- Summary

- Table Of Content

- Methodology

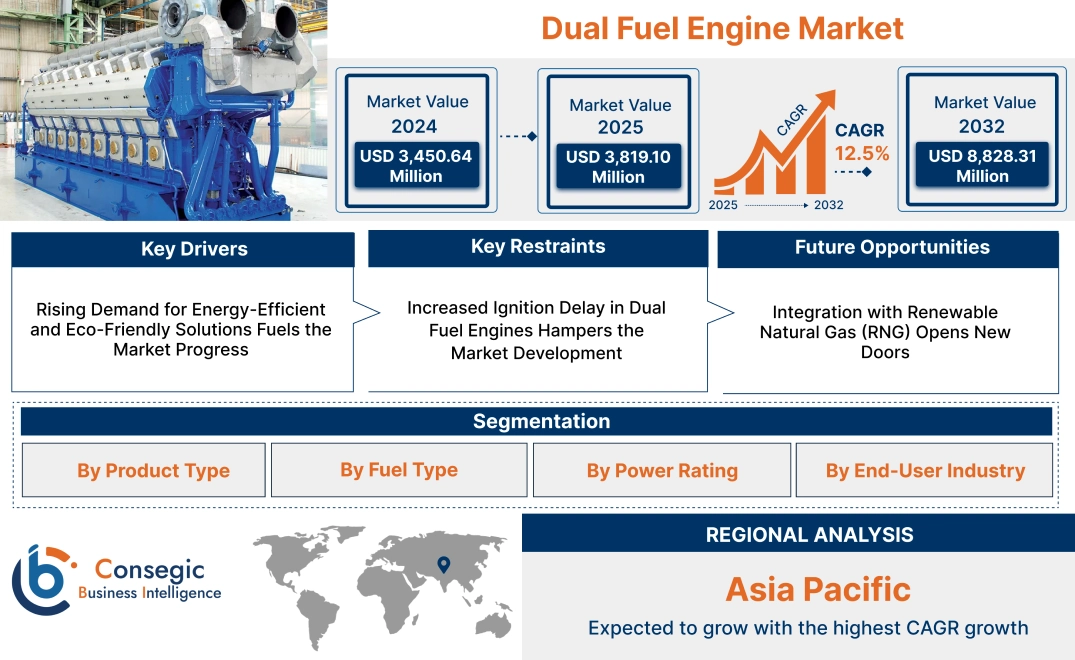

Dual Fuel Engine Market Size:

Dual Fuel Engine Market size is estimated to reach over USD 8,828.31 Million by 2032 from a value of USD 3,450.64 Million in 2024 and is projected to grow by USD 3,819.10 Million in 2025, growing at a CAGR of 12.5% from 2025 to 2032.

Dual Fuel Engine Market Scope & Overview:

A dual fuel engine is an internal combustion engine designed to operate on two types of fuel simultaneously or alternately, typically combining a primary fuel like natural gas with a secondary fuel such as diesel. This configuration allows the engine to switch between fuels or blend them for optimized performance, offering greater flexibility and operational efficiency across various applications.

These engines are engineered to deliver reliable performance while accommodating varying fuel availability and operational demands. They are widely used in marine vessels, power generation, and heavy-duty industrial machinery due to their adaptability and ability to maintain consistent power output. These fuel engines are designed with advanced control systems to manage fuel mixing ratios and ensure seamless transition between fuel sources.

End-users include industries such as maritime, energy, and manufacturing, where flexible and efficient power generation is essential. These engines play a critical role in enhancing fuel efficiency and operational reliability in diverse industrial sectors.

Dual Fuel Engine Market Dynamics - (DRO) :

Key Drivers:

Rising Demand for Energy-Efficient and Eco-Friendly Solutions Fuels the Market Progress

By utilizing a combination of diesel and natural gas or LNG, dual fuel engines offer improved fuel efficiency while significantly reducing harmful emissions, such as nitrogen oxides (NOx) and particulate matter. This makes them an attractive choice for industries striving to meet stricter environmental regulations and reduce their carbon footprints. As governments globally impose more stringent emissions standards, particularly in sectors like transportation, shipping, and power generation, these engines present a viable alternative to traditional diesel-only engines. They allow operators to reduce reliance on more polluting fuels while maintaining high performance and lower operational costs. The fuel engine's ability to use cleaner fuels, such as natural gas, positions it as a key solution in the transition toward more sustainable and environmentally responsible energy use. Thus, the aforementioned factors are driving the dual fuel engine market growth.

Key Restraints:

Increased Ignition Delay in Dual Fuel Engines Hampers the Market Development

A significant restraint for dual fuel engines is the increased ignition delay when operating on a combination of fuels, typically diesel and natural gas or LNG. Unlike conventional diesel engines, which rely solely on the rapid ignition of diesel, these engines experience a delay in the ignition of natural gas. This delay occurs because natural gas has a higher ignition temperature and requires additional time to combust when mixed with diesel. The increased ignition delay affects engine performance, resulting in reduced efficiency and power output, especially at lower engine speeds or under varying load conditions. Furthermore, this delay leads to higher levels of unburned fuel in the exhaust, affecting overall emissions and contributing to engine knocking or misfiring. Addressing ignition delay requires sophisticated control systems and precise fuel management, which increases the complexity and cost, limiting the dual fuel engine market demand.

Future Opportunities :

Integration with Renewable Natural Gas (RNG) Opens New Doors

The integration of renewable natural gas (RNG), produced from biogas sources such as organic waste, into dual fuel engines offers a significant opportunity to create a fully sustainable energy solution. By replacing conventional natural gas with RNG, which is carbon-neutral or even carbon-negative, dual fuel systems will drastically reduce their overall carbon emissions. This shift not only enhances the environmental benefits of dual fuel engines but also aligns with global sustainability goals. Utilizing RNG in these engines contributes to the reduction of greenhouse gases, making it an attractive option for industries aiming to meet stricter emissions regulations. Additionally, the use of RNG helps promote the circular economy by converting waste into energy, reducing reliance on fossil fuels. As the infrastructure for RNG expands and technology advances, this integration will further position these engines as a crucial part of the transition to greener, more sustainable energy solutions across sectors, creating new dual fuel engine market opportunities.

Dual Fuel Engine Market Segmental Analysis :

By Product Type:

Based on product type, the market is segmented into four-stroke dual fuel engines and two-stroke dual fuel engines.

The four-stroke dual fuel engine segment held the largest revenue of the total dual fuel engine market share in 2024.

- Four-stroke engines offer better fuel efficiency and durability, making them ideal for heavy-duty industrial and marine applications.

- These engines are widely used in power generation and transportation sectors due to their lower emissions and compliance with environmental regulations.

- The segment's dominance is further driven by advancements in engine technology, enhancing fuel flexibility and operational efficiency.

- Increased investments in infrastructure development and shipping industries globally have significantly boosted the adoption of four-stroke dual fuel engines, fueling the dual fuel engine market expansion.

The two-stroke dual fuel engine segment is expected to register the fastest CAGR during the forecast period.

- Two-stroke engines provide higher power output and are preferred for applications requiring high-speed operations, such as marine propulsion.

- The compact design and lightweight structure of two-stroke engines make them suitable for various industrial applications.

- The segment's growth is supported by the increasing adoption of two-stroke engines in the maritime sector for cost-effective and efficient operations.

- As per the dual fuel engine market analysis, rising focus on reducing emissions in heavy industries is driving the integration of cleaner dual fuel solutions like two-stroke engines.

By Fuel Type:

Based on fuel type, the market is segmented into diesel & natural gas, diesel & biofuel, gasoline & natural gas, and others.

The diesel & natural gas segment accounted for the largest revenue of the total dual fuel engine market share in 2024.

- Diesel and natural gas dual fuel engines offer a cost-effective and cleaner alternative to conventional diesel engines.

- The availability of natural gas and advancements in engine designs supporting dual fuel integration have driven the segment's dominance.

- The reduction in carbon emissions and operational costs aligns with global environmental regulations, boosting segment growth.

- As per the dual fuel engine market trends, increasing adoption of diesel & natural gas fuel engines in transportation and power generation sectors is contributing to market expansion.

The diesel & biofuel segment is anticipated to witness the fastest CAGR during the forecast period.

- Biofuels provide a renewable and sustainable energy source, aligning with global decarbonization efforts.

- The rising demand for alternative fuels in industries aiming to reduce their carbon footprint supports this segment’s growth.

- Government policies promoting the use of biofuels in industrial and transport applications are driving adoption.

- As per the dual fuel engine market analysis, technological advancements in blending biofuels with diesel improve engine performance and fuel efficiency, further accelerating segment growth.

By Power Rating:

Based on power rating, the market is categorized into below 1 MW, 1–5 MW, 5–10 MW, and above 10 MW.

The 1–5 MW segment accounted for the largest market share in 2024.

- Engines within this range are extensively used in industrial manufacturing and power generation due to their efficiency and versatility.

- Growing industrialization in developing countries has increased the demand for medium-capacity dual fuel engines.

- These engines are preferred for their operational flexibility, balancing fuel efficiency and performance.

- Increased infrastructure development projects worldwide are further supporting segment growth, contributing to the dual fuel engine market demand.

The above 10 MW segment is expected to exhibit the fastest CAGR during the forecast period.

- High-power dual fuel engines are essential for large-scale applications like marine propulsion and large industrial operations.

- The growing shipping industry and expansion of global trade routes drive the need for high-capacity engines.

- The push for cleaner fuel solutions in heavy industries is promoting the adoption of large-capacity fuel engines.

- As per the dual fuel engine market trends, investments in offshore oil and gas projects contribute to segment progress due to the need for robust power solutions.

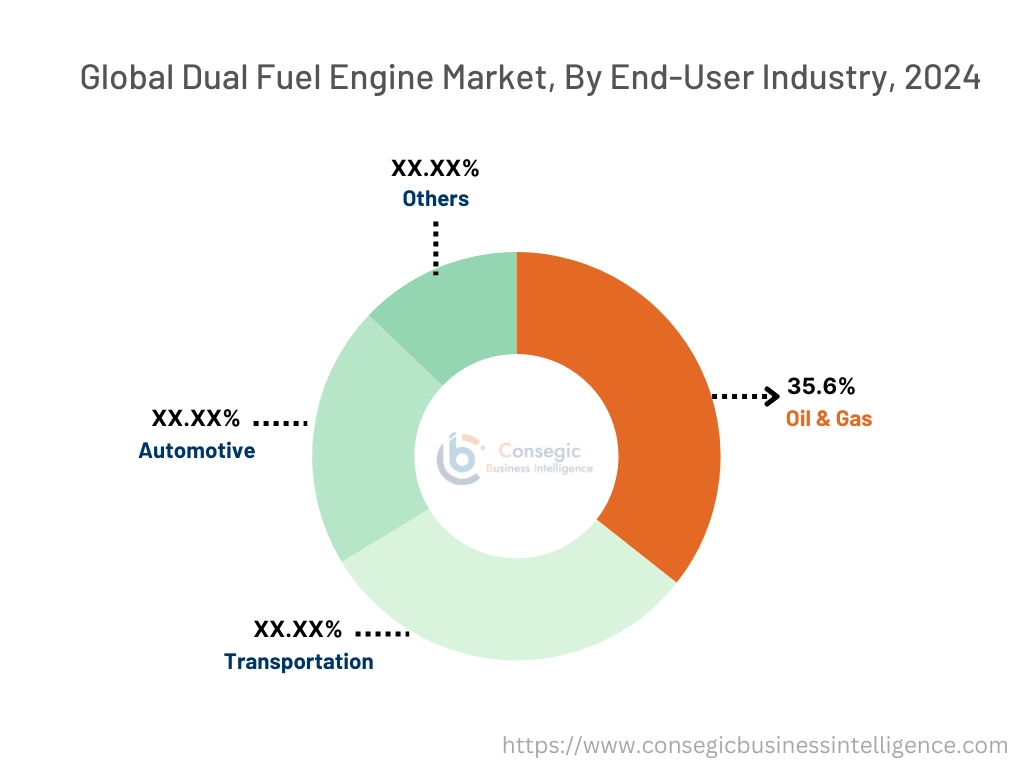

By End-Use Industry:

Based on the end-user industry, the market is segmented into oil & gas, transportation, automotive, and others.

The oil & gas segment accounted for the largest market share of 35.6% in 2024.

- Dual fuel engines are extensively used in offshore drilling rigs and power generation in oilfields, offering cost efficiency.

- The ability to switch between diesel and natural gas helps reduce operational costs and ensures continuous operation.

- Stringent emission regulations in the oil & gas sector drive the adoption of cleaner dual fuel technologies.

- Thus, increasing exploration and production activities worldwide fuels the dual fuel engine market growth.

The transportation segment is projected to grow at the fastest CAGR during the forecast period.

- Rising demand for sustainable fuel solutions in maritime and heavy-duty transportation supports segment progress.

- The need for fuel flexibility and lower emissions in commercial shipping is driving the adoption of dual fuel engines.

- Government policies promoting the use of alternative fuels in logistics and freight industries are further boosting growth.

- As per the market trends, advancements in fuel engine technology ensure better fuel efficiency and compliance with environmental standards, encouraging widespread adoption, driving the dual fuel engine market opportunities.

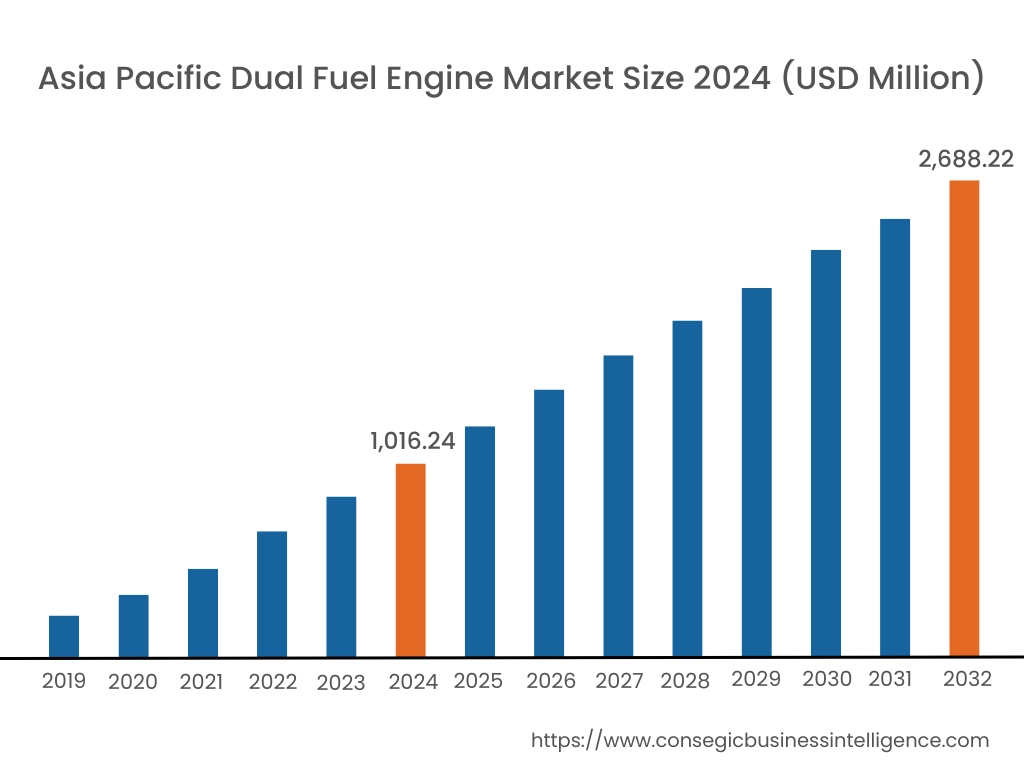

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

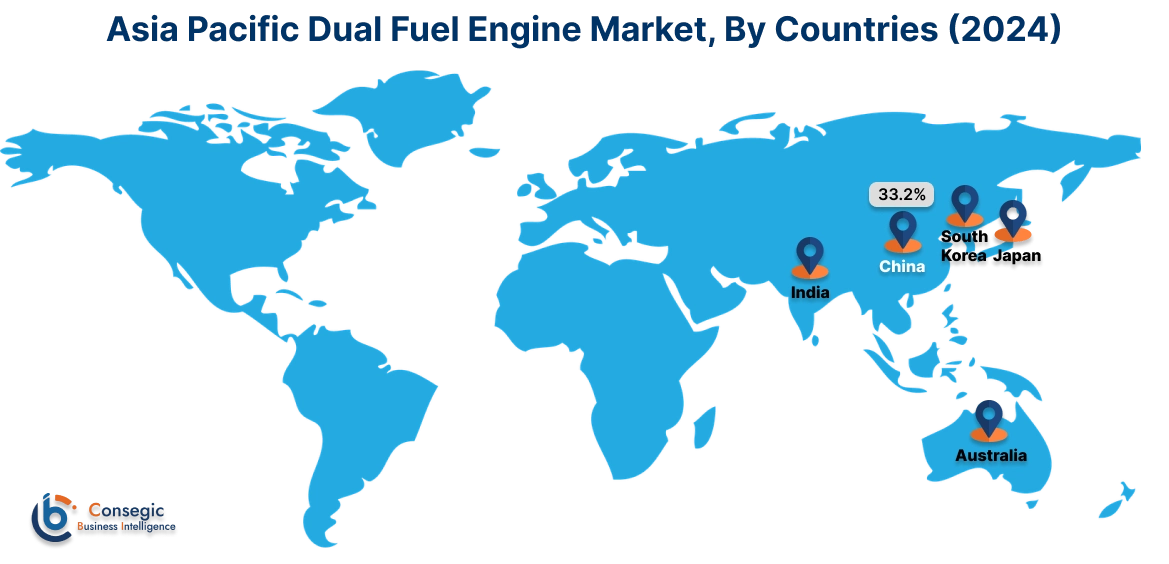

Asia Pacific region was valued at USD 1,016.24 Million in 2024. Moreover, it is projected to grow by USD 1,127.94 Million in 2025 and reach over USD 2,688.22 Million by 2032. Out of this, China accounted for the maximum revenue share of 33.2%. The Asia-Pacific region is witnessing rapid advancements in the dual fuel engine market, attributed to an increase in governmental activities and restrictions regarding fuel engines in nations like China, India, South Korea, and Japan. A prominent trend is the development of these fuel engines to meet the rising energy needs and environmental concerns in these countries. Analysis indicates that China holds the largest market portion, with India being the fastest-growing market in the Asia-Pacific region.

North America is estimated to reach over USD 2,861.25 Million by 2032 from a value of USD 1,144.61 Million in 2024 and is projected to grow by USD 1,264.41 Million in 2025. This region commands a substantial portion of the dual fuel engine market, driven by stringent environmental regulations and the expanding availability of LNG infrastructure. A notable trend is the increasing adoption of dual fuel engines in industries such as marine, power generation, and transportation, where the ability to switch between natural gas and diesel reduces fuel costs and emissions. Analysis indicates that the United States is a major participant in the market, with government incentives and programs encouraging the use of greener energy technology and lower carbon footprints.

European countries, particularly Germany and the UK, are key players in the fuel engine market, with a strong emphasis on reducing emissions in the automotive and transportation industries. A significant trend is the high need for dual-fuel engines in these sectors, driven by stringent environmental regulations and a focus on sustainability. Analysis suggests that Europe will hold a significant market share due to these factors, with Germany holding the largest market portion and the UK being the fastest-growing market in the region.

In the Middle East, the market is influenced by the region's efforts to diversify energy sources and invest in sustainable technologies. The focus is on adopting advanced dual fuel engine solutions to support renewable energy projects and enhance energy security. In Africa, the market is gradually developing, with initiatives to improve access to electricity through sustainable and efficient energy systems. Analysis suggests that international collaborations and investments in energy infrastructure are crucial for dual fuel engine market expansion in these regions.

Latin American countries are increasingly recognizing the importance of advanced engine technologies in supporting renewable energy integration and improving grid stability. A notable trend is the adoption of these fuel engines in various sectors, including power generation and transportation, to enhance fuel efficiency and reduce emissions. However, economic constraints and limited technological infrastructure may impact the pace of adoption. The analysis of market trends indicates that government initiatives to promote clean energy and investments in technological advancements could play a pivotal role in advancing the dual fuel engine market in this region.

Top Key Players and Market Share Insights:

The Dual Fuel Engine market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Dual Fuel Engine market. Key players in the Dual Fuel Engine industry include -

- Wärtsilä Corporation (Finland)

- MAN Energy Solutions (Germany)

- Rolls-Royce Holdings plc (UK)

- General Electric Company (USA)

- Kawasaki Heavy Industries, Ltd. (Japan)

- Caterpillar Inc. (USA)

- Cummins Inc. (USA)

- Yanmar Co., Ltd. (Japan)

- Mitsui E&S Holdings Co., Ltd. (Japan)

- Hyundai Heavy Industries Co., Ltd. (South Korea)

Recent Industry Developments :

Service Launch:

- In October 2024, Wärtsilä introduced its NextDF feature for the Wärtsilä 25DF dual-fuel engine, cutting methane emissions to as low as 1.1% during LNG operation. It also lowers NOx emissions below IMO Tier III standards. This innovation supports LNG's role as a transitional marine fuel and aligns with upcoming GHG regulations from the IMO and EU. Wärtsilä's efforts aim to enhance LNG viability and contribute to marine decarbonization.

Partnerships & Collaborations:

- In March 2024, MAN Energy Solutions and China Classification Society (CCS) signed a sub-agreement to advance the MAN L21/31DF-M methanol dual-fuel engine in China. This partnership highlights growing interest in methanol as a marine fuel and supports global maritime decarbonization efforts.

Dual Fuel Engine Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 8,828.31 Million |

| CAGR (2025-2032) | 12.5% |

| By Product Type |

|

| By Fuel Type |

|

| By Power Rating |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Dual Fuel Engine Market? +

The Dual Fuel Engine Market size is estimated to reach over USD 8,828.31 Million by 2032 from a value of USD 3,450.64 Million in 2024 and is projected to grow by USD 3,819.10 Million in 2025, growing at a CAGR of 12.5% from 2025 to 2032.

What are the key segments in the Dual Fuel Engine Market? +

The market is segmented by product type (four-stroke dual fuel engine, two-stroke dual fuel engine), fuel type (diesel & natural gas, diesel & biofuel, gasoline & natural gas, others), power rating (below 1 MW, 1–5 MW, 5–10 MW, above 10 MW), and end-user industry (oil & gas, transportation, automotive, others).

Which segment is expected to grow the fastest in the Dual Fuel Engine Market? +

The diesel & biofuel segment is anticipated to witness the fastest CAGR during the forecast period, driven by the increasing demand for renewable and sustainable fuel solutions to reduce carbon footprints.

Who are the major players in the Dual Fuel Engine Market? +

Key players in the Dual Fuel Engine market include Wärtsilä Corporation (Finland), MAN Energy Solutions (Germany), Caterpillar Inc. (USA), Cummins Inc. (USA), Yanmar Co., Ltd. (Japan), Mitsui E&S Holdings Co., Ltd. (Japan), Hyundai Heavy Industries Co., Ltd. (South Korea), Rolls-Royce Holdings plc (UK), General Electric Company (USA), Kawasaki Heavy Industries, Ltd. (Japan).