- Summary

- Table Of Content

- Methodology

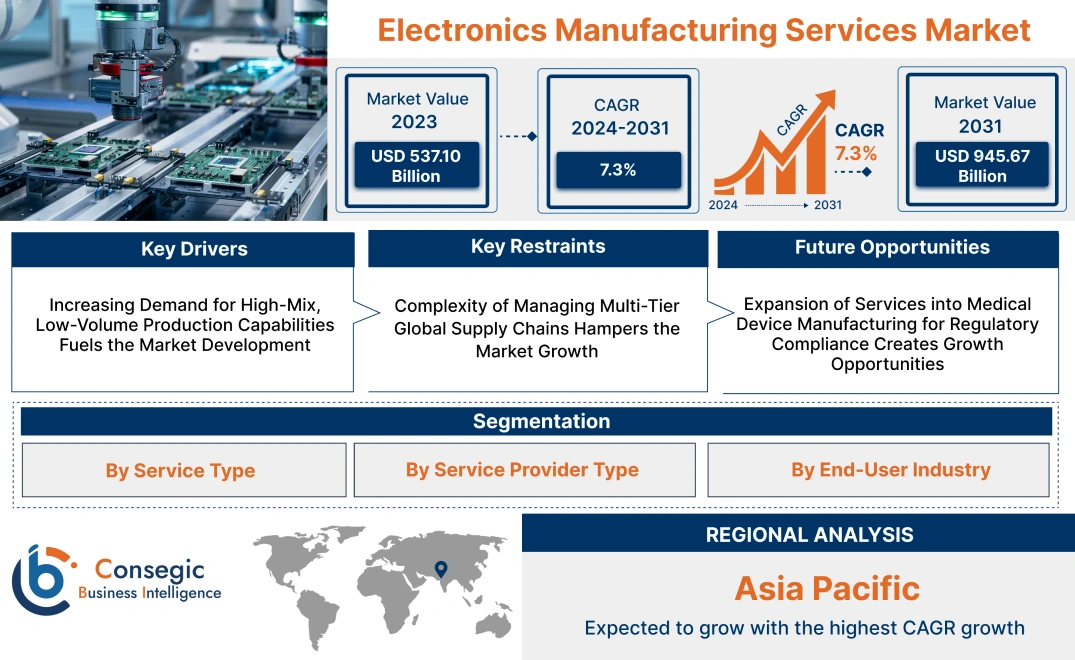

Electronics Manufacturing Services Market Size:

Electronics Manufacturing Services Market size is estimated to reach over USD 945.67 Billion by 2031 from a value of USD 537.10 Billion in 2023 and is projected to grow by USD 566.89 Billion in 2024, growing at a CAGR of 7.3% from 2024 to 2031.

Electronics Manufacturing Services Market Scope & Overview:

Electronics Manufacturing Services (EMS) encompass a range of services provided by specialized companies that design, manufacture, test, distribute, and offer return/repair services for electronic components and assemblies. These services are integral to industries such as consumer electronics, automotive, healthcare, and telecommunications, where they help streamline production processes, reduce time-to-market, and enhance product quality. EMS providers offer solutions including printed circuit board assembly (PCBA), component sourcing, testing, and logistics support, enabling companies to focus on core competencies while outsourcing their manufacturing needs.

With the rising adoption of IoT devices, 5G technology, and automation in various industries, EMS providers play a vital role in ensuring efficient production, scalability, and cost optimization. Key end-users of EMS include original equipment manufacturers (OEMs), consumer electronics companies, automotive suppliers, and medical device manufacturers. The market is expected to witness substantial development as industries continue to prioritize cost-effective and flexible manufacturing solutions to meet the increasing demand for electronic products and innovations.

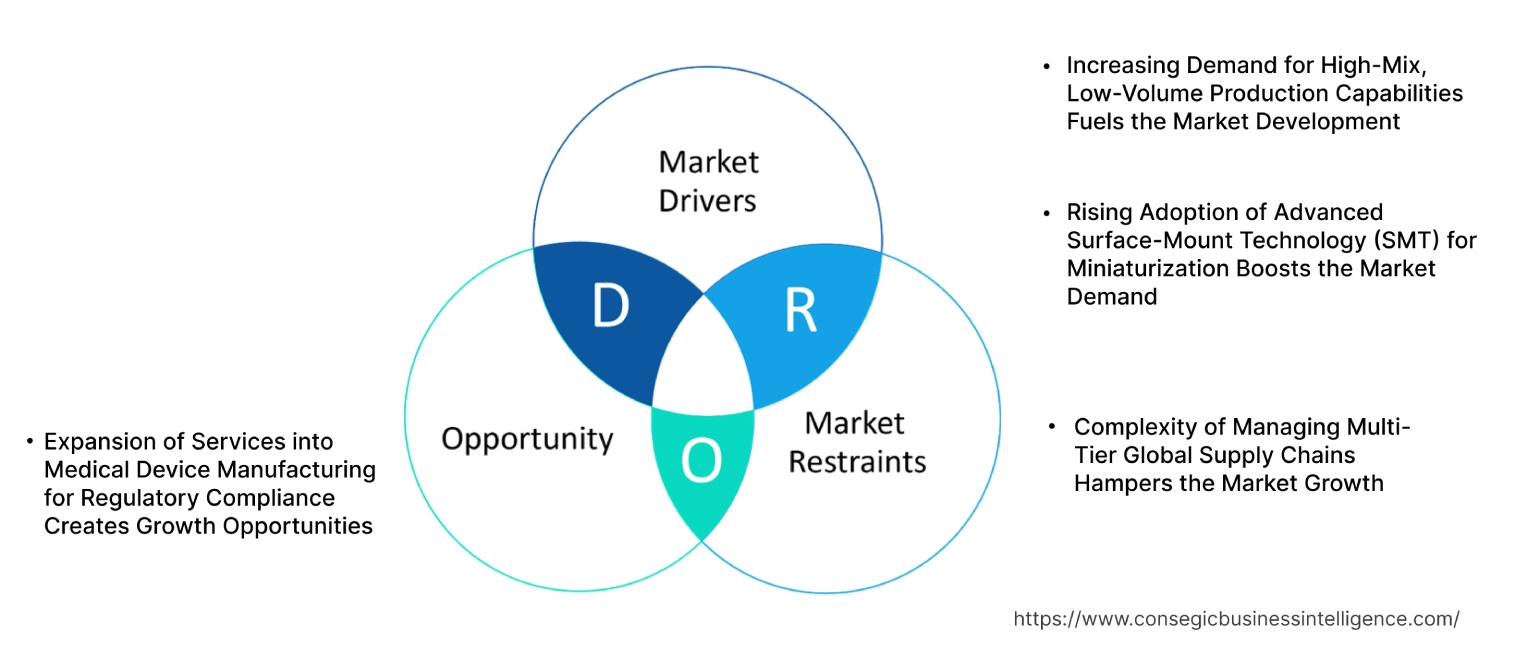

Electronics Manufacturing Services Market Dynamics - (DRO) :

Key Drivers:

Increasing Demand for High-Mix, Low-Volume Production Capabilities Fuels the Market Development

The growing trend toward customized electronics and niche product markets is driving need for electronics manufacturing services providers specializing in high-mix, low-volume (HMLV) production. Many Original Equipment Manufacturers (OEM), particularly in sectors such as medical devices, aerospace, and industrial electronics, require manufacturing solutions tailored to produce small batches of highly complex and customized products. The ability of EMS providers to offer flexible production lines, rapid prototyping, and efficient turnaround times for HMLV orders gives them a competitive edge, especially as the market shifts towards more personalized and application-specific electronics. This capability allows OEMs to quickly respond to market changes, reduce time-to-market for new products, and efficiently manage inventory, drives the electronics manufacturing services market growth.

Rising Adoption of Advanced Surface-Mount Technology (SMT) for Miniaturization Boosts the Market Demand

The increasing need for miniaturized electronic components in consumer electronics, wearables, and IoT devices is propelling the adoption of advanced Surface-Mount Technology (SMT) in the electronics manufacturing services market. SMT offers several advantages, including higher component density, reduced weight, and improved electrical performance, making it ideal for manufacturing compact and complex circuit boards. As devices become smaller and more feature-rich, the requirement for precise and high-speed SMT capabilities grows. EMS providers investing in cutting-edge SMT equipment and automated assembly lines are well-positioned to meet the evolving needs of OEMs looking for efficient solutions to produce smaller, lightweight, and high-performance electronic products. Therefore, the growing requirement for SMT further drives the electronics manufacturing services market demand.

Key Restraints :

Complexity of Managing Multi-Tier Global Supply Chains Hampers the Market Growth

The increasing complexity of multi-tier global supply chains is a significant challenge for the electronics manufacturing services market. EMS providers often source components and raw materials from multiple suppliers across various regions, each with its own set of logistical, regulatory, and operational challenges. Disruptions at any level of the supply chain—whether due to geopolitical tensions, natural disasters, or supplier issues— leads to delay, increased costs, and production bottlenecks. Managing such complex, multi-tier networks requires sophisticated supply chain visibility and coordination tools, which may not be fully integrated across all suppliers. The lack of real-time tracking and efficient communication across the supply chain leads to issues like component shortages, order backlogs, and increased lead times, impacting the ability of EMS companies to deliver products on schedule. This further impacts the electronics manufacturing services market expansion.

Future Opportunities :

Expansion of Services into Medical Device Manufacturing for Regulatory Compliance Creates Growth Opportunities

The growing demand for electronics in medical devices, driven by advancements in wearable health monitors, diagnostic equipment, and implantable devices, presents a significant opportunity for EMS providers specializing in high-reliability and regulated manufacturing environments. Medical device manufacturing requires stringent adherence to regulatory standards such as ISO 13485 for quality management systems and FDA compliance for product safety. EMS providers that offer specialized services, including cleanroom assembly, biocompatible materials handling, and comprehensive traceability, are well-positioned to attract OEMs in the medical device sector. As the medical technology market expands, driven by trends in telemedicine and patient monitoring, electronics manufacturing services companies capable of meeting these rigorous standards have a substantial growth opportunity. Therefore, the expanding medical technology market drives the electronics manufacturing services market opportunities.

Electronics Manufacturing Services Market Segmental Analysis :

By Service Type:

Based on service type, the electronics manufacturing services market is segmented into design & engineering services, manufacturing services, logistics services, and testing & quality control services.

The manufacturing services segment accounted for the largest revenue of the total electronics manufacturing services market share in 2023.

- Manufacturing services include the entire production process, such as component sourcing, assembly, and product fabrication.

- These services are critical for OEMs looking to reduce production costs and streamline supply chains.

- The rising trend of outsourcing manufacturing to specialized EMS providers, particularly in consumer electronics and automotive sectors, drives demand.

- EMS companies utilize advanced technologies like surface-mount technology (SMT) and automated assembly to enhance production efficiency.

- Manufacturing services dominate the market due to their comprehensive role in product development and the growing need for scalable, cost-effective production solutions.

- As per electronics manufacturing services market analysis, the manufacturing services segment boosts the market progress.

The logistics services segment is anticipated to register the fastest CAGR during the forecast period.

- Logistics services encompass inventory management, supply chain optimization, and distribution, enabling efficient movement of components and finished products.

- The increasing complexity of global supply chains and the need for efficient inventory management are driving demand for logistics services.

- EMS providers offer integrated logistics solutions, helping OEMs reduce lead times and optimize supply chain operations.

- The rise of just-in-time (JIT) manufacturing and the focus on minimizing warehousing costs are propelling development in the logistics segment.

- Logistics services are expected to grow rapidly due to the increasing need for efficient supply chain management and integrated distribution solutions.

- As per segmental trends analysis, the logistics services segment boosts the market development.

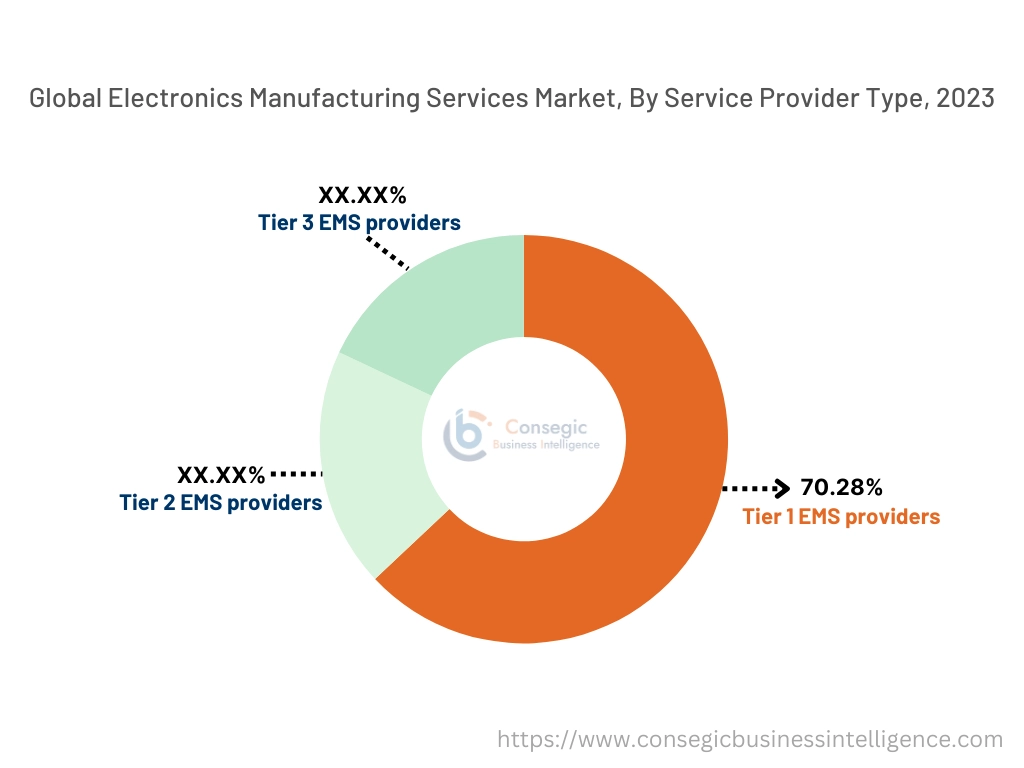

By Service Provider Type:

Based on service provider type, the electronics manufacturing services market is segmented into Tier 1 EMS providers, Tier 2 EMS providers, and Tier 3 EMS providers.

The Tier 1 EMS providers segment accounted for the largest revenue of 70.28% in 2023.

- Tier 1 providers are large, multinational companies offering end-to-end services, including design, prototyping, mass production, and after-sales support.

- These providers handle complex, high-volume projects for major OEMs across industries like consumer electronics, automotive, and telecommunications.

- Tier 1 EMS providers leverage extensive global supply chains and advanced technologies, such as robotics and AI-driven production lines.

- Their dominance is driven by the ability to manage large-scale projects and provide comprehensive solutions tailored to the needs of leading OEMs.

- Tier 1 EMS providers lead the market due to their strong partnerships with major OEMs and their capacity to deliver high-quality, large-scale manufacturing solutions.

- As per electronics manufacturing services market trends, the Tier 1 EMS providers segment boosts the market development.

The Tier 2 EMS providers segment is anticipated to register the fastest CAGR during the forecast period.

- Tier 2 EMS providers focus on mid-sized projects and offer specialized services, catering to niche market needs or specific field applications.

- These companies provide more flexible, tailored solutions, making them attractive to smaller OEMs and emerging startups.

- The increasing requirement for mid-volume production services and customized solutions is driving growth in the Tier 2 segment.

- Tier 2 EMS providers emphasize agility, quick turnaround times, and closer client relationships, meeting the needs of OEMs seeking specialized services.

- Tier 2 EMS providers are expected to grow rapidly due to their focus on niche services and mid-sized projects, catering to specific sector requirements.

- As per segmental trends analysis, the Tier 2 EMS providers segment boosts the market progress.

By End-User Industry:

Based on end-user industry, the EMS market is segmented into electronics, automotive, healthcare, and telecommunications.

The electronics segment accounted for the largest revenue share of the total electronics manufacturing services market share in 2023.

- The electronics industry is a major consumer of EMS services, particularly for the production of smartphones, tablets, wearables, and home entertainment devices.

- High requirement for feature-rich, high-quality devices drives the outsourcing of manufacturing to specialized EMS providers.

- The trend towards miniaturization and faster product launch cycles is further accelerating demand in the electronics segment.

- Leading EMS providers use advanced manufacturing processes to ensure high production volumes, precision, and cost-efficiency.

- Electronics dominate the EMS market due to the high requirement for efficient, scalable production solutions in consumer electronics and industrial applications.

- As per segmental trends analysis, the electronics segment boosts the market progress.

The automotive segment is anticipated to register the fastest CAGR during the forecast period.

- The automotive industry increasingly relies on EMS providers for the manufacturing of complex electronic components, including infotainment systems, ADAS, and electric vehicle (EV) parts.

- The shift towards smart and electric vehicles is driving the need for specialized, high-reliability electronics in automotive applications.

- EMS providers are playing a crucial role in producing advanced components for autonomous driving, safety systems, and connected vehicle technologies.

- The increasing adoption of electric vehicles and the integration of advanced electronics in traditional vehicles are boosting the need for EMS services in the automotive sector.

- The automotive segment is expected to grow rapidly, fueled by the rising integration of electronics and the shift towards electric and autonomous vehicles.

- As per segmental trends analysis, the automotive segment boosts the market progress.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

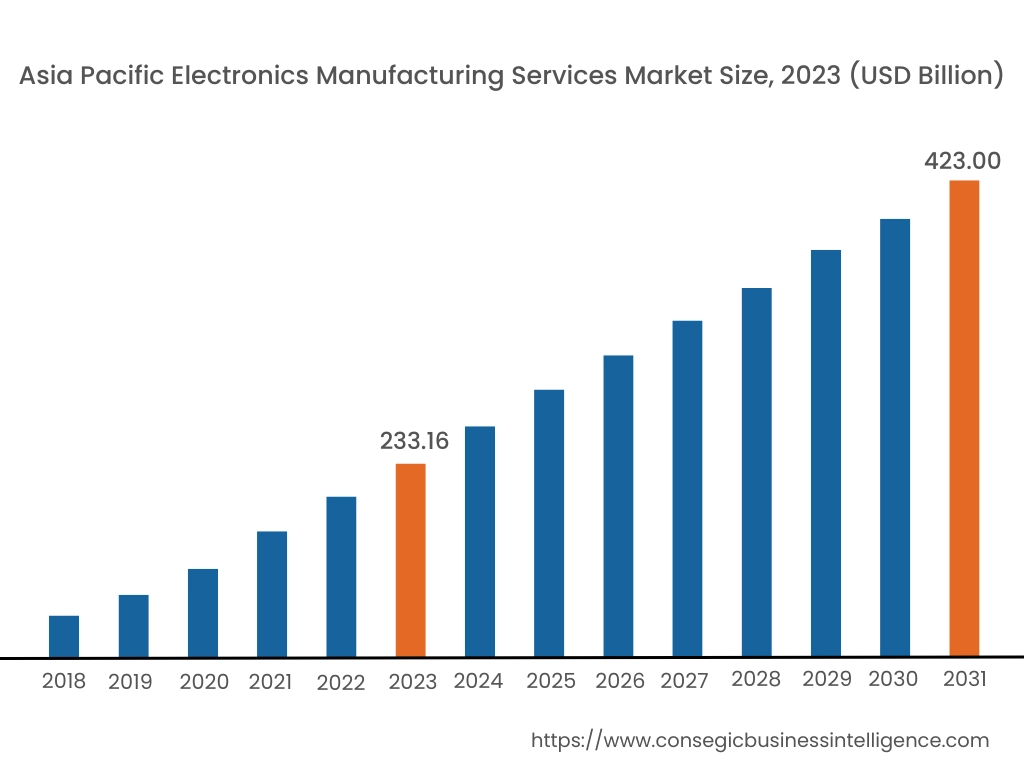

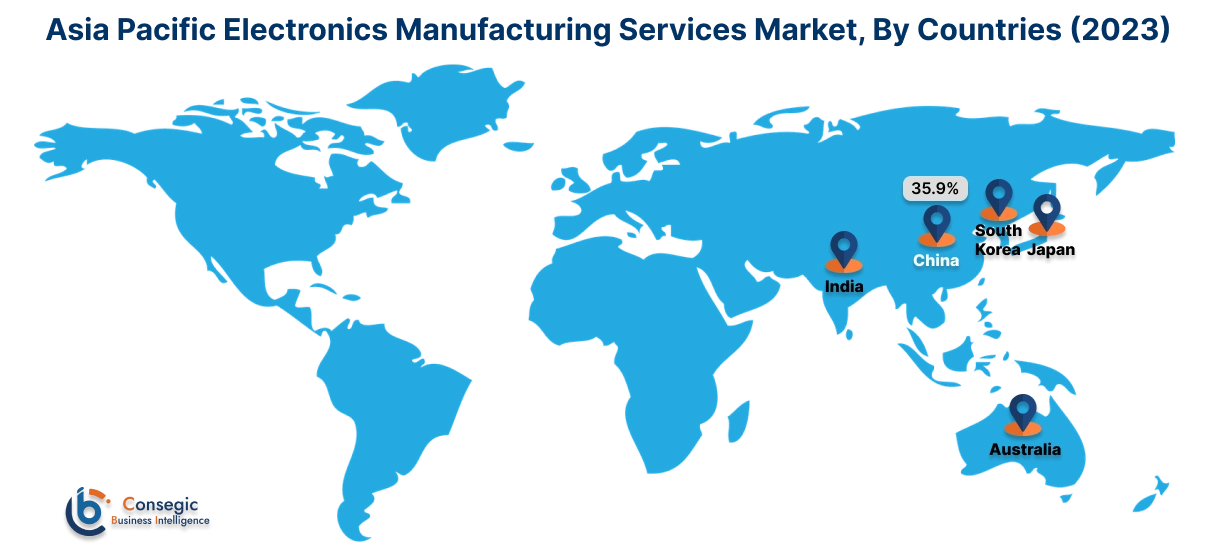

Asia Pacific region was valued at USD 233.16 Billion in 2023. Moreover, it is projected to grow by USD 246.71 Billion in 2024 and reach over USD 423.00 Billion by 2031. Out of which, China accounted for the largest share of 35.9% in 2023. Asia-Pacific is witnessing the fastest growth in the EMS market, driven by increasing electronics production, rising disposable incomes, and rapid urbanization in countries like China, Japan, and India. The region has become a global hub for electronics manufacturing, with a strong supply chain and cost advantages. The growing need for consumer electronics, automotive electronics, and telecommunications equipment contributes to market expansion.

North America is estimated to reach over USD 274.24 Billion by 2031 from a value of USD 157.29 Billion in 2023 and is projected to grow by USD 165.87 Billion in 2024. This region holds a substantial share of the EMS market, primarily due to a well-established electronics sector and the presence of major technology companies. The United States, in particular, has a significant market presence, with a focus on high-value and complex manufacturing services. The increasing need for advanced electronics in sectors such as aerospace, defense, and healthcare propels market growth.

Europe represents a significant share of the global EMS market, with countries like Germany, the UK, and France leading in terms of adoption and innovation. The region benefits from strong government support for advanced manufacturing and a robust industrial base. The focus on Industry 4.0 and the integration of smart manufacturing technologies further accelerates the adoption of EMS.

The Middle East & Africa region shows promising potential in the EMS market, particularly in countries like the UAE, Saudi Arabia, and South Africa. Increasing investments in infrastructure, a growing consumer electronics market, and government initiatives to promote local manufacturing drive the need for EMS. The expanding telecommunications sector and the adoption of smart technologies further support market growth.

Latin America is an emerging market for EMS, with Brazil and Mexico being the primary progress drivers. The rising adoption of consumer electronics, improving industrialization, and increasing focus on enhancing manufacturing capabilities contribute to the market's expansion. Government initiatives aimed at modernizing manufacturing infrastructure and promoting foreign investments support market progression.

Top Key Players & Market Share Insights:

The Electronics Manufacturing Services Market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Electronics Manufacturing Services Market. Key players in the Electronics Manufacturing Services industry include –

- Hon Hai Precision Industry Co., Ltd. (Foxconn) (Taiwan)

- Pegatron Corporation (Taiwan)

- Wistron Corporation (Taiwan)

- Flex Ltd. (Singapore)

- Jabil Inc. (USA)

- BYD Electronic (International) Company Limited (China)

- Universal Scientific Industrial Co., Ltd. (USI) (China)

- Sanmina Corporation (USA)

- New Kinpo Group (Taiwan)

- Celestica Inc. (Canada)

Recent Industry Developments :

Business Expansion:

- In October 2024, Cyient DLM has expanded its global footprint by acquiring a U.S.-based electronics manufacturing services (EMS) provider. This strategic acquisition strengthens Cyient DLM's capabilities in high-complexity, low-to-medium volume manufacturing, particularly in aerospace, defense, medical, and industrial sectors. It also enhances the company's presence in the U.S. market, positioning it for growth in advanced electronics manufacturing and supply chain services.

- In June 2024, TVS Electronics has expanded its manufacturing capabilities by adding Electronics Manufacturing Services (EMS) to its portfolio. This enhancement allows TVS to cater to a wider range of industries, offering comprehensive EMS solutions including design, manufacturing, and product lifecycle management. The initiative is aimed at supporting the growing demand for electronics manufacturing in India, aligning with the government's "Make in India" mission and boosting the company's position in the electronics industry.

- In February 2024, Neotech has launched a state-of-the-art NPI (New Product Introduction) and Electronics Manufacturing Center of Excellence in Silicon Valley, Northern California. This facility is designed to support advanced electronics manufacturing and product development, focusing on industries like aerospace, defense, and medical devices. It enhances Neotech's capabilities in high-reliability applications, offering cutting-edge technologies for rapid prototyping, testing, and production.

Electronics Manufacturing Services Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 945.67 Billion |

| CAGR (2024-2031) | 7.3% |

| By Service Type |

|

| By Service Provider Type |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Electronics Manufacturing Services (EMS) market? +

Electronics Manufacturing Services Market size is estimated to reach over USD 945.67 Billion by 2031 from a value of USD 537.10 Billion in 2023 and is projected to grow by USD 566.89 Billion in 2024, growing at a CAGR of 7.3% from 2024 to 2031.

What specific segmentation details are covered in the Electronics Manufacturing Services (EMS) Market report? +

The Electronics Manufacturing Services market report includes segmentation details for service type, service provider type, end-user industry, and region.

Which is the fastest-growing industry in the Electronics Manufacturing Services (EMS) market? +

According to the analysis, the automotive industry is the fastest growing in the EMS market, driven by the increasing demand for electric vehicles (EVs) and advanced driver-assistance systems (ADAS).

Who are the major players in the Electronics Manufacturing Services (EMS) Market? +

The key players in the EMS market include Foxconn Technology Group (Taiwan), Flex Ltd. (Singapore), Jabil Inc. (USA), Pegatron Corporation (Taiwan), Wistron Corporation (Taiwan), BYD Electronic (International) Company Limited (China), Universal Scientific Industrial Co., Ltd. (USI) (China), Celestica Inc. (Canada), Sanmina Corporation (USA), and New Kinpo Group (Taiwan).