- Summary

- Table Of Content

- Methodology

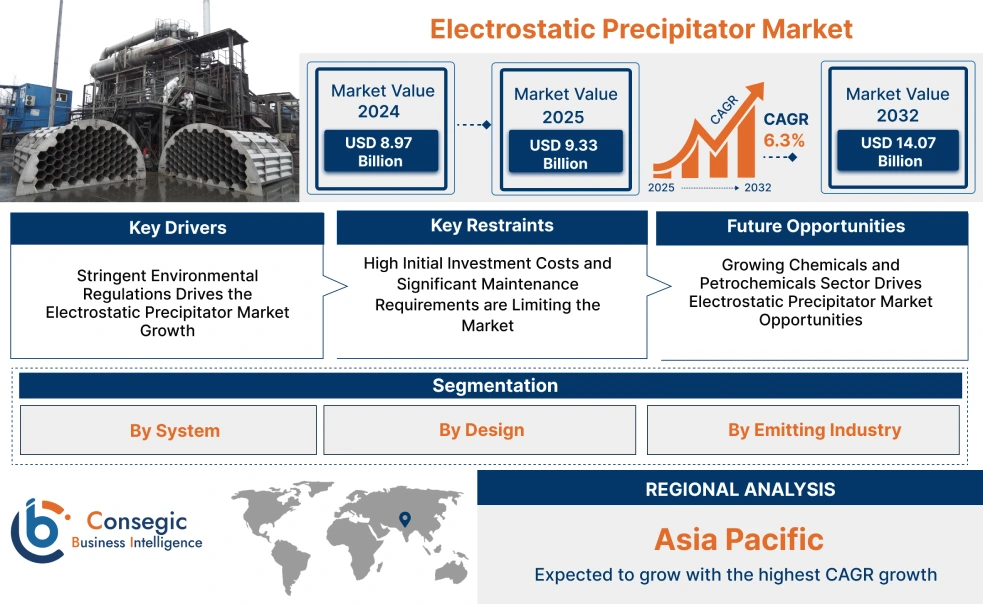

Electrostatic Precipitator Market Size:

Electrostatic Precipitator Market is estimated to reach over USD 14.07 Billion by 2032 from a value of USD 8.97 Billion in 2024 and is projected to grow by USD 9.33 Billion in 2025, growing at a CAGR of 6.3% from 2025 to 2032.

Electrostatic Precipitator Market Scope & Overview:

Electrostatic precipitators (ESPs) are air cleaning systems that utilize electrical fields to extract particulate pollutants from industrial emissions, essentially charging and capturing the particles on collection plates. A wide range of benefits including high particulate removal efficiency, adaptability to diverse industrial applications, and the ability to handle high-temperature gases are driving the market. Further, key trends including integration of digital monitoring and control systems, development of more energy-efficient designs, and increasing focus on retrofitting existing systems are driving the market.

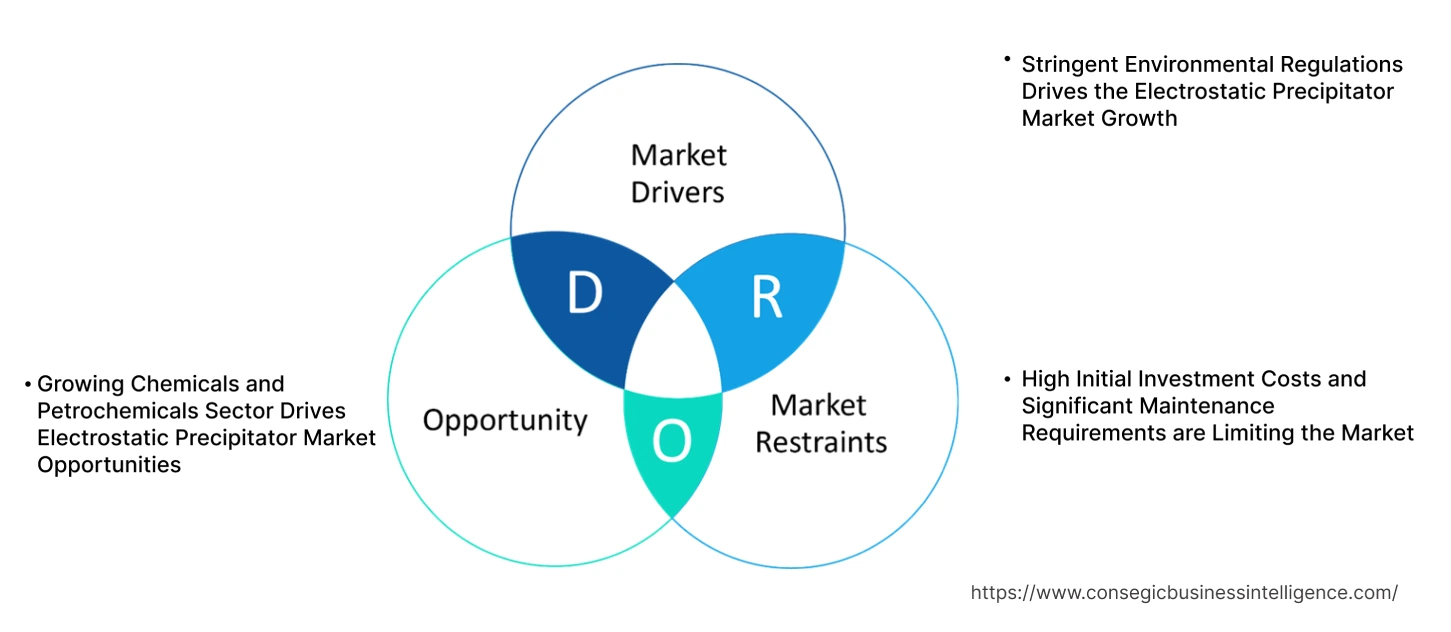

Electrostatic Precipitator Market Dynamics - (DRO) :

Key Drivers:

Stringent Environmental Regulations Drives the Electrostatic Precipitator Market Growth

Stringent environmental regulations are a primary catalyst for the Electrostatic Precipitator (ESP) market. Governments across the globe are enacting strict air pollution control measures to mitigate the adverse effects of industrial emissions on public health and the environment. These regulations mandate significant reductions in particulate matter, heavy metals, and other pollutants, compelling industries like power generation, cement, and metal processing to adopt efficient emission control technologies. Further ESPs, known for their high particle collection efficiency, become indispensable in achieving regulatory compliance. Consequently, industries are investing in new precipitator installations and upgrading existing systems to meet these stringent standards.

- For instance, S. Clean Air Act is a federal law that empowers the Environmental Protection Agency (EPA) to regulate air emissions from various sources, aiming to protect public health and the environment. Essentially, it's the cornerstone of U.S. air pollution control, driving significant reductions in harmful emissions.

Thus, regulatory push along with rapid industrialization and urbanization contributes significantly to the electrostatic precipitator market size.

Key Restraints:

High Initial Investment Costs and Significant Maintenance Requirements are Limiting the Market

The electrostatic precipitator market faces limitations primarily due to the substantial upfront capital required for installation. This high initial investment poses a significant barrier, particularly for smaller industries or those with limited budgets. Furthermore, precipitator systems necessitate consistent and rigorous maintenance to ensure optimal performance and longevity. This includes regular cleaning, electrode inspection, and component replacements, leading to significant operational expenses. The ongoing maintenance demands, coupled with the need for specialized expertise, can strain resources. Thus, financial and operational burdens collectively hinder the widespread adoption of precipitator technology, restricting market growth.

Future Opportunities :

Growing Chemicals and Petrochemicals Sector Drives Electrostatic Precipitator Market Opportunities

The expanding chemical and petrochemicals sectors present a significant growth avenue for the market. The sector generates diverse and often challenging pollutants, including corrosive gases, sticky particulates, and hazardous air pollutants (HAPs), necessitating robust emission control solutions. Further, stringent environmental regulations targeting these emissions compel companies to invest in advanced technologies, especially wet precipitators, which are effective in handling such difficult pollutants. Furthermore, the sector's demand for customized solutions, tailored to specific process emissions, further fuels market growth. Moreover, the increasing focus on sustainable practices and reducing environmental impact within the chemical sector creates a consistent need for efficient precipitator systems. Thus, convergence of regulatory pressure and sector expansion drives substantial drives the electrostatic precipitator market opportunities

Electrostatic Precipitator Market Segmental Analysis :

By System:

Based on the system, the market is segmented into wet and dry.

Trends in the System:

- Wet systems are increasingly used to remove sticky, corrosive, and fine particulates which in turn is driving the electrostatic precipitator market trends.

- Wet systems are increasingly integrated with other air pollution control technologies, such as scrubbers and selective catalytic reduction systems which are expected to drive electrostatic precipitator market size.

Dry accounted for the largest revenue share in the year 2024 and is anticipated to register the fastest CAGR during the forecast period.

- Increasing focus on optimizing electrode designs to improve particle collection efficiency which is driving the electrostatic precipitator market share.

- Further, integration of sensors, data analytics, and automation systems for real-time monitoring and control.

- Furthermore, development of systems with lower power consumption to reduce operational costs and environmental impact which in turn drives the electrostatic precipitator market trends.

- For instance, ANDRITZ offers dry precipitators for various industrial applications to handle diverse fuels and achieving high removal rates.

- Thus, as per electrostatic precipitator market analysis, enhanced efficiency increased automation and digitalization, and focus on energy efficiency are driving the market.

By Design:

Based on the design, the market is segmented into plate and tubular.

Trends in the Design:

- Increasing focus on the development of more compact tubular precipitator designs to reduce footprint and facilitate installation in space-constrained environments which in turn drives the electrostatic precipitator market demand.

- The incorporation of sensors and data analytics to monitor plate performance, detect anomalies, and enable predictive maintenance.

Plate accounted for the largest revenue share in the market in 2024.

- Growing demand for improvements in plate designs to maximize particle collection efficiency is driving the electrostatic precipitator market demand.

- Further, stricter air pollution control regulations and need for higher collection efficiency are influencing the design trends which in tune drives the electrostatic precipitator industry.

- Furthermore, increasing adoption of modular plate designs to allow for easier installation, maintenance, and customization to specific industrial applications.

- Thus, as per electrostatic precipitator market analysis, optimization of plate geometry, modular design, and stringent regulations are driving the market.

Tubular is anticipated to register the fastest CAGR during the forecast period.

- Development of advanced materials with enhanced corrosion resistance and electrical conductivity for tubular electrodes is driving the electrostatic precipitator market share.

- Further, growing focus on optimizing the internal gas flow within tubular system to ensure uniform particle distribution and maximize collection efficiency which subsequently propels the electrostatic precipitator market expansion.

- Therefore, based on analysis, improved tubular electrode materials and optimized gas flow dynamics are anticipated to boost the growth of the market during the forecast period.

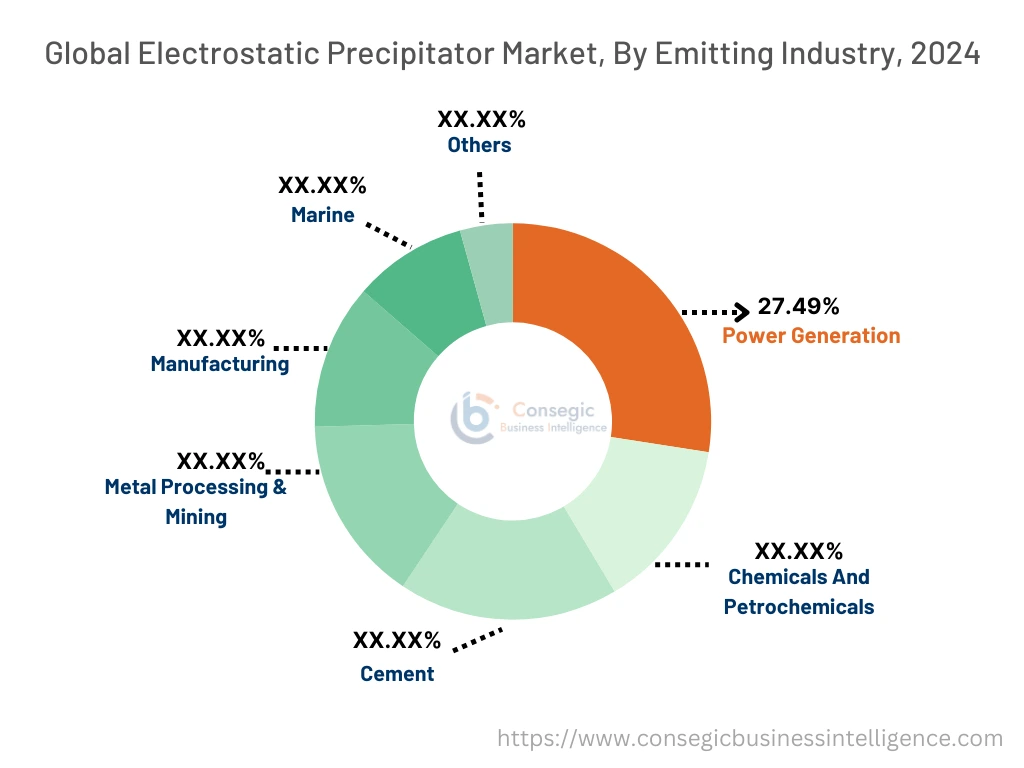

By Emitting Industry:

Based on the emitting industry, the market is segmented into power generation, chemicals and petrochemicals, cement, metal processing & mining, manufacturing, marine, and others.

Trends in the Emitting Industry:

- Increasing focus on developing solutions that can handle a wide range of particulate emissions from various manufacturing activities which in turn drive the market.

- Adhering to the International Maritime Organization's (IMO) regulations on air pollution from ships propels the market.

Power generation accounted for the largest revenue share of 27.49% in the year 2024.

- Increasing focus on capturing very small particles especially from coal-fired power plants to meet stricter PM2.5 regulations which is driving the market.

- Further, combining precipitators with Flue Gas Desulfurization (FGD) systems to achieve comprehensive air pollution control which in turn drives the market.

- Furthermore, implementing advanced monitoring and diagnostic systems to optimize the system performance and reduce downtime which in turn drives electrostatic precipitator market growth.

- For instance, MITSUBISHI HEAVY INDUSTRIES, LTD. offers ESPs as part of their Air Quality Control Systems (AQCS), capable of handling up to 1,050 MW and achieving very low dust emissions.

- Thus, based on analysis, emphasis on ultra-fine particle removal, integration with Flue Gas Desulfurization (FGD) systems, and digitalization is driving the market.

Metal processing & mining is anticipated to register the fastest CAGR during the forecast period.

- Growing focus on efficiently removing heavy metal particulates from flue gases to protect human health and the environment.

- Further, designing systems to withstand the harsh conditions of metal processing and mining operations subsequently propels the electrostatic precipitator market expansion.

- There is increased regulation of fugitive dust emissions from mining operations which in turn drives the market.

- Therefore, based on analysis, aforementioned factors are anticipated to drive the market growth.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

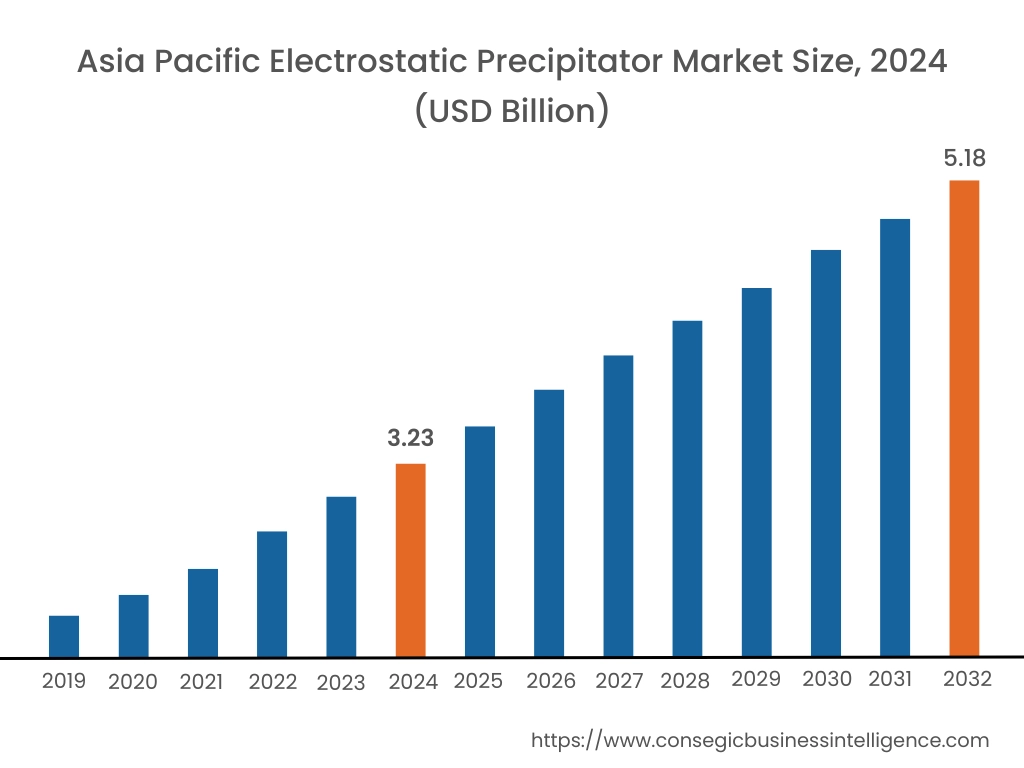

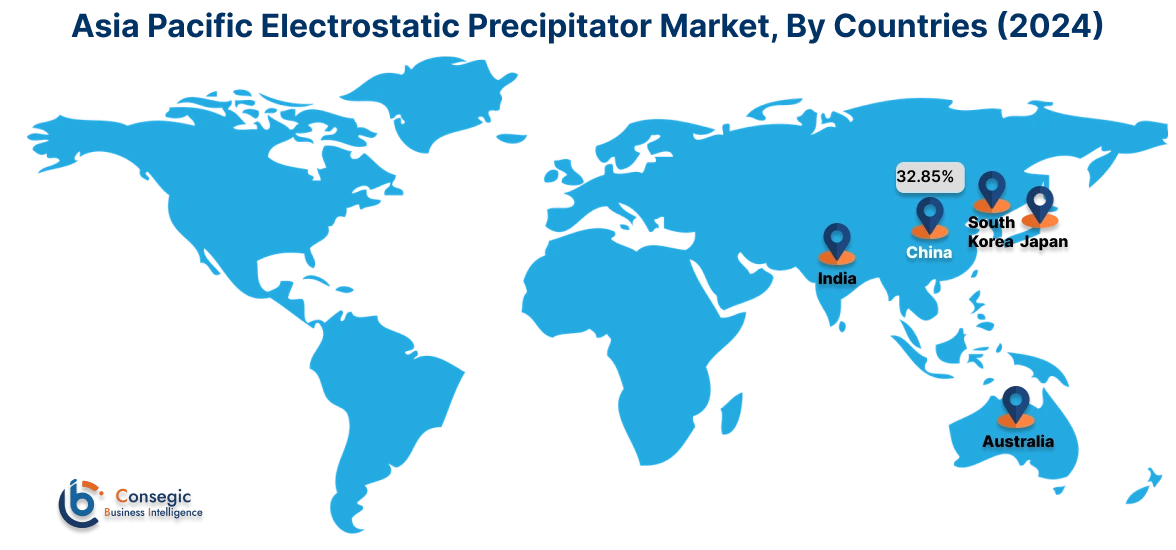

Asia Pacific region was valued at USD 3.23 Billion in 2024. Moreover, it is projected to grow by USD 3.37 Billion in 2025 and reach over USD 5.18 Billion by 2032. Out of this, China accounted for the maximum revenue share of 32.85%. The market growth is mainly driven by rapid industrialization and urbanization coupled with the increasing implementation of stricter air pollution control policies.

- For instance, in August 2021, Ecospray, a maritime emissions technology company launched a new WESP system designed to remove particulate matter and black smoke from ship exhaust. This technology, aimed at improving sustainable navigation, integrates with existing Exhaust Gas Cleaning Systems and is a step towards future carbon capture solutions.

North America is estimated to reach over USD 3.79 Billion by 2032 from a value of USD 2.42 Billion in 2024 and is projected to grow by USD 2.52 Billion in 2025. The North American market is primarily driven by enforcement of stringent environmental regulations, particularly those set by the EPA, coupled with the need to modernize aging industrial infrastructure.

- For instance, in May 2022, Valmet launched a new Wet Electrostatic Precipitator (WESP) for the marine sector, exceeding IMO 2020 regulations by effectively removing harmful particulate matter from ship exhaust.

The regional trends analysis depicts that growing environmental awareness, stringent emission reduction targets and the focus on sustainable industrial practices in Europe is driving the market. Additionally, the factors driving the market in the Middle East and African region are growing industrial sector, particularly in oil and gas and cement production, coupled with rising environmental awareness and government initiatives. Further, increasing industrial development is paving the way for the progress of market trends in Latin America region.

Top Key Players and Market Share Insights:

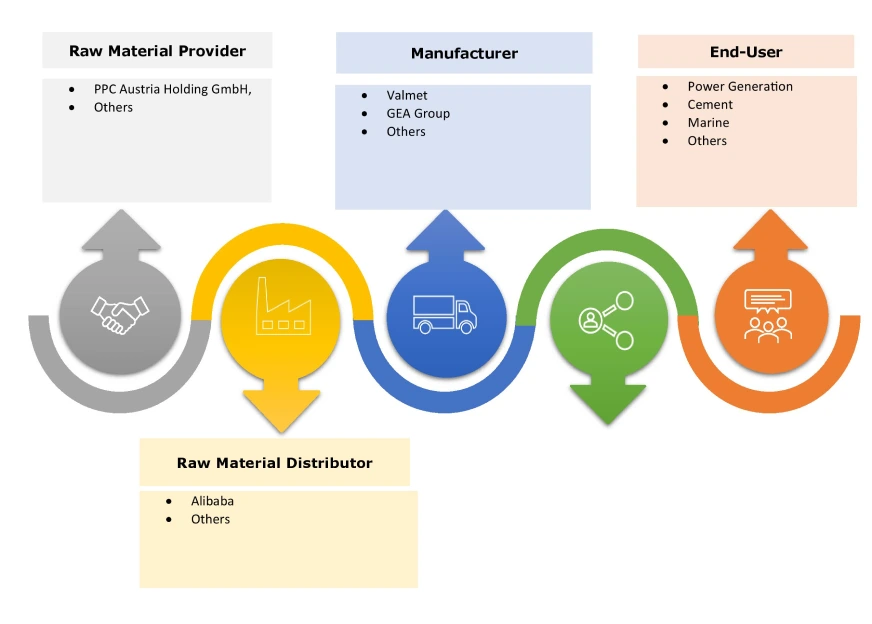

The global electrostatic precipitator market is highly competitive with major players providing solutions to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the electrostatic precipitator industry. Key players in the global electrostatic precipitator market include-

- Mitsubishi Heavy Industries Ltd. (Japan)

- Valmet (Finland)

- GEA Group (Germany)

- Babcock and Wilcox Enterprises (US)

- DUCON (US)

- DURR Group (Germany)

- FLSmidth (Denmark)

- Fuel Tech Inc. (US)

- Monroe Environmental (US)

- Sumitomo Heavy Industries (Japan)

Recent Industry Developments :

Collaboration and Partnership:

- In February 2024, Valmet supply electrostatic precipitators to Nordic Paper's Bäckhammar mill in Sweden, aiming to reduce dust emissions by over two-thirds. The order supports Nordic Paper's sustainability goals and is scheduled for completion by the end of 2025.

- In June 2024, Babcock & Wilcox (B&W), Babcock & Wilcox secured over USD 18 million in contracts to rebuild wet and dry electrostatic precipitators for particulate emissions control in U.S. and European utility and industrial facilities.

Electrostatic Precipitator Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 14.07 Billion |

| CAGR (2025-2032) | 6.3% |

| By System |

|

| By Design |

|

| By Emitting Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the electrostatic precipitator market? +

The electrostatic precipitator market is estimated to reach over USD 14.07 Billion by 2032 from a value of USD 8.97 Billion in 2024 and is projected to grow by USD 9.33 Billion in 2025, growing at a CAGR of 6.3% from 2025 to 2032.

What specific segmentation details are covered in the electrostatic precipitator report? +

The electrostatic precipitator report includes specific segmentation details for system, design, emitting industry, and region.

Which is the fastest segment anticipated to impact the market growth? +

In the electrostatic precipitator market, tubular design is the fastest-growing segment during the forecast period.

Who are the major players in the electrostatic precipitator market? +

The key participants in the electrostatic precipitator market are Mitsubishi Heavy Industries Ltd. (Japan), Valmet (Finland), GEA Group (Germany), Babcock and Wilcox Enterprises (US), DUCON (US), DURR Group (Germany), FLSmidth (Denmark), Fuel Tech Inc. (US), Monroe Environmental (US), Sumitomo Heavy Industries (Japan)and others.

What are the key trends in the electrostatic precipitator market? +

The electrostatic precipitator market is being shaped by several key trends including increasingly stringent environmental regulations and the growing emphasis on air quality management across various industries.