- Summary

- Table Of Content

- Methodology

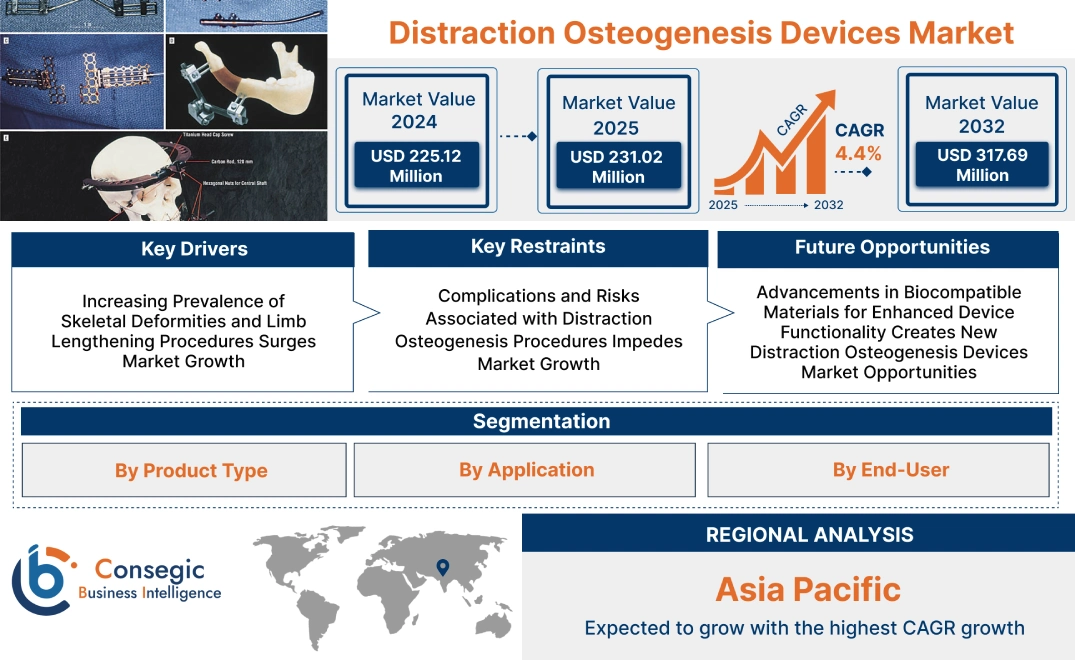

Distraction Osteogenesis Devices Market Size:

Distraction Osteogenesis Devices Market size is estimated to reach over USD 317.69 Million by 2032 from a value of USD 225.12 Million in 2024 and is projected to grow by USD 231.02 Million in 2025, growing at a CAGR of 4.4% from 2025 to 2032.

Distraction Osteogenesis Devices Market Scope & Overview:

Distraction osteogenesis devices are medical tools used in orthopedics and reconstructive surgeries to promote bone distraction osteogenesis devices market growth through gradual mechanical stretching. These devices are primarily used for bone lengthening, deformity correction, and facial reconstructive procedures. The devices offer features like adjustable mechanisms, high precision, and minimal patient discomfort. They promote controlled bone regeneration and reduce the need for complex surgeries.

Its benefits include faster recovery times, reduced surgical risk, and improved patient outcomes. These devices are widely applied in the treatment of congenital deformities, limb length discrepancies, and craniofacial reconstruction. Its end-use industries are healthcare, particularly in hospitals, orthopedic centers, and specialized clinics. They play a crucial role in improving treatment outcomes for patients undergoing bone-related surgeries.

Distraction Osteogenesis Devices Market Dynamics - (DRO):

Key Drivers:

Increasing Prevalence of Skeletal Deformities and Limb Lengthening Procedures Surges Market Growth

Distraction osteogenesis devices are increasingly being used for limb lengthening and the correction of skeletal deformities. This technique, which involves the gradual stretching of bone segments, is highly effective in treating conditions like congenital limb length discrepancies and post-traumatic deformities. In particular, limb lengthening procedures have gained popularity due to their ability to avoid the need for more invasive surgeries. The use of external fixators, such as the Ilizarov apparatus, in treating these deformities continues to rise globally, as they offer a non-invasive alternative to traditional methods.

For example, the Ilizarov system is widely used in orthopedic surgeries for bone deformities and lengthening, offering precise control over the elongation process. As awareness of these benefits spreads and the number of deformity cases increases, the distraction osteogenesis devices market trend continues to rise.

Key Restraints:

Complications and Risks Associated with Distraction Osteogenesis Procedures Impedes Market Growth

Although distraction osteogenesis is an effective treatment for various skeletal deformities, the procedure does carry certain risks and complications. These may include infection, nerve damage, joint stiffness, and failure of the bone to heal properly during the distraction process. Additionally, the external fixators used in these procedures may cause discomfort and require extended treatment periods. The complexity of the technique and the need for post-operative monitoring can discourage some patients from opting for distraction osteogenesis devices.

These challenges associated with the procedure hinder its widespread adoption, especially in regions where healthcare resources are limited or where patients are hesitant to undergo the lengthy process.

Future Opportunities:

Advancements in Biocompatible Materials for Enhanced Device Functionality Creates New Distraction Osteogenesis Devices Market Opportunities

The future of distraction osteogenesis devices lies in the development of advanced, biocompatible materials that improve device functionality and patient comfort. Researchers are focusing on materials that are lighter, stronger, and more durable, reducing the risk of complications and making the devices easier for patients to tolerate. Additionally, the integration of smart technology, such as sensors that monitor the bone healing process in real time, presents an opportunity to enhance treatment outcomes.

The development of these advanced materials and technologies is expected to increase the effectiveness and acceptance of the devices, driving further distraction osteogenesis devices market trend in the coming years. As these innovations become more widespread, the market will expand significantly.

Distraction Osteogenesis Devices Market Segmental Analysis :

By Product Type:

Based on product type, the distraction osteogenesis devices market is segmented into internal distraction devices and external distraction devices.

The external distraction devices segment accounted for the largest revenue in distraction osteogenesis devices market share in 2024.

- External distraction devices are widely used for limb lengthening and correcting dentofacial deformities. These devices are applied externally and include fixators that gradually apply controlled mechanical force on bones to stimulate distraction osteogenesis devices market growth.

- They are effective for both limb lengthening and orthognathic surgery, offering flexibility, precision, and the ability to correct severe deformities. The segment’s dominance is attributed to the growing adoption in reconstructive surgeries and the increasing number of patients requiring limb lengthening procedures.

- The external fixation devices have witnessed significant technological advancements, with improvements in their design, ease of use, and comfort, leading to enhanced patient compliance.

- The segment continues to be driven by the trend for advanced orthotic devices in both hospitals and orthopedic clinics, and its applications are expanding as the awareness of osteogenesis continues to rise.

- Therefore, according to distraction osteogenesis devices market analysis, the external distraction devices segment remains the largest contributor to the market due to their broad applicability and technological advancements. Their ability to treat a variety of deformities makes them a crucial part of the distraction osteogenesis landscape.

The internal distraction devices segment is anticipated to register the fastest CAGR during the forecast period.

- Internal distraction devices are gaining popularity due to their ability to offer a more discreet and comfortable solution for patients. These devices are implanted inside the body, reducing the visibility of external fixators and enhancing the patient’s aesthetic appearance.

- The internal devices are particularly effective for treating dentofacial deformities and are less prone to infections compared to external devices. As technological innovations improve, these devices are becoming more effective and less invasive.

- The rapid trend in the adoption of minimally invasive surgical techniques is expected to boost the internal distraction devices segment, further fueling its distraction osteogenesis devices market expansion.

- Thus, according to distraction osteogenesis devices market analysis, the internal distraction devices segment is poised for significant growth, driven by the increasing preference for minimally invasive treatments and advancements in internal fixation technologies.

By Application:

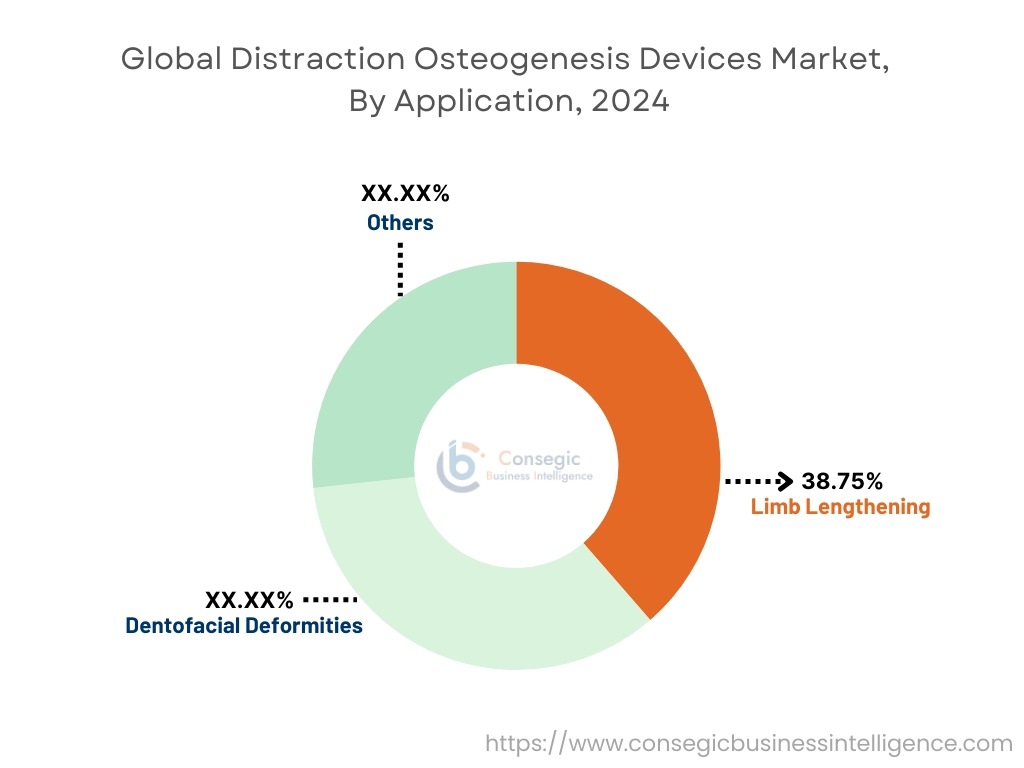

Based on application, the distraction osteogenesis devices market is segmented into dentofacial deformities, limb lengthening, and others.

The limb lengthening application accounted for the largest revenue in distraction osteogenesis devices market share by 38.75% in 2024.

- Limb lengthening procedures are commonly performed to treat short stature caused by congenital defects, trauma, or disease. The devices used for limb lengthening are critical in gradually stimulating bone growth and restoring normal limb proportions.

- The rising number of patients seeking limb lengthening treatments, along with the growing prevalence of skeletal dysplasias and other medical conditions, has contributed to the significant trend for distraction osteogenesis devices in this application.

- Moreover, advancements in technology, such as the introduction of precise and controlled mechanical force delivery systems, have further expanded the capabilities of limb lengthening procedures.

- Therefore, according to market analysis, limb lengthening remains the largest application segment, driven by its widespread use in treating a variety of conditions and the increased trend for surgical interventions in the field of orthopedics.

The dentofacial deformities application is anticipated to register the fastest CAGR during the forecast period.

- Distraction osteogenesis in dentofacial deformities involves the use of distraction devices to correct abnormalities in the jaw and facial bones. It is commonly used for patients with conditions such as craniofacial malformations, congenital defects, and post-traumatic deformities.

- Its application for dentofacial deformities is gaining momentum due to their ability to produce more natural and aesthetic outcomes compared to traditional surgical methods.

- With increasing awareness and advancements in surgical techniques, the distraction osteogenesis devices market demand for these devices in correcting dentofacial deformities is expected to grow rapidly.

- Thus, according to market analysis, the dentofacial deformities segment is expected to experience robust trend, driven by improvements in aesthetic outcomes and the increasing number of patients opting for surgical interventions.

By End-User:

Based on end-users, the distraction osteogenesis devices market is segmented into hospitals, orthopedic clinics, ambulatory surgical centers, and others.

The hospital segment accounted for the largest revenue share in 2024.

- Hospitals are the primary healthcare setting where distraction osteogenesis procedures are performed, especially for complex cases requiring advanced treatment techniques.

- The segment’s dominance is attributed to the availability of specialized surgical teams, advanced technologies, and a wide range of surgical interventions in hospitals. Additionally, the increasing patient pool and rising number of surgeries being performed in hospitals support this trend.

- Hospitals also have the necessary infrastructure to handle post-operative care and rehabilitation, which is crucial in distraction osteogenesis procedures.

- Therefore, according to market analysis, hospitals continue to lead the market due to their capability to manage complex surgeries and provide comprehensive patient care throughout the osteogenesis treatment process.

The ambulatory surgical centers segment is anticipated to register the fastest CAGR during the forecast period.

- Ambulatory surgical centers are increasingly adopting distraction osteogenesis procedures due to their ability to provide cost-effective treatments in a less complex setting. These centers focus on outpatient services, offering patients an efficient and convenient option for undergoing surgeries.

- With advancements in medical technology and minimally invasive procedures, ambulatory surgical centers are becoming an attractive alternative to traditional hospital settings, particularly for less complex limb lengthening and dentofacial deformity surgeries.

- The growing preference for outpatient surgeries and shorter recovery times is expected to drive the distraction osteogenesis devices market demand in this segment.

- Thus, according to market analysis, ambulatory surgical centers are poised to experience rapid growth, driven by the increasing trend toward outpatient surgeries and the adoption of more efficient and patient-friendly procedures.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

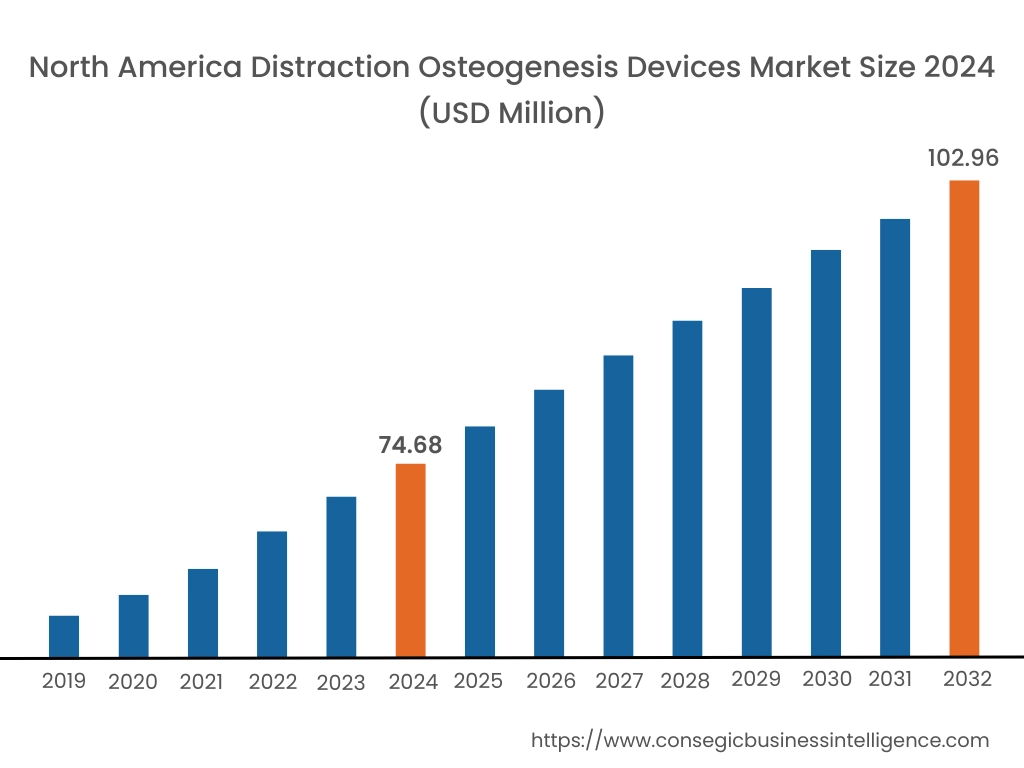

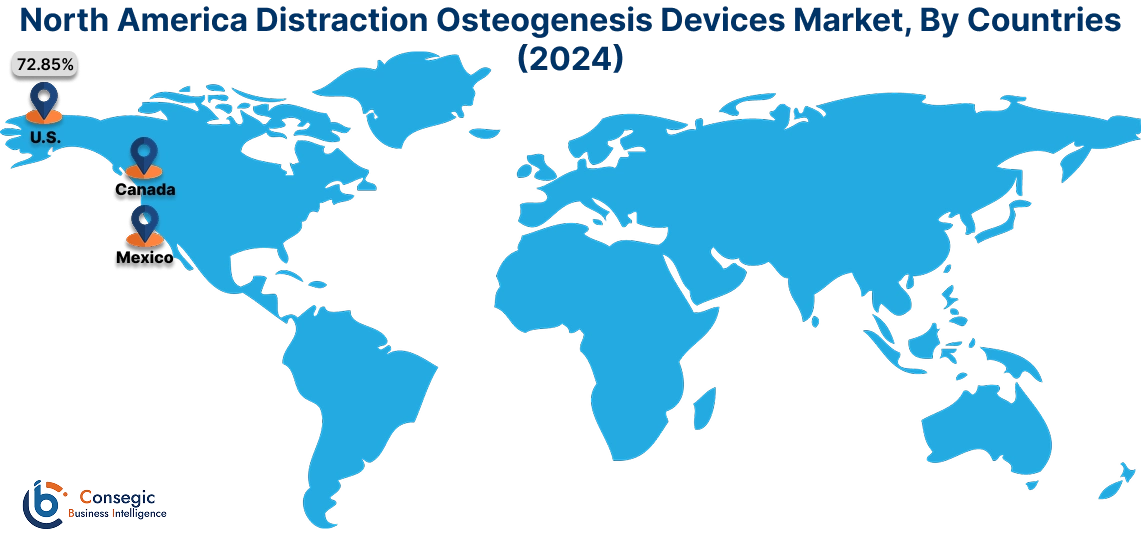

In 2024, North America was valued at USD 74.68 Million and is expected to reach USD 102.96 Million in 2032. In North America, the U.S. accounted for the highest share of 72.85% during the base year of 2024. North America leads the distraction osteogenesis devices market due to advanced healthcare infrastructure, high adoption of innovative technologies, and a significant patient pool requiring orthopedic treatments. The United States is the dominant market in this region, with widespread use of distraction osteogenesis for limb lengthening and deformity correction. The region benefits from favorable reimbursement policies, extensive research and development activities, and a high focus on patient safety, which supports distraction osteogenesis devices market expansion.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 4.8% over the forecast period. The Asia-Pacific region shows substantial potential for growth in the distraction osteogenesis devices market. Countries like China, Japan, and India are witnessing an increasing number of orthopedic procedures, driven by rising healthcare access and improving medical technology. The growing awareness of advanced bone reconstruction techniques contributes to market demand. Additionally, a rising geriatric population and higher incidences of congenital defects and trauma injuries further fuel its need in the region.

In Europe, the market for distraction osteogenesis devices is well-established, with significant contributions from countries like Germany, France, and the United Kingdom. The region’s focus on advanced medical procedures, including orthopedic treatments for complex bone deformities, supports market demand. Furthermore, European countries emphasize minimally invasive procedures and personalized patient care, leading to higher adoption. However, variations in healthcare regulations and reimbursement policies across countries may create some market challenges.

The Middle East and Africa are emerging markets for distraction osteogenesis devices, with increasing demand driven by improving healthcare infrastructure and higher patient awareness. Countries like the United Arab Emirates and Saudi Arabia are leading the market in the region, with growing healthcare investments. However, the market in many African countries faces challenges due to limited access to advanced medical devices and high treatment costs. Efforts to enhance healthcare systems and expand access to orthopedic services are expected to contribute to market development.

Latin America is experiencing steady growth in the distraction osteogenesis devices market. Brazil and Mexico are the largest markets in this region, with increasing awareness of orthopedic procedures and advancements in medical technology. The adoption of modern treatment methods, including distraction osteogenesis, is rising due to improved healthcare infrastructure and a growing focus on specialized care. However, challenges such as economic disparity and limited insurance coverage in rural areas may hinder broader market access.

Top Key Players & Market Share Insights:

The Global Distraction Osteogenesis Devices Market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the Global Distraction Osteogenesis Devices Market. Key players in the Distraction Osteogenesis Devices industry include-

- Orthofix Medical Inc. (United States)

- Stryker Corporation (United States)

- Zimmer Biomet Holdings, Inc. (United States)

- Trumed Healthcare (India)

- MEDARTIS AG (Switzerland)

- Medtronic PLC (Ireland)

- Smith & Nephew PLC (United Kingdom)

- DePuy Synthes (United States)

- Shanghai United Orthopaedic Technology Co., Ltd. (China)

- Biomet, Inc. (United States)

Recent Industry Developments :

Product Launches:

- In May 2024, Agilent Technologies introduced the AdvanceBio Spin Columns. These gel-filtration-based spin columns are designed for efficient desalting and buffer exchange of proteins or oligonucleotides under aqueous conditions, preserving their native structure. They are available in both analytical and semipreparative scales, as well as 96-sample plates for high-throughput settings.

Partnerships & Collaborations:

- In January 2023, Sartorius extended its strategic collaboration with RoosterBio Inc. to address purification challenges and establish scalable downstream manufacturing processes for exosome-based therapies. This partnership aims to strengthen Sartorius' bioprocessing portfolio.

Distraction Osteogenesis Devices Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 317.69 Million |

| CAGR (2025-2032) | 4.4% |

| By Product Type |

|

| By Application |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Distraction Osteogenesis Devices Market? +

In 2024, the Distraction Osteogenesis Devices Market was USD 225.12 million.

What will be the potential market valuation for the Distraction Osteogenesis Devices Market by 2032? +

In 2032, the market size of Distraction Osteogenesis Devices Market is expected to reach USD 317.69 million.

What are the segments covered in the Distraction Osteogenesis Devices Market report? +

The product type, application and end-user are the segments covered in this report.

Who are the major players in the Distraction Osteogenesis Devices Market? +

Orthofix Medical Inc. (United States), Stryker Corporation (United States), Zimmer Biomet Holdings, Inc. (United States), Medtronic PLC (Ireland), Smith & Nephew PLC (United Kingdom), DePuy Synthes (United States), Shanghai United Orthopaedic Technology Co., Ltd. (China), Biomet, Inc. (United States), Trumed Healthcare (India), MEDARTIS AG (Switzerland) are the major players in the Distraction Osteogenesis Devices market.