- Summary

- Table Of Content

- Methodology

Electronic Packaging Market Size:

Electronic Packaging Market size is estimated to reach over USD 6,994.37 Million by 2031 from a value of USD 1,765.48 Million in 2023 and is projected to grow by USD 2,065.54 Million in 2024, growing at a CAGR of 18.78% from 2024 to 2031.

Electronic Packaging Market Scope & Overview:

Electronic packaging involves the enclosure and protection of electronic components and assemblies to ensure their functionality, reliability, and durability in various applications. This includes designing and manufacturing casings, housings, and substrates that protect sensitive components from environmental factors such as moisture, dust, and mechanical stress. Electronic packaging also facilitates thermal management, electrical interconnection, and signal integrity, making it a critical aspect of electronic device production.

This packaging technology is utilized across a wide range of sectors, including consumer electronics, automotive, aerospace, and industrial equipment. It supports various forms, such as chip-scale packaging, multi-chip modules, and printed circuit board (PCB) enclosures, to meet the specific requirements of different devices. Modern electronic packaging solutions integrate advanced materials and processes to ensure lightweight designs, compact structures, and enhanced performance.

End-users of these solutions include electronics manufacturers, semiconductor companies, and industrial equipment providers that rely on robust packaging to maintain the functionality and longevity of their products. Electronic packaging plays a pivotal role in ensuring the seamless operation of electronic devices in both standard and demanding environments.

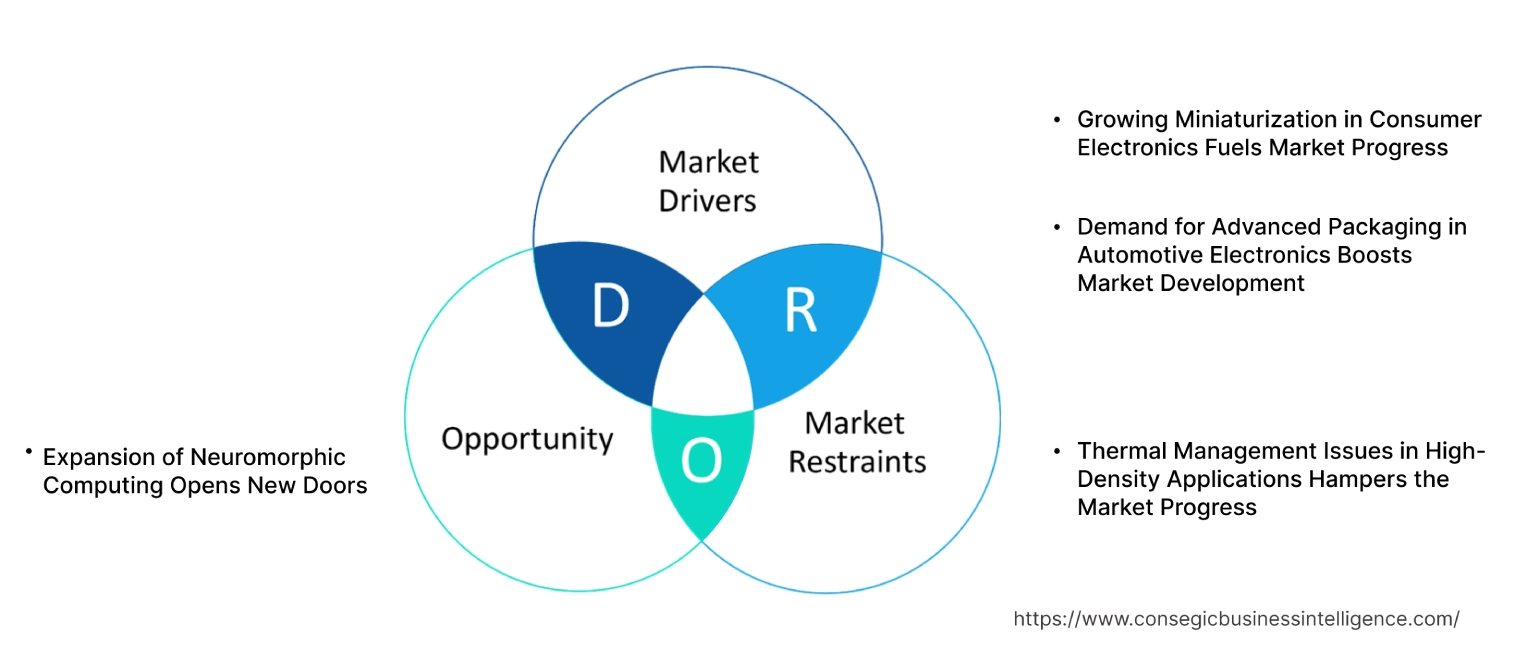

Electronic Packaging Market Dynamics - (DRO) :

Key Drivers:

Growing Miniaturization in Consumer Electronics Fuels Market Progress

The rising demand for compact and portable consumer electronics, including smartphones, wearables, and IoT devices, is significantly driving the need for innovative packaging solutions. As device sizes shrink, manufacturers require advanced technologies such as chip-scale packaging (CSP) and wafer-level packaging (WLP) to integrate multiple components efficiently within limited spaces. These solutions maintain high functionality, enhance performance, and improve thermal management, meeting the challenges of miniaturization without compromising reliability.

Additionally, lightweight designs and higher levels of component integration are becoming critical to support advanced features like 5G connectivity, AI processing, and extended battery life. Packaging technologies are evolving to meet these needs, ensuring seamless operation in compact devices. This trend toward miniaturization aligns with consumer preferences for sleek, portable products and is accelerating innovation across the industry, making advanced packaging solutions indispensable in modern electronics manufacturing. Thus, the aforementioned factors drive the electronic packaging market growth.

Demand for Advanced Packaging in Automotive Electronics Boosts Market Development

The automotive sector's rapid transition toward electric vehicles (EVs) and autonomous technologies is driving significant demand for advanced packaging solutions. Modern vehicles rely on sophisticated electronics, including advanced driver-assistance systems (ADAS), power management modules, and in-vehicle sensors, all of which require packaging that withstand high temperatures, vibrations, and harsh operating conditions.

Power modules in EVs, for example, need robust thermal management and efficient interconnect designs to ensure optimal performance and longevity. Similarly, ADAS and autonomous systems require high-reliability packaging to support sensors and processors critical for real-time data processing and safety. As the automotive sector integrates more electronics to enhance efficiency, safety, and functionality, innovative packaging solutions tailored for automotive-specific needs are becoming essential. This trend is pushing manufacturers to develop technologies that balance durability, performance, and scalability for next-generation vehicles, driving electronic packaging market demand.

Key Restraints :

Thermal Management Issues in High-Density Applications Hampers the Market Progress

The integration of high-performance chips in compact designs has intensified thermal management issues, especially in high-density applications such as data centers, high-performance computing (HPC) systems, and automotive electronics. These chips generate substantial heat during operation, and inadequate heat dissipation leads to performance degradation, system failures, or reduced lifespan of components. Advanced packaging technologies must incorporate efficient thermal management solutions, such as thermal vias, heat spreaders, or specialized materials, to maintain reliability and performance.

However, designing and implementing these solutions adds significant complexity and costs, making it difficult for some industries to adopt these technologies at scale. This constraint is particularly acute in applications requiring consistent, high-reliability operation under extreme conditions. The growing need for compact, high-performance systems continues to drive innovation in thermal management, but the cost and complexity restrain the electronic packaging market expansion.

Future Opportunities :

Expansion of Neuromorphic Computing Opens New Doors

The rise of neuromorphic computing, which emulates the neural structure of the human brain, is opening new opportunities in the electronics packaging market. Neuromorphic processors are designed for applications requiring real-time data processing, low latency, and energy efficiency, such as AI, robotics, and autonomous systems. These processors demand advanced packaging technologies that support high-density interconnects and exceptional thermal management due to the significant heat generated during operation.

Innovative packaging solutions, such as 3D integration and advanced thermal materials, are critical to ensure the reliability and performance of these processors. Additionally, the compact designs of neuromorphic systems require miniaturized yet robust packaging to facilitate efficient integration into diverse applications. As industries like healthcare, automotive, and consumer electronics explore neuromorphic computing for next-generation devices, the requirement for specialized packaging technologies tailored to this cutting-edge field is expected to grow, driving significant electronic packaging market opportunities.

Electronic Packaging Market Segmental Analysis :

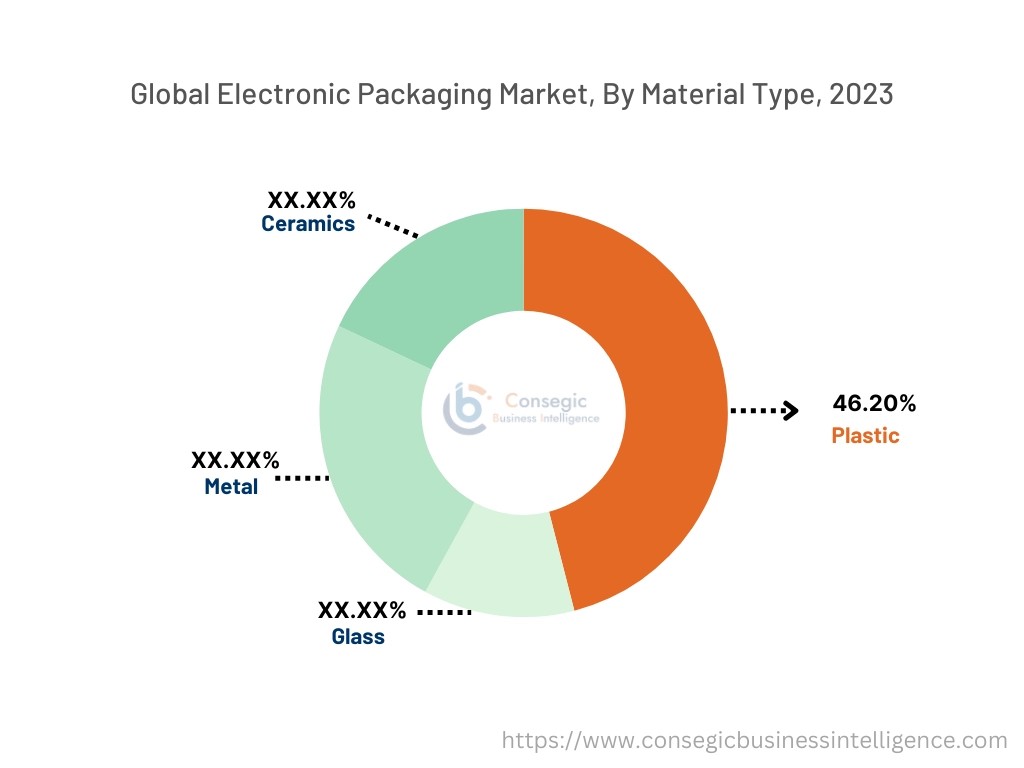

By Material Type:

Based on material type, the market is segmented into Plastic, Glass, Metal, and Ceramics.

The plastic segment accounted for the largest revenue of 46.20% of the total electronic packaging market share in 2023.

- Plastic materials are extensively used in electronic packaging due to their lightweight, cost-effectiveness, and excellent insulating properties.

- These materials offer versatility in design and are molded into complex shapes, making them ideal for consumer electronics and automotive components.

- Advancements in biodegradable and recyclable plastic materials are aligning with sustainability trends, further boosting adoption.

- As per electronic packaging market analysis, the dominance of this segment reflects its adaptability and extensive use across a wide range of electronic applications.

The ceramics segment is expected to grow at the fastest CAGR during the forecast period.

- Ceramics are preferred for high-performance electronic packaging applications due to their superior thermal conductivity and resistance to high temperatures.

- These materials are widely used in aerospace and defense applications, where reliability and durability are critical.

- Technological advancements in ceramic packaging, such as multilayer structures, are enabling integration with high-frequency electronic components.

- The analysis of segmental trends shows that the rapid progress of this segment is driven by the increasing need for advanced packaging solutions in high-end applications, fueling the electronic packaging market growth.

By Packaging Type:

Based on packaging type, the market is segmented into Surface Mount Packaging, Through-Hole Packaging, and Hybrid Packaging.

The surface mount packaging segment held the largest revenue of the total electronic packaging market share in 2023.

- Surface mount packaging is extensively used in compact and lightweight electronic devices, offering improved performance and ease of assembly.

- This packaging type supports high-speed manufacturing processes, making it a preferred choice for mass production in the consumer electronics and automotive sectors.

- The integration of surface mount technology with advanced materials is enhancing thermal management and reliability.

- As per electronic packaging market trends, the dominance of this segment reflects its ability to meet the requirements of modern electronic devices, including smartphones, tablets, and wearables.

The hybrid packaging segment is expected to grow at the fastest CAGR during the forecast period.

- Hybrid packaging combines the benefits of surface mount and through-hole technologies, enabling flexibility in design and functionality.

- This packaging type is gaining traction in aerospace and healthcare applications, where customized solutions are essential for high-performance electronics.

- The segment benefits from advancements in microelectronics and miniaturization, supporting its adoption in cutting-edge devices.

- As per segmental trends analysis, the rapid growth of this segment reflects its role in addressing the evolving needs of specialized electronic applications.

By End-User Industry:

Based on the end-user industry, the market is segmented into Consumer Electronics, Automotive, Aerospace & Defense, Healthcare, IT & Telecom, and Others.

The consumer electronics segment accounted for the largest revenue share in 2023.

- Electronic packaging is critical for protecting components in consumer devices such as smartphones, laptops, and gaming consoles.

- The growing adoption of IoT-enabled devices and smart home technologies is driving demand for reliable and cost-effective packaging solutions.

- Integration of advanced packaging materials is enhancing device performance, contributing to the dominance of this segment.

- As per electronic packaging market analysis, the segment's growth is supported by the increasing penetration of consumer electronics in emerging economies.

The aerospace & defense segment is expected to grow at the fastest CAGR during the forecast period.

- Aerospace and defense applications require electronic packaging solutions with high thermal and mechanical reliability.

- These solutions are integral to mission-critical systems, including avionics, radar systems, and satellite communication devices.

- The segment benefits from advancements in materials and technologies, ensuring durability in extreme environmental conditions.

- As per electronic packaging market trends, the fast-track growth of this segment is driven by increased investments in defense modernization programs and space exploration initiatives.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

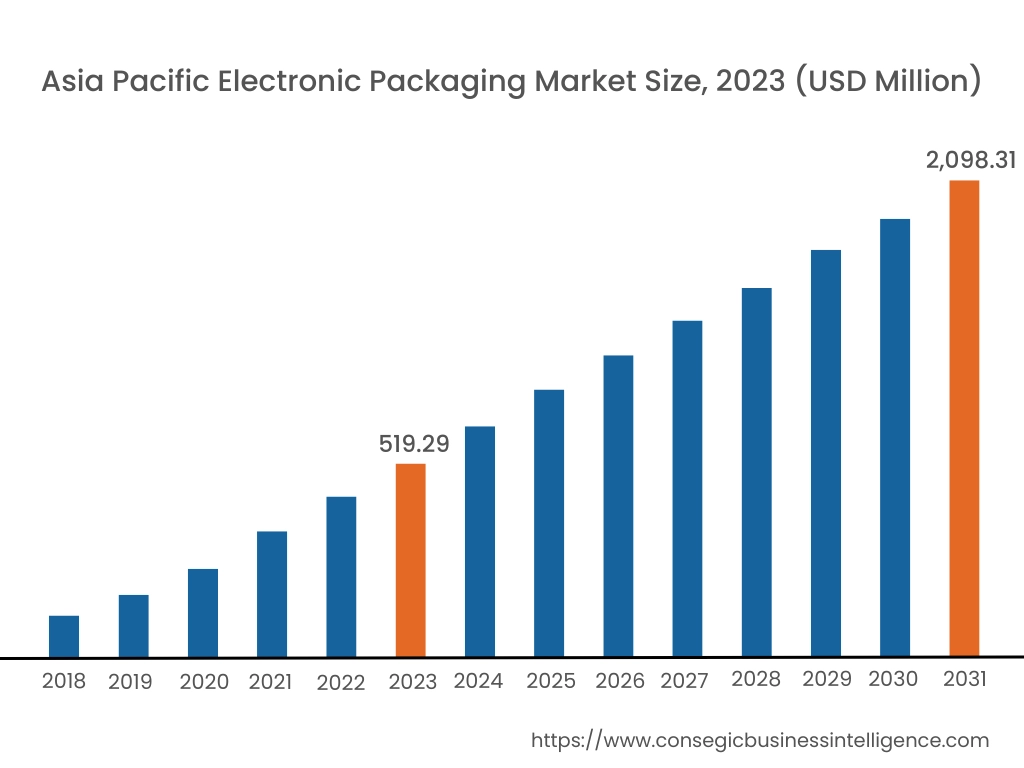

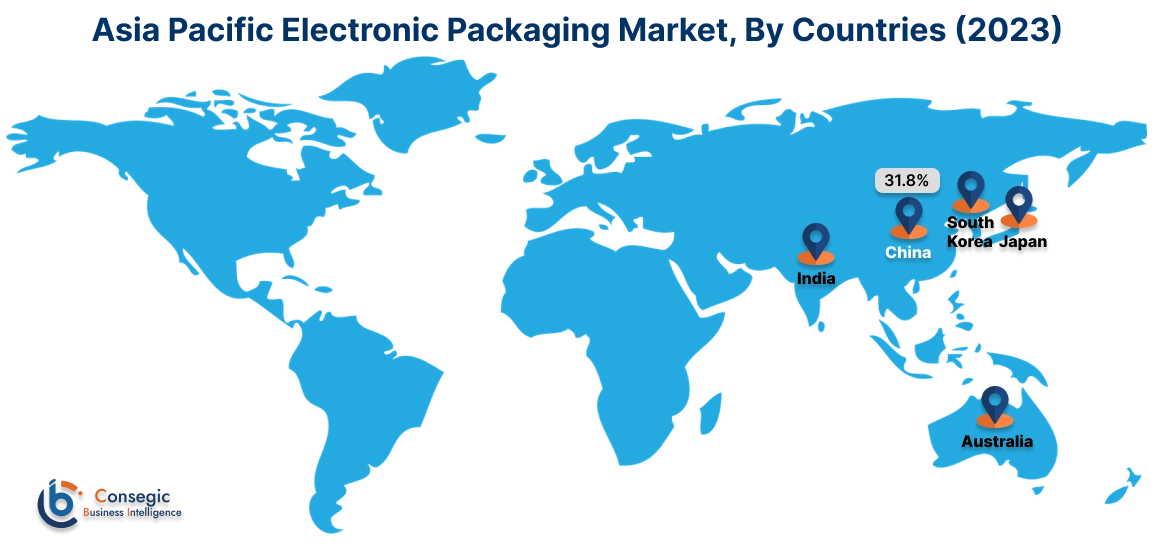

Asia Pacific region was valued at USD 519.29 Million in 2023. Moreover, it is projected to grow by USD 608.55 Million in 2024 and reach over USD 2,098.31 Million by 2031. Out of these, China accounted for the largest share of 31.8% in 2023. The Asia-Pacific region is experiencing rapid growth in the electronic packaging market, driven by industrialization and urbanization in countries like China, India, and Japan. The region has become a global hub for electronics manufacturing, with a strong emphasis on consumer electronics to support the growing middle-class population. The increasing investments in technology and the proliferation of the semiconductor sector are further propelling the electronic packaging market demand.

North America is estimated to reach over USD 2,301.15 Million by 2031 from a value of USD 586.83 Million in 2023 and is projected to grow by USD 685.98 Million in 2024. This region maintains a significant position in the electronic packaging market, primarily due to its advanced industrial sector and early adoption of innovative technologies. The United States, in particular, has integrated electronic packaging solutions extensively across industries such as consumer electronics, healthcare equipment, aerospace, and defense. The trend towards miniaturization and enhanced functionality in electronic devices has further propelled the utilization of advanced packaging techniques.

Europe holds a substantial share of the global market, with countries like Germany, France, and the United Kingdom leading in terms of adoption and innovation. The region benefits from a well-established electronics sector and a strong emphasis on sustainability. The requirement for eco-friendly and efficient packaging solutions is increasing, driven by stringent environmental regulations and the push towards reducing electronic waste further boosting the electronic packaging market opportunities.

The Middle East & Africa region shows promising potential in the market, particularly in countries like Saudi Arabia, the United Arab Emirates, and South Africa. Increasing investments in technology infrastructure and the enlargement of the electronics sector are driving the need for advanced packaging solutions. The analysis of the market trends shows that the focus on diversifying economies and reducing dependence on oil revenues has led to growth in the electronics manufacturing sector.

Latin America is an emerging market for electronic packaging, with Brazil and Mexico being the primary growth drivers. The rising adoption of consumer electronics, improving manufacturing infrastructure, and increasing focus on enhancing product safety contribute to the market’s development. As per market analysis, government initiatives aimed at modernizing manufacturing processes and promoting technological innovation are supporting electronic packaging market expansion.

Top Key Players & Market Share Insights:

The electronic packaging market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global electronic packaging market. Key players in the electronic packaging industry include -

- Amkor Technology, Inc. (USA)

- ASE Technology Holding Co., Ltd. (Taiwan)

- JCET Group Co., Ltd. (China)

- Intel Corporation (USA)

- Samsung Electronics Co., Ltd. (South Korea)

- Advanced Semiconductor Engineering, Inc. (Taiwan)

- Nippon Mektron, Ltd. (Japan)

- STATS ChipPAC Ltd. (Singapore)

- SPIL (Siliconware Precision Industries Co., Ltd.) (Taiwan)

- Powertech Technology Inc. (Taiwan)

Recent Industry Developments :

- In August 2024, AOS (Alpha and Omega Semiconductor) expanded its surface mount package offerings with the LFPAK 5x6 package, designed for high-performance and high-reliability applications. The new package, available in 40V, 60V, and 100V options, is built for industries requiring robust power handling, such as industrial, server, telecom, and solar markets. The LFPAK features rugged gull-wing leads, improved electrical/thermal performance, and supports high-reliability applications with low on-resistance and enhanced heat dispersion.

Electronic Packaging Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 6,994.37 Million |

| CAGR (2024-2031) | 18.78% |

| By Material Type |

|

| By Packaging Type |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Electronic Packaging Market? +

Electronic Packaging Market size is estimated to reach over USD 6,994.37 Million by 2031 from a value of USD 1,765.48 Million in 2023 and is projected to grow by USD 2,065.54 Million in 2024, growing at a CAGR of 18.78% from 2024 to 2031.

What are the key segments in the Electronic Packaging Market report? +

The Electronic Packaging Market is segmented by material type (Plastic, Glass, Metal, Ceramics), packaging type (Surface Mount Packaging, Through-Hole Packaging, Hybrid Packaging), end-user industry (Consumer Electronics, Automotive, Aerospace & Defense, Healthcare, IT & Telecom, Others), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which material type segment is expected to grow the fastest in the Electronic Packaging Market? +

The ceramics segment is expected to grow at the fastest CAGR during the forecast period, driven by its superior thermal conductivity and resistance to high temperatures, making it ideal for aerospace and defense applications.

Who are the major players in the Electronic Packaging Market? +

Major players in the Electronic Packaging Market include Amkor Technology, Inc. (USA), ASE Technology Holding Co., Ltd. (Taiwan), JCET Group Co., Ltd. (China), Intel Corporation (USA), Samsung Electronics Co., Ltd. (South Korea), Advanced Semiconductor Engineering, Inc. (Taiwan), and others.