- Summary

- Table Of Content

- Methodology

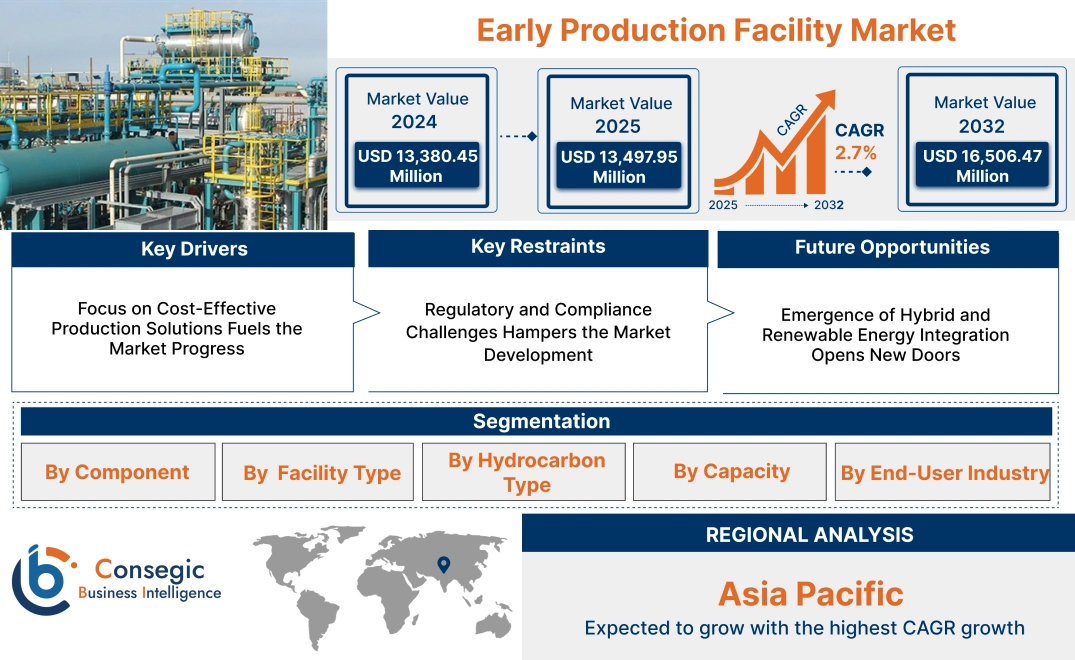

Early Production Facility Market Size:

Early Production Facility Market size is estimated to reach over USD 16,506.47 Million by 2032 from a value of USD 13,380.45 Million in 2024 and is projected to grow by USD 13,497.95 Million in 2025, growing at a CAGR of 2.7% from 2025 to 2032.

Early Production Facility Market Scope & Overview:

An early production facility (EPF) is a modular and temporary setup used in the oil and gas sector to enable the early extraction and processing of hydrocarbons before the completion of permanent production infrastructure. These facilities allow operators to begin production operations while full-scale production systems are still under development, accelerating revenue generation and providing valuable production data.

EPFs typically include essential components such as separators, storage units, pumps, gas compressors, and control systems, designed for efficient handling of oil, gas, and water. They are engineered for rapid deployment, operational flexibility, and scalability, ensuring seamless integration with future permanent facilities. These systems are also designed to comply with industry safety and environmental standards.

End-users of early production facilities include oil and gas exploration and production companies seeking to maximize early-stage asset performance and operational efficiency. EPFs play a critical role in optimizing field development strategies and reducing project execution timelines.

Early Production Facility Market Dynamics - (DRO) :

Key Drivers:

Focus on Cost-Effective Production Solutions Fuels the Market Progress

The focus on cost-effective production solutions is a key driver for the adoption of early production facilities in the oil and gas sector. As oil and gas prices remain volatile, companies face constant pressure to reduce production costs while maintaining operational efficiency. Early production facilities provide a solution by offering a more affordable alternative to large-scale, permanent infrastructure. These modular, temporary systems allow operators to access resources quickly and begin production with lower initial capital investment. The flexibility of these facilities enables companies to scale production as needed, reducing the financial risk associated with large, long-term projects. Additionally, early production facilities are deployed in remote or less-developed fields, where traditional infrastructure is too costly or impractical. This ability to minimize upfront costs while still delivering valuable energy resources makes early production systems an attractive choice for operators aiming to balance cost control with efficient resource extraction, driving the early production facility market growth.

Key Restraints:

Regulatory and Compliance Challenges Hampers the Market Development

Early production systems in the oil and gas sector face significant regulatory and compliance constraints, particularly in regions with strict environmental standards. These systems must adhere to numerous safety and environmental regulations to ensure that operations do not harm the environment or pose risks to human health. Compliance with local laws regarding emissions, waste management, and resource extraction are complex and time-consuming. Securing the necessary permits, undergoing environmental impact assessments, and ensuring adherence to safety protocols adds substantial delays and costs to projects. These regulatory burdens slow down the deployment of early production systems, limiting their scalability and reducing market growth. Companies must invest in legal expertise, environmental monitoring, and advanced technologies to meet these requirements, which is especially difficult in markets where regulatory frameworks are still evolving. These constraints act as a barrier for operators seeking to implement flexible and cost-efficient production solutions, restraining the early production facility market demand.

Future Opportunities :

Emergence of Hybrid and Renewable Energy Integration Opens New Doors

The emergence of hybrid and renewable energy integration into early production facilities offers a significant opportunity for enhancing sustainability in the oil and gas sector. As the requirement for reducing carbon footprints increases, integrating renewable energy sources, such as solar or wind power, into these facilities will help reduce reliance on fossil fuels. Hybrid power systems that combine renewable energy with traditional power sources will lower operational emissions and reduce fuel consumption, making early production operations more eco-friendly. This transition supports compliance with increasingly stringent environmental regulations and helps companies meet their sustainability goals. By adopting renewable energy solutions, early production facilities will be able to operate more efficiently and cost-effectively, particularly in remote or off-grid locations where traditional power infrastructure is limited. This presents new early production facility market opportunities for growth as the industry moves toward greener, more sustainable production methods.

Early Production Facility Market Segmental Analysis :

By Component:

Based on component, the market is segmented into separators, heat exchangers, compressors, pumps, flare systems, and others.

The separators segment accounted for the largest revenue of the total early production facility market share in 2024.

- Separators are critical for efficient phase separation of oil, gas, and water, optimizing production and ensuring smooth downstream processing.

- The rising exploration and production activities in the oil and gas sector drive the demand for advanced separators.

- Their ability to handle high-pressure and high-temperature environments makes them indispensable in onshore and offshore production.

- Technological advancements in separator design have enhanced performance, further boosting adoption across global markets, contributing to the early production facility market expansion.

The compressors segment is projected to witness the fastest CAGR during the forecast period.

- Compressors are essential for maintaining pressure and facilitating the transportation of natural gas from production sites.

- Growing natural gas exploration activities globally are driving the need for high-performance compressors.

- Integration of energy-efficient and low-emission compressor systems supports market development.

- As per the early production facility market analysis, the expansion of offshore gas fields has increased the reliance on advanced compressor technologies, propelling segment growth.

By Facility Type:

Based on facility type, the market is segmented into onshore early production facilities and offshore early production facilities.

The onshore early production facilities segment accounted for the largest revenue of the total early production facility market share in 2024.

- Onshore facilities offer easier access for installation, maintenance, and operation, making them a preferred choice for oil producers.

- Lower operational costs and simplified logistics compared to offshore facilities contribute to their market dominance.

- Rising onshore exploration activities in regions like North America and the Middle East drive segment extension.

- As per the early production facility market trends, rapid deployment of modular onshore EPFs accelerates production timelines and enhances profitability.

The offshore early production facilities segment is expected to grow at the fastest CAGR during the forecast period.

- Increasing deep-water and ultra-deep-water exploration activities are fueling the need for offshore EPFs.

- Offshore facilities are designed to operate in harsh marine environments, enabling extraction from complex reserves.

- Technological advancements in offshore infrastructure are enhancing safety and operational efficiency.

- Significant investments in offshore oil and gas fields globally are driving segment growth, creating substantial early production facility market opportunities.

By Hydrocarbon Type:

Based on hydrocarbon type, the market is segmented into crude oil, natural gas, condensates, and others.

The crude oil segment held the largest revenue share in 2024.

- The global dependence on crude oil for energy and industrial applications sustains high production levels.

- Continuous exploration and development of onshore and offshore oil fields support the demand for EPFs.

- Rising investments in upstream oil projects in developing economies further strengthen segment growth.

- Integration of enhanced oil recovery techniques with EPFs improves production efficiency, boosting early production facility market expansion.

The natural gas segment is expected to register the fastest CAGR during the forecast period.

- Growing need for cleaner energy sources is propelling natural gas exploration and production.

- Governments worldwide are promoting natural gas as a transition fuel, driving investments in related infrastructure.

- Advanced EPFs designed for natural gas processing enhance extraction and production capabilities.

- As per the market trends, the shift towards liquefied natural gas (LNG) projects further accelerates the segment's growth, fueling the early production facility market demand.

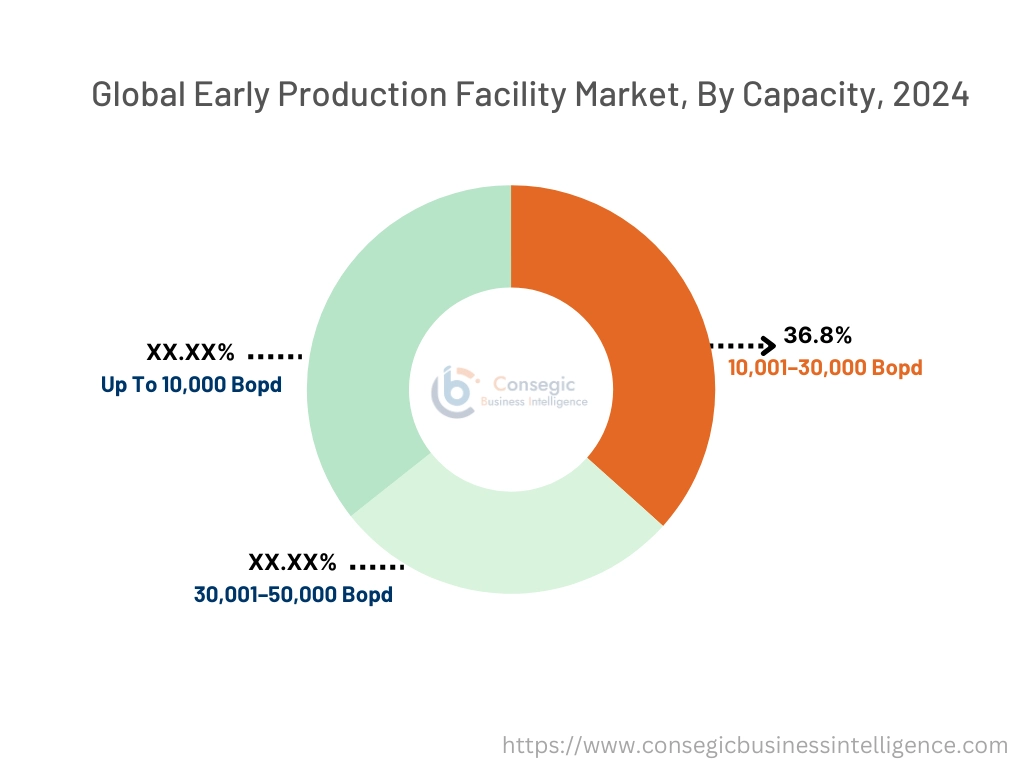

By Capacity:

Based on capacity, the market is segmented into up to 10,000 Bopd, 10,001–30,000 Bopd, and 30,001–50,000 Bopd.

The 10,001–30,000 Bopd segment accounted for the largest revenue of 36.8% share in 2024.

- This capacity range is ideal for medium-scale oil fields, balancing operational efficiency and cost-effectiveness.

- It supports scalable production, allowing operators to adjust output based on market demand.

- The flexibility and modular design of EPFs in this range enable quick deployment and field development.

- As per the early production facility market analysis, growing investments in mid-sized oil fields globally contribute to the segment's strong market position.

The 30,001–50,000 Bopd segment is anticipated to grow at the fastest CAGR during the forecast period.

- The increasing discovery of large oil reserves is driving demand for high-capacity EPFs.

- Enhanced production technologies enable efficient handling of high-volume crude extraction.

- Operators prefer larger EPFs for cost optimization in large-scale projects.

- As per the early production facility market trends, expanding oil exploration in untapped regions fuels the progress of this capacity segment.

By End-Use Industry:

Based on end-user industry, the market is segmented into oil & gas, energy & power, petrochemical, and others.

The oil & gas segment accounted for the largest revenue share in 2024.

- Early production facilities are crucial for the rapid monetization of oil and gas discoveries.

- Continuous exploration and development of new oil and gas fields globally sustain high demand for EPFs.

- Integration of advanced technologies improves production efficiency and reduces operational costs.

- Strategic investments in oil-rich regions by major oil companies further support segment dominance, driving the early production facility market growth.

The petrochemical segment is projected to grow at the fastest CAGR during the forecast period.

- Increasing need for feedstock materials from petrochemical industries drives the need for efficient EPFs.

- Rapid industrialization and expanding chemical production facilities globally fuel the segment's progress.

- EPFs enable timely and cost-effective supply of raw materials to petrochemical plants.

- Thus, as per the market trends, government initiatives to strengthen petrochemical industries in developing economies support market enlargement.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

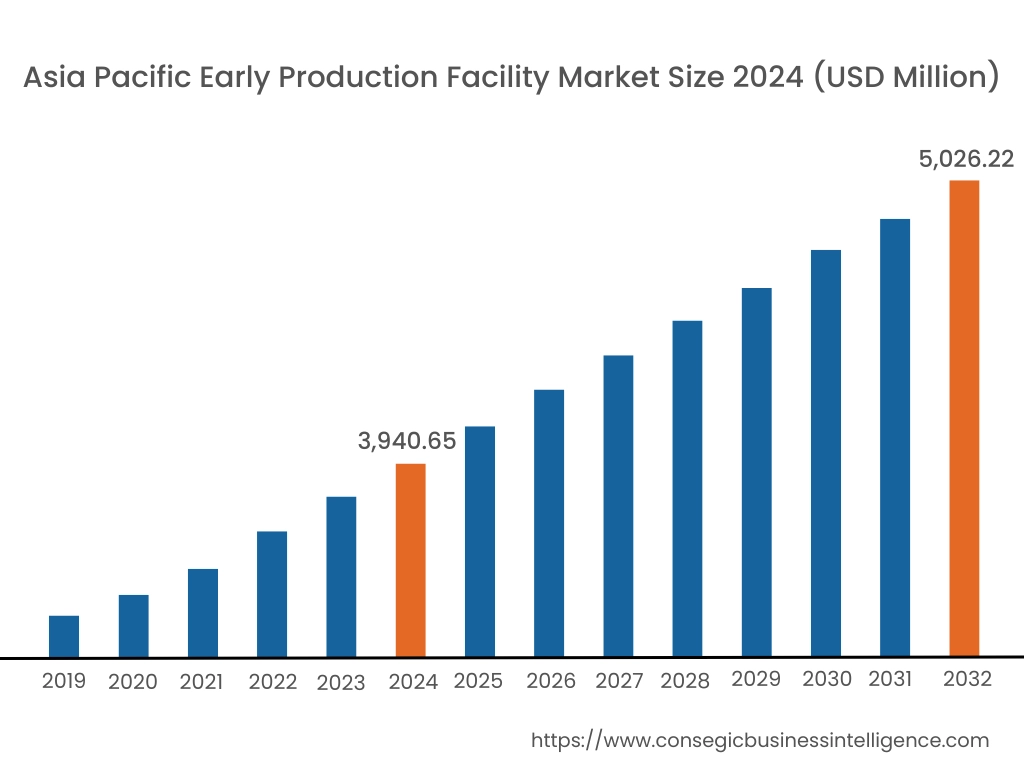

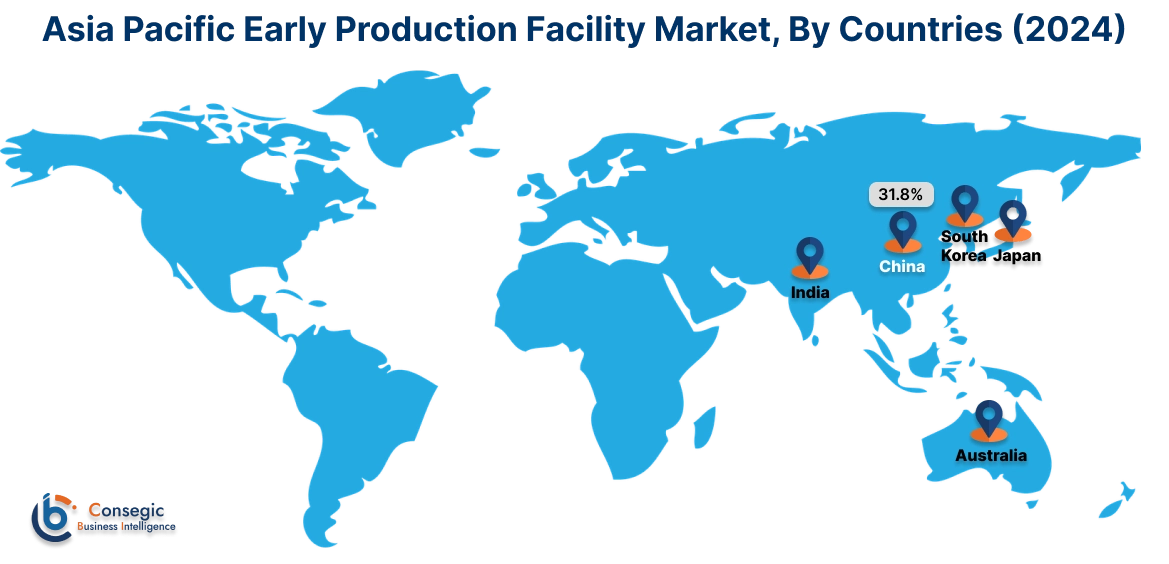

Asia Pacific region was valued at USD 3,940.65 Million in 2024. Moreover, it is projected to grow by USD 3,986.50 Million in 2025 and reach over USD 5,026.22 Million by 2032. Out of this, China accounted for the maximum revenue share of 31.8%. The Asia-Pacific region is witnessing increased adoption of EPFs, attributed to rising energy consumption and the exploration of new oil and gas reserves. A prominent trend is the utilization of EPFs in remote and offshore locations to expedite production and generate early cash flow. Analysis indicates that countries like China and India are investing in EPFs to meet their growing energy needs and reduce dependence on imports.

North America is estimated to reach over USD 5,349.75 Million by 2032 from a value of USD 4,438.41 Million in 2024 and is projected to grow by USD 4,468.83 Million in 2025. This region holds a significant portion of the EPF market, driven by advancements in drilling technologies and the development of new hydrocarbon fields, both onshore and offshore. A notable trend is the implementation of digital technologies, including artificial intelligence and the Internet of Things, to monitor and analyze real-time reservoir and production data. Analysis indicates that the U.S. EPF market is growing rapidly, supported by increased upstream capital expenditure and ongoing investments in research and development for oil and gas production.

European countries, particularly those with mature oil and gas fields, are focusing on optimizing production through the deployment of EPFs. A significant trend is the emphasis on modular and skid-mounted facilities that offer flexibility and cost-effectiveness. Analysis suggests that the integration of EPFs is aiding in extending the life of existing fields and enhancing recovery rates, aligning with the region's commitment to energy efficiency and sustainability.

In the Middle East, the EPF market is influenced by the region's vast hydrocarbon resources and the strategic objective to maximize production efficiency. The focus is on deploying EPFs to rapidly monetize new discoveries and manage production from marginal fields. In Africa, EPFs are being utilized to develop oil and gas projects in challenging environments, facilitating early market entry and revenue generation. Analysis suggests that EPFs are instrumental in overcoming infrastructure constraints and accelerating development timelines in these regions.

Latin American countries are increasingly recognizing the benefits of EPFs in optimizing production from both new and mature fields. A notable trend is the adoption of EPFs to enhance operational flexibility and reduce time-to-market for hydrocarbon resources. However, economic constraints and political factors may impact the pace of adoption. Analysis indicates that collaborations with international oil companies and investments in technology are pivotal in advancing the EPF market in this region.

Top Key Players and Market Share Insights:

The Early Production Facility market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Early Production Facility market. Key players in the Early Production Facility industry include -

- Schlumberger Limited (USA)

- Halliburton Company (USA)

- Pyramid E&C (UAE)

- Frames Group (Netherlands)

- OilSERV (UAE)

- TechnipFMC plc (UK)

- Saipem S.p.A. (Italy)

- Petrofac Limited (UK)

- Expro Group (UK)

- TETRA Technologies, Inc. (USA)

Early Production Facility Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 16,506.47 Million |

| CAGR (2025-2032) | 2.7% |

| By Component |

|

| By Facility Type |

|

| By Hydrocarbon Type |

|

| By Capacity |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Early Production Facility Market? +

The Early Production Facility Market size is estimated to reach over USD 16,506.47 Million by 2032 from a value of USD 13,380.45 Million in 2024 and is projected to grow by USD 13,497.95 Million in 2025, growing at a CAGR of 2.7% from 2025 to 2032.

What are the key segments in the Early Production Facility Market? +

The market is segmented by component (separators, heat exchangers, compressors, pumps, flare systems, others), facility type (onshore early production facilities, offshore early production facilities), hydrocarbon type (crude oil, natural gas, condensates, others), capacity (up to 10,000 Bopd, 10,001–30,000 Bopd, 30,001–50,000 Bopd), and end-user industry (oil & gas, energy & power, petrochemical, others).

Which segment is expected to grow the fastest in the Early Production Facility Market? +

The offshore early production facilities segment is expected to grow at the fastest CAGR during the forecast period, driven by increasing deep-water exploration and offshore infrastructure development.

Who are the major players in the Early Production Facility Market? +

Key players in the Early Production Facility market include Schlumberger Limited (USA), Halliburton Company (USA), TechnipFMC plc (UK), Saipem S.p.A. (Italy), Petrofac Limited (UK), Expro Group (UK), TETRA Technologies, Inc. (USA), Pyramid E&C (UAE), Frames Group (Netherlands), OilSERV (UAE).