- Summary

- Table Of Content

- Methodology

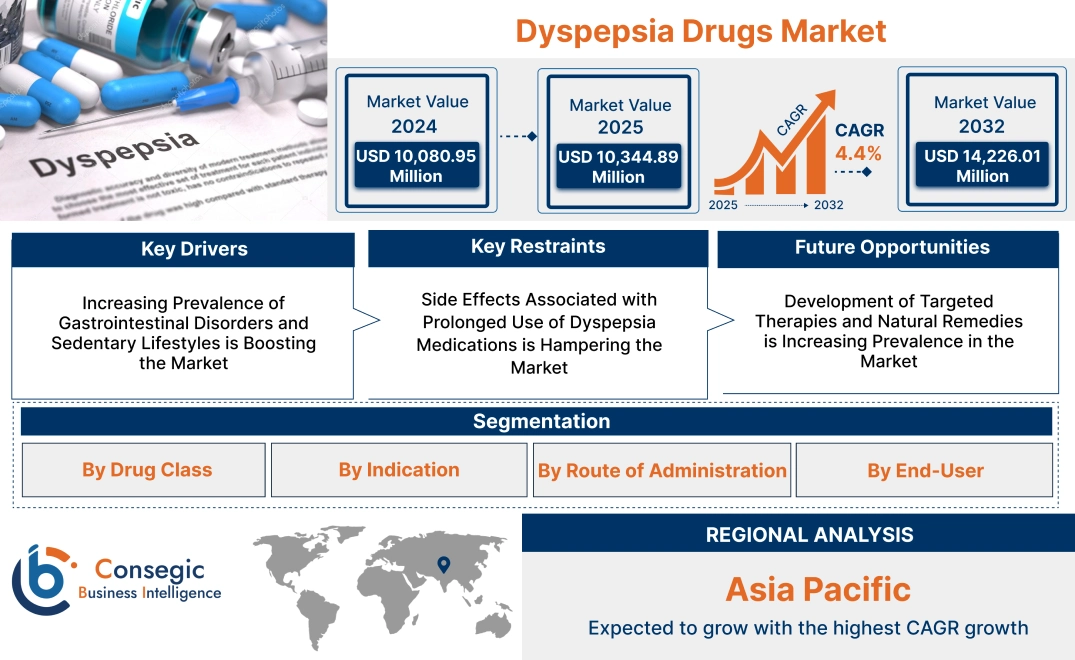

Dyspepsia Drugs Market Size:

Dyspepsia Drugs Market size is estimated to reach over USD 14,226.01 Million by 2032 from a value of USD 10,080.95 Million in 2024 and is projected to grow by USD 10,344.89 Million in 2025, growing at a CAGR of 4.4% from 2025 to 2032.

Dyspepsia Drugs Market Scope & Overview:

The dyspepsia drugs works on the development, production, and distribution of pharmaceutical treatments aimed at managing dyspepsia, commonly referred to as indigestion. This condition is characterized by symptoms such as abdominal discomfort, bloating, nausea, and heartburn. The market includes a wide range of drug classes such as antacids, proton pump inhibitors (PPIs), H2-receptor antagonists, prokinetics, and herbal remedies.

Key characteristics of dyspepsia drugs include rapid symptom relief, high efficacy in reducing gastric acid production, and improved gastrointestinal motility. The benefits include enhanced patient comfort, prevention of complications like gastroesophageal reflux disease (GERD) or peptic ulcers, and better quality of life.

Applications span acute and chronic dyspepsia treatment in hospital settings, outpatient clinics, and over-the-counter (OTC) retail markets. End-users include healthcare providers, gastroenterologists, and individual consumers, driven by increasing prevalence of gastrointestinal disorders, rising adoption of OTC indigestion remedies, advancements in drug formulations, and growing awareness of digestive health.

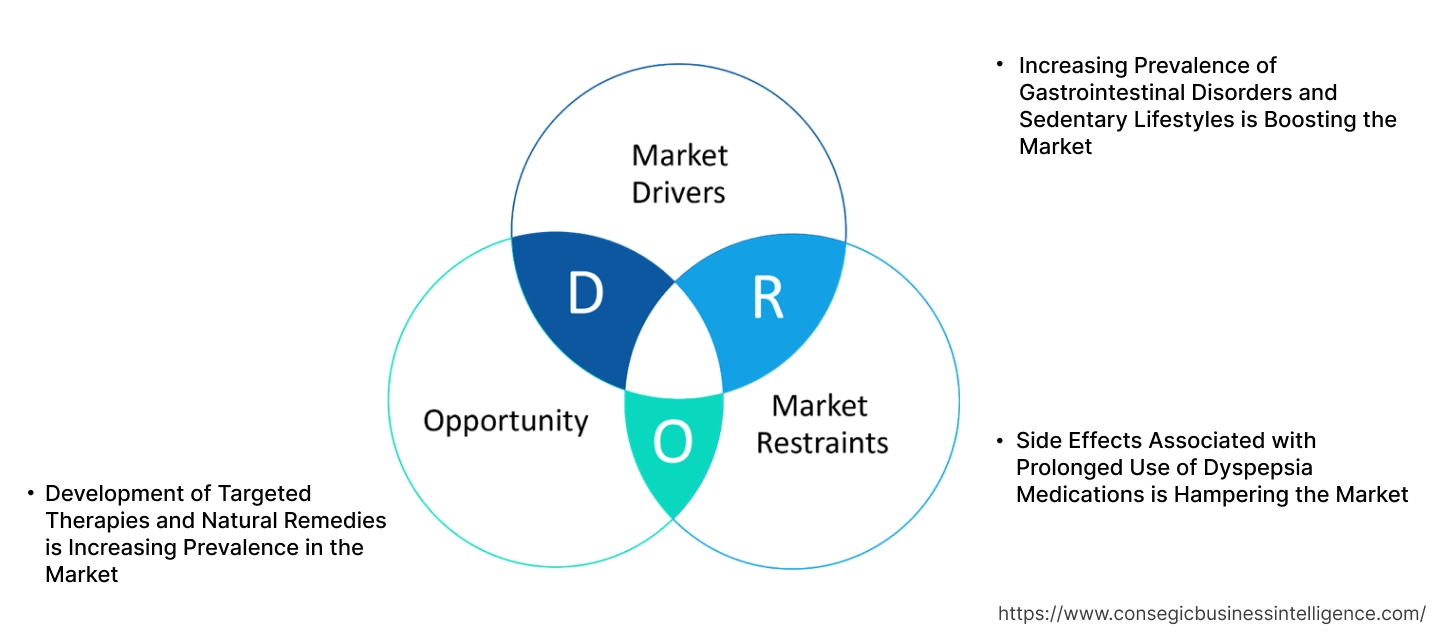

Dyspepsia Drugs Market Dynamics - (DRO) :

Key Drivers:

Increasing Prevalence of Gastrointestinal Disorders and Sedentary Lifestyles is Boosting the Market

The growing prevalence of gastrointestinal disorders, particularly functional dyspepsia, is a major driver of the dyspepsia drugs market. Dyspepsia, or indigestion, is often associated with sedentary lifestyles, unhealthy dietary habits, and stress, all of which are increasingly common in modern urban populations. Conditions such as gastroesophageal reflux disease (GERD), peptic ulcers, and Helicobacter pylori infections are contributing factors to dyspepsia, driving the demand for effective pharmacological treatments. The rising incidence of chronic conditions such as diabetes, which often presents with gastrointestinal symptoms, further fuels the need for dyspepsia drugs. With an increasing awareness of gastrointestinal health, patients are seeking both over-the-counter (OTC) and prescription medications to manage symptoms, propelling market dyspepsia drugs market growth.

Key Restraints:

Side Effects Associated with Prolonged Use of Dyspepsia Medications is Hampering the Market

The dyspepsia drugs market faces challenges due to the side effects associated with prolonged use of certain medications, such as proton pump inhibitors (PPIs) and H2 receptor antagonists. Long-term use of PPIs has been linked to risks such as nutrient malabsorption, kidney disease, and increased susceptibility to infections, which raises concerns among healthcare providers and patients. Additionally, overuse or misuse of OTC antacids and other symptomatic treatments can mask underlying conditions, delaying proper diagnosis and treatment. These factors may limit the adoption of certain dyspepsia drugs, particularly for chronic users, and highlight the need for safer, long-term treatment options.

Future Opportunities:

Development of Targeted Therapies and Natural Remedies is Increasing Prevalence in the Market

The development of targeted therapies and the increasing trends for natural remedies present significant opportunities in the market. Innovations in drug development, such as prokinetics and novel acid suppressants, are addressing the limitations of traditional treatments by targeting specific pathways involved in dyspepsia, offering improved efficacy and safety profiles. Additionally, the growing consumer preference for natural and herbal remedies, such as peppermint oil, ginger extracts, and probiotics, is creating a new segment within the market. These products are perceived as safer alternatives for managing mild to moderate dyspepsia symptoms, particularly among health-conscious consumers. Companies focusing on research and development in both pharmacological and natural treatment options are well-positioned to capitalize on this growing demand.

These dynamics highlight the importance of addressing the rising burden of dyspepsia and related gastrointestinal disorders. While concerns about side effects and misuse persist, advancements in targeted therapies and natural remedies offer promising trends in opportunities for the dyspepsia drugs market, enabling better symptom management and improved patient outcomes.

Dyspepsia Drugs Market Segmental Analysis :

By Drug Class:

Based on drug class, the market is segmented into antacids, proton pump inhibitors (PPIs), H2 receptor antagonists, prokinetics, enzymes, and antibiotics (for H. Pylori).

The proton pump inhibitors (PPIs) segment accounted for the largest revenue in dyspepsia drugs market share in 2024.

- PPIs are highly effective in reducing stomach acid production, making them the first-line treatment for dyspepsia.

- Widely prescribed for functional dyspepsia and cases associated with gastroesophageal reflux disease (GERD), PPIs dominate the market.

- Their extended duration of action and minimal side effects enhance patient compliance, driving segment analysis.

- Increasing awareness and availability of over-the-counter (OTC) PPIs contribute to their widespread adoption globally.

The antibiotics (for H. Pylori) segment is anticipated to register the fastest CAGR during the forecast period.

- Helicobacter pylori infection is a significant cause of organic dyspepsia, necessitating antibiotic therapy for eradication.

- Growing awareness and advancements in diagnostic techniques for identifying H. pylori infections drive demand for targeted antibiotic treatments.

- Combination therapies involving antibiotics and PPIs are increasingly recommended, boosting this segmental analysis.

- Expanding healthcare access in emerging economies for diagnosing and treating bacterial infections supports rapid growth.

By Indication:

Based on indication, the market is segmented into functional dyspepsia and organic dyspepsia.

The functional dyspepsia segment accounted for the largest revenue in dyspepsia drugs market share in 2024.

- Functional dyspepsia, being more prevalent than organic dyspepsia, drives significant growth for treatment solutions.

- Increasing focus on lifestyle-related disorders and rising stress levels contribute to the higher incidence of functional dyspepsia.

- Widely used therapies, such as antacids, PPIs, and prokinetics, support dominance in this segmental analysis.

- Growing awareness campaigns promoting early diagnosis and treatment of functional dyspepsia enhance dyspepsia drugs market growth.

The organic dyspepsia segment is anticipated to register the fastest CAGR during the forecast period.

- Organic dyspepsia, caused by underlying conditions such as ulcers or H. pylori infection, requires specific therapeutic interventions.

- Advancements in diagnostic techniques, such as endoscopy and imaging, have improved the detection of organic dyspepsia.

- Increasing adoption of antibiotics and enzyme therapies for targeted treatment drives dyspepsia drugs market opportunities in this segment.

- Rising awareness about the complications of untreated organic dyspepsia is expected to propel growth for treatment solutions.

By Route of Administration:

Based on the route of administration, the market is segmented into oral and injectable.

The oral segment accounted for the largest revenue share in 2024.

- Oral medications, including antacids, PPIs, and H2 receptor antagonists, are the most commonly prescribed for dyspepsia.

- High patient compliance due to ease of administration and availability of OTC options supports segment dominance.

- Expanding product portfolios of oral formulations by pharmaceutical companies enhance dyspepsia drugs market trends.

- Rising adoption of combination therapies in oral form further boosts trends in this segment.

The injectable segment is anticipated to register the fastest CAGR during the forecast period.

- Injectable formulations are primarily used in severe dyspepsia cases or when oral administration is not feasible.

- Increasing hospital admissions for dyspepsia-related complications drive dyspepsia drugs market demand for injectable treatments.

- Advancements in injectable drug delivery technologies improve efficacy and reduce side effects, supporting trends.

- Growing adoption of parenteral antibiotics for treating H. pylori infections contributes to the segment’s expansion.

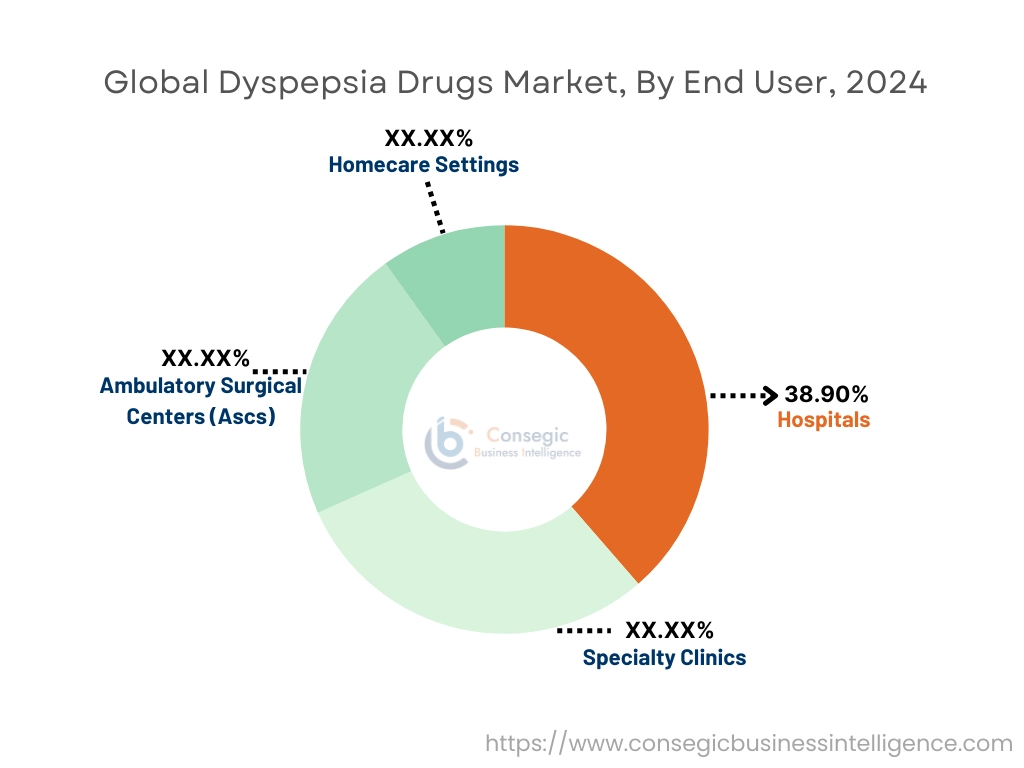

By End-User:

Based on end-user, the market is segmented into hospitals, specialty clinics, ambulatory surgical centers (ASCs), and homecare settings.

The hospitals segment accounted for the largest revenue of 38.90% share in 2024.

- Hospitals are the primary facilities for diagnosing and treating severe dyspepsia cases and related complications.

- Increasing hospital visits for diagnostic tests, such as endoscopy and imaging, drive demand for hospital-based treatment solutions.

- Availability of advanced healthcare infrastructure and skilled professionals supports dominance in this segment.

- Rising government investments in hospital infrastructure in developing economies further bolster dyspepsia drugs market demand.

The specialty clinics segment is anticipated to register the fastest CAGR during the forecast period.

- Specialty clinics, particularly gastroenterology-focused facilities, offer targeted and personalized care for dyspepsia patients.

- Increasing preference for outpatient services and specialized care drives trends in this segment.

- Expanding access to specialty clinics equipped with advanced diagnostic tools supports dyspepsia drugs market trends.

- Rising awareness campaigns and education about gastrointestinal health contribute to the growth of specialty clinics.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

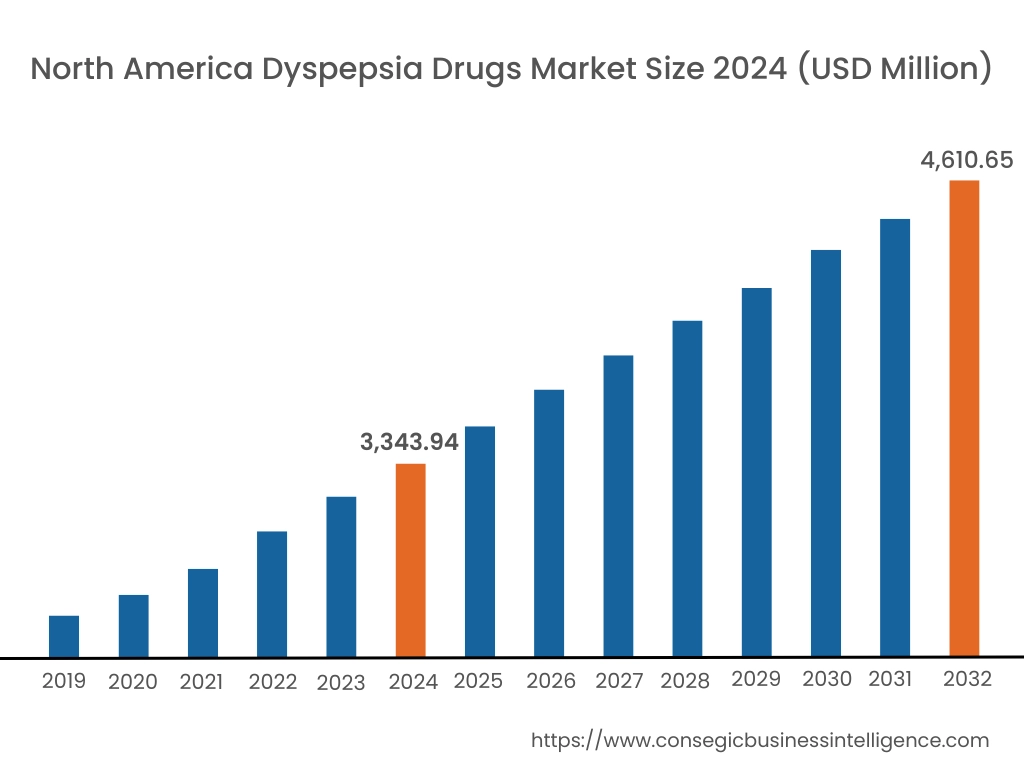

In 2024, North America was valued at USD 3,343.94 Million and is expected to reach USD 4,610.65 Million in 2032. In North America, the U.S. accounted for the highest share of 71.60% during the base year of 2024. North America holds a significant share in the global dyspepsia drugs market, driven by the high prevalence of gastrointestinal disorders, increasing geriatric population, and advanced healthcare infrastructure. The U.S. dominates the region due to the widespread adoption of over-the-counter (OTC) antacids and proton pump inhibitors (PPIs), along with strong R&D investments in developing effective therapies for dyspepsia. Canada contributes to the market with growing awareness about digestive health and the availability of generic medications. However, the overuse of dyspepsia medications in the region raises concerns about long-term side effects and drug resistance.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 4.8% over the forecast period. The dyspepsia drugs market analysis, is fueled by changing dietary habits, increasing stress levels, and a rising prevalence of gastrointestinal disorders in China, India, and Japan. China dominates the region with growing demand for OTC antacids and prescription medications, supported by expanding healthcare access. India’s rising middle-class population and growing awareness about digestive health drive trends for affordable treatments. Japan focuses on advanced pharmaceutical formulations and research into combination therapies for chronic dyspepsia. However, limited access to healthcare facilities in rural areas may hinder market opportunities in some parts of the region.

Europe is a prominent market for dyspepsia drugs, supported by an aging population, increasing prevalence of lifestyle-related digestive disorders, and a robust pharmaceutical industry. Countries like Germany, the UK, and France are key contributors. As per the dyspepsia drugs market analysis, it is portrayed Germany leads with high trends for PPIs and H2 receptor antagonists, supported by advanced diagnostic capabilities for gastrointestinal issues. The UK emphasizes preventive healthcare and promotes the use of OTC dyspepsia drugs, while France focuses on prescription-based treatments and research into novel therapies. However, strict regulations on drug approvals and reimbursement policies may challenge dyspepsia drugs market expansion.

The Middle East & Africa region is witnessing steady growth in the market, driven by increasing healthcare investments and rising prevalence of lifestyle-related digestive disorders. Countries like Saudi Arabia and the UAE are adopting advanced pharmaceutical treatments and promoting public awareness about digestive health through healthcare modernization initiatives. In Africa, South Africa is emerging as a key market, focusing on improving access to affordable dyspepsia drugs and addressing digestive health through community health programs. However, limited healthcare infrastructure in some parts of the region may restrict broader market development.

Latin America is an emerging market for dyspepsia drugs, with Brazil and Mexico leading the region. Brazil’s growing healthcare sector and increasing incidence of digestive disorders drive demand for OTC and prescription-based medications. Mexico analysis shows it focuses on expanding access to affordable dyspepsia drugs through public healthcare programs and partnerships with global pharmaceutical companies. The region also benefits from rising awareness about dietary modifications and preventive care for gastrointestinal issues. However, economic instability and inconsistent healthcare infrastructure in smaller economies may pose challenges to market expansion.

Top Key Players & Market Share Insights:

The dyspepsia drugs market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global dyspepsia drugs market. Key players in the dyspepsia drugs industry include -

- Takeda Pharmaceutical Company Limited (Japan)

- Pfizer Inc. (United States)

- AbbVie Inc. (United States)

- Eisai Co., Ltd. (Japan)

- Procter & Gamble Co. (United States)

- Bayer AG (Germany)

- Johnson & Johnson (United States)

- GlaxoSmithKline plc (United Kingdom)

- AstraZeneca plc (United Kingdom)

- Sanofi S.A. (France)

Recent Industry Developments :

Collaboration:

- In June 2024, Zeria entered into an exclusive agreement with Agastra-Lab s.r.l. for the development and market access of Acotiamide in Europe, the United States, and Canada. This collaboration aims to extend the availability of Acotiamide to patients suffering from FD in these regions.

Product Launch:

- In May 2024, Acotiamide was launched in several Latin American countries, including Ecuador, Dominican Republic, Honduras, El Salvador, and Chile, through a partnership with Faes Farma. This expansion signifies Zeria's commitment to addressing FD globally.

Dyspepsia Drugs Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 14,226.01 Million |

| CAGR (2025-2032) | 4.4% |

| By Drug Class |

|

| By Indication |

|

| By Route of Administration |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the market size and growth rate of the dyspepsia drugs market? +

Dyspepsia Drugs Market size is estimated to reach over USD 14,226.01 Million by 2032 from a value of USD 10,080.95 Million in 2024 and is projected to grow by USD 10,344.89 Million in 2025, growing at a CAGR of 4.4% from 2025 to 2032.

What are the major drivers, restraints, and opportunities shaping the market? +

The study examines the impact of increasing gastrointestinal disorders, lifestyle changes, and advancements in targeted therapies, alongside challenges like side effects and high dependency on certain drug classes.

Which drug class dominates the market, and which is growing the fastest? +

Proton pump inhibitors (PPIs) lead in revenue due to their efficacy in acid suppression, while antibiotics for H. pylori treatment are the fastest-growing segment due to advancements in targeted therapies.

What regional trends influence the dyspepsia drugs market? +

Insights into regional performance, including North America's dominance due to advanced healthcare infrastructure and Asia Pacific's rapid growth fueled by lifestyle changes and healthcare investments, are thoroughly covered.