- Summary

- Table Of Content

- Methodology

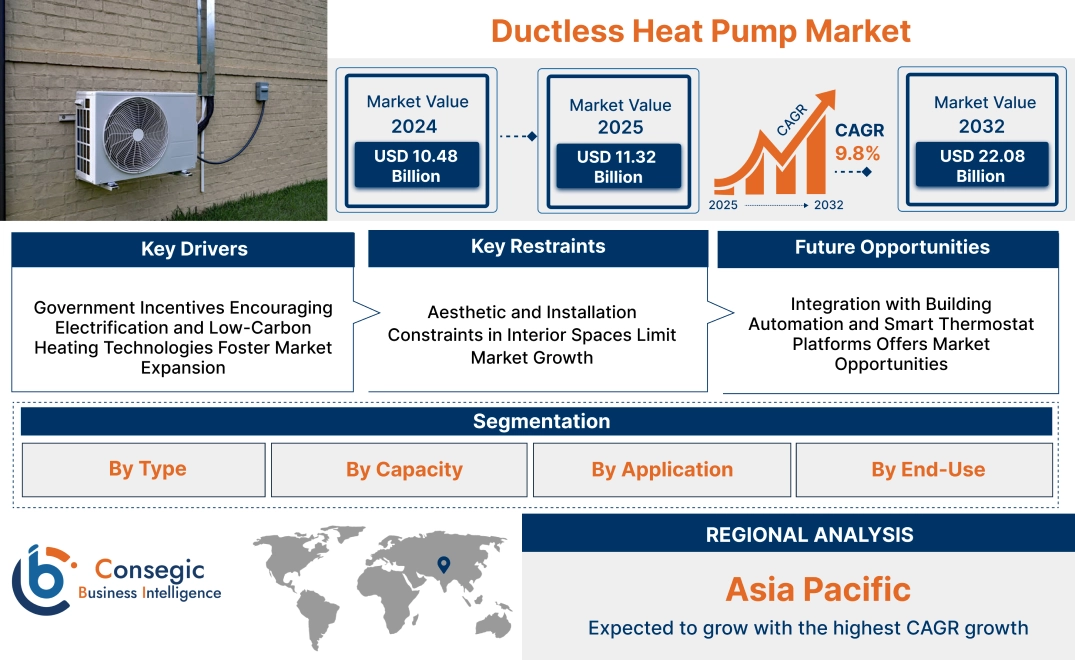

Ductless Heat Pump Market Size:

Ductless Heat Pump Market size is estimated to reach over USD 22.08 Billion by 2032 from a value of USD 10.48 Billion in 2024 and is projected to grow by USD 11.32 Billion in 2025, growing at a CAGR of 9.8% from 2025 to 2032.

Ductless Heat Pump Market Scope & Overview:

Ductless heat pump is a small, split-system air-conditioning unit that is intended to offer both heating and cooling without ductwork. Installed in individual rooms or zones directly, it has an outdoor compressor and one or more indoor air-handling units, providing focused temperature control with excellent energy efficiency.

These systems consist of inverter-driven compressors, programmable timers, multi-speed fans, and wireless remote controls. Their advantages are flexible installation, quiet performance, and zoned comfort control. Ductless reduces thermal losses and installation difficulty and is ideal for retrofits, additions, and new builds.

Well-suited to residential, light commercial, and multi-family dwellings, ductless heat pump systems provide a consistent indoor climate control with small space demands. Their flexibility in adapting to extensive varieties of architectural designs and interior tastes guarantees solid comfort solutions addressing user requirements with support for functional as well as aesthetic needs.

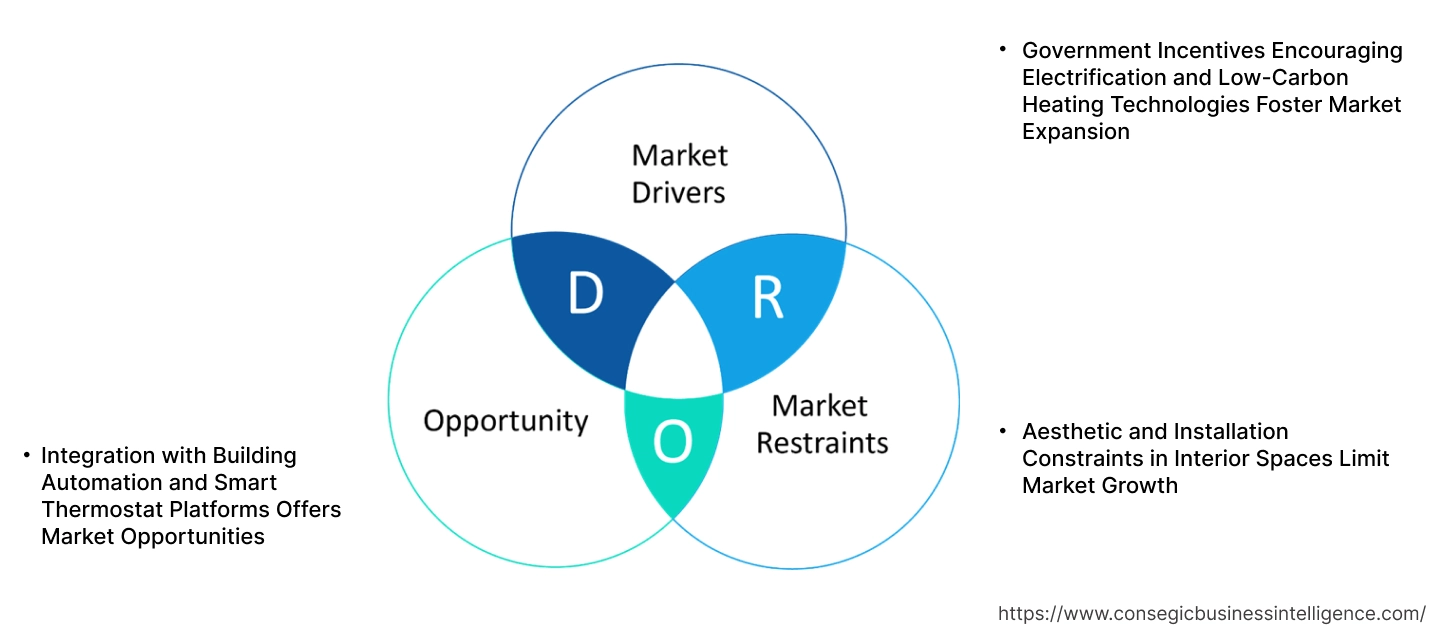

Ductless Heat Pump Market Dynamics - (DRO):

Key Drivers:

Government Incentives Encouraging Electrification and Low-Carbon Heating Technologies Foster Market Expansion

Governments in North America, Europe, and Asia are launching aggressive policy initiatives to drive electrification of heating systems and lower building emissions. Ductless heat pumps are eligible for subsidies, tax credits, and low-interest loans under initiatives like the U.S. Inflation Reduction Act, Canada's Greener Homes Initiative, and several EU-level decarbonization programs. These incentives lower installation costs substantially, making the technology available to residential and small commercial customers. Furthermore, public utility rebates for efficient appliances also motivate building operators and homeowners to shift from gas systems to electric options. The alignment of these incentives with national climate policies and net-zero building codes enables quick uptake, particularly in areas that are implementing fossil fuel phaseouts. This policy-induced acceleration is driving demand among price-conscious buyers and early adopters.

- For instance, in January 2025, the Mayor and the Burlington Electric Department jointly announced new and expanded net-zero energy electrification incentives in Burlington, Vermont, USA. This included, among others, substantial rebates of up to 75% of the installed cost on ductless mini-split heat pumps.

With regulatory and financial drive favoring low-emission HVAC technologies, public-private sector cooperation is a central driver for ductless heat pump market growth.

Key Restraints:

Aesthetic and Installation Constraints in Interior Spaces Limit Market Growth

Wall-mounted indoor units, the typical design in ductless systems, tend to be at odds with the architectural and interior design desires of designers and homeowners who are concerned with aesthetic consistency and clear interior layouts. In upscale residential complexes and commercial buildings with contemporary architecture, exposed HVAC equipment is seen as a visual eyesore. Ceiling cassette and concealed ducted types provide other design options but entail more installation effort and space provisions. In addition, retrofitting indoor units in occupied buildings entails running refrigerant lines and condensate drains through existing walls, which contributes to labor complexity and potential disruption. These considerations discourage deployment in buildings where visual impact and construction constraints are of greater importance than efficiency benefits. A lack of standardized interior design integration also reduces design flexibility and market penetration in architecturally sensitive projects. These combined visual and technical factors dampen demand in certain building segments, serving as a limitation to wider ductless heat pump market expansion.

Future Opportunities:

Integration with Building Automation and Smart Thermostat Platforms Offers Market Opportunities

Ductless heat pump systems are becoming more upgraded with intelligent controls that allow for easy integration into building automation systems and consumer-facing platforms. With Wi-Fi-capable thermostats and cloud-based software, occupants can have real-time access to temperature control, energy consumption, and system diagnostics. This feature allows for participation in demand-response programs and adaptation of load control during peak-demand periods, aligning with smart grid efforts. Commercial building managers appreciate centralized control and zone scheduling, which enhance energy efficiency and occupant comfort. Residential consumers value these features for cost savings and convenience, particularly in areas with fluctuating electricity tariffs. As buildings become smart environments, HVAC systems need to provide not only performance but also data visibility and automation compatibility. These digital capabilities are driving system value and creating new applications throughout smart homes and smart buildings.

- For instance, in February 2025, Lennox unveiled the 'Lennox Powered by Samsung' Mini-Split and VRF product lineups, designed in collaboration with Samsung. The mini-split systems offer compatibility with the Samsung SmartThings app, enabling the management of home temperature remotely along with receiving system updates and tracking energy usage in real time.

Consequently, integration with automation technologies is releasing long-term ductless heat pump market opportunities fueled by necessity and expansion.

Ductless Heat Pump Market Segmental Analysis :

By Type:

Based on type, the market is segmented into mini-split systems (multi-zone mini-split, floor standing, ceiling cassette), multi-split systems, variable refrigerant flow (VRF) systems, window heat pumps, and others.

The mini-split systems segment accounted for the largest ductless heat pump market share in 2024.

- Mini-split systems are widely adopted in both residential and light commercial settings due to ease of installation and zoning flexibility.

- The ability to control temperatures independently across multiple zones significantly improves energy efficiency and indoor comfort.

- Subtypes like multi-zone, floor-standing, and ceiling cassette formats cater to diverse architectural needs, boosting overall adoption.

- As per ductless heat pump market analysis, increasing retrofitting projects in urban dwellings are a major contributor to mini-split system need.

The variable refrigerant flow (VRF) systems segment is expected to register the fastest CAGR during the forecast period.

- VRF systems allow simultaneous heating and cooling across different zones, making them ideal for large commercial buildings and institutions.

- These systems offer precise temperature control and improved operational efficiency through inverter-driven compressors.

- Growing commercial construction and energy regulations in urban regions drive the shift toward VRF installations.

- According to ductless heat pump market trends, integration with smart building automation systems is enhancing VRF system need.

By Capacity:

Based on capacity, the ductless heat pump market is segmented into up to 2 tons, 2–4 tons, and above 4 tons.

The up to 2 tons segment accounted for the largest revenue share in 2024.

- Small-capacity systems are most suited for residential and light commercial spaces with limited heating and cooling requirements.

- These systems are cost-effective and energy-efficient for individual rooms or compact homes, especially in temperate climates.

- Increased requirement for affordable solutions in urban housing has contributed to dominance in this capacity range.

- As per ductless heat pump market analysis, high penetration in single-family homes and small offices drives the segment’s performance.

The 2–4 tons segment is projected to witness the fastest CAGR during the forecast period.

- This capacity range is ideal for mid-size commercial spaces and large residential units requiring moderate heating and cooling loads.

- Increasing adoption in retrofitting applications and mid-size hospitality structures drives the segment growth.

- Energy-saving technologies and inverter-driven systems improve performance and cost-effectiveness in this category.

- According to ductless heat pump market trends, growing awareness about long-term energy cost savings is supporting segment expansion.

By Application:

Based on application, the market is segmented into heating, cooling, and both heating & cooling.

The both heating & cooling segment accounted for the largest ductless heat pump market share in 2024.

- Dual-mode systems offer year-round functionality, which is particularly appealing in regions with seasonal weather variability.

- These units reduce the need for separate HVAC installations, lowering installation and maintenance costs.

- Widespread application across residential and institutional settings contributes to consistent segment dominance.

- As per ductless heat pump market demand insights, the preference for all-season energy-efficient systems fuels this segment.

The heating segment is expected to grow at the fastest CAGR during the forecast period.

- Increased requirement in colder regions for eco-friendly heating solutions without ductwork is propelling segment growth.

- Government incentives for renewable heating systems support faster market adoption of ductless heating systems.

- Improved compressor technologies have enhanced performance even at sub-zero temperatures.

- According to market trends, the rising fuel cost and emission regulations are encouraging investment in heating-focused systems and driving ductless heat pump market expansion.

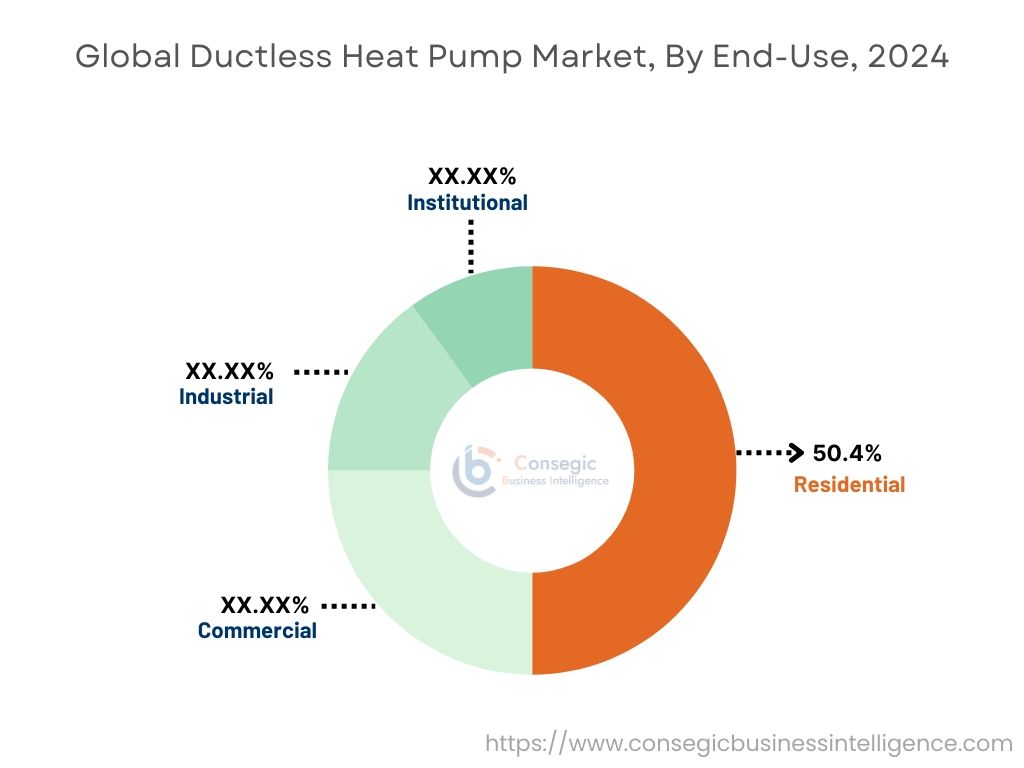

By End-Use:

Based on end-use, the market is segmented into residential, commercial (offices, retail, hospitality), industrial, and institutional (healthcare, education, government buildings).

The residential segment accounted for the largest revenue share of 50.4% in 2024.

- Rapid urbanization and home renovations in both developed and emerging economies drive residential installations.

- Homeowners prefer ductless solutions for energy savings, design flexibility, and zoning control.

- Noise reduction and compact unit designs enhance user experience in modern home environments.

- Furthermore, residential retrofits continue to generate substantial ductless heat pump market demand.

The commercial segment is expected to witness the fastest CAGR during the forecast period.

- Businesses increasingly adopt ductless systems for cost-effective, scalable climate control in retail, offices, and hospitality sectors.

- The ability to manage HVAC in multi-zone environments enhances comfort and energy efficiency in commercial spaces.

- Construction of green buildings and smart commercial infrastructure further accelerates adoption.

- According to ductless heat pump market growth forecasts, the commercial sector will be central to upcoming market expansion.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

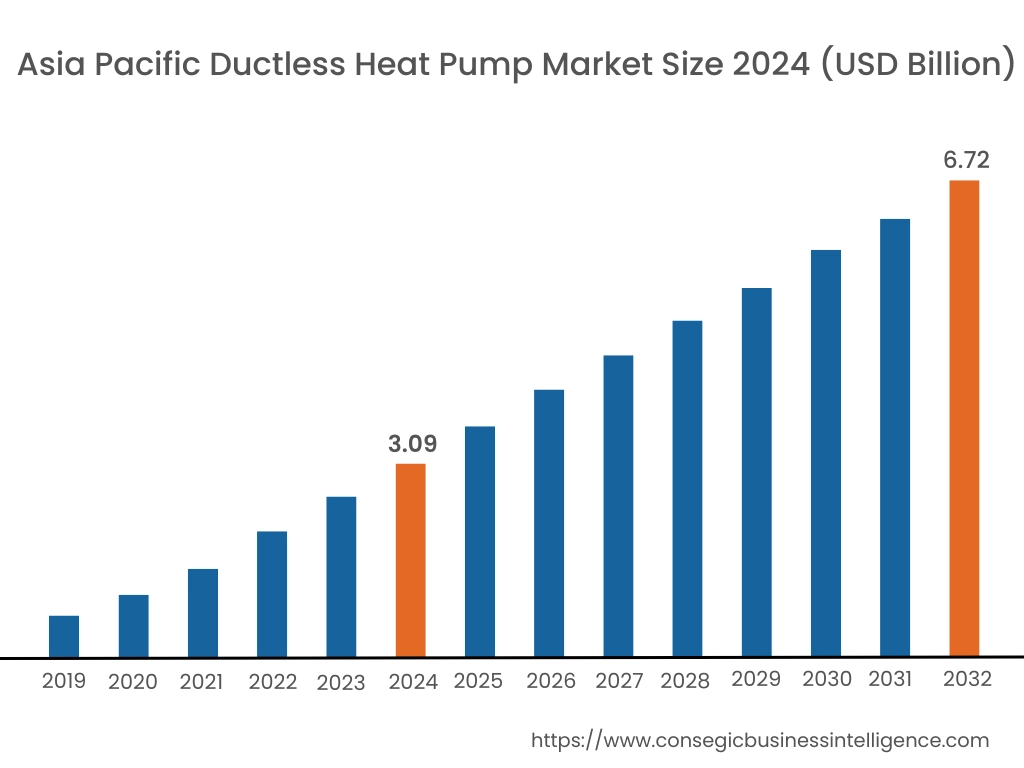

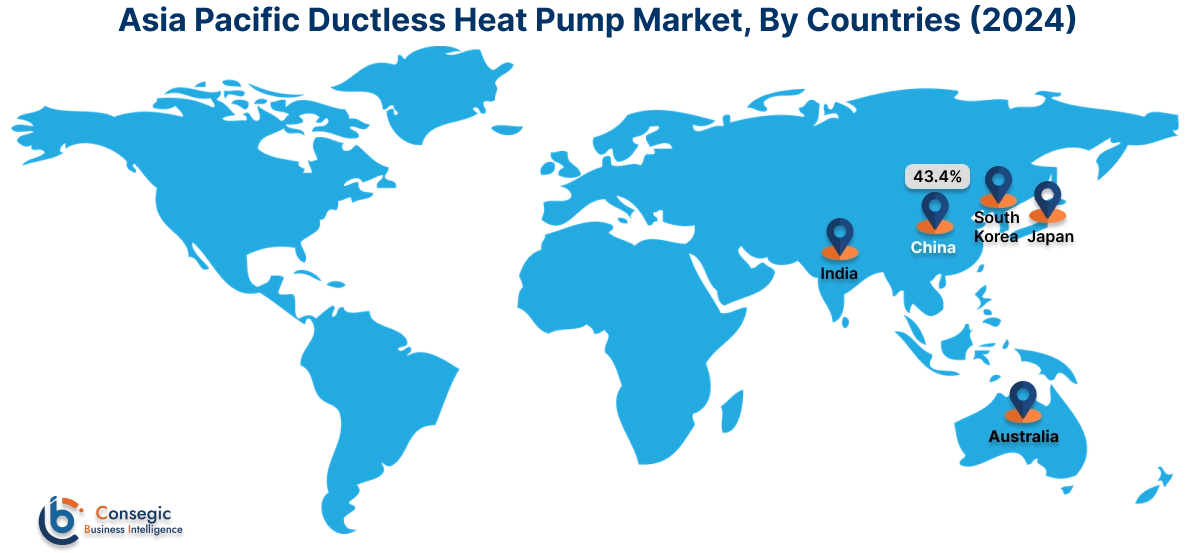

Asia Pacific region was valued at USD 3.09 Billion in 2024. Moreover, it is projected to grow by USD 3.34 Billion in 2025 and reach over USD 6.72 Billion by 2032. Out of this, China accounted for the maximum revenue share of 43.4%. Asia-Pacific is the fastest-growing region due to extensive urbanization, increased disposable income, and the spread of middle-class families in search of modern climate control technology. China, Japan, South Korea, and India are at the heart of this momentum, where government initiatives facilitate effective heating and cooling in both new buildings and retrofits. Analysis indicates demand is particularly acute in high-population cities with space-constrained and energy-conscious systems. Product innovation is also being driven in the region, with manufacturers bringing to market compact, smart-capable units for regional climatic conditions and local consumer tastes.

North America is estimated to reach over USD 7.15 Billion by 2032 from a value of USD 3.48 Billion in 2024 and is projected to grow by USD 3.75 Billion in 2025. North America exhibits a robust and increasingly growing ductless heat pump industry, especially in seasonal temperature-fluctuating areas like the northern U.S. and Canada. Rising emphasis on energy efficiency, tax credits for renewable technologies, and the transition from fossil fuel-driven HVAC systems have spurred need for ductless systems in residential and light commercial usage. Analysis shows that aging building stock and the demand for affordable retrofitting options are also key drivers of market activity. Consumer need for zoned comfort and reduced noise levels is also driving product adoption in both urban and rural areas.

- For instance, in February 2025, Viessmann Canada launched a new heat pump system for residential and limited commercial purposes. The Vitocal 100-S single-zone air-to-air ductless heat pump system offers customers reliable comfort through quiet operation and high-efficiency inverter technology. It ensures a compact, cost-effective and complete solution for the comfort of the entire home.

Europe is still a mature and innovative region, where environmental policy and energy conservation objectives continue to influence product adoption. Nations such as Germany, France, and Nordic countries are leading the decarbonization of heating systems in buildings, with ductless solutions emerging as popular in retrofits, multi-unit homes, and aging buildings where the installation of ducts is infeasible. In-depth research of the European market shows increased coupling of ductless heat pumps with renewable sources of power including solar PV and low-carbon grids. The drive for electrification, supplemented by ambitious emissions-cutting ambitions, continues to reinforce Western and Central European long-term growth prospects.

Adoption is increasing slowly in Latin America in nations like Brazil, Mexico, and Chile, especially in urban centers and higher-end housing segments. While traditional HVAC systems continue to be the norm in much of the region, awareness of the long-term cost-effectiveness and sustainability advantages of ductless systems is on the increase. Market analysis indicates that expansion is highly correlated with enhancements in electricity infrastructure, availability of high-efficiency products, and public awareness campaigns on environmentally friendly cooling and heating options. The region has the potential in both domestic and hospitality use, particularly where there are seasonally changing climates.

The Middle East and Africa market is in the nascent stages of development, although market conditions are changing with the growth of residential building and infrastructure upgradation. The UAE, Saudi Arabia, and South Africa are indicating interest in ductless solutions due to their energy efficiency and the fact that they are well-suited for single room control, which is imperative in large buildings or villas. Regional analysis suggests that the growing focus on building performance standards and energy conservation programs will drive market growth. Yet, increased awareness and availability of technologically sophisticated systems are required to realize wider adoption in emerging markets.

Top Key Players & Market Share Insights:

The ductless heat pump market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global ductless heat pump market. Key players in the ductless heat pump industry include –

- Daikin Industries Ltd. (Japan)

- Mitsubishi Electric Corporation (Japan)

- Fujitsu General Limited (Japan)

- Climaveneta (Mitsubishi Electric) (Italy)

- Bryant Heating & Cooling Systems (USA)

- LG Electronics Inc. (South Korea)

- Panasonic Corporation (Japan)

- Gree Electric Appliances Inc. (China)

- Samsung Electronics Co., Ltd. (South Korea)

- Bosch Thermotechnik GmbH (Germany)

Recent Industry Developments :

Partnerships:

- In March 2025, Panasonic Canada and EMCO announced a national partnership to expand residential heat pump distribution in Canada. This collaboration aims to increase access to high-performance HVAC solutions which are energy-efficient and environmentally friendly.

Ductless Heat Pump Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 22.08 Billion |

| CAGR (2025-2032) | 9.8% |

| By Type |

|

| By Capacity |

|

| By Application |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Ductless Heat Pump Market? +

Ductless Heat Pump Market size is estimated to reach over USD 22.08 Billion by 2032 from a value of USD 10.48 Billion in 2024 and is projected to grow by USD 11.32 Billion in 2025, growing at a CAGR of 9.8% from 2025 to 2032.

What specific segmentation details are covered in the Ductless Heat Pump Market report? +

The Ductless Heat Pump market report includes specific segmentation details for type, capacity, application and end-use.

What are the end-uses in the Ductless Heat Pump Market? +

The end-uses of the Ductless Heat Pump Market are residential, commercial (offices, retail, hospitality), industrial and institutional (healthcare, education, government buildings).

Who are the major players in the Ductless Heat Pump Market? +

The key participants in the Ductless Heat Pump market are Daikin Industries Ltd. (Japan), Mitsubishi Electric Corporation (Japan), Fujitsu General Limited (Japan), LG Electronics Inc. (South Korea), Panasonic Corporation (Japan), Gree Electric Appliances Inc. (China), Samsung Electronics Co., Ltd. (South Korea), Bosch Thermotechnik GmbH (Germany), Climaveneta (Mitsubishi Electric) (Italy) and Bryant Heating & Cooling Systems (USA).