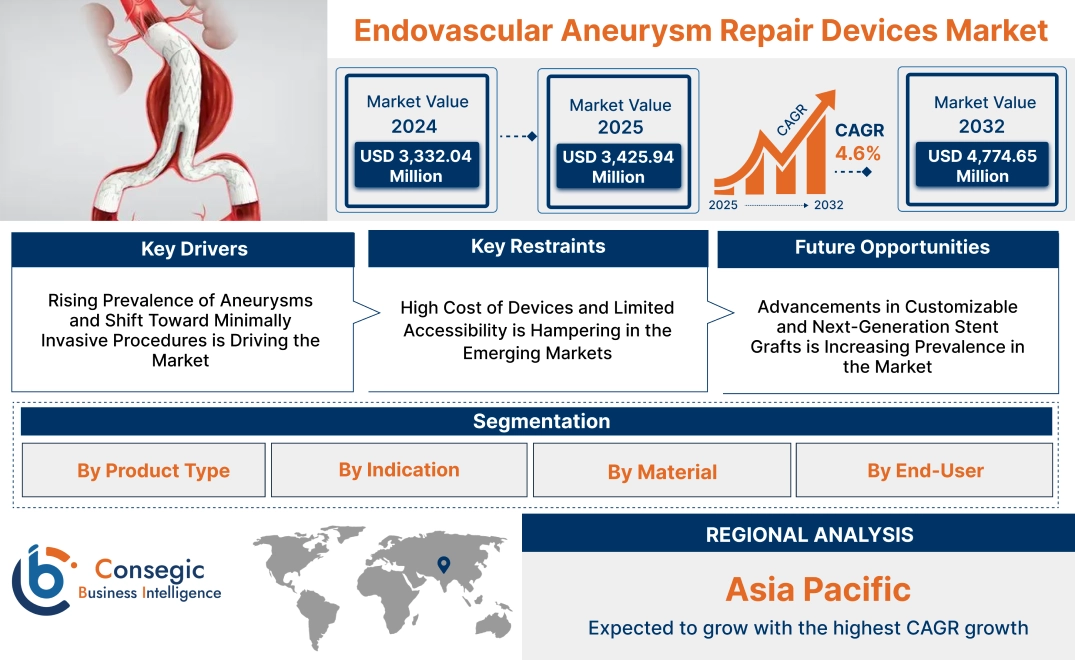

Endovascular Aneurysm Repair Devices Market size is estimated to reach over USD 4,774.65 Million by 2032 from a value of USD 3,332.04 Million in 2024 and is projected to grow by USD 3,425.94 Million in 2025, growing at a CAGR of 4.6% from 2025 to 2032.

Endovascular Aneurysm Repair Devices Market Scope & Overview:

The endovascular aneurysm repair (EVAR) devices are minimally invasive and medically designed devices to treat aortic aneurysms by reinforcing the weakened blood vessel wall. These devices, including stent grafts and delivery systems, are deployed within the affected artery to prevent rupture and reduce the risk of life-threatening complications. EVAR has become a preferred alternative to open surgical repair due to its reduced recovery time and lower procedural risks.

Key characteristics of EVAR devices include high precision in deployment, durability under high-pressure conditions, and compatibility with advanced imaging systems for real-time guidance. The benefits include improved patient outcomes, faster recovery, and reduced post-operative complications.

Applications span abdominal aortic aneurysm (AAA) repair and thoracic aortic aneurysm (TAA) repair in hospitals, ambulatory surgical centers, and specialized vascular clinics. End-users include vascular surgeons, interventional radiologists, and patients, driven by increasing prevalence of aortic aneurysms, demand in stent graft technologies, and the rising adoption of minimally invasive techniques globally.

Endovascular Aneurysm Repair Devices Market Dynamics - (DRO) :

Key Drivers:

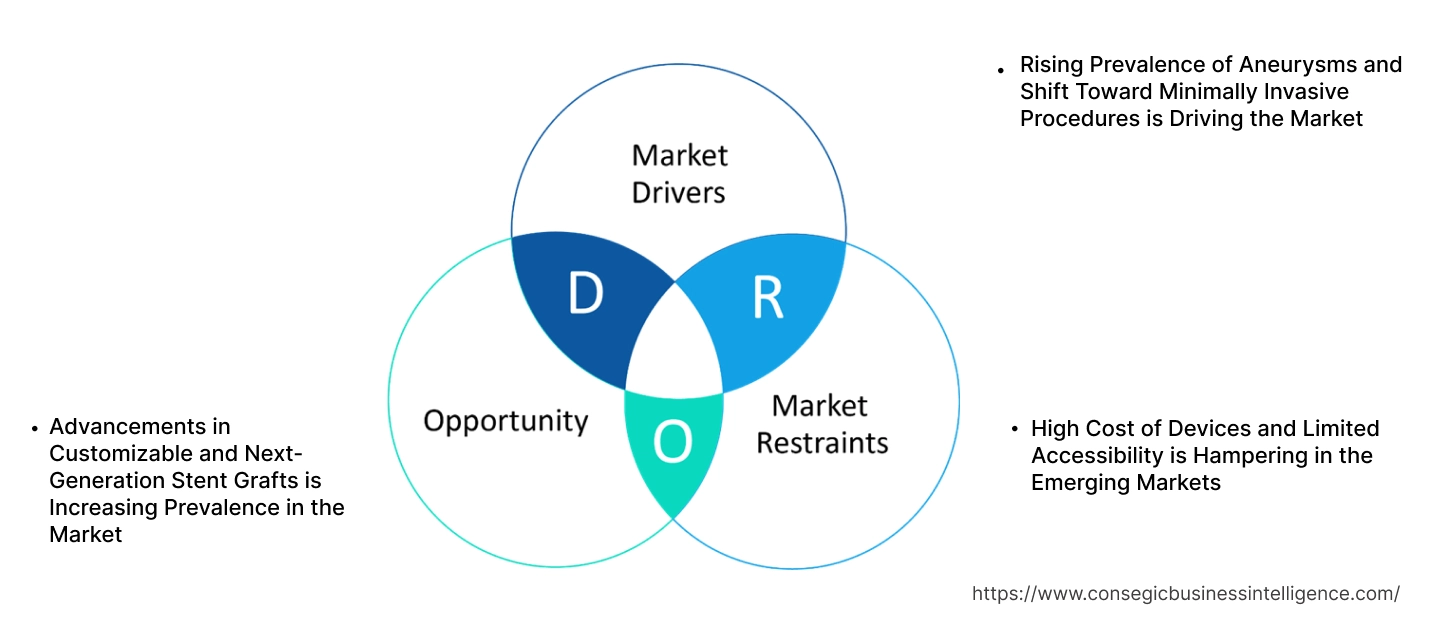

Rising Prevalence of Aneurysms and Shift Toward Minimally Invasive Procedures is Driving the Market

The growing prevalence of abdominal aortic aneurysms (AAA) and thoracic aortic aneurysms (TAA), driven by risk factors such as aging populations, hypertension, smoking, and genetic predispositions, is a significant driver for the EVAR devices market. Endovascular aneurysm repair (EVAR) has emerged as a preferred treatment option due to its minimally invasive nature, offering reduced perioperative morbidity, shorter hospital stays, and quicker recovery compared to traditional open surgical repair. The increasing awareness of early diagnosis of aneurysms, combined with advancements in imaging technologies such as CT and MRI for precise aneurysm detection, has further fueled the adoption of EVAR devices. Additionally, the growing acceptance of EVAR procedures in high-risk surgical patients has significantly expanded its application scope.

Key Restraints:

High Cost of Devices and Limited Accessibility is Hampering in the Emerging Markets

The high cost of EVAR devices and the infrastructure required for endovascular procedures remain significant restraints in the market. Advanced stent graft systems and imaging technologies used in EVAR are expensive, making these procedures less accessible in low- and middle-income regions where healthcare infrastructure is limited. Additionally, a shortage of trained vascular surgeons and endovascular specialists in these regions further restricts the widespread adoption of EVAR procedures. Reimbursement challenges and inconsistent healthcare policies in emerging markets also deter patients and healthcare providers from opting for EVAR, slowing market penetration in cost-sensitive areas.

Future Opportunities :

Advancements in Customizable and Next-Generation Stent Grafts is Increasing Prevalence in the Market

The development of customizable and next-generation stent grafts presents significant growth opportunities for the EVAR devices market. Innovations in stent graft technology, such as fenestrated and branched stent grafts, are enabling the treatment of complex aneurysms involving branches of the aorta. These devices offer greater flexibility, precision, and adaptability to patient-specific anatomies, expanding their application in cases where traditional EVAR was previously unsuitable. Additionally, the integration of biocompatible materials, improved sealing mechanisms, and low-profile delivery systems is enhancing the safety and efficacy of EVAR procedures. Emerging technologies such as 3D printing are being explored to create patient-specific stent grafts, further advancing personalized aneurysm repair solutions. Companies investing in R&D for next-generation devices are well-positioned to address the unmet needs of high-risk and anatomically complex patients.

These dynamics underscore the critical role of EVAR devices in advancing the treatment of aortic aneurysms. While challenges related to cost and accessibility remain, technological innovations and the rising adoption of minimally invasive procedures are driving significant growth for endovascular aneurysm repair devices market opportunities, enhancing patient outcomes and expanding the global market.

Endovascular Aneurysm Repair Devices Market Segmental Analysis :

By Product Type:

Based on product type, the market is segmented into stent grafts, catheters, guidewires, and sheaths.

The stent grafts segment accounted for the largest revenue in endovascular aneurysm repair devices market share in 2024.

- Stent grafts are the core component of endovascular aneurysm repair (EVAR) procedures, providing structural support and sealing aneurysmal sacs.

- Increasing prevalence of aortic aneurysms globally has driven demand for advanced stent graft solutions.

- Innovations in stent graft designs, such as fenestrated and branched stent grafts, enhance procedural outcomes.

- Rising adoption of minimally invasive procedures further bolsters the trends for stent grafts in EVAR treatments as per this segmental analysis.

The guidewires segment is anticipated to register the fastest CAGR during the forecast period.

- Guidewires play a crucial role in ensuring accurate device placement during EVAR procedures, reducing procedural risks.

- Technological advancements in flexible and high-torque guidewires improve navigation in complex anatomies.

- This segmental analysis displays, increasing preference for advanced guidewires with enhanced trackability and push ability supports trends.

- Expanding use of guidewires in hybrid and complex aortic aneurysm repairs drives segment growth.

By Indication:

Based on indication, the market is segmented into abdominal aortic aneurysm (AAA), thoracic aortic aneurysm (TAA), and thoracoabdominal aortic aneurysm.

The abdominal aortic aneurysm (AAA) segment accounted for the largest revenue share in 2024.

- AAA is the most commonly treated aortic aneurysm condition, contributing significantly to the demand for EVAR devices.

- Increasing awareness and adoption of screening programs for AAA among at-risk populations boost endovascular aneurysm repair devices market trends.

- Technological advancements are increasing endovascular aneurysm repair devices market demand in stent grafts specifically designed for AAA repair enhance procedural success rates.

- Rising prevalence of smoking, hypertension, and other risk factors associated with AAA supports segment trends analysis.

The thoracoabdominal aortic aneurysm segment is anticipated to register the fastest CAGR during the forecast period.

- Thoracoabdominal aneurysms are complex conditions requiring advanced and specialized EVAR devices for treatment.

- Rising adoption of hybrid surgical approaches combining open and endovascular techniques supports endovascular aneurysm repair devices market growth.

- Expanding availability of branched and fenestrated stent grafts designed for thoracoabdominal aneurysm repairs enhances procedural success.

- Increasing focus on early diagnosis and treatment of thoracoabdominal aneurysms drives demand for innovative EVAR solutions.

By Material:

Based on material, the market is segmented into polyester, polytetrafluoroethylene (PTFE), and others.

The polyester segment accounted for the largest revenue in endovascular aneurysm repair devices market share in 2024.

- Polyester is widely used in stent graft manufacturing due to its durability, biocompatibility, and resistance to thrombosis.

- Increasing adoption of polyester-based stent grafts in AAA and TAA repairs drives market trends.

- Advancements in polyester fabric technology enhance graft flexibility and reduce procedural complications.

- Widespread availability of polyester-based EVAR devices globally supports this segment’s dominance.

The PTFE segment is anticipated to register the fastest CAGR during the forecast period.

- PTFE offers excellent hemodynamic properties and reduced risk of infection, making it ideal for EVAR procedures.

- Growing preference for PTFE grafts in complex aneurysm repairs due to their adaptability and durability drives endovascular aneurysm repair devices market trends.

- Technological advancements in PTFE coatings and materials improve procedural success rates and patient outcomes.

- Increasing adoption of PTFE-based EVAR devices in emerging markets supports the segment’s expansion.

By End-User:

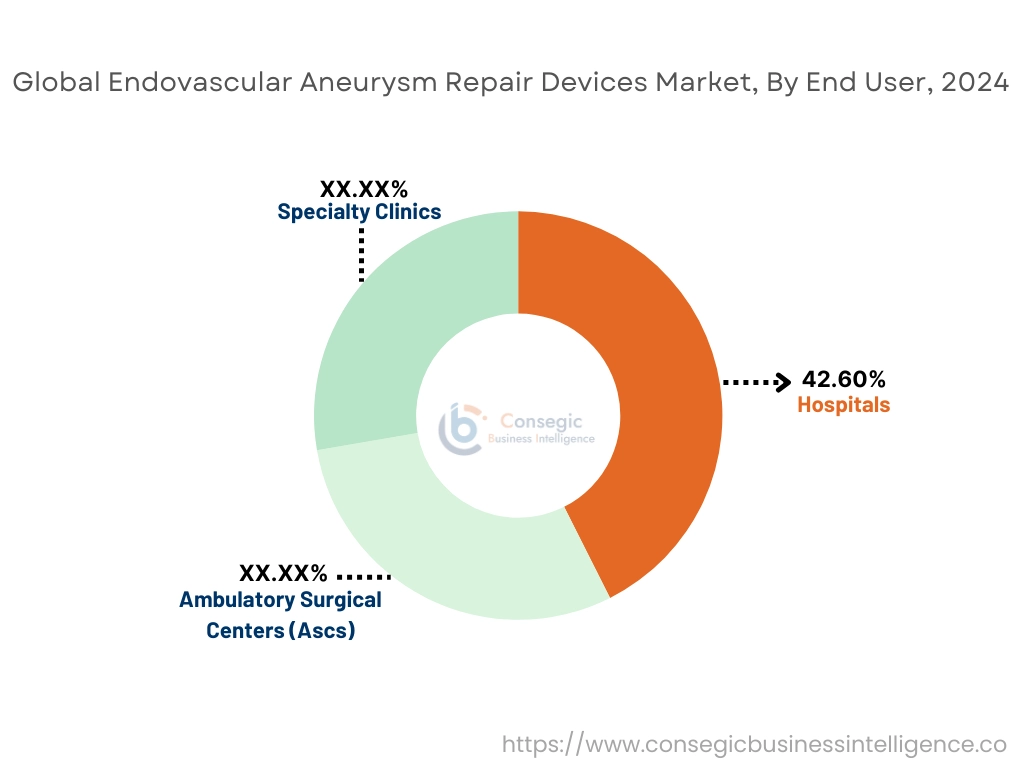

Based on end-user, the market is segmented into hospitals, ambulatory surgical centers (ASCs), and specialty clinics.

The hospitals segment accounted for the largest revenue share of 42.60% in 2024.

- Hospitals are the primary facilities for complex EVAR procedures, supported by advanced imaging and surgical infrastructure.

- Increasing hospital admissions for aortic aneurysm repairs due to improved screening and diagnostic capabilities support growing trends.

- Availability of skilled vascular surgeons and multidisciplinary care enhances patient outcomes in hospital settings.

- Rising government investments in hospital infrastructure, particularly in developing regions, bolster market trends.

The ambulatory surgical centers (ASCs) segment is anticipated to register the fastest CAGR during the forecast period.

- ASCs offer cost-effective and efficient solutions for minimally invasive EVAR procedures, driving patient preference.

- Increasing adoption of advanced imaging and surgical equipment in ASCs supports their growing role in aneurysm repairs.

- Reduced hospital stays and faster recovery times associated with procedures in ASCs enhance segment analysis.

- Expanding availability of specialized ASCs focused on vascular and endovascular surgeries fuels endovascular aneurysm repair devices market expansion.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

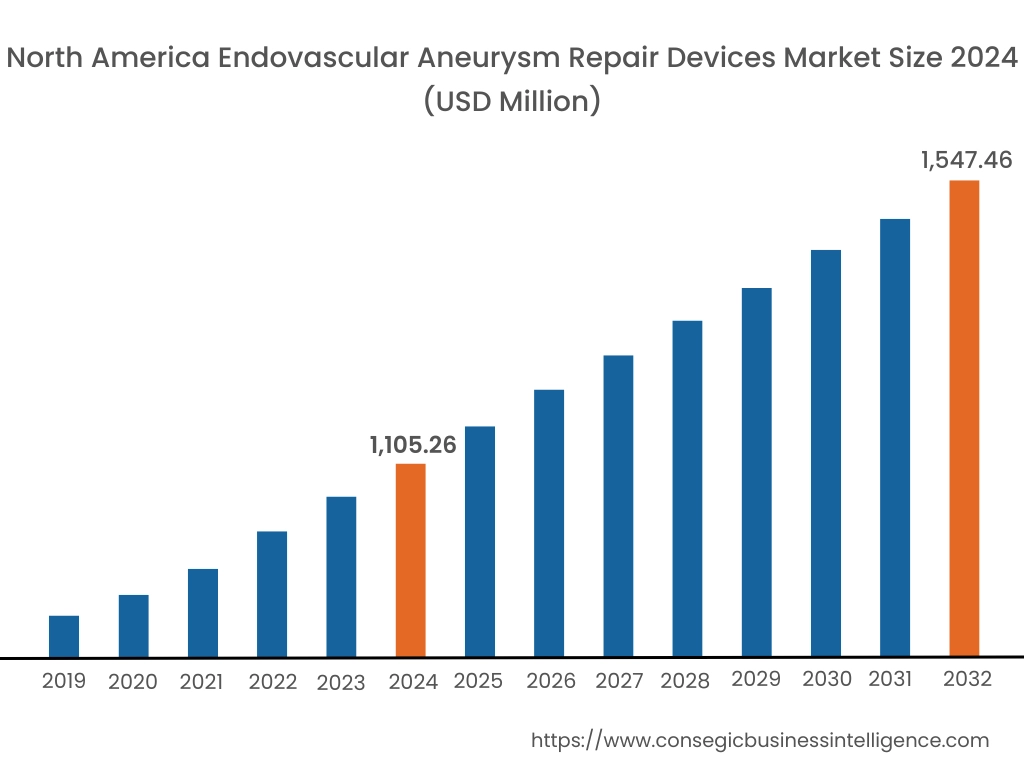

In 2024, North America was valued at USD 1,105.26 Million and is expected to reach USD 1,547.46 Million in 2032. In North America, the U.S. accounted for the highest share of 71.40% during the base year of 2024. North America holds a significant share in the global EVAR devices market, driven by the increasing prevalence of aortic aneurysms, advanced healthcare infrastructure, and widespread adoption of minimally invasive surgical procedures. The U.S. leads the region due to a growing aging population at high risk of aneurysms, significant investments in R&D for advanced EVAR technologies, and favorable reimbursement policies. Canada contributes through rising awareness about aneurysm screening and increasing access to EVAR procedures in public healthcare facilities. However, the high cost of EVAR devices and procedures may limit accessibility for some patients in underserved areas.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 5.0% over the forecast period. The EVAR devices market , is fueled by rising healthcare investments, improving healthcare infrastructure, and increasing awareness about vascular health in China, India, and Japan. China dominates the region with a growing number of aortic aneurysm cases and government-led initiatives to expand access to advanced surgical treatments. India’s expanding healthcare sector supports the adoption of cost-effective EVAR devices, particularly in urban areas with specialized vascular care centers. Japan emphasizes high-quality medical devices and precision vascular surgery techniques, leveraging its strong medical technology sector. However, limited access to specialized vascular surgeons in rural areas may hinder growth in certain parts of the region.

Europe is a prominent market, it is supported by a high prevalence of aortic aneurysms, increasing adoption of minimally invasive surgeries, and robust healthcare systems. Countries like Germany, the UK, and France are key contributors. Germany drives demand through its advanced vascular surgery centers and strong focus on clinical trials for new EVAR technologies. The UK emphasizes government-supported aneurysm screening programs, leading to earlier diagnosis and increased adoption of EVAR devices. As per the endovascular aneurysm repair devices market analysis, France focuses on expanding access to advanced surgical treatments in public healthcare facilities. However, differences in reimbursement policies across countries may impact uniform adoption of EVAR devices in the region.

The Middle East & Africa region is witnessing steady growth in the EVAR devices market, driven by increasing investments in healthcare modernization and rising prevalence of lifestyle-related risk factors such as hypertension and smoking. Countries like Saudi Arabia and the UAE are adopting advanced EVAR technologies to meet the growing demand for minimally invasive vascular treatments. As per the endovascular aneurysm repair devices market analysis of Africa, South Africa it is seen as a emerging key market, focusing on improving access to vascular care and advanced medical devices through public-private partnerships. However, limited healthcare infrastructure and a shortage of skilled professionals may restrict broader endovascular aneurysm repair devices market expansion in certain areas.

Latin America is an emerging market for EVAR devices, with Brazil and Mexico leading the region. Brazil’s growing healthcare sector and increasing prevalence of aortic aneurysms among its aging population drive endovascular aneurysm repair devices market demand for minimally invasive vascular treatments. Mexico focuses on improving access to advanced surgical devices through government healthcare programs and collaborations with global medical device manufacturers. The region benefits from rising awareness about aneurysm screening and the advantages of EVAR procedures over open surgery. However, economic instability and inconsistent healthcare infrastructure in smaller economies may pose challenges to endovascular aneurysm repair devices market growth.

Top Key Players & Market Share Insights:

The endovascular aneurysm repair devices market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global endovascular aneurysm repair devices market. Key players in the endovascular aneurysm repair devices industry include -

- Medtronic plc (Ireland)

- Cook Medical (United States)

- MicroPort Scientific Corporation (China)

- Lombard Medical Technologies Inc. (United Kingdom)

- Abbott Laboratories (United States)

- L. Gore & Associates, Inc. (United States)

- Terumo Corporation (Japan)

- Endologix LLC (United States)

- Cardinal Health, Inc. (United States)

- Becton, Dickinson and Company (United States)

Recent Industry Developments :

Innovations:

- In August 2024, Terumo India, a subsidiary of Terumo Corporation, announced the launch of the TREO Abdominal Stent-Graft System, an advanced solution for Endovascular Aneurysm Repair (EVAR). Designed for the treatment of infrarenal abdominal aortic aneurysms, the TREO system is notable for featuring both suprarenal and infrarenal active fixation, enhancing stability and reducing migration risks. Its three-piece design allows for in situ limb adjustability, accommodating a wide range of aortic anatomies and improving patient outcomes.

- In May 2024, Endologix LLC released the "AFX2 Endovascular AAA System Annual Clinical Update – 2023," providing comprehensive data on the performance of the AFX2 System for abdominal aortic aneurysm repair. The update includes final results from the LEOPARD Trial, a multicenter, prospective, randomized study comparing the AFX2 System to other commercially available endografts. Findings indicate that the AFX2 System demonstrates comparable freedom from aneurysm-related complications over a five-year follow-up period. This evidence supports the AFX2 System as a reliable option in the endovascular aneurysm repair devices market.

Endovascular Aneurysm Repair Devices Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 4,774.65 Million |

| CAGR (2025-2032) | 4.6% |

| By Product Type |

|

| By Indication |

|

| By Material |

|

| By End Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the estimated market size by 2032? +

Endovascular Aneurysm Repair Devices Market size is estimated to reach over USD 4,774.65 Million by 2032 from a value of USD 3,332.04 Million in 2024 and is projected to grow by USD 3,425.94 Million in 2025, growing at a CAGR of 4.6% from 2025 to 2032.

Which segment holds the largest market share? +

Stent grafts lead the market due to their essential role in EVAR procedures.

Which region is the fastest-growing? +

Asia Pacific is expected to grow the fastest due to rising healthcare investments and increasing prevalence of aortic aneurysms.

Who are the key market players? +

Leading players include Medtronic plc, Cook Medical, W. L. Gore & Associates, and Terumo Corporation, among others.