- Summary

- Table Of Content

- Methodology

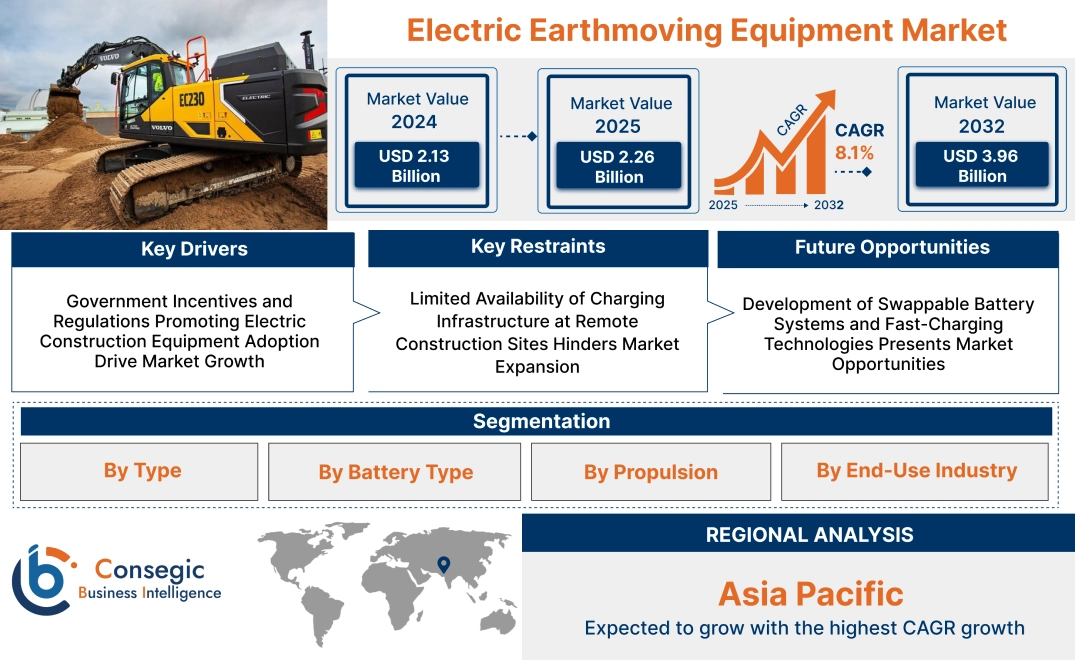

Electric Earthmoving Equipment Market Size:

Electric Earthmoving Equipment Market size is estimated to reach over USD 3.96 Billion by 2032 from a value of USD 2.13 Billion in 2024 and is projected to grow by USD 2.26 Billion in 2025, growing at a CAGR of 8.1% from 2025 to 2032.

Electric Earthmoving Equipment Market Scope & Overview:

Electric earthmoving equipment refers to battery-powered or hybrid machinery designed for excavation, grading, and material relocation in construction, mining, and utility projects. These machines encompass excavators, loaders, dozers, and dump trucks equipped with electric drivetrains and rechargeable power systems.

Reduced engine noise, zero on-site emissions, regenerative braking, and advanced control interfaces are common features included in the machinery. Additionally, many models now incorporate telematics, modular battery packs, and rapid charging capabilities to ensure continuous operation and easy integration into fleet workflows.

Electric earthmoving equipment offers operational benefits such as lower maintenance requirements, improved energy efficiency, and enhanced operator comfort. Their performance supports applications in urban areas, confined environments, and projects with strict environmental standards. The ability to match conventional equipment in functionality while delivering added sustainability makes these machines a strategic solution for modern construction and excavation tasks focused on efficiency, precision, and reduced environmental impact.

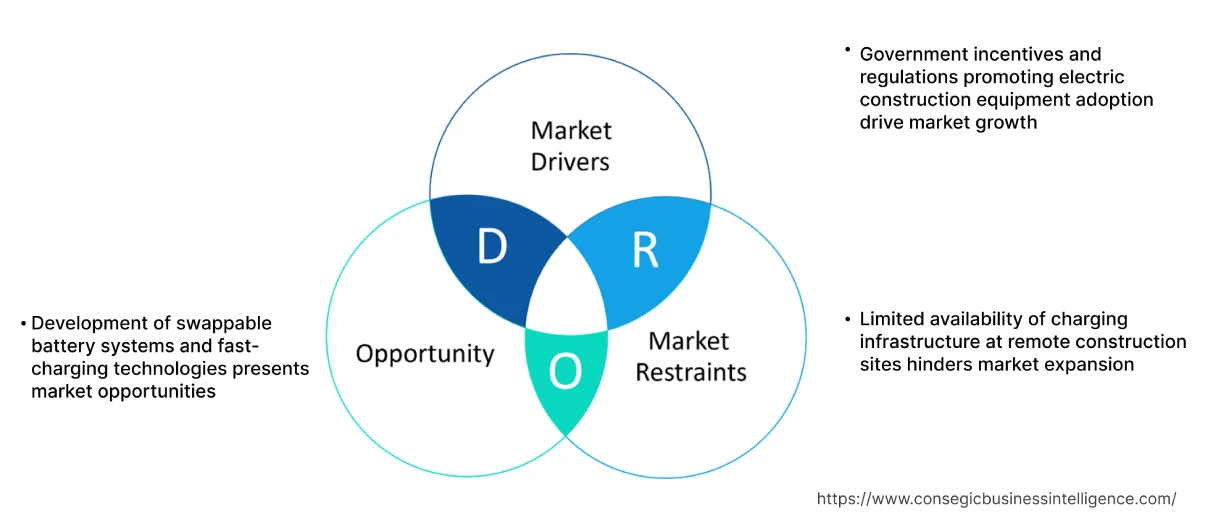

Electric Earthmoving Equipment Market Dynamics - (DRO) :

Key Drivers:

Lovernment incentives and regulations promoting electric construction equipment adoption drive market growth

Government bodies across the globe are actively supporting the transition to cleaner construction machinery through incentive programs, emissions regulations, and public procurement standards. Several countries in Europe and North America are offering grants, subsidies, and tax breaks to encourage contractors and fleet operators to replace diesel-powered machines with electric alternatives. Additionally, low-emission zones in urban centers are restricting the use of fossil-fuel-driven equipment on job sites, further accelerating adoption. Policies tied to climate action frameworks, such as the European Green Deal and California’s CARB regulations, are putting pressure on the construction industry to reduce its carbon footprint. As a result, large contractors, rental companies, and public infrastructure projects are increasingly adopting electric earthmoving solutions to comply with regulations and sustainability goals.

- For instance, in April 2022, Chile introduced legislation to achieve 100% zero-emission for sales of new equipment over 560 kW by 2035 and for new equipment between 19 kW and 560 kW by 2040.

With demand rising for environmentally aligned equipment, these policy measures are playing a crucial role in driving the electric earthmoving equipment market expansion.

Key Restraints:

Limited availability of charging infrastructure at remote construction sites hinders market expansion

One of the key challenges in deploying electric earthmoving equipment at scale is the lack of reliable charging infrastructure on remote or off-grid construction sites. Earthmoving operations often occur in undeveloped areas, infrastructure corridors, or mining zones where access to high-capacity electrical supply is limited or non-existent. Without dedicated charging setups or mobile energy stations, operators face downtime and project delays when recharging machines. Even in semi-urban locations, the absence of fast-charging options can disrupt multi-shift operations and reduce productivity. Smaller contractors and rural developers are especially affected due to limited resources for setting up temporary charging stations. Although demand for clean equipment is increasing, the infrastructure gap between urban and remote construction areas continues to create deployment bottlenecks, ultimately slowing electric earthmoving equipment market growth across challenging geographies.

Future Opportunities :

Development of swappable battery systems and fast-charging technologies presents market opportunities

To overcome runtime and charging limitations, manufacturers are shifting focus toward modular battery designs and high-speed charging systems tailored for earthmoving applications. Swappable battery packs allow operators to replace depleted units with charged ones in minutes, reducing downtime and enabling continuous operation during extended shifts. Fast-charging solutions are being integrated into jobsite energy hubs, enabling machines to top up quickly during scheduled breaks. These innovations are gaining traction among contractors seeking operational flexibility and energy efficiency. As demand grows for electric machinery that matches diesel in productivity, the emergence of smart battery management, thermal control systems, and energy-as-a-service platforms is reshaping fleet deployment strategies. Equipment makers are also collaborating with power solution providers to streamline charging workflows for large-scale sites.

- For instance, in April 2025, XCMG launched XE215EV, a new electric excavator providing zero-emission, low-noise, and energy-efficient operation, for the European market in 20-ton-class.

These technological advances are creating a new wave of electric earthmoving equipment market opportunities centered on scalable performance, runtime optimization, and jobsite adaptability.

Electric Earthmoving Equipment Market Segmental Analysis :

By Type:

Based on type, the market is segmented into excavators, loaders, bulldozers, dump trucks, motor graders, and others.

The excavators segment accounted for the largest electric earthmoving equipment market share in 2024.

- Electric excavators offer high efficiency and precision in digging, lifting, and moving heavy materials, making them ideal for construction and mining projects.

- Their adoption is growing due to the increasing need for sustainable machinery in urban construction, where reduced emissions and noise are a priority.

- With advancements in battery technology, electric excavators provide improved operational times and reduced energy costs.

- For instance, in May 2024, Volvo CE unveiled the EC230 Electric, Asia's first 20-ton mid-size excavator in Japan. The battery-powered, medium-sized hydraulic excavator has an operating machine weight of 23,000 to 26,100 kg, a bucket capacity of 0.48 to 1.44 m³, and a lifting capacity of 7,560 kg. Its battery capacity is 264 kWh and an operating time of 5 hours.

- As per the electric earthmoving equipment market analysis, the excavator segment remains dominant due to its widespread use in heavy construction and large-scale civil projects.

The dump truck segment is projected to witness the fastest CAGR during the forecast period.

- Electric dump trucks are gaining popularity due to their large capacity for transporting heavy loads with reduced environmental impact.

- These trucks are particularly useful in mining, construction, and logistics, where the efficient transportation of materials is critical.

- Battery-powered dump trucks are being adopted in mining operations to reduce the carbon footprint of hauling operations.

- For instance, in April 2024, Sany India launched the SKT105E Electric Dump Truck, India’s first locally manufactured fully electric mining truck. With a payload capacity of 70 tonnes, it ensures energy efficiency and cost-effectiveness.

- According to electric earthmoving equipment market trends, the need for electric dump trucks is accelerating due to rising fuel costs and increasing regulatory pressures on emissions.

By Battery Type:

Based on battery type, the market is segmented into lithium-ion and lead-acid.

The lithium-ion segment held the largest revenue share in 2024.

- Lithium-ion batteries are widely preferred in electric earthmoving equipment due to their superior energy density, longer life span, and lighter weight compared to lead-acid batteries.

- They offer faster charging times and longer operational periods, which is essential for high-demand earthmoving operations.

- The development of fast-charging solutions for lithium-ion batteries is further boosting their adoption in the market.

- As per electric earthmoving equipment market analysis, lithium-ion batteries dominate due to their superior performance in heavy-duty equipment and longer return on investment.

The lead-acid segment is expected to experience fastest CAGR during the forecast period.

- Lead-acid batteries remain a cost-effective option for entry-level electric earthmoving equipment in low-budget markets or for lighter-duty tasks.

- These batteries are particularly useful in smaller equipment used for residential or landscaping projects where lower capacity and cost are key considerations.

- While lead-acid batteries have a shorter lifespan and lower energy efficiency than lithium-ion, their affordability ensures continued adoption in niche applications.

- As per electric earthmoving equipment market trends, the lead-acid segment still plays a crucial role in regions with lower upfront costs but is gradually being replaced by lithium-ion in more demanding applications.

By Propultion:

Based on propulsion, the market is segmented into battery-powered, plug-in hybrid, and hybrid.

The battery-powered segment accounted for the largest electric earthmoving equipment market share in 2024.

- Battery-powered electric earthmoving equipment operates entirely on electric power, reducing emissions, operational costs, and the environmental impact compared to fossil fuel-powered machines.

- These machines are becoming increasingly prevalent in urban environments and are ideal for environmentally-conscious construction and mining projects.

- The segment benefits from improvements in battery technology, such as higher energy density and faster charging capabilities.

- Thus, battery-powered machines remain the largest segment due to their ability to meet environmental regulations and offer long-term cost savings supporting the increasing electric earthmoving equipment market demand.

The hybrid segment is expected to grow at the fastest CAGR during the forecast period.

- Hybrid models combine electric propulsion with traditional fuel sources, offering the flexibility to switch between the two depending on the work environment.

- These machines are particularly attractive in large-scale projects where continuous operation is required, and recharging opportunities are limited.

- Hybrid systems allow for energy regeneration, providing additional efficiency, particularly in mining and construction applications where long operational hours are common.

- Hence, hybrid systems are growing in popularity as they combine the benefits of electric machines with the versatility of traditional fuel engines, bolstering electric earthmoving equipment market expansion.

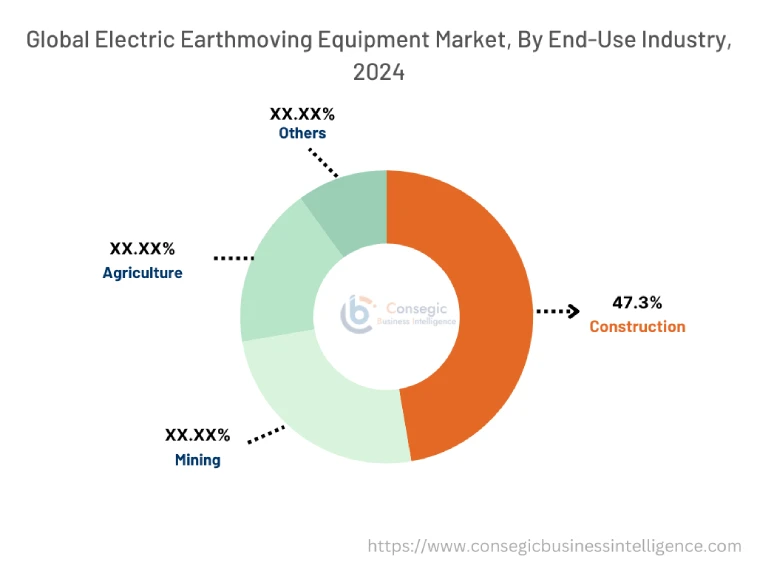

By End-Use Industry:

Based on end-use industry, the electric earthmoving equipment market is segmented into construction, mining, agriculture, and others.

The construction segment held the largest revenue share of 47.3% in 2024.

- Electric earthmoving equipment is heavily used in construction for tasks such as excavation, material handling, and grading.

- The need for eco-friendly and energy-efficient machines in urban construction projects is rising, driving the adoption of electric machinery.

- The construction sector’s focus on sustainability, noise reduction, and reducing its carbon footprint is propelling the requirement.

- As per electric earthmoving equipment market demand, the construction sector is the primary driver of the market, with significant investments in green building technologies.

The mining segment is projected to witness the fastest CAGR during the forecast period.

- Mining companies are increasingly adopting electric earthmoving equipment to reduce fuel costs and improve the sustainability of their operations.

- These machines are ideal for underground mining, where emissions and noise levels need to be minimized for worker safety.

- With the growing emphasis on reducing environmental impacts and improving operational efficiency in mining, the adoption of electric systems is accelerating.

- Thus, the mining sector is expected to lead the electric earthmoving equipment market growth, driven by sustainability goals and the need for more cost-effective operations.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

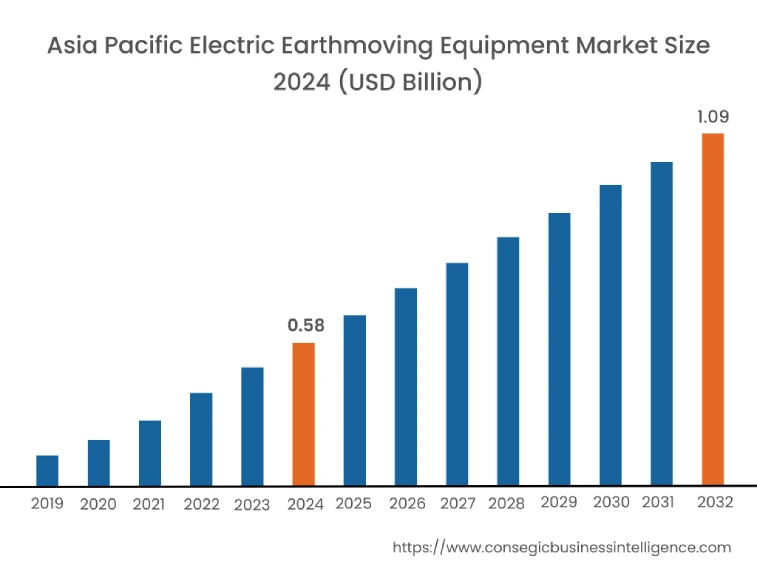

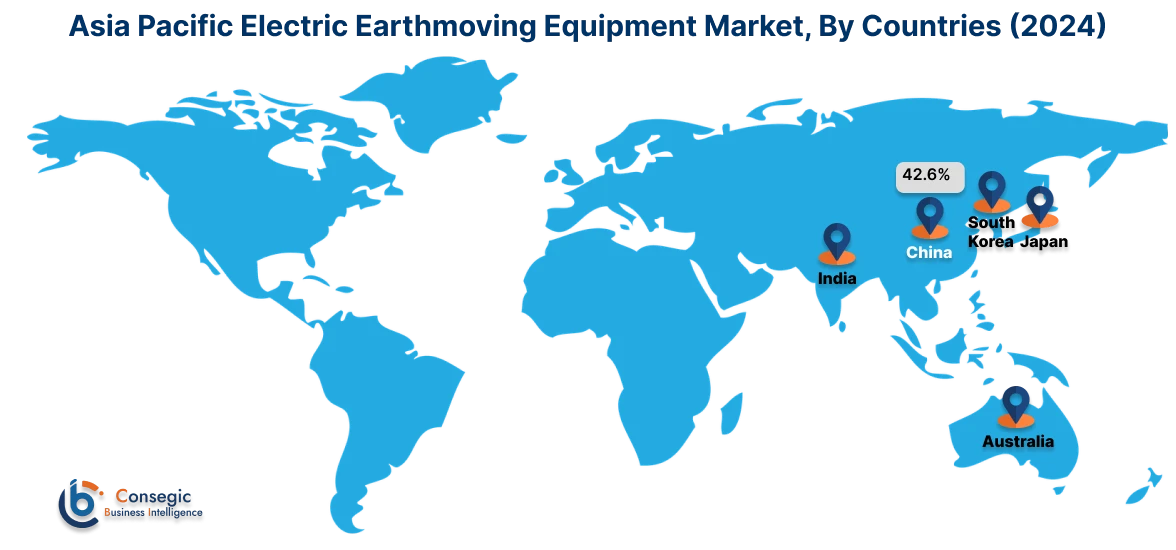

Asia Pacific region was valued at USD 0.58 Billion in 2024. Moreover, it is projected to grow by USD 0.61 Billion in 2025 and reach over USD 1.09 Billion by 2032. Out of this, China accounted for the maximum revenue share of 42.6%. Asia-Pacific is emerging as a fast-growing region in the electric earthmoving equipment industry, driven by large-scale construction activity, increasing urban density, and environmental compliance frameworks. In China, the government mandates are promoting clean energy alternatives in construction zones, particularly in high-pollution urban areas. Japan and South Korea are investing in advanced electric machinery with automated controls and fast-charging capabilities. Market analysis shows that India and Australia are in early phases, with growing interest among infrastructure developers and EPC contractors. Regional growth is underpinned by advancements in battery manufacturing, support for green building certifications, and the rise of smart city infrastructure.

North America is estimated to reach over USD 1.17 Billion by 2032 from a value of USD 0.63 Billion in 2024 and is projected to grow by USD 0.67 Billion in 2025. In North America, adoption is steadily increasing due to infrastructure investment plans and growing environmental pressure on the construction sector. The United States and Canada are witnessing integration of electric excavators, loaders, and compact track machines across urban construction, utility maintenance, and landscaping projects. Market analysis highlights that rental companies and municipal contractors are adopting electric models to comply with zero-emission targets and reduce long-term operational costs. Growth in this region is supported by state-level clean energy incentives and pilot programs that encourage deployment of battery-powered equipment on government-led infrastructure projects.

Europe leads in policy-driven adoption of electric earthmoving solutions, where construction firms are aligning with stringent emissions legislation and urban noise restrictions. Countries such as Norway, the Netherlands, Germany, and France are deploying electric equipment for roadworks, tunneling, and residential development in noise-sensitive and low-emission zones. Market analysis indicates high requirement for compact and mid-size electric machinery with telematics, regenerative braking, and modular battery systems. Incentives under EU Green Deal initiatives, public-private partnerships, and accelerated timelines to phase out diesel machines on urban job sites support market development.

Latin America is gradually exploring electric earthmoving solutions, especially in Brazil, Mexico, and Chile, where urban development and infrastructure renewal projects are gaining pace. Market analysis suggests that while diesel equipment still dominates, government-backed green initiatives and interest in reducing fuel dependency are prompting interest in electrified fleets. Construction firms are testing compact electric loaders and excavators in city projects and enclosed environments such as tunnels and subways. The electric earthmoving equipment market opportunity here lies in facilitating access to affordable electric models and strengthening local technical support for maintenance and charging logistics.

The Middle East and Africa are slowly progressing toward electric earthmoving adoption, particularly in the UAE, Saudi Arabia, and South Africa. The focus in these markets is on sustainable urban development, logistics infrastructure, and energy-efficient construction in temperature-sensitive zones. Market analysis reveals that hybrid and electric machines are being trialed in flagship developments and smart city projects where noise control and emissions compliance are essential. Although diesel remains the dominant powertrain, long-term growth is expected through sustainability-focused procurement policies, investment in renewable energy-powered charging networks, and greater awareness of total cost-of-ownership advantages.

Top Key Players and Market Share Insights:

The electric earthmoving equipment market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global electric earthmoving equipment market. Key players in the electric earthmoving equipment industry include –

- Komatsu Ltd. (Japan)

- Volvo Construction Equipment (Sweden)

- XCMG Group (China)

- Hitachi Construction Machinery Co., Ltd. (Japan)

- Caterpillar Inc. (USA)

- CNH Industrial N.V. (CASE Construction) (United Kingdom)

- Doosan Infracore (South Korea)

- Hyundai Construction Equipment Co., Ltd. (South Korea)

- JCB Ltd. (United Kingdom)

- SANY Group (China)

Recent Industry Developments :

Acquisitions:

- In February 2025, Cummins acquired the assets of First Mode, a leader in retrofit hybrid solutions for mining and rail operations. This includes hybrid mining, rail product lines and hydrogen and battery powertrain solutions. Furthermore, Cummins has also gained First Mode’s commercial portfolio, manufacturing and technical teams in Australia, the United States and Chile.

Partnerships:

- In October 2024, Chinese heavy equipment manufacturer SANY partnered with the service provider Alltrucks to ensure customers in Europe a comprehensive service for electric trucks.

Electric Earthmoving Equipment Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 3.96 Billion |

| CAGR (2025-2032) | 8.1% |

| By Type |

|

| By Battery Type |

|

| By Propulsion |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Electric Earthmoving Equipment Market? +

Electric Earthmoving Equipment Market size is estimated to reach over USD 3.96 Billion by 2032 from a value of USD 2.13 Billion in 2024 and is projected to grow by USD 2.26 Billion in 2025, growing at a CAGR of 8.1% from 2025 to 2032.

What specific segmentation details are covered in the Electric Earthmoving Equipment Market report? +

The Electric Earthmoving Equipment market report includes specific segmentation details for type, battery type, propulsion and end-use industry.

What are the end-use industries of the Electric Earthmoving Equipment Market?` +

The end-use industries of the Electric Earthmoving Equipment Market are construction, mining, agriculture, and others.

Who are the major players in the Electric Earthmoving Equipment Market? +

The key participants in the Electric Earthmoving Equipment market are Komatsu Ltd. (Japan), Volvo Construction Equipment (Sweden), XCMG Group (China), Hitachi Construction Machinery Co., Ltd. (Japan), Caterpillar Inc. (USA), CNH Industrial N.V. (CASE Construction) (United Kingdom), Doosan Infracore (South Korea), Hyundai Construction Equipment Co., Ltd. (South Korea), JCB Ltd. (United Kingdom) and SANY Group (China).