- Summary

- Table Of Content

- Methodology

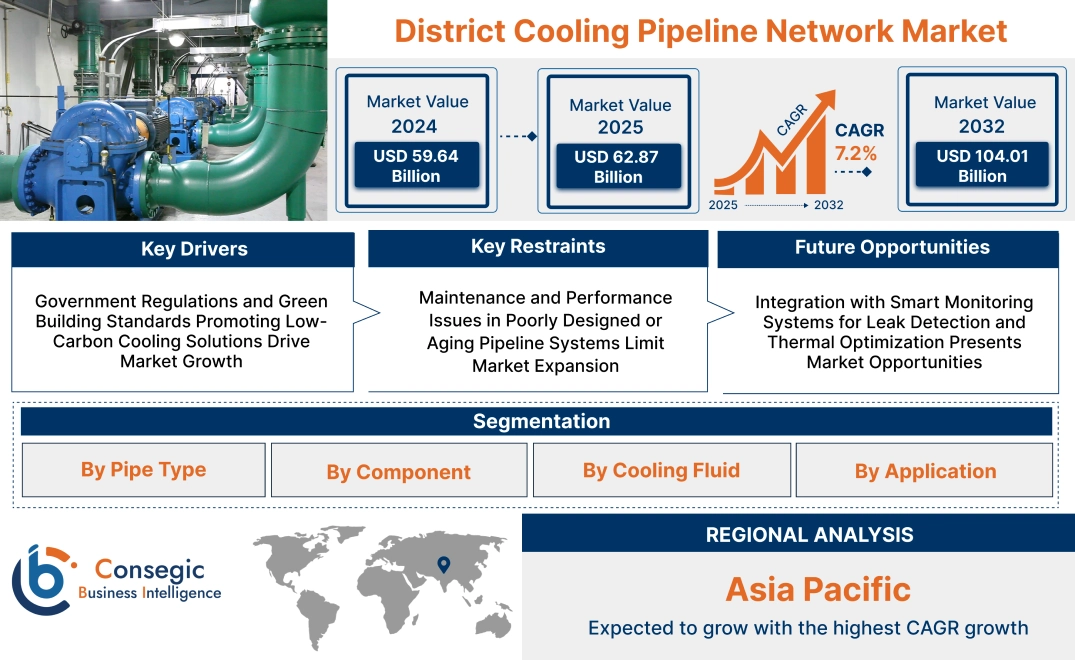

District Cooling Pipeline Network Market Size:

District Cooling Pipeline Network Market size is estimated to reach over USD 104.01 Billion by 2032 from a value of USD 59.64 Billion in 2024 and is projected to grow by USD 62.87 Billion in 2025, growing at a CAGR of 7.2% from 2025 to 2032.

District Cooling Pipeline Network Market Scope & Overview:

District cooling pipeline network is an integrated infrastructure system designed to distribute chilled water from a central cooling plant to multiple buildings for air conditioning purposes. These underground pipelines circulate cooled fluid through a closed-loop system, enabling large-scale and energy-efficient climate control across urban and commercial developments.

Typical components include pre-insulated steel or polymer pipes, thermal insulation layers, leak detection systems, and flow control mechanisms. Engineered for high thermal integrity and mechanical durability, the network ensures stable temperature delivery with minimal energy loss.

The district cooling pipeline network facilitates centralized maintenance, reduces peak electricity demand, and minimizes space requirements within individual buildings. It supports scalable installations and long-term operational efficiency, making it suitable for high-density zones such as business districts, residential complexes, airports, and institutional campuses. Its adaptability and performance in delivering reliable, low-maintenance cooling solutions position it as a vital asset in sustainable urban infrastructure planning.

District Cooling Pipeline Network Market Dynamics - (DRO) :

Key Drivers:

Government Regulations and Green Building Standards Promoting Low-Carbon Cooling Solutions Drive Market Growth

Governments and urban planning authorities are enforcing energy efficiency mandates and green building standards that promote the adoption of centralized district cooling systems. Certifications such as LEED, Estidama, and BREEAM encourage integration with district cooling infrastructure due to its lower carbon footprint, reduced refrigerant leakage, and improved energy intensity. Municipal policies in regions like the Middle East, Singapore, and Northern Europe mandate the use of district cooling for large-scale developments, especially in commercial and high-density residential zones. These regulations are aligned with national carbon neutrality goals and urban sustainability targets, encouraging developers and utilities to invest in robust pipeline networks.

- For instance, in March 2025, SP Group (SP) commenced operations of a distributed district cooling (DDC) network at Tampines, Singapore. As part of the Singapore Green Plan 2030, this network reduces carbon emissions by 1,000 tonnes and achieves energy savings of more than 2,300,000 kilowatt-hours (kWh) annually. This is also the first DDC network designed specifically for brownfield developments in Singapore, with seven buildings connecting to the network. It utilizes existing in-building chiller plants.

The growing policy emphasis on decarbonizing building operations and reducing electricity load during peak demand is directly increasing the adoption of centralized cooling infrastructure, driving long-term district cooling pipeline network market expansion.

Key Restraints:

Maintenance and Performance Issues in Poorly Designed or Aging Pipeline Systems Limit Market Expansion

Older district cooling infrastructure often suffers from thermal inefficiencies, mechanical wear, and pipeline degradation, leading to increased energy consumption and frequent operational disruptions. Inadequate insulation, corroded components, or misaligned hydraulic balancing systems reduce cooling efficiency and create uneven load distribution across buildings. These inefficiencies result in higher operational costs and compromise service reliability, particularly during peak demand periods. In poorly planned networks, lack of accurate system mapping and insufficient monitoring makes it difficult to localize faults or prevent leaks. The need for regular flushing, sensor calibration, and corrosion control adds to maintenance complexity. These issues deter utilities and municipalities from expanding existing networks or replicating them in new districts. Despite growing need for centralized cooling, reliability and lifecycle performance concerns in legacy systems continue to restrain district cooling pipeline network market growth.

Future Opportunities :

Integration with Smart Monitoring Systems for Leak Detection and Thermal Optimization Presents Market Opportunities

The adoption of smart monitoring technologies is transforming how district cooling pipeline networks are managed and maintained. IoT-enabled sensors and flow meters embedded within the network provide real-time data on pressure drops, thermal gradients, and potential leak points. When integrated with SCADA and analytics platforms, operators gain visibility into network performance, enabling predictive maintenance, early fault detection, and optimized hydraulic control. These systems reduce unplanned downtime, energy loss, and service interruptions, enhancing the overall efficiency and reliability of the cooling infrastructure. Demand for digitalized utility networks is increasing as smart cities and green infrastructure become central to urban development strategies.

- For instance, in January 2024, Sensata unveiled a new smart pressure sensor for in-meter monitoring, the 129CP Series Digital Water Pressure Sensor. This sensor enables sustainable water use by reducing water wastage due to leaks by monitoring the pressure outputs to identify leaks and other issues to minimize loss.

The combination of data intelligence and proactive asset management is creating a strong case for investment in advanced monitoring systems, unlocking scalable district cooling pipeline network market opportunities driven by both performance growth and sustainability goals.

District Cooling Pipeline Network Market Segmental Analysis :

By Pipe Type:

Based on pipe type, the district cooling pipeline network market is segmented into pre-insulated steel pipes, polymer pipes, composite pipes, and others.

The pre-insulated steel pipes segment accounted for the largest revenue share in 2024.

- Pre-insulated steel pipes are widely used in district cooling systems due to their durability, thermal insulation efficiency, and ability to handle high pressures.

- These pipes are typically paired with polyurethane foam and HDPE jackets, ensuring minimal heat gain during chilled water transmission.

- Their performance in large-scale commercial and institutional applications makes them the preferred choice for urban infrastructure.

- As per district cooling pipeline network market analysis, long lifecycle and thermal resistance contribute to the segment’s leadership.

The polymer pipes segment is projected to register the fastest CAGR.

- Polymer pipes, including HDPE and PEX, are gaining popularity for their flexibility, corrosion resistance, and ease of installation.

- These pipes are especially useful in projects where ground movement or tight bends are involved.

- Lightweight construction reduces transportation and labor costs, making them suitable for medium-capacity networks.

- For instance, in November 2023, Baker Hughes launched its new PythonPipe™ portfolio, the latest in reinforced thermoplastic pipe (RTP) technology, which enables faster installation, reduced time to first production and lower lifecycle emissions.

- According to district cooling pipeline network market trends, polymer pipes are increasingly used in retrofit projects and developing cities.

By Component:

Based on component, the market is segmented into central cooling plant, pipeline network, pump house, and others.

The central cooling plant segment held the largest district cooling pipeline network market share in 2024.

- Central cooling plants generate chilled water or cooling fluids that are distributed across districts to multiple buildings, improving overall energy efficiency.

- These plants typically utilize centrifugal chillers, absorption chillers, and thermal energy storage to manage peak loads.

- Centralized cooling helps in space saving, noise reduction, and carbon emission control at the building level.

- District cooling pipeline network market trends indicate that urban sustainability policies are boosting investment in centralized plant infrastructure.

The pipeline network segment is expected to witness the fastest CAGR.

- The pipeline network is the backbone of any district cooling system, connecting the cooling plant to the end-users via insulated transmission and distribution pipes.

- Innovations in joint sealing, pre-fabricated connections, and leak detection systems are enhancing reliability and operational safety.

- Smart monitoring systems are being integrated to improve predictive maintenance and reduce downtime.

- As per district cooling pipeline network market analysis, investment in advanced pipeline infrastructure is key to long-term system performance.

By Cooling Fluid:

Based on cooling fluid, the district cooling pipeline network market is segmented into water, glycol-based fluids, and other fluids.

The water segment accounted for the largest revenue share in 2024.

- Water is the most commonly used cooling fluid due to its high thermal conductivity, availability, and non-toxic nature.

- It is suitable for closed-loop systems and is widely used in both commercial and residential district cooling networks.

- Regulatory authorities favor water-based systems for their safety and environmental compatibility.

- As per the district cooling pipeline network market demand, the use of water remains dominant due to system design simplicity and efficiency.

The glycol-based fluids segment is projected to grow at the fastest CAGR.

- Glycol-based fluids, such as ethylene glycol or propylene glycol mixtures, are used in regions with extreme climates to prevent fluid freezing.

- These fluids offer enhanced freeze protection and thermal stability, especially in applications involving variable outdoor temperatures.

- They are commonly used in hybrid systems and in pipeline segments exposed to potential freezing risks.

- District cooling pipeline network market expansion is supported by glycol systems in geographically diverse and weather-sensitive regions.

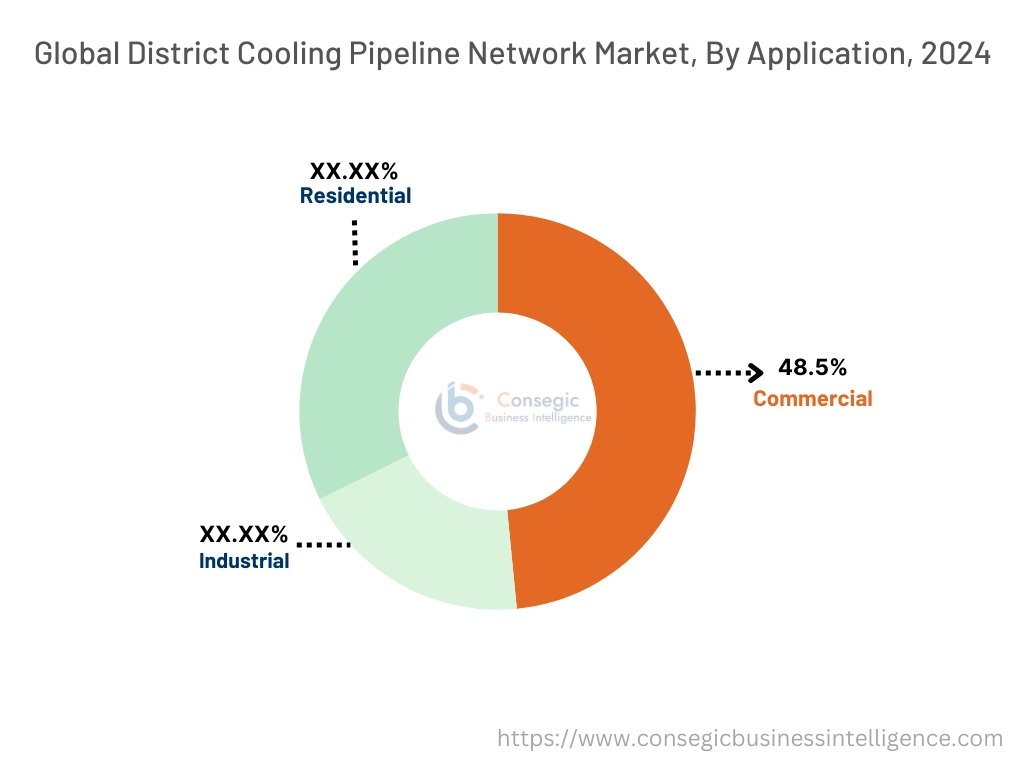

By Application:

Based on application, the market is segmented into residential, commercial, and industrial.

The commercial segment accounted for the largest district cooling pipeline network market share of 48.5% in 2024.

- Commercial applications, including office buildings, shopping malls, hotels, and hospitals, rely heavily on centralized cooling for space optimization and energy savings.

- District cooling offers consistent comfort, energy cost reduction, and reduced maintenance over traditional air conditioning systems.

- The segment benefits from high requirement in rapidly growing urban hubs across the Middle East, Southeast Asia, and Europe.

- Hence, commercial expansion projects and smart city developments are driving the district cooling pipeline network market demand.

The industrial segment is projected to witness the fastest CAGR.

- Industrial facilities utilize district cooling to maintain equipment temperature, stabilize manufacturing environments, and improve energy efficiency.

- Sectors such as pharmaceuticals, data centers, and electronics require consistent cooling for operational reliability.

- The adoption of sustainable industrial practices and carbon reduction goals is promoting the shift from in-house chillers to district networks.

- The district cooling pipeline network market growth is supported by increasing demand for reliable cooling solutions in large-scale industrial clusters.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

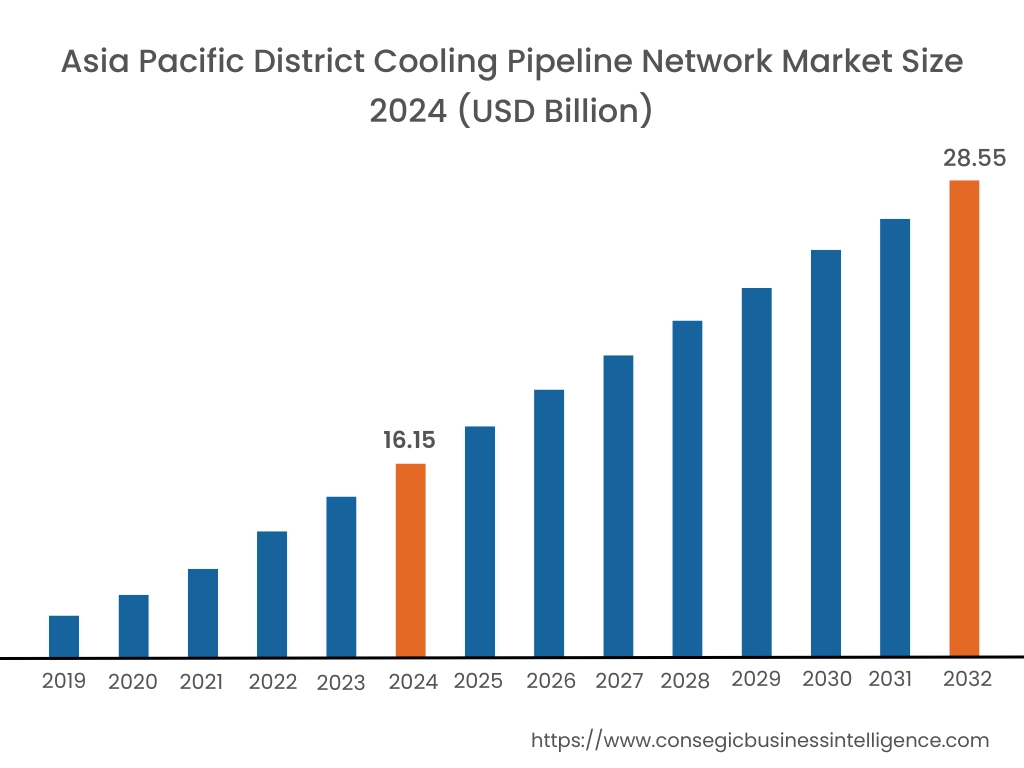

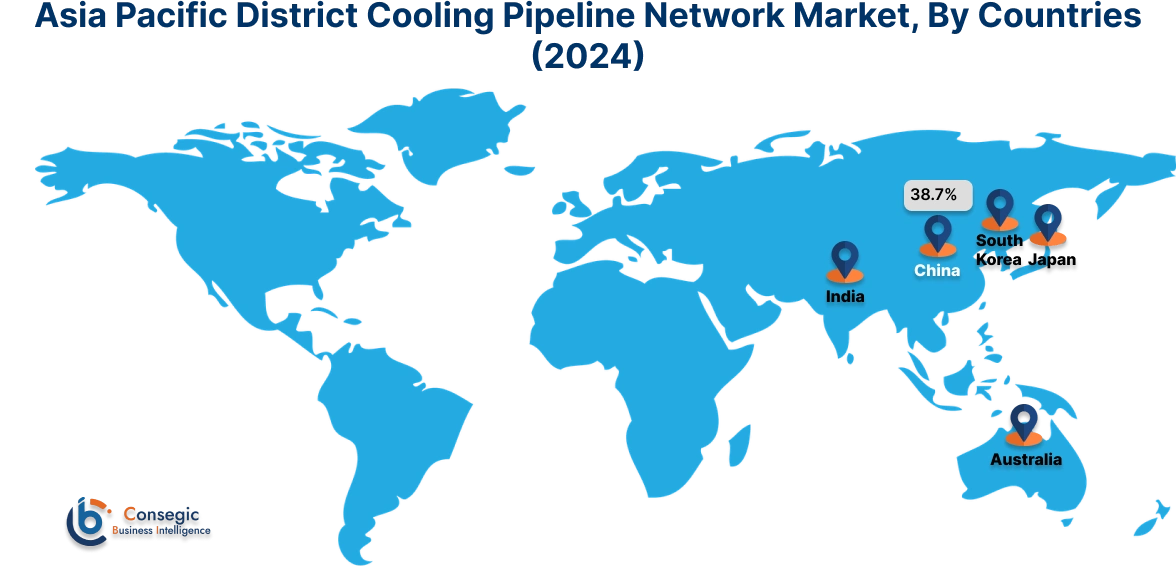

Asia Pacific region was valued at USD 16.15 Billion in 2024. Moreover, it is projected to grow by USD 17.04 Billion in 2025 and reach over USD 28.55 Billion by 2032. Out of this, China accounted for the maximum revenue share of 38.7%.Asia-Pacific is experiencing the substantial growth in the district cooling pipeline network industry, fueled by massive urban development, rising temperatures, and increasing pressure on electricity grids. Countries like China, India, Japan, and South Korea are deploying pipeline-based cooling networks in commercial, governmental, and residential clusters. Market analysis shows a strong shift toward smart grid integration, chilled water storage systems, and insulated pipelines with enhanced thermal conductivity. In rapidly urbanizing regions, district cooling is being positioned as a core element of smart city infrastructure, supported by government mandates and energy efficiency incentives. Additionally, growing participation of international EPC contractors and technology providers is strengthening the regional ecosystem.

North America is estimated to reach over USD 34.65 Billion by 2032 from a value of USD 19.83 Billion in 2024 and is projected to grow by USD 20.91 Billion in 2025. North America is steadily advancing in district cooling applications, particularly in urban zones and institutional campuses where centralized systems offer significant operational and energy-saving benefits. In the United States and Canada, integration of district cooling networks is growing in commercial business districts, universities, and healthcare complexes. Market analysis indicates that emphasis on reducing peak electricity loads and aligning with green building certifications is encouraging investment in pre-insulated pipelines and leak detection systems. Growth in this region is supported by decarbonization targets, public-private partnerships, and thermal storage integration designed to enhance grid stability and environmental performance.

Europe remains a strategically evolving market, with adoption driven by energy performance directives and decarbonization mandates. Countries such as Sweden, Germany, and France are modernizing their thermal infrastructure to include both heating and cooling solutions through district energy systems. Market analysis highlights that district cooling is gaining traction in southern European cities due to rising temperatures and need for low-carbon cooling. Retrofitting of historical urban infrastructure is generating demand for compact, corrosion-resistant pipeline networks that can be deployed in dense areas. The market opportunity in Europe is amplified by EU-level funding for sustainable cities, where combined district heating and cooling networks are positioned as critical enablers of climate-neutral development.

The Middle East is one of the most established and fastest-expanding regions for district cooling networks due to its extreme climate and large-scale real estate developments. The UAE, Saudi Arabia, and Qatar have implemented extensive pipeline infrastructure to service hotels, malls, and government buildings. Market analysis underscores the importance of centralized cooling in reducing energy consumption for air conditioning, which accounts for a significant portion of electricity use in the region. Africa, though at an earlier stage, is beginning to explore centralized solutions in countries such as Egypt and South Africa, particularly in commercial and institutional projects. The district cooling pipeline network market opportunity in this region is bolstered by government-backed sustainability goals and the need for long-term resource efficiency.

Latin America is an emerging market for district cooling, with early adoption seen in select urban zones in Brazil, Mexico, and Colombia. While the region primarily relies on standalone HVAC systems, rising urban temperatures and the drive for low-emission infrastructure are prompting interest in centralized pipeline-based cooling. Market analysis suggests that commercial real estate developers and special economic zones are beginning to recognize the benefits of district systems for cost savings and carbon footprint reduction. Opportunities exist in new city planning initiatives, especially in climate-vulnerable coastal regions where the need for scalable and efficient cooling is steadily rising.

Top Key Players and Market Share Insights:

The district cooling pipeline network market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (r&d), product innovation, and end-user launches to hold a strong position in the global district cooling pipeline network market. Key players in the district cooling pipeline network industry include -

- Veolia (France)

- ENGIE (France)

- Fortum (Finland)

- Vattenfall (Sweden)

- Uniper (Germany)

- Tabreed (National Central Cooling Company PJSC) (United Arab Emirates)

- Emirates Central Cooling Systems Corporation (Empower) (United Arab Emirates)

- Enwave Energy Corporation (Canada)

- Brugg Pipes (Switzerland)

- Logstor (Denmark)

Recent Industry Developments :

Partnerships:

- In July 2023, Emicool and Kamstrup signed an official partnership contract to drive innovation in cooling meter technology. With this partnership, Emicool aimed to expand its industry presence and energize over 500,000 TRs in the next five years.

District Cooling Pipeline Network Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 104.01 Billion |

| CAGR (2025-2032) | 7.2% |

| By Pipe Type |

|

| By Component |

|

| By Cooling Fluid |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the District Cooling Pipeline Network Market? +

District Cooling Pipeline Network Market size is estimated to reach over USD 104.01 Billion by 2032 from a value of USD 59.64 Billion in 2024 and is projected to grow by USD 62.87 Billion in 2025, growing at a CAGR of 7.2% from 2025 to 2032.

What specific segmentation details are covered in the District Cooling Pipeline Network Market report? +

The District Cooling Pipeline Network market report includes specific segmentation details for pipe type, component, cooling fluid and application.

What are the applications of the District Cooling Pipeline Network Market? +

The applications of the District Cooling Pipeline Network Market are residential, commercial, and industrial.

Who are the major players in the District Cooling Pipeline Network Market? +

The key participants in the District Cooling Pipeline Network market are Veolia (France), ENGIE (France), Fortum (Finland), Vattenfall (Sweden), Uniper (Germany), Tabreed (National Central Cooling Company PJSC) (United Arab Emirates), Emirates Central Cooling Systems Corporation (Empower) (United Arab Emirates), Enwave Energy Corporation (Canada), Brugg Pipes (Switzerland) and Logstor (Denmark).