- Summary

- Table Of Content

- Methodology

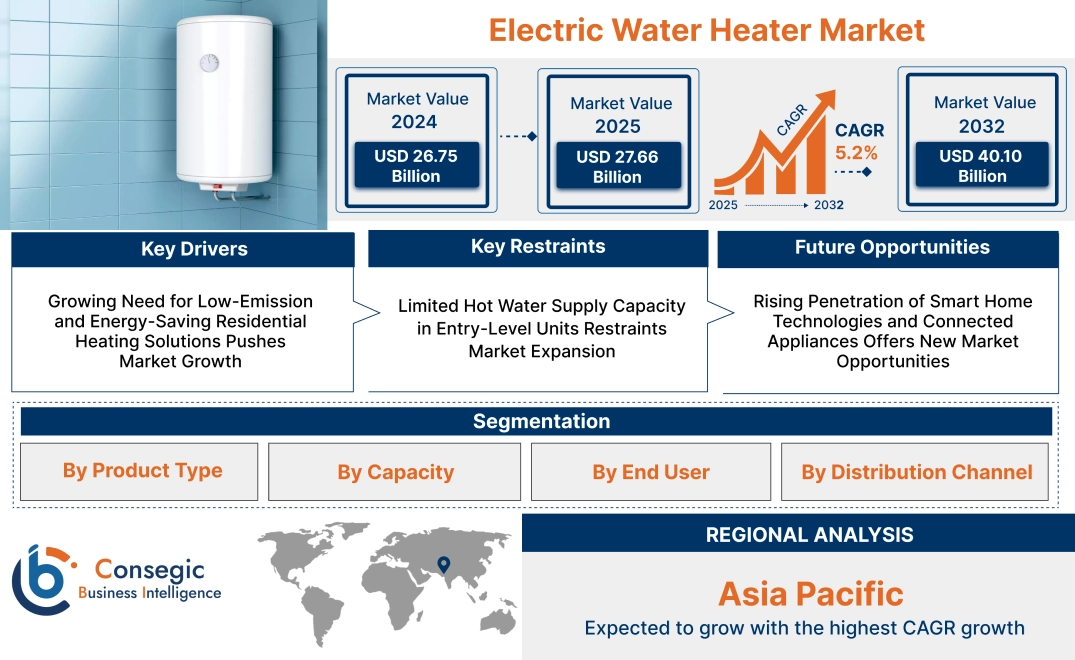

Electric Water Heater Market Size:

Electric Water Heater Market size is estimated to reach over USD 40.10 Billion by 2032 from a value of USD 26.75 Billion in 2024 and is projected to grow by USD 27.66 Billion in 2025, growing at a CAGR of 5.2% from 2025 to 2032.

Electric Water Heater Market Scope & Overview:

Electric water heater is a device that heats water by electrical resistance elements, typically used in domestic, commercial, and institutional environments. It offers on-demand or stored hot water via tank-type or tankless configurations, satisfying various usage needs with accurate temperature control.

These systems provide the attributes of energy-efficient insulation, digital thermostats, safety shut-off, and space-saving configurations. Their advantages are low working noise, steady output, and low maintenance levels over fuel-based counterparts. Their versatility in installation and compatibility with different building geometries add to their popularity.

Whether installed as centralized plumbing or at point-of-use fixtures, an electric water heater enables consistent provision of hot water for sanitation, cooking, and cleaning. These units' ability to adapt in small households up to large-scale facilities provides high applicability levels, thus the units form an essential part of contemporary water heating infrastructure, meant to be convenient as well as in operation.

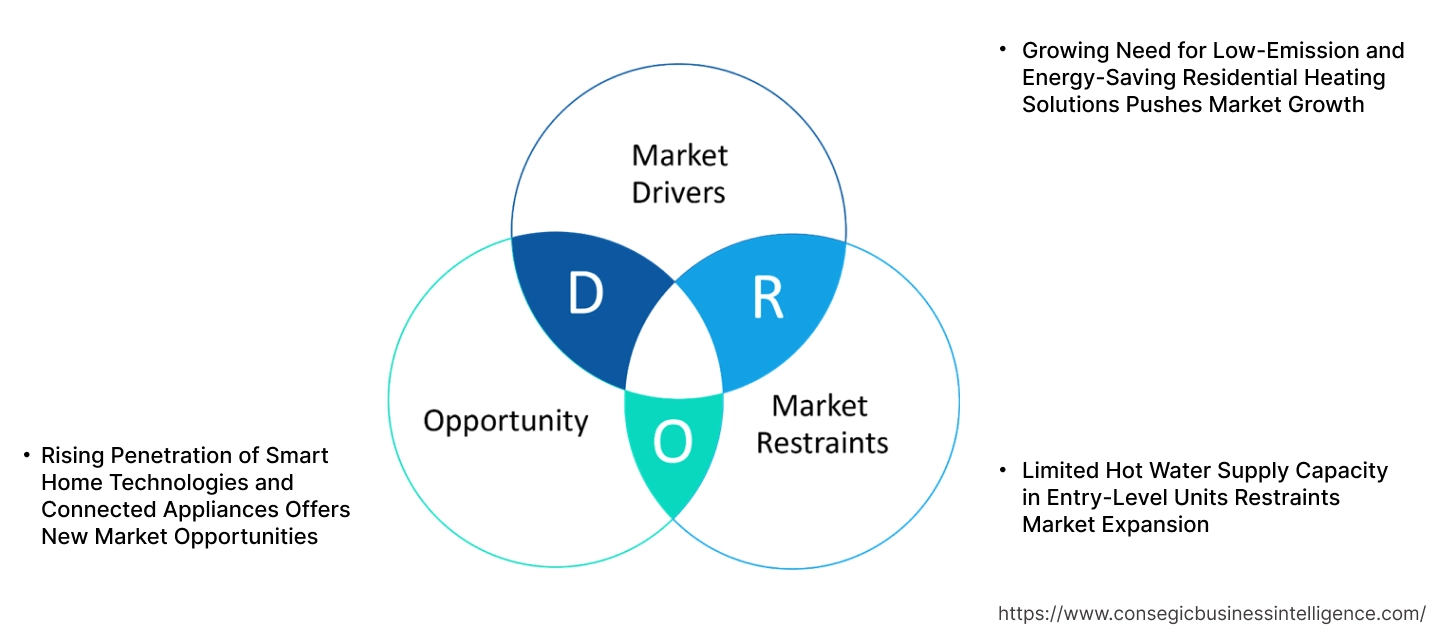

Electric Water Heater Market Dynamics - (DRO):

Key Drivers:

Growing Need for Low-Emission and Energy-Saving Residential Heating Solutions Pushes Market Growth

The move towards energy-saving household systems has raised the stature of electric water heaters in new residential systems. The devices provide hot water without emissions related to combustion, in line with tightening building energy codes and decarbonization requirements. With newer technology featuring improved insulation and smart thermostat operation, newer models minimize standby heat loss and optimize usage. European, North American, and Asian urban homes are adopting electric types as gas subsidies are reducing and grid electrification is spreading. Moreover, the efficiency of electric systems with solar PV installations is further supporting the use of electric variants in green building schemes. The changeover is also being driven by growing concern about indoor air quality, as electric heating does away with the threat from carbon monoxide indoors. Cumulatively, these technical, regulatory, and health-driven factors are driving a strong incentive for energy-efficient consumers to replace conventional systems. The synergy of these trends is driving long-term electric water heater market expansion.

Key Restraints:

Limited Hot Water Supply Capacity in Entry-Level Units Restraints Market Expansion

Entry-level electric water heaters, especially those targeting small apartments or budget-conscious markets, tend to have limited tank capacity and slower reheating times. In applications with high or concurrent water usage—e.g., multi-family homes or back-to-back showers—these systems find it difficult to satisfy user expectations for continued hot water. The small recovery rate results in discomfort and dissatisfaction, causing some consumers to switch to alternative technologies with increased tanks or flow rates. These small systems are also not very flexible for integration into multi-zone plumbing configurations, restricting applications in larger residences or commercial environments. In hospitality, retail, or healthcare settings, where continuous hot water availability is not negotiable and performance reliability is a major buying factor, the requirement for well-functioning heaters is rising. Although the price point is still competitive, operational constraints frequently outweigh initial cost savings in high-usage scenarios. This ongoing performance shortfall undermines broader adoption in mid- to high-demand markets, thus hindering electric water heater market growth.

Future Opportunities:

Rising Penetration of Smart Home Technologies and Connected Appliances Offers New Market Opportunities

Home automation infrastructure is quickly changing, with consumers increasingly prioritizing energy visibility, convenience, and control over their home systems. Electric water heaters are subsequently being redesigned to meet these expectations—with Wi-Fi connectivity, app-based interfaces, and voice assistant integration. These upgrades allow homeowners to schedule hot water cycles, track consumption patterns, and be informed in real-time about energy usage. In areas with dynamic electricity tariffs or time-of-use pricing models, these characteristics promote load shifting, improving cost-effectiveness and grid stability. Furthermore, utilities are also starting to integrate connected water heaters into demand-response programs, further establishing these systems as active participants in today's energy environment. The integration of connectivity, automation, and energy intelligence is transforming how consumers engage with residential water heating.

- For instance, in March 2025, Cala, a tech startup, unveiled the world's first smart heat pump water heater. It provides long-term savings, along with hot water maximization and reduced carbon footprint. Its smart home technology integrates solar panels as well as learns the habits of the user's hot water usage, allowing efficient performance. In addition, it optimizes the heating rate based on future planning, improving the user experience.

This digital evolution is not only increasing the functional benefit of these devices but also releasing premium price potential and service models, ultimately establishing huge electric water heater market opportunities fueled by both necessity and growth.

Electric Water Heater Market Segmental Analysis :

By Product Type:

Based on product type, the electric water heater market is segmented into storage water heaters, tankless (on-demand) water heaters, and hybrid water heaters.

Storage water heaters dominated the largest electric water heater market share in 2024.

- They hold pre-heated water, and hence, they are best suited for residential use with constant water usage.

- Storage water heaters support low-voltage configurations and are economical to install and maintain.

- They are equipped with smart thermostats and energy-efficient insulation, making them more desirable.

- High usage in emerging economies, according to the electric water heater market analysis, makes them the dominant segment.

Tankless water heaters are projected to register the fastest CAGR during the forecast period.

- Instant hot water provision by on-demand systems minimizes standby energy loss and makes operations energy-efficient.

- Their small size enables deployment in urban apartments with limited space and variable usage patterns.

- According to segmental trends, the increasing demand for green buildings and smart homes drives adoption.

- For instance, in November 2024, Noritz upgraded its EZ Series residential tankless water heaters with higher energy efficiencies and Bluetooth connectivity. The product line also includes a new heater size.

- The segment will drive the electric water heater market growth due to the growing energy-conscious consumer behavior.

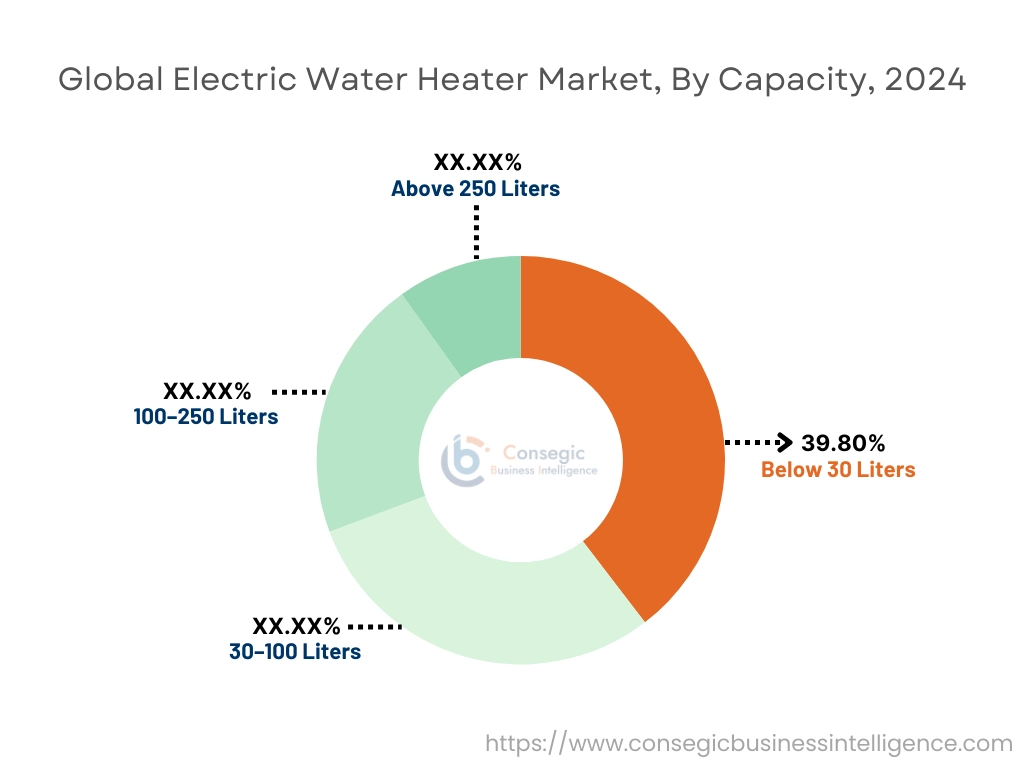

By Capacity:

Based on capacity, the market is divided into below 30 liters, 30–100 liters, 100–250 liters, and above 250 liters.

Below 30 Liters was the dominant segment with 39.8% market in 2024.

- Compact electric water heaters below 30 liters are ideal for point-of-use installations, particularly in residential settings such as kitchens and single-bathroom homes.

- Their affordability, ease of installation, and low power consumption drive strong adoption across urban households and low-rise buildings.

- Widespread integration in small commercial applications including cafés, clinics, and offices further supports electric water heater market demand.

- According to electric water heater market analysis, increasing construction of compact housing units and growing emphasis on energy efficiency are key drivers for this segment.

Above 250 Liters is expected to witness the fastest CAGR during the forecast period.

- These big capacity models appeal to commercial units, hotels, and large-scale households with multiple-point usage.

- The sector is driven by expansion in hospitality and healthcare markets, which have a need for continuous hot water supply.

- They are incorporating IoT-based monitoring and remote diagnostics to increase operational reliability.

- According to electric water heater market trends, growing adoption among commercial verticals will fuel growth in the future.

By End Use:

On the basis of end-user, the market is categorized into residential, commercial, and industrial.

The residential segment held the largest electric water heater market share in 2024.

- Urbanization, improving living standards, and weather-driven heating demands are driving residential installations.

- Government subsidies in Asia-Pacific and Europe encourage homebuyers to convert to efficient models.

- Wi-Fi connected and timer-run smart electric water heaters are trending in the sector.

- This way, electric water heater market demand within residential is underpinned by replacement cycles which do not fail consistently.

The commercial segment is expected to register the fastest CAGR during the forecast period.

- Hotels, hospitals, and shopping areas demand continuous hot water for sanitary as well as for comfort applications.

- Increased infrastructure growth in emerging economies is driving quick product deployment.

- Incorporation of solar-electric hybrid systems in commercial properties is aiding sustainability objectives.

- Furthermore, smart monitoring and centralized heating control are boosting commercial adoption, which in turn is propelling the electric water heater market demand.

By Distribution Channel:

Based on distribution channel, the market is segmented into offline (retail stores, distributors) and online (e-commerce platforms, brand websites).

Offline distribution led the market in terms of revenue share in 2024.

- Shoppers like to physically inspect and consult from franchisees before buying water heaters.

- Local retail channels are a vital factor in tier-2 and tier-3 cities where internet penetration is weak.

- Product bundling, financing options, and after-sales service reinforce offline dominance in sales.

- Electric water heater market trends indicate that offline channels provide faster delivery and installation facilities..

Online is expected to be the fastest-growing distribution channel during the forecast period.

- E-commerce facilitates price transparency, reviews, and broad product availability throughout regions.

- The swift uptake of digital purchasing behavior among urban customers enhances this segment's performance.

- Manufacturers are collaborating with online marketplaces and investing in D2C platforms.

- In addition, online channels are driving the electric water heater market expansion through seasonal promotions and doorstep service.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

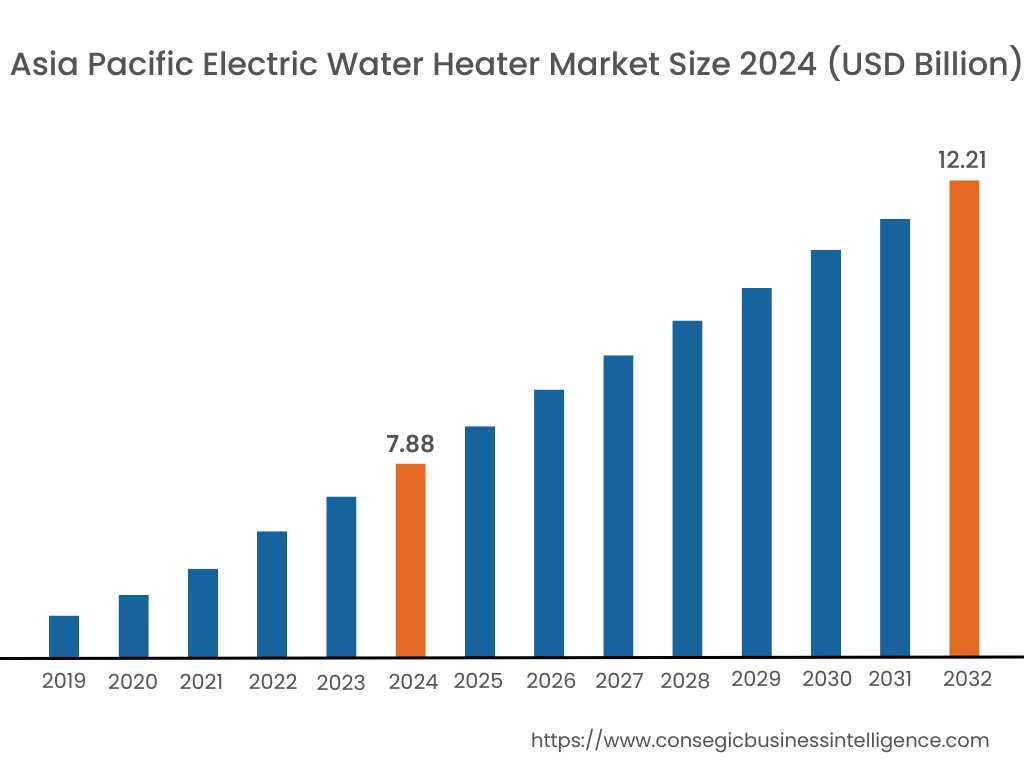

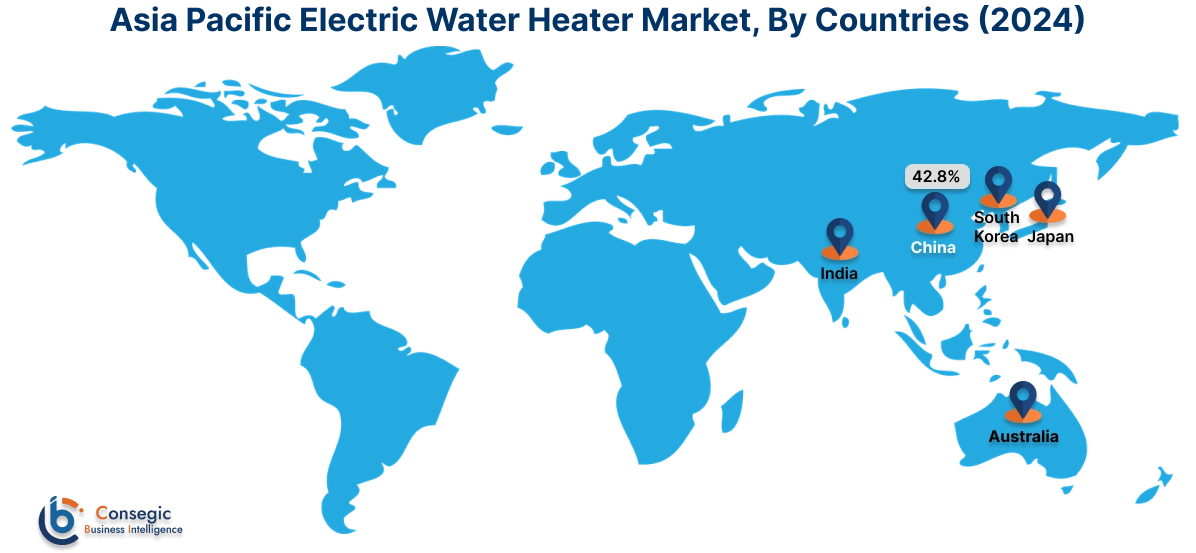

Asia Pacific region was valued at USD 7.88 Billion in 2024. Moreover, it is projected to grow by USD 8.17 Billion in 2025 and reach over USD 12.21 Billion by 2032. Out of this, China accounted for the maximum revenue share of 42.8%. Asia-Pacific is witnessing strong growth, as reinforced by strong urban development, increased disposable income, and increasing electrification of dwelling infrastructure. Production and consumption leaders are China, India, Japan, and South Korea, where middle-income residential homes and hotels have adopted in bulk. Data analysis indicates that continuous electrification policies, particularly in rural towns, and spread of online channels for retail sales have increased the speed of accessing affordable water heating solutions. The high population growth and increasing pipeline of housing constructions in the region offer a substantial electric water heater market opportunity in the long run.

North America is estimated to reach over USD 13.00 Billion by 2032 from a value of USD 8.87 Billion in 2024 and is projected to grow by USD 9.16 Billion in 2025. North America is a mature market with high replacement needs, growing knowledge about the importance of energy efficiency, and steady investment in home upgrades. The United States and Canada illustrate mass adoption, especially in single-family residences, rentals, and small commercial structures. Analysis reveals growing demand for intelligent, tankless, and ENERGY STAR®-certified equipment as customers turn toward environmentally friendly and cost-efficient technologies. Policy support of decarbonization and increasing utility rebates for efficient heating products are also supporting product adoption within the region.

Europe continues to hold a major position in the international electric water heater industry, supported by its established energy-efficiency standards and green climate goals. Germany, the UK, France, and the Netherlands are driving the adoption of energy-efficient heating devices as part of comprehensive building decarbonization processes. Regional trend analysis points towards a market trend towards compact, wall-mounted, and hybrid models that are tied to solar thermal systems. The demand is strongest in multi-residential buildings, city retrofits, and districts where central heat distribution networks are being replaced with decentralized systems.

Latin America is experiencing gradual market growth, particularly in Brazil, Mexico, Chile, and Colombia. Middle-class income is increasing, causing regional adoption because of growing awareness of home comfort products and local manufacturing efforts. Analysis indicates that instantaneous water heaters are favored where climates are warm, but storage-type units are becoming popular in high-altitude and cooler locations. Residential real estate growth and tourism-driven projects are likely to drive steady market performance.

Middle East and Africa is a developing market, and product demand is fueled by a combination of urbanization, enhanced availability of power, and growing consumer expectations in the UAE, Saudi Arabia, South Africa, and Kenya. The market study of the region reveals that while gas and solar heaters continue to be prevalent in some segments, interest is growing in electric water heating solutions due to their ease of installation and reliability. Smart city projects and infrastructural developments in major metropolitan zones continue to bring in growth opportunities, especially where energy reliability from utility-scale sources is being enhanced.

Top Key Players & Market Share Insights:

The electric water heater market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global electric water heater market. Key players in the electric water heater industry include –

- Smith Corporation (USA)

- Robert Bosch GmbH (Germany)

- Whirlpool Corporation (USA)

- Bajaj Electricals Ltd. (India)

- Haier Group Corporation (China)

- Ariston Thermo Group (Italy)

- Rheem Manufacturing Company (USA)

- Rinnai Corporation (Japan)

- Bradford White Corporation (USA)

- Noritz Corporation (Japan)

Recent Industry Developments :

Product Launches:

- In July 2024, Rinnai Australia launched its first Electric Continuous Flow hot water system, Rinnai Efinity. The heater boasts precise temperature control along with adjustable temperature and flow rates to meet the requirements of modern consumers. It is designed to ensure uninterrupted hot water access for residential and commercial purposes.

Acquisitions:

- In March 2025, Ariston Group acquired DDR Heating, a U.S.-based manufacturer specializing in tubular electric heaters for professional and industrial applications. This move enables the entry of the Ariston Group’s components division, Thermowatt, into the North American market.

Electric Water Heater Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 40.10 Billion |

| CAGR (2025-2032) | 5.2% |

| By Product Type |

|

| By Capacity |

|

| By End User |

|

| By Distribution Channel |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Electric Water Heater Market? +

Electric Water Heater Market size is estimated to reach over USD 40.10 Billion by 2032 from a value of USD 26.75 Billion in 2024 and is projected to grow by USD 27.66 Billion in 2025, growing at a CAGR of 5.2% from 2025 to 2032.

What specific segmentation details are covered in the Electric Water Heater Market report? +

The Electric Water Heater market report includes specific segmentation details for product type, capacity, distribution channel and end-user.

What are the end-users in the Electric Water Heater Market? +

The end-users of the Electric Water Heater Market are residential, commercial and industrial.

Who are the major players in the Electric Water Heater Market? +

The key participants in the Electric Water Heater market are A. O. Smith Corporation (USA), Robert Bosch GmbH (Germany), Ariston Thermo Group (Italy), Rheem Manufacturing Company (USA), Rinnai Corporation (Japan), Bradford White Corporation (USA), Noritz Corporation (Japan), Whirlpool Corporation (USA), Bajaj Electricals Ltd. (India) and Haier Group Corporation (China).