- Summary

- Table Of Content

- Methodology

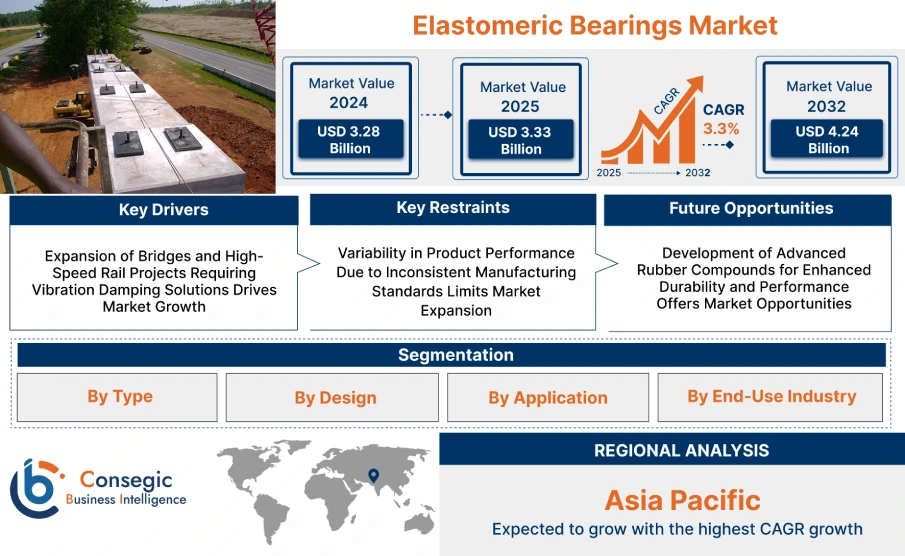

Elastomeric Bearings Market Size:

Elastomeric Bearings Market size is estimated to reach over USD Billion by 2032 from a value of USD 3.28 Billion in 2024 and is projected to grow by USD 3.33 Billion in 2025, growing at a CAGR of 3.3% from 2025 to 2032.

Elastomeric Bearings Market Scope & Overview:

Elastomeric bearings are flexible structural components designed to accommodate movements and distribute loads between bridge decks or building structures and their supports. Constructed from natural or synthetic rubber bonded with steel laminates, these bearings absorb vibrations, rotational forces, and horizontal displacements caused by thermal expansion, seismic activity, or live loads.

They are commonly used in bridge construction, elevated highways, and multi-story buildings to enhance stability and structural longevity. Key features include high load-bearing capacity, resistance to environmental degradation, and maintenance-free performance over extended periods.

They ensure smooth load transfer, reduce stress concentrations, and enhance durability in dynamic structures. Their ability to withstand variable conditions, including temperature fluctuations and moisture, makes them essential for infrastructure subjected to continual movement. These components support efficient design while improving overall structural safety and reliability in both new construction and retrofitting projects.

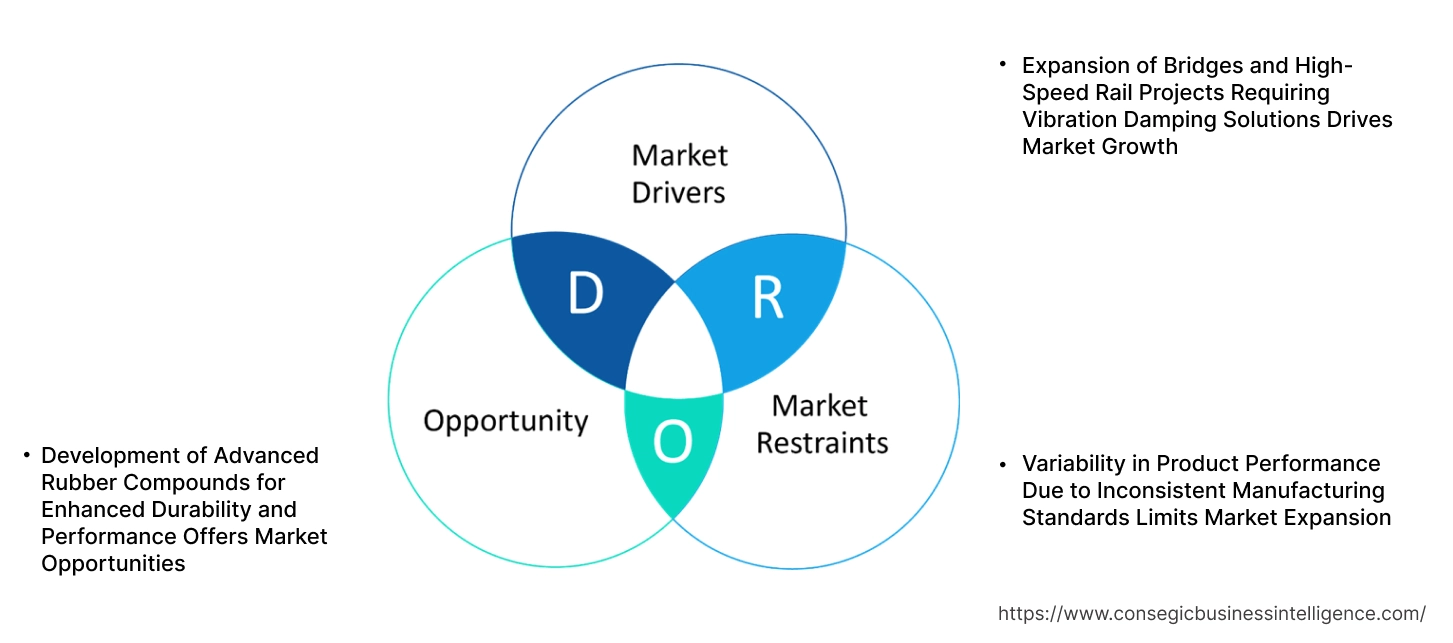

Elastomeric Bearings Market Dynamics - (DRO) :

Key Drivers:

Expansion of Bridges and High-Speed Rail Projects Requiring Vibration Damping Solutions Drives Market Growth

Global investment in transportation infrastructure—particularly in bridges, viaducts, and high-speed rail networks—is increasing the deployment of vibration-damping systems that ensure structural stability and long-term durability. Elastomeric bearings play a critical role in absorbing loads, accommodating thermal expansion, and minimizing vibration transmission between superstructures and substructures. As governments focus on upgrading regional connectivity and reducing travel times, demand for long-span and elevated infrastructure is rising. High-speed rail systems and modern highway bridges require high-performance products to manage the dynamic forces generated by fast-moving loads and variable environmental conditions. The durability and maintenance-free nature of these bearings make them a preferred solution for such applications.

- For instance, in April 2025, the 7th Open Web Girder (OWG) bridge was launched over the two Dedicated Freight Corridor tracks in Gujarat, India, as part of the Mumbai-Ahmedabad Bullet Train Project (MAHSR). Fabricated in Kolkata and subsequently transported to the site, the steel bridge weighs 674 metric tons, measures 13 meters in height and 14 meters in width. 28800 units of Tor-Shear Type High Strength (TTHS) bolts, subjected to C5 system painting, and elastomeric bearings were also used in the design.

With new bridge corridors and rail expansion projects underway globally, the need for high-load, fatigue-resistant bearings continues to rise, supporting long-term elastomeric bearings market expansion.

Key Restraints:

Variability in Product Performance Due to Inconsistent Manufacturing Standards Limits Market Expansion

Performance of elastomeric bearings is heavily dependent on precise material formulation, layer thickness, bonding integrity, and curing processes. Inconsistencies in manufacturing practices, especially among low-cost regional producers, lead to significant variation in product reliability and durability. Bearings produced without adherence to international standards often experience premature failure, excessive creep, or inadequate load distribution, compromising structural safety. This variability forces engineers to over-specify products or invest in frequent inspection and maintenance, increasing project costs. Contractors and infrastructure developers in many countries remain cautious when selecting elastomeric bearing suppliers due to limited quality assurance in parts of the global supply chain. These concerns hinder market penetration in large-scale infrastructure projects where long-term performance and certification are non-negotiable. Despite growing demand for vibration control systems, the lack of standardized manufacturing benchmarks continues to impede consistent product performance, ultimately restraining the elastomeric bearings market growth.

Future Opportunities :

Development of Advanced Rubber Compounds for Enhanced Durability and Performance Offers Market Opportunities

Material innovation is reshaping the elastomeric bearings industry, with manufacturers investing in advanced rubber compounds that deliver improved resistance to UV radiation, ozone exposure, extreme temperatures, and high-cycle fatigue. New formulations such as chloroprene and EPDM blends enhance elasticity retention and chemical stability over extended service life. These upgrades are particularly beneficial in coastal bridges, high-altitude railways, and industrial settings where bearings are exposed to harsh environmental conditions. Additionally, advancements in bonding agents and steel reinforcement integration improve structural cohesion and shear performance. The demand for maintenance-free, long-lifespan products is increasing as governments prioritize resilient infrastructure that reduces lifecycle costs. As infrastructure owners seek longer inspection intervals and better ROI on component investments, these material enhancements are driving product differentiation.

- For instance, in March 2021, researchers at the University of Science and Technology of China investigated the self-healing properties of elastomers based on multiple hydrogen bonds. Such materials find potential applications in the field of wearable electronics, electronic skins, motion tracking, and health monitoring.

The shift toward performance-optimized elastomers is opening promising elastomeric bearings market opportunities fueled by technological growth and evolving engineering requirements.

Elastomeric Bearings Market Segmental Analysis :

By Type:

Based on type, the market is segmented into natural rubber bearings, synthetic rubber bearings, and others.

The natural rubber bearings segment accounted for the largest revenue share in 2024.

- Natural rubber bearings are widely used due to their excellent damping properties and ability to provide a stable foundation for heavy structures.

- These bearings are highly durable, resilient to wear and tear, and provide superior shock absorption, making them ideal for applications in bridges, highways, and buildings.

- Their affordability and superior flexibility compared to synthetic rubbers make them a preferred choice in a wide range of infrastructure projects.

- As per the elastomeric bearings market analysis, natural rubber bearings continue to lead due to their widespread use in traditional infrastructure projects, particularly in high-traffic and high-load areas.

The synthetic rubber bearings segment is projected to grow at the fastest CAGR during the forecast period.

- Synthetic rubber bearings are increasingly used for their enhanced performance characteristics, including better resistance to aging, oils, and temperature extremes.

- These bearings are preferred in more demanding environments such as oil & gas infrastructure and power generation plants.

- The segment's growth is driven by the demand for advanced materials that offer improved durability and performance under harsh conditions.

- According to the elastomeric bearings market trends, the shift towards synthetic rubber bearings is accelerating due to the need for more specialized applications in industrial sectors.

By Design:

Based on design, the market is segmented into flat bearings, cylindrical bearings, laminated bearings, and others.

The laminated bearings segment held the largest elastomeric bearings market share in 2024.

- Laminated bearings are made from multiple layers of rubber and steel, offering high-load capacity and excellent flexibility, making them suitable for large infrastructure projects like bridges and viaducts.

- These bearings provide superior load distribution and seismic protection, which is crucial in areas with high seismic activity.

- The increasing use of laminated bearings in complex construction projects that require superior load-bearing capacity and shock absorption is driving segment dominance.

- For instance, the laminated bearings, Series EL, of Canam-Bridges are made of high-quality natural rubber or neoprene with vulcanized steel plates for application in bridges, viaducts and buildings for protection from seismic vibrations. It sustains a load of 7MPa with movement of up to 70mm.

- As per the elastomeric bearings market demand, laminated bearings remain dominant due to their high performance and ability to withstand dynamic forces in large civil engineering projects.

The flat bearings segment is expected to grow at the fastest CAGR during the forecast period.

- Flat bearings are used in applications where uniform load distribution and minimal space are important.

- These bearings are widely used in buildings, highways, and storage tanks, offering ease of installation and maintenance.

- The segment benefits from the need for simple yet effective bearing solutions in residential and small commercial construction projects.

- According to elastomeric bearings market trends, the demand for flat bearings is growing due to their simplicity, cost-effectiveness, and performance in less demanding applications.

By Application:

Based on application, the market is segmented into bridges, buildings, highways, railways, viaducts, storage tanks, and others.

The bridges segment accounted for the largest revenue share in 2024.

- They are widely used in bridge construction to provide stability and flexibility, allowing the structure to withstand vibrations, temperature changes, and seismic forces.

- Their role in isolating the structural elements from the ground motion makes them essential for ensuring bridge longevity and safety.

- As infrastructure development accelerates globally, especially in regions with aging infrastructure, their requirement in bridge projects is rising.

- As per elastomeric bearings market analysis, the bridge application segment remains the dominant force due to the growing number of public and private investments in bridge construction and retrofitting.

The building segment is projected to grow at the fastest CAGR during the forecast period.

- Elastomeric bearings in buildings are essential for reducing vibrations, minimizing settlement issues, and enhancing the overall structural integrity.

- With the rise of tall buildings, urban infrastructure, and residential projects in seismic zones, they have become increasingly important for maintaining the safety and longevity of buildings.

- The increasing focus on earthquake-resistant construction in areas prone to seismic activity is driving the need.

- According to segmental trends, the building sector is boosting the elastomeric bearings market growth as more urban projects prioritize seismic protection and vibration control.

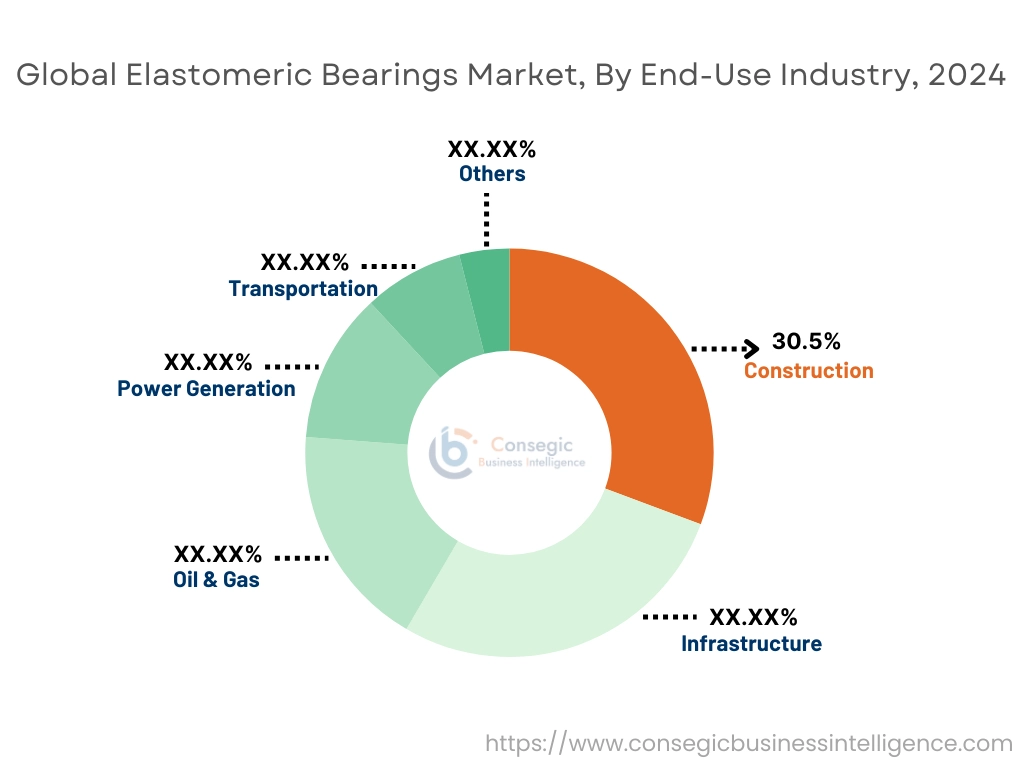

By End-Use Industry:

Based on end-use industry, the market is segmented into construction, infrastructure, oil & gas, power generation, transportation, and others.

The construction segment held the largest elastomeric bearings market share of 30.5% in 2024.

- Elastomeric bearings are widely used in various construction applications, including residential, commercial, and industrial buildings, to provide stability, shock absorption, and vibration control.

- The segment benefits from the increasing global need for modern infrastructure, urbanization, and residential development projects.

- Its use in buildings and infrastructure is growing as more projects aim to meet seismic standards and reduce operational risks.

- Thus, the construction industry remains the largest segment, driven by the growth of housing, commercial properties, and infrastructure projects globally and supporting the elastomeric bearings market demand.

The infrastructure segment is projected to experience the fastest CAGR during the forecast period.

- Infrastructure projects, such as bridges, tunnels, and viaducts, are increasingly adopting them to ensure seismic resilience and stability.

- The need for sustainable and durable infrastructure in regions with heavy traffic or seismic activity is pushing the adoption of advanced bearing technologies.

- Infrastructure investments in both emerging and developed economies are creating significant requirements.

- According to the segmental trends, the infrastructure sector is bolstering the elastomeric bearings market expansion due to increasing urban development and infrastructure renovation projects.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

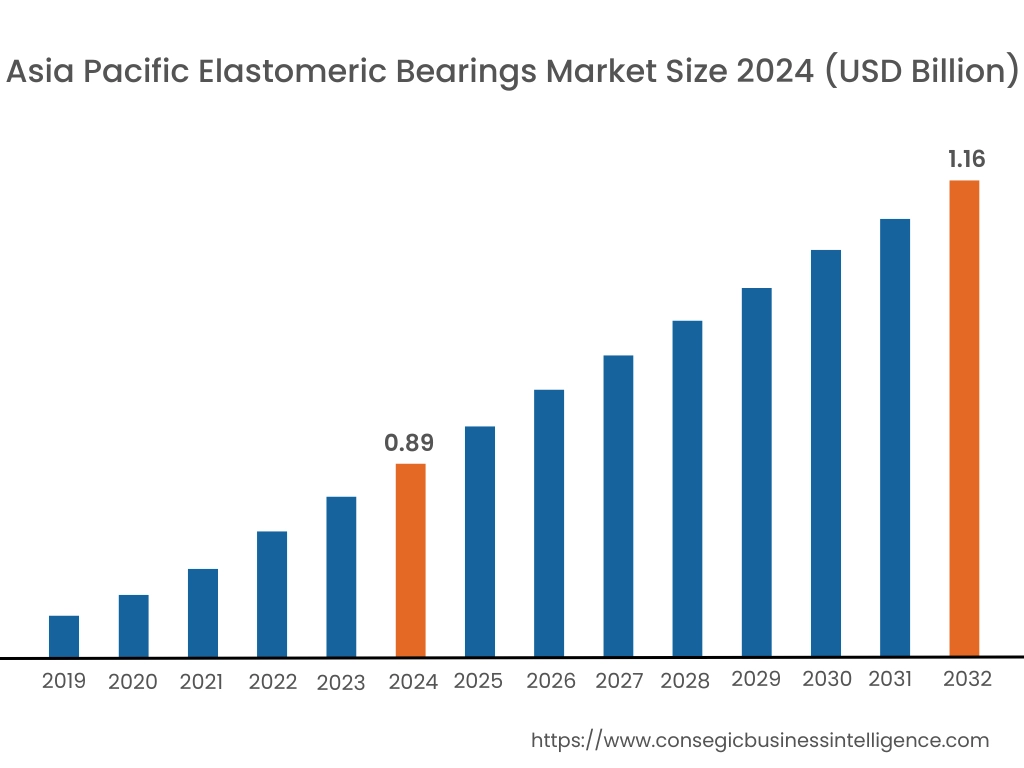

Asia Pacific region was valued at USD 0.89 Billion in 2024. Moreover, it is projected to grow by USD 0.90 Billion in 2025 and reach over USD 1.16 Billion by 2032. Out of this, China accounted for the maximum revenue share of 50.3%. Asia-Pacific is witnessing rapid growth in the elastomeric bearings industry due to large-scale highway and railway development, seismic vulnerability, and government-led urban infrastructure initiatives. In countries like China, India, Japan, and South Korea, these components are widely deployed in bridge superstructures, metro lines, and high-rise foundations. Market analysis highlights the use of advanced manufacturing techniques for bearings that meet region-specific seismic, thermal, and dynamic load requirements. Growth is bolstered by domestic production capabilities and public infrastructure investments under programs such as China’s Belt and Road Initiative and India’s Smart Cities Mission, both of which require long-lasting, low-maintenance structural support systems.

North America is estimated to reach over USD 1.41 Billion by 2032 from a value of USD 1.09 Billion in 2024 and is projected to grow by USD 1.11 Billion in 2025. In North America, the requirement is driven by aging bridge infrastructure, seismic safety retrofits, and modular construction techniques. Market analysis shows that the United States and Canada are adopting high-performance neoprene and natural rubber bearings for highway overpasses, rail infrastructure, and large-scale building foundations. Public infrastructure renewal programs, especially those focused on bridge rehabilitation, are fueling steady growth. Additionally, adherence to AASHTO standards and its integration into seismic mitigation designs contribute to increasing utilization. The region also emphasizes lifecycle cost benefits, prompting widespread use in both new construction and retrofit applications.

Europe maintains a highly standardized market, with adoption aligned with stringent Eurocode requirements. Countries such as Germany, France, and Italy are utilizing these components extensively in civil infrastructure, particularly in bridge expansion joints and precast concrete segments. Market analysis indicates growing emphasis on material certification, aging resistance, and temperature tolerance due to diverse climatic conditions. The elastomeric bearings market opportunity in Europe is further strengthened by investments in cross-border transport corridors and green infrastructure projects. Additionally, sustainability-focused designs promote the use of recyclable and long-lasting bearing materials in modern engineering applications.

In Latin America, elastomeric bearings are gaining traction in response to bridge expansions, transport modernization efforts, and increased focus on structural safety. Brazil, Mexico, and Chile are the region’s primary adopters, particularly in highway viaducts and seismic-prone structures. Market analysis indicates growing adoption in both public and private sector infrastructure, with design preferences shifting toward maintenance-free bearings that withstand moisture and load variation. The region is also gradually incorporating international design standards to improve bearing performance. The market opportunity in Latin America is enhanced by planned investments in transportation corridors and improved structural design frameworks.

The Middle East and Africa represent an emerging elastomeric bearings market, with activity concentrated in the UAE, Saudi Arabia, and South Africa. The focus in these regions is on large-scale infrastructure developments, such as elevated roadways, rail viaducts, and airport linkages. Market analysis shows increasing interest in high-load, heat-resistant elastomeric products that can operate effectively in arid climates. In Africa, donor-funded infrastructure programs are beginning to specify their use in bridges and public works to ensure resilience and ease of installation. Growth is expected to continue as regional infrastructure standards evolve and the need for cost-effective, durable bridge components expands.

Top Key Players and Market Share Insights:

The elastomeric bearings market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global elastomeric bearings market. Key players in the elastomeric bearings industry include-

- Trelleborg AB (Sweden)

- Bridgestone Corporation (Japan)

- Freyssinet SAS (France)

- Maurer SE (Germany)

- Granor Rubber & Engineering Pty Ltd. (Australia)

- DS Brown Company (USA)

- Kantaflex Private Limited (India)

- Toyo Tire Corporation (Japan)

- Zaoqiang Dacheng Rubber Co., Ltd. (China)

- GUMBA GmbH & Co. KG (Germany)

Recent Industry Developments :

Acquisitions:

- In November 2021, the leading global manufacturer and marketer of precision bearings, RBC Bearings, completed the acquisition of ABB’s DODGE mechanical power transmission business.

Elastomeric Bearings Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 4.24 Billion |

| CAGR (2025-2032) | 3.3% |

| By Type |

|

| By Design |

|

| By Application |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Elastomeric Bearings Market? +

Elastomeric Bearings Market size is estimated to reach over USD 4.24 Billion by 2032 from a value of USD 3.28 Billion in 2024 and is projected to grow by USD 3.33 Billion in 2025, growing at a CAGR of 3.3% from 2025 to 2032.

What specific segmentation details are covered in the Elastomeric Bearings Market report? +

The Elastomeric Bearings market report includes specific segmentation details for type, design, application and end-use industry.

What are the end-use industries of the Elastomeric Bearings Market? +

The end-use industries of the Elastomeric Bearings Market are construction, infrastructure, oil & gas, power generation, transportation, and others.

Who are the major players in the Elastomeric Bearings Market? +

The key participants in the Elastomeric Bearings market are Trelleborg AB (Sweden), Bridgestone Corporation (Japan), Freyssinet SAS (France), Maurer SE (Germany), Granor Rubber & Engineering Pty Ltd. (Australia), DS Brown Company (USA), Kantaflex Private Limited (India), Toyo Tire Corporation (Japan), Zaoqiang Dacheng Rubber Co., Ltd. (China) and GUMBA GmbH & Co. KG (Germany).