- Summary

- Table Of Content

- Methodology

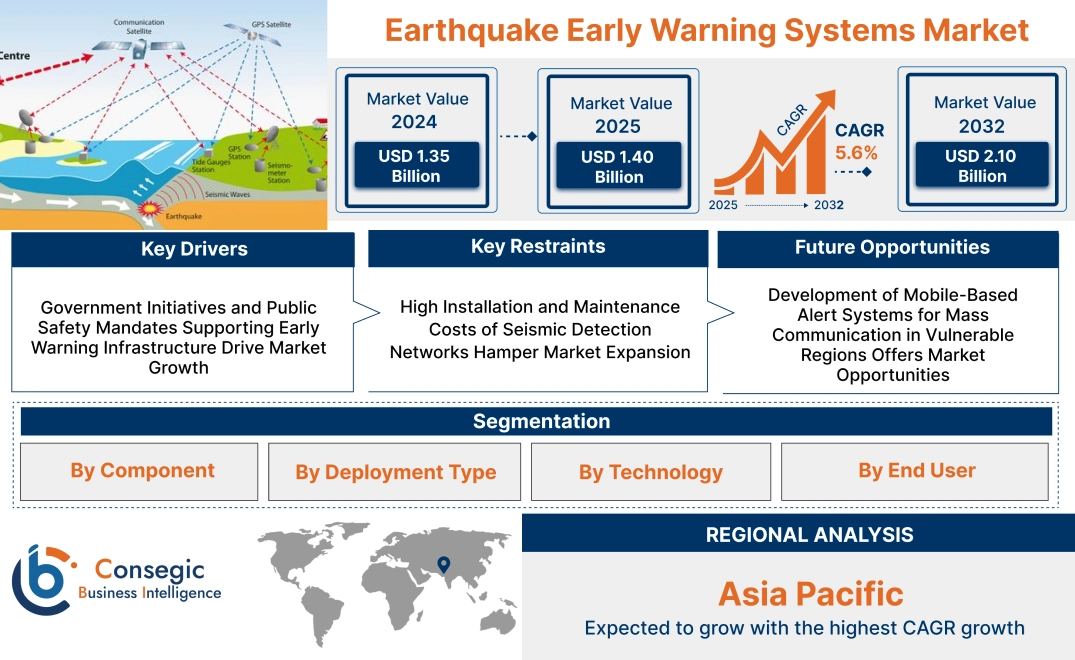

Earthquake Early Warning Systems Market Size:

Earthquake Early Warning Systems Market size is estimated to reach over USD 2.10 Billion by 2032 from a value of USD 1.35 Billion in 2024 and is projected to grow by USD 1.40 Billion in 2025, growing at a CAGR of 5.6% from 2025 to 2032.

Earthquake Early Warning Systems Market Scope & Overview:

Earthquake early warning systems are integrated networks designed to detect initial seismic waves and transmit alerts before destructive ground shaking occurs. These systems rely on a combination of ground-based sensors, GPS, and data processing algorithms to analyze seismic activity in real time and issue notifications within seconds.

Core components include seismometers, accelerometers, communication infrastructure, and control software capable of delivering alerts to emergency services, public infrastructure, and end users through automated channels.

The key benefits of earthquake early warning systems include improved response time, reduced infrastructure damage, and enhanced public safety. By providing a brief but crucial window for automated shutdowns, evacuation protocols, and protective actions, these systems support risk mitigation in vulnerable regions. Their application spans government agencies, transportation networks, utility providers, and high-risk industrial operations, offering a critical layer of preparedness in comprehensive disaster management strategies.

Earthquake Early Warning Systems Market Dynamics - (DRO) :

Key Drivers:

Government Initiatives and Public Safety Mandates Supporting Early Warning Infrastructure Drive Market Growth

Governments across seismic-prone countries are prioritizing public safety by deploying earthquake early warning systems that alert populations seconds before tremors occur. Agencies in Japan, Mexico, the United States, and parts of Europe are investing in dense seismic sensor networks and integrated alert platforms to minimize casualties and infrastructure damage. These efforts are often supported by national disaster management policies and emergency preparedness mandates. Public and private partnerships are further accelerating deployment in schools, hospitals, transport hubs, and industrial facilities. With growing awareness of the risks posed by seismic activity, authorities are expanding infrastructure to enhance readiness and resilience.

- For instance, in November 2024, China announced its plan to launch three FengYun geostationary satellites for high-frequency disaster monitoring in African, Asian and Pacific countries as well as share its cloud-based early warning system with other countries.

As the focus on community safety and disaster response continues to rise globally, demand for efficient and reliable alert mechanisms is increasing, driving consistent earthquake early warning systems market expansion.

Key Restraints:

High Installation and Maintenance Costs of Seismic Detection Networks Hamper Market Expansion

Deploying a functional early warning system requires the installation of hundreds or even thousands of seismic sensors, backed by robust communication and computing infrastructure. These costs are especially burdensome in developing countries or in geologically complex areas requiring dense sensor coverage. Ongoing maintenance, calibration, and data processing expenses further add to operational challenges, making it difficult for regional governments and local agencies to sustain the system without significant financial support. The need for redundancy, real-time data transmission, and integration with communication platforms makes the initial setup capital-intensive. In rural or mountainous zones, logistical difficulties also raise installation timelines and cost. Although demand for earthquake preparedness solutions is rising, these high investment requirements continue to slow widespread deployment, ultimately restraining earthquake early warning systems market growth across resource-constrained regions.

Future Opportunities :

Development of Mobile-Based Alert Systems for Mass Communication in Vulnerable Regions Offers Market Opportunities

Mobile alert systems are transforming how earthquake warnings are delivered to populations at risk. With smartphone penetration increasing globally, even in remote or economically challenged areas, mobile-based platforms offer a cost-effective solution for disseminating early warnings. By leveraging GPS, wireless networks, and app-based technologies, authorities can deliver real-time alerts customized by location and intensity. These systems complement sensor networks without requiring large physical infrastructure investments. Additionally, mobile alerts can be linked with school safety protocols, transportation shutdowns, and healthcare emergency responses. The demand for fast, targeted, and widely accessible warnings is growing, particularly in regions that lack dense seismic instrumentation but face high quake exposure.

- For instance, in December 2024, the California Governor’s Office of Emergency Services (Cal OES) and UC Berkeley Seismology Lab announced the new MyShake app for early earthquake notification is able for download on Chromebooks and MacOS. With more than 3.7 million downloads since its launch, the app provided up to 15 seconds of notice in the Humboldt earthquake and more than 10 seconds of notice in the Nevada earthquake. Additionally, recent updates of the app include the availability of audio messages for test and live alerts in six different languages, magnitude information, orientation expansion and user-informed background improvements.

As governments and tech developers collaborate on scalable communication frameworks, the mobile-first approach is opening significant earthquake early warning systems market opportunities driven by communication innovation and public safety growth.

Earthquake Early Warning Systems Market Segmental Analysis :

By Component:

Based on component, the market is segmented into hardware, software, and services.

The hardware segment accounted for the largest revenue share in 2024.

- Hardware components, including seismic sensors, accelerometers, and GPS units, are critical for the detection and monitoring of seismic activity.

- The installation and maintenance of these devices across strategic locations ensure real-time data collection and early detection.

- The integration of hardware systems with other safety infrastructure, such as alarms and automatic shutdown systems, is fueling requirement.

- For instance, in April 2025, STMicroelectronics launched IIS2DULPX, a new industrial-grade accelerometer with edge AI and low power for smart sensing. The accelerometer is capable of operating at high temperatures and ensuring smarter, data-driven operations and decision-making.

- As per the earthquake early warning systems market analysis, hardware remains the dominant segment due to its vital role in ensuring the effectiveness of early warning systems.

The software segment is projected to experience the fastest CAGR during the forecast period.

- Software enables real-time data processing and analysis of seismic information from various sensors, providing users with accurate and timely warnings.

- Key software features include user interfaces for displaying alerts, integrating with other safety systems, and predictive analytics for earthquake intensity estimation.

- Advanced algorithms and machine learning are incorporated into software for more accurate earthquake detection and predictions.

- According to earthquake early warning systems market trends, the software segment is experiencing steady growth due to advancements in data processing and predictive capabilities.

By Deployment Type:

Based on deployment type, the market is segmented into cloud-based systems and on-premises systems.

The cloud-based systems segment held the largest earthquake early warning systems market share in 2024.

- Cloud-based systems offer flexibility, scalability, and cost-effectiveness by enabling earthquake early warning solutions to be accessed remotely.

- These systems provide a centralized platform for data collection, analysis, and dissemination of warnings, reducing infrastructure and maintenance costs for users.

- The cloud infrastructure allows for the integration of other public safety systems, such as weather and traffic management systems, for a comprehensive safety framework.

- Thus, cloud-based solutions remain dominant due to their ease of deployment and the increasing adoption of cloud technology in public safety systems, driving the earthquake early warning systems market growth.

The on-premises systems segment is projected to witness the fastest CAGR during the forecast period.

- On-premises systems provide users with more control over their infrastructure, offering data privacy and security, which is essential in certain government and military applications.

- These systems are suitable for critical infrastructure that requires highly secure, localized control over earthquake data processing and alert generation.

- On-premises systems are typically preferred in regions with more stringent data security regulations.

- According to earthquake early warning systems market trends, the demand for on-premises solutions remains stable as government and industrial sectors prioritize data protection.

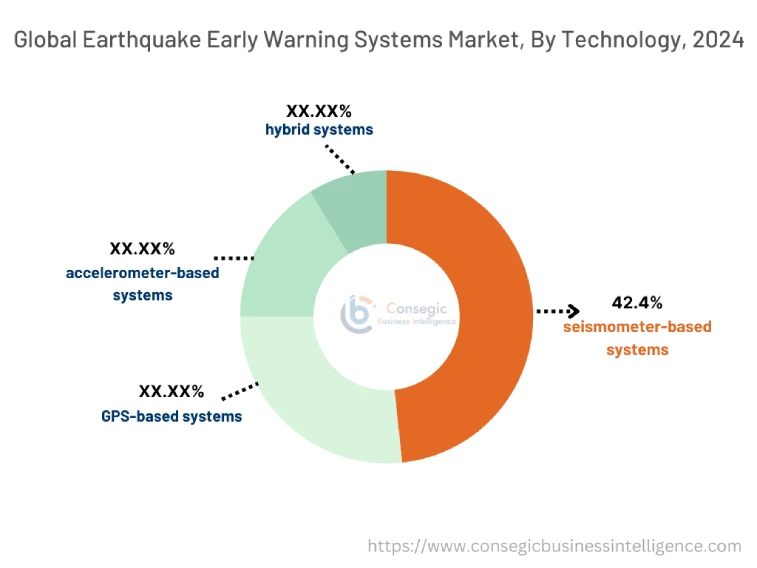

By Technology:

Based on technology, the market is segmented into seismometer-based systems, GPS-based systems, accelerometer-based systems, and hybrid systems.

The seismometer-based systems segment accounted for the largest revenue share of 42.4% in 2024.

- Seismometers are highly sensitive instruments used to measure ground motion and seismic waves, which are crucial for detecting and analyzing earthquakes in real time.

- These systems are commonly used in geological surveys, government monitoring networks, and research institutes.

- They provide high accuracy and are widely adopted in regions with frequent seismic activity, particularly in Japan, the U.S., and Latin America.

- As per earthquake early warning systems market demand, seismometer-based systems remain the most prevalent due to their accuracy and reliability in seismic detection.

The hybrid systems segment is projected to grow at the fastest CAGR during the forecast period.

- Hybrid systems combine the strengths of seismometers, GPS, and accelerometers to provide a more comprehensive and accurate earthquake early warning solution.

- These systems offer better detection capabilities, faster alert generation, and greater coverage across diverse geographical areas.

- With advancements in sensor technology and the integration of multiple sensing modalities, hybrid systems are becoming more attractive for real-time, large-scale monitoring.

- According to earthquake early warning systems market analysis, hybrid solutions are driving the market's growth due to their ability to provide a more robust and reliable warning system.

By End-Use Industry:

Based on the end-user, the market is segmented into electronics, healthcare, aerospace & defense, automotive, and others.

Trends in the End-User:

Based on end-use industry, the market is segmented into government, energy, transportation, healthcare, broadcast and telecommunication, construction, manufacturing, educational institutions, residential, and others.

The government segment held the largest earthquake early warning systems market share in 2024.

- Governments invest heavily in earthquake early warning systems to protect public safety, minimize infrastructure damage, and reduce casualties.

- These systems are deployed across seismic zones to monitor activity and provide timely alerts to citizens, businesses, and emergency services.

- The growing number of government initiatives and regulations mandating earthquake preparedness is driving the need for advanced warning systems.

- Thus, the government sector remains the largest user of these systems due to the critical need for public safety, bolstering earthquake early warning systems market expansion.

The energy segment is expected to experience the fastest CAGR.

- Energy production facilities, such as power plants and oil & gas refineries, are increasingly adopting earthquake early warning systems to protect critical infrastructure and personnel during seismic events.

- The adoption of such systems ensures the safety of operations, minimizes downtime, and protects expensive equipment from seismic damage.

- Increased investments in renewable energy projects in seismic regions are also boosting the requirement for these systems.

- Thus, the heavy investment of the energy sector in proactive risk management solutions to enhance the resilience of their operations propels the earthquake early warning systems market demand.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

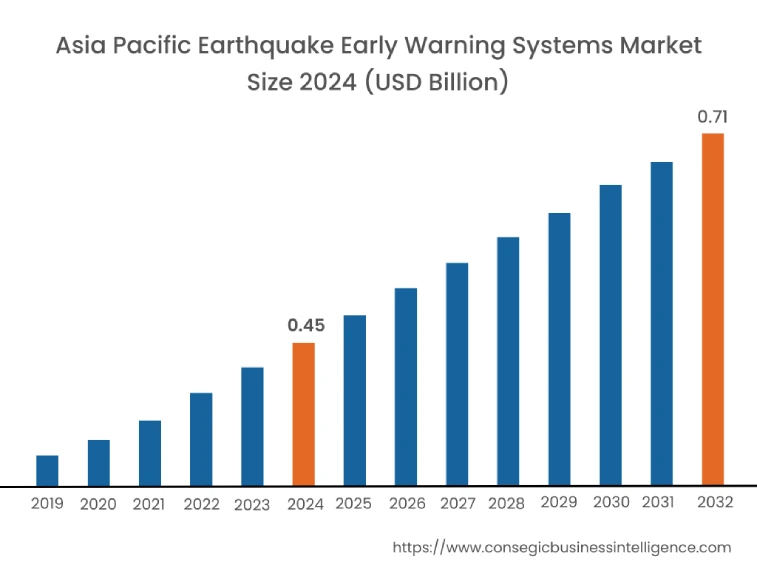

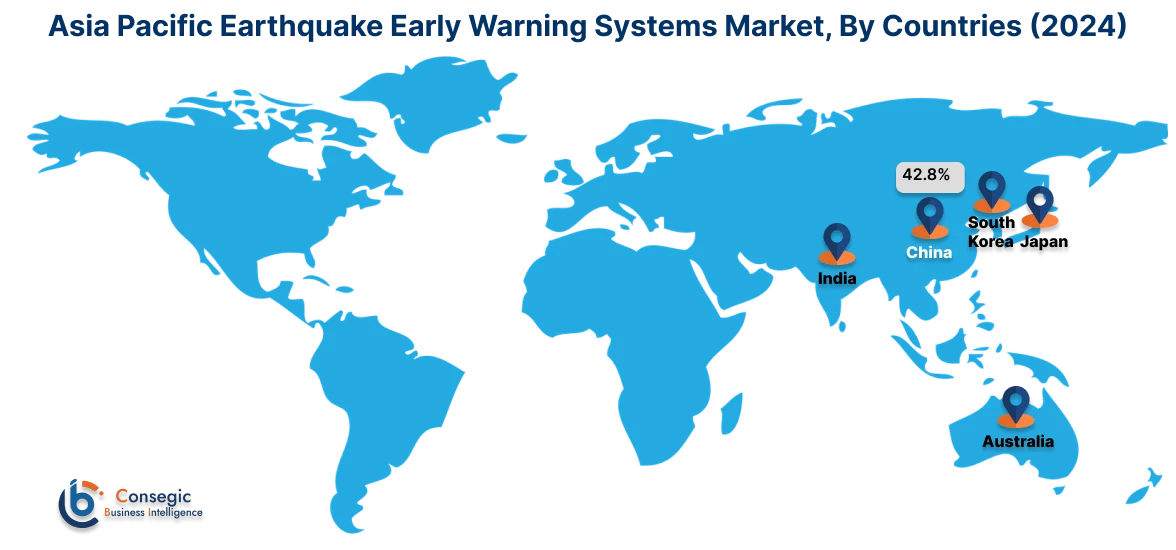

Asia Pacific region was valued at USD 0.45 Billion in 2024. Moreover, it is projected to grow by USD 0.47 Billion in 2025 and reach over USD 0.71 Billion by 2032. Out of this, China accounted for the maximum revenue share of 42.8%. Asia-Pacific is the most active and fastest-growing region in the earthquake early warning systems industry due to frequent seismic activity, high population density, and urban vulnerability. Countries such as Japan, China, Taiwan, and Indonesia have invested heavily in dense seismic networks and automated response protocols. Market analysis indicates a mature adoption in Japan, where early warnings are integrated into public broadcast systems and rail networks, while other nations are scaling their systems to protect schools, factories, and transportation corridors. Growth is further fueled by national resilience programs and public-private initiatives to enhance data collection, algorithm accuracy, and multi-channel dissemination. The region’s demand for rapid-response systems and real-time building automation continues to expand.

North America is estimated to reach over USD 0.62 Billion by 2032 from a value of USD 0.40 Billion in 2024 and is projected to grow by USD 0.41 Billion in 2025. North America represents a well-developed market, with significant infrastructure already in place, particularly along the western coast of the United States and Canada. Market analysis shows that seismic monitoring networks in California, Washington, and British Columbia are integrated with public alert systems, transportation networks, and utility infrastructure. Growth in this region is being driven by continued federal funding, academic collaboration, and the integration of alerts with smart devices and public safety platforms. The region’s earthquake-prone areas remain a focal point for ongoing upgrades in sensor density and data analytics capabilities to improve lead times and reduce false positives.

Europe is witnessing the steady adoption of early warning systems, especially in southern and eastern regions exposed to tectonic activity. Countries such as Italy, Greece, and Turkey are expanding sensor networks and real-time communication platforms for civil protection. Market analysis reveals an increasing emphasis on cross-border collaboration through EU-supported frameworks to standardize alerts and data-sharing protocols. Growth in this region is influenced by earthquake impacts on heritage cities and dense urban centers, driving requirement for early alerts that can protect rail, metro, and energy grid operations. The developments in the market are supported by the EU’s focus on multi-hazard risk management and funding mechanisms for resilient infrastructure.

Latin America is expanding its use of early warning technologies, particularly in countries like Mexico, Chile, and Peru, where major fault zones impact urban and coastal areas. Market analysis shows growing collaboration between government agencies, research institutions, and telecom providers to issue timely alerts to residents and first responders. While some systems are in early stages, investment is growing in upgrading regional networks with low-latency sensors and cloud-based alert platforms. The earthquake early warning systems market opportunity here lies in integrating alerts with emergency evacuation plans, retrofitted building infrastructure, and school safety systems across seismic zones.

The Middle East and Africa present an emerging market for early warning solutions, with initial deployments in Turkey, Iran, and parts of East Africa. Market analysis indicates that while overall sensor coverage remains limited, efforts are being made to monitor fault lines near population clusters and critical infrastructure. Regional initiatives are focusing on building national seismic observatories, improving public risk education, and integrating basic warning functions with telecom carriers. Long-term growth is expected through international partnerships and donor-backed projects aimed at improving disaster preparedness in vulnerable regions. As seismic data infrastructure improves, system interoperability and cloud-based analytics are expected to play a central role in scaling capabilities.

Top Key Players and Market Share Insights:

The earthquake early warning systems market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global earthquake early warning systems market. Key players in the earthquake early warning systems industry include-

- GeoSIG Ltd. (Switzerland)

- Tokyo Sokushin Co., Ltd. (Japan)

- Kinemetrics, Inc. (USA)

- Jenoptik AG (Germany)

- Nanometrics Inc. (Canada)

- Teledyne Geotech (USA)

- Guralp Systems Ltd. (United Kingdom)

- Trimble Inc. (USA)

- Hakusan Corporation (Japan)

- Swiss Seismological Service (SED) (Switzerland)

Recent Industry Developments :

Partnerships:

- In February 2024, Kinemetrics Inc. entered a strategic partnership with USGS to deliver the ShakeAlert®-powered earthquake early warning alerts via the OasisPlus Earthquake Response Platform. The platform combines smart sensing technology, real-time processing, and predictive computations to ensure effective emergency response. The warning provided enables the reduction of risk to human life and economic loss.

Earthquake Early Warning Systems Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 2.10 Billion |

| CAGR (2025-2032) | 5.6% |

| By Component |

|

| By Deployment Type |

|

| By Technology |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Earthquake Early Warning Systems Market? +

Earthquake Early Warning Systems Market size is estimated to reach over USD 2.10 Billion by 2032 from a value of USD 1.35 Billion in 2024 and is projected to grow by USD 1.40 Billion in 2025, growing at a CAGR of 5.6% from 2025 to 2032.

What specific segmentation details are covered in the Earthquake Early Warning Systems Market report? +

The Earthquake Early Warning Systems market report includes specific segmentation details for component, deployment type, technology and end-user.

Who are the end-users of the Earthquake Early Warning Systems Market? +

The end-user of the Earthquake Early Warning Systems Market are government, energy, transportation, healthcare, broadcast and telecommunication, construction, manufacturing, educational institutions, residential, and others.

Who are the major players in the Earthquake Early Warning Systems Market? +

The key participants in the Earthquake Early Warning Systems market are GeoSIG Ltd. (Switzerland), Tokyo Sokushin Co., Ltd. (Japan), Kinemetrics, Inc. (USA), Jenoptik AG (Germany), Nanometrics Inc. (Canada), Teledyne Geotech (USA), Guralp Systems Ltd. (United Kingdom), Trimble Inc. (USA), Hakusan Corporation (Japan) and Swiss Seismological Service (SED) (Switzerland).