- Summary

- Table Of Content

- Methodology

Digital Water Solutions Market Scope & Overview:

Digital water solutions encompass advanced technologies and tools designed to monitor, manage, and optimize water resources and infrastructure. These solutions integrate IoT devices, data analytics, cloud computing, and smart sensors to provide real-time insights into water quality, distribution, and usage. They are widely utilized across municipal, industrial, and agricultural sectors to enhance water management and ensure operational efficiency.

These systems offer functionalities such as automated leak detection, predictive maintenance, and remote monitoring, ensuring accurate and efficient management of water networks. Digital water solutions are designed to integrate seamlessly with existing infrastructure, enabling scalability and adaptability to diverse operational requirements. Their data-driven approach ensures precise decision-making and resource optimization.

End-users include water utilities, industrial facilities, and agricultural organizations seeking innovative tools to improve water management processes. These solutions play a critical role in modernizing water systems and addressing challenges associated with water distribution and resource conservation.

Digital Water Solutions Market Size:

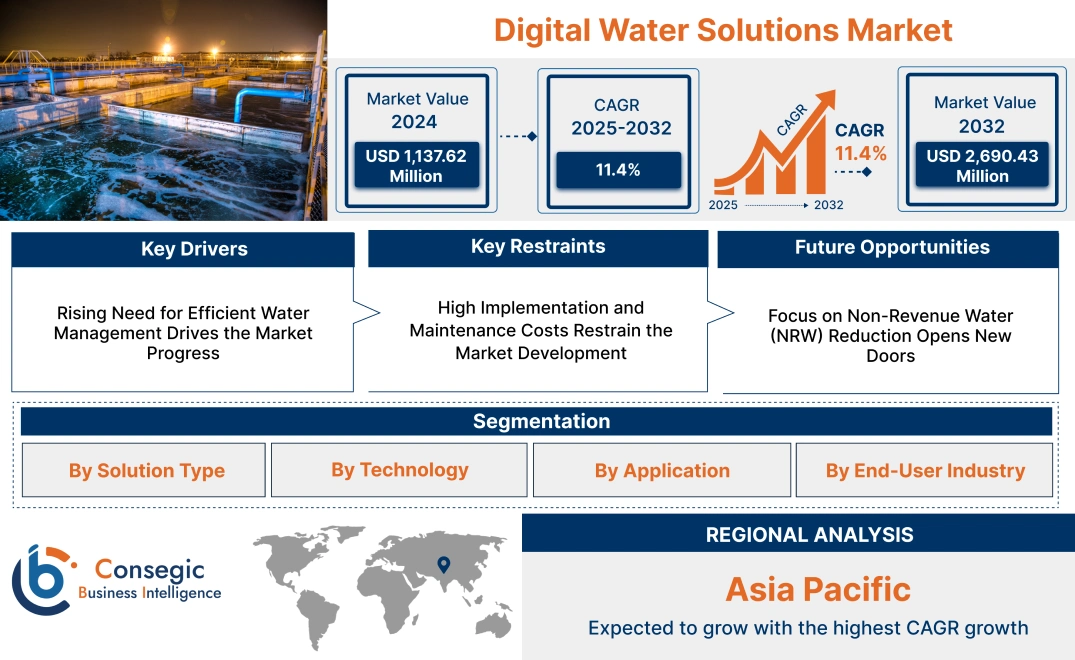

Digital Water Solutions Market size is estimated to reach over USD 2,690.43 Million by 2032 from a value of USD 1,137.62 Million in 2024 and is projected to grow by USD 1,246.58 Million in 2025, growing at a CAGR of 11.4% from 2025 to 2032.

Digital Water Solutions Market Dynamics - (DRO) :

Key Drivers:

Rising Need for Efficient Water Management Drives the Market Progress

The global scarcity of freshwater resources, combined with rising water consumption across industries and households, is intensifying the demand for efficient water management systems. Smart technologies are emerging as a solution to address these challenges by providing real-time monitoring, automated leak detection, and predictive maintenance.

These systems enable utilities to track water flow, pressure, and quality, allowing immediate identification and resolution of inefficiencies such as leaks or excessive usage. By leveraging data analytics, utilities forecast demand, reduce operational wastage, and allocate resources more effectively.

Additionally, such technologies contribute to cost savings by minimizing water loss and lowering maintenance expenses. As urbanization and industrialization continue to grow, the adoption of smart water solutions is becoming essential for achieving sustainability and meeting regulatory requirements. These advancements align with trends in resource optimization and play a critical role in addressing global water challenges, fueling the digital water solutions market growth.

Key Restraints:

High Implementation and Maintenance Costs Restrain the Market Development

The adoption of advanced water management technologies comes with substantial financial restraints. Digital water systems necessitate significant upfront investments in hardware, such as sensors and smart meters, as well as in software platforms and integration services. The costs associated with deploying these solutions, particularly in extensive water networks, are prohibitive for smaller utilities or regions operating on limited budgets.

Additionally, these systems require ongoing maintenance, regular updates, and potential scalability upgrades to remain effective, which adds to the financial burden over time. For utilities in developing regions or those serving low-revenue areas, these costs deter adoption, despite the long-term efficiency and sustainability benefits of digital solutions.

The financial constraints posed by implementation and maintenance create disparities in access to modern water management technologies, slowing the digital water solutions market demand in cost-sensitive sectors and regions.

Future Opportunities :

Focus on Non-Revenue Water (NRW) Reduction Opens New Doors

Non-revenue water (NRW) losses, resulting from leaks, unauthorized consumption, and inefficiencies in water distribution systems, are a significant challenge for utilities worldwide. These losses not only reduce revenue but also exacerbate water scarcity issues, particularly in regions with limited resources. Smart water systems offer innovative solutions to address NRW challenges through real-time leak detection, pressure management, and advanced analytics.

By enabling utilities to identify and resolve issues promptly, these systems help minimize water wastage and improve operational efficiency. The integration of smart meters and IoT-enabled devices further enhances monitoring and control, providing actionable insights into water distribution networks.

As utilities increasingly prioritize NRW reduction to ensure sustainable resource utilization and improve financial performance, the adoption of smart water technologies is accelerating, creating significant digital water solutions market opportunities.

Top Key Players and Market Share Insights:

The Digital Water Solutions market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Digital Water Solutions market. Key players in the Digital Water Solutions industry include -

- Siemens AG (Germany)

- Schneider Electric (France)

- IBM Corporation (USA)

- Bentley Systems, Inc. (USA)

- Honeywell International Inc. (USA)

- ABB Ltd. (Switzerland)

- Xylem Inc. (USA)

- SUEZ Group (France)

- Emerson Electric Co. (USA)

- General Electric Company (GE) (USA)

Digital Water Solutions Market Segmental Analysis :

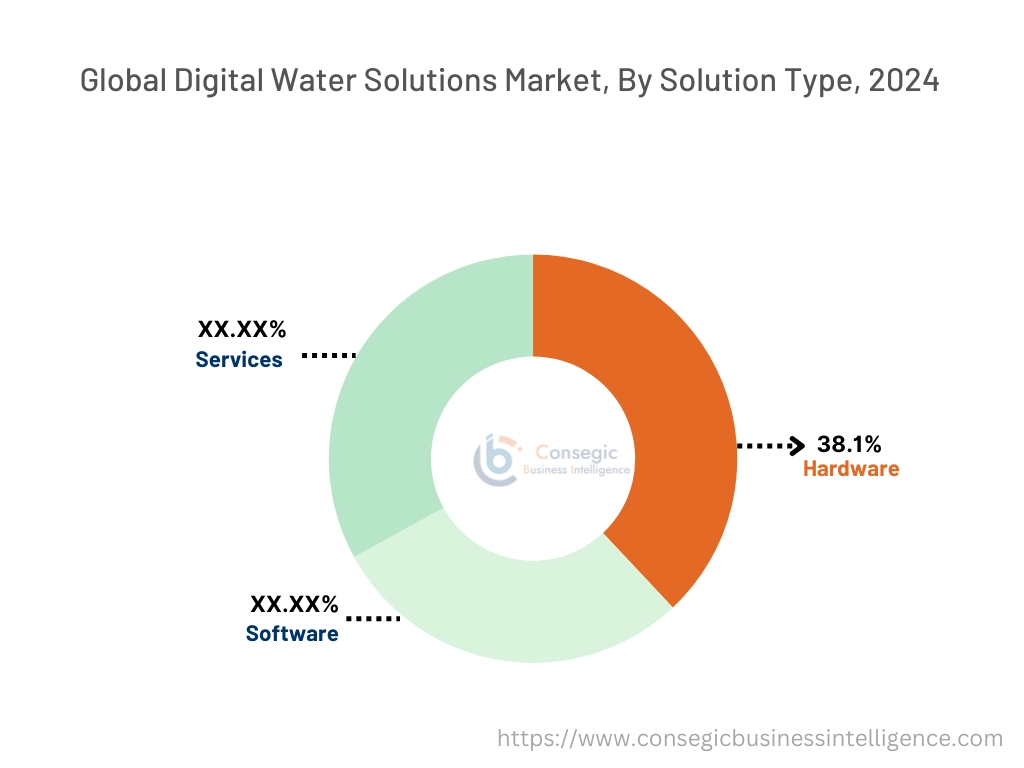

By Solution Type:

Based on solution type, the market is segmented into hardware, software, and services.

The hardware segment accounted for the largest revenue of 38.1% of the total digital water solutions market share in 2024.

- Advanced sensors and meters enable precise water quality monitoring and leak detection, forming the backbone of digital water systems.

- Communication devices ensure seamless data transmission, enabling real-time monitoring and analysis for efficient water management.

- The increasing adoption of smart metering systems in municipal and industrial sectors supports the dominance of this segment.

- As per digital water solutions market trends, the hardware segment remains critical in enabling accurate data acquisition and efficient network operation.

The services segment is expected to register the fastest CAGR during the forecast period.

- Consulting services assist organizations in adopting tailored solutions for water management challenges, driving efficiency.

- Integration and deployment services ensure smooth implementation of advanced technologies like IoT and AI.

- Maintenance services play a vital role in ensuring long-term operational efficiency and reducing downtime in digital water systems.

- The growth of this segment is supported by increasing demand for expert assistance in deploying and maintaining complex water management solutions, contributing to the digital water solutions market expansion.

By Technology:

Based on technology, the market is segmented into IoT, AI & machine learning, cloud computing, digital twin, and others.

The IoT segment held the largest revenue of the total digital water solutions market share in 2024.

- IoT-enabled devices provide real-time monitoring and control of water systems, enhancing decision-making and resource optimization.

- Smart sensors integrated with IoT platforms enable advanced features like predictive maintenance and anomaly detection.

- IoT technology is widely adopted in municipal and industrial water management for operational efficiency and cost savings.

- As per the digital water solutions market analysis, the IoT segment dominates due to its extensive application in connecting various water management systems.

The digital twin segment is expected to register the fastest CAGR during the forecast period.

- Digital twins allow virtual simulation of water networks, helping in identifying potential inefficiencies and optimizing operations.

- The ability to model and test scenarios in real-time supports decision-making for water utilities and industrial operators.

- Increasing investments in advanced technologies for efficient resource management drive the adoption of digital twin solutions.

- The rapid adoption of this technology is propelled by its ability to improve sustainability and reduce operational costs, boosting the digital water solutions market growth.

By Application:

Based on application, the market is segmented into water quality monitoring, leak detection, pressure management, and others.

The water quality monitoring segment held the largest revenue share in 2024.

- Advanced monitoring solutions enable real-time detection of contaminants, ensuring compliance with regulatory standards.

- Municipalities and industrial facilities prioritize water quality monitoring to safeguard public health and maintain operational efficiency.

- The integration of IoT and AI technologies enhances the precision and efficiency of water quality analysis.

- As per digital water solutions market analysis, the dominance of this segment reflects its critical role in ensuring safe and sustainable water management practices.

The leak detection segment is expected to register the fastest CAGR during the forecast period.

- Automated leak detection systems minimize water losses and operational disruptions in distribution networks.

- Advanced technologies like AI and IoT help identify leaks at early stages, reducing repair costs and resource wastage.

- Increasing focus on water conservation and sustainability drives the adoption of leak detection systems across industries.

- The segment's rapid growth is fueled by the rising awareness about reducing non-revenue water losses, which further encourages the digital water solutions market expansion.

By End-User Industry:

Based on end-user industry, the market is segmented into municipal, industrial, residential, and commercial.

The municipal segment accounted for the largest revenue share in 2024.

- Municipalities increasingly adopt smart water solutions to improve efficiency, reduce costs, and ensure sustainable resource management.

- Applications like leak detection, quality monitoring, and pressure management are crucial for municipal water networks.

- The adoption of IoT and AI technologies enhances operational efficiency, supporting the segment's dominance.

- Thus, the municipal segment is critical in addressing the growing need for improved water infrastructure and management solutions, fueling the digital water solutions market demand.

The industrial segment is expected to register the fastest CAGR during the forecast period.

- Industries rely on advanced water solutions for applications like process optimization, wastewater treatment, and resource conservation.

- The integration of digital twin technology enhances operational efficiency, enabling precise monitoring and control.

- Increasing regulatory pressure for sustainable water management accelerates the adoption of digital solutions in the industrial sector.

- Therefore, the segment's rapid growth is driven by the rising focus on cost reduction and sustainability in industrial water management practicesTop of Form, creating new digital water solutions market opportunities.

Digital Water Solutions Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 2,690.43 Million |

| CAGR (2025-2032) | 11.4% |

| By Solution Type |

|

| By Technology |

|

| By Application |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

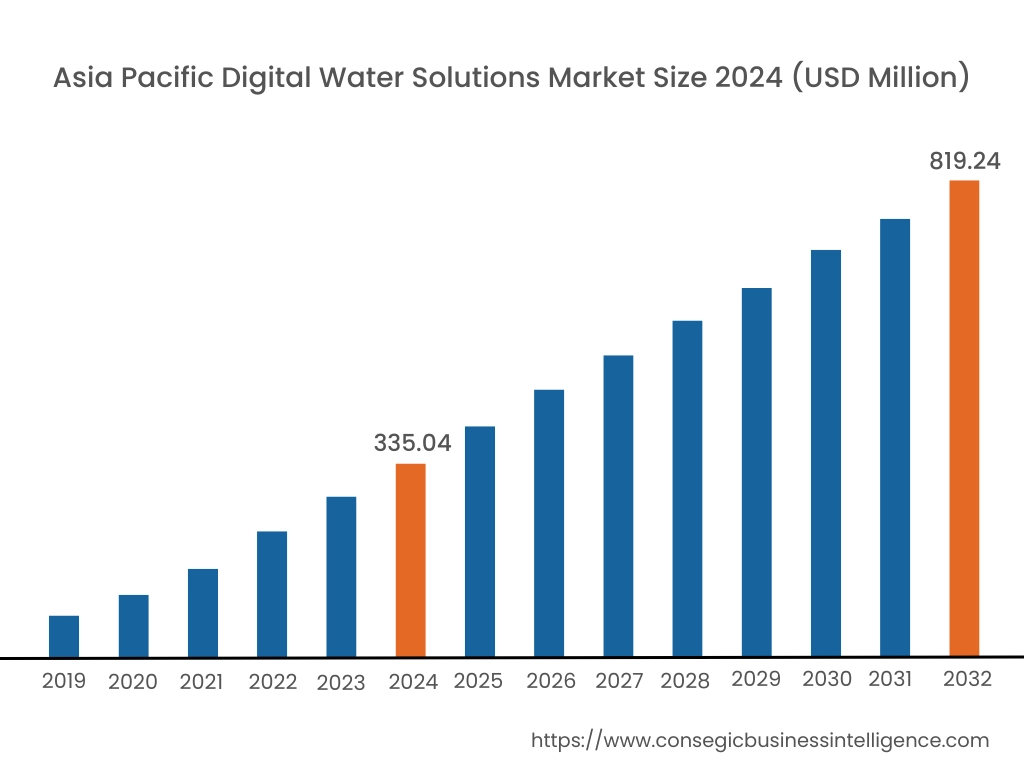

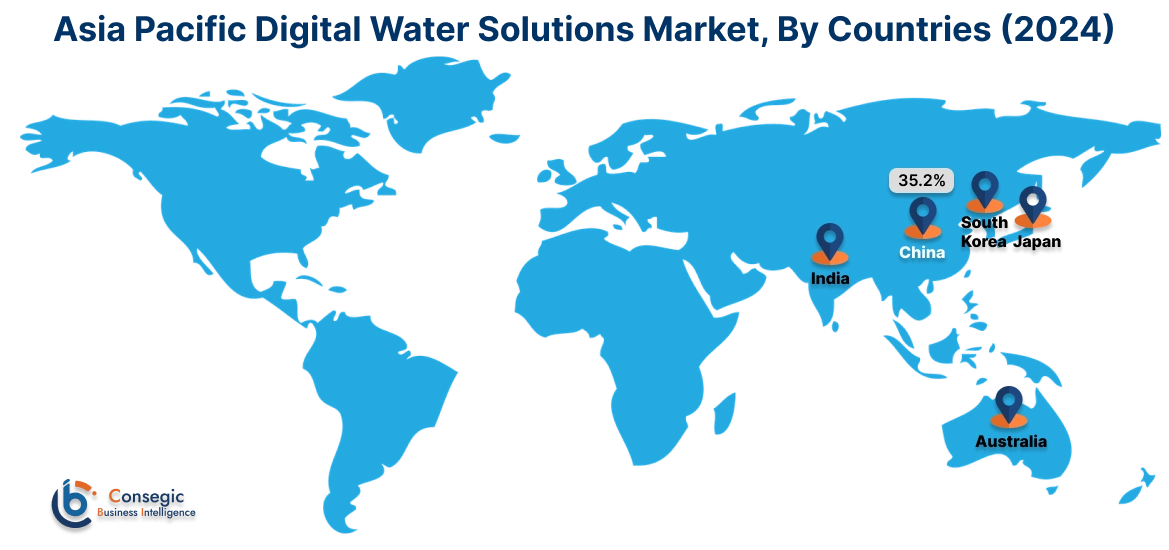

Asia Pacific region was valued at USD 335.04 Million in 2024. Moreover, it is projected to grow by USD 368.17 Million in 2025 and reach over USD 819.24 Million by 2032. Out of this, China accounted for the maximum revenue share of 35.2%. The Asia-Pacific region is witnessing rapid urbanization and industrialization, leading to increased pressure on water resources. Countries such as China, India, and Japan are investing in digital water solutions to address these challenges. A significant trend is the implementation of smart metering systems and real-time water quality monitoring to ensure safe and reliable water supply. As per the digital water solutions market trends, government initiatives aimed at infrastructure development and smart city projects are key drivers for the market growth.

North America is estimated to reach over USD 871.97 Million by 2032 from a value of USD 377.36 Million in 2024 and is projected to grow by USD 412.71 Million in 2025. This region stands as a prominent player in the digital water solutions arena, driven by the early adoption of smart technologies and a robust focus on water conservation. The United States and Canada are at the forefront, implementing advanced metering infrastructure and real-time monitoring systems to enhance water management. A notable trend is the integration of Internet of Things (IoT) devices with cloud-based analytics platforms, enabling utilities to optimize operations and detect anomalies promptly. Analysis indicates that supportive government policies and substantial investments in smart city initiatives further propel the market growth in this region.

Europe exhibits a strong inclination towards sustainable water management practices, with countries like Germany, France, and the United Kingdom leading the charge. The region's stringent environmental regulations and commitment to reducing water wastage have accelerated the adoption of digital solutions. A growing trend is the deployment of advanced data analytics and machine learning algorithms to predict consumption patterns and manage resources efficiently. Analysis reveals that collaborative efforts between public utilities and private tech firms are fostering innovation.

In the Middle East & Africa region, water scarcity issues are prompting the adoption of digital water technologies. Nations like the United Arab Emirates and Saudi Arabia are exploring innovative solutions such as remote monitoring and automated control systems to manage water distribution efficiently. A notable trend is the use of digital platforms for leak detection and predictive maintenance to minimize losses. Analysis indicates that while there is a growing interest in digital solutions, economic diversification efforts and political factors may influence the pace of adoption.

Latin America is gradually embracing digital water solutions, with countries like Brazil and Mexico taking initial steps toward modernization. The focus is on improving water distribution networks and reducing non-revenue water through digital interventions. A developing trend is the adoption of Geographic Information System (GIS) mapping and sensor technologies for better network management.

Recent Industry Developments:

Acquisitions & Mergers:

- In December 2024, Xylem acquired a majority stake in Idrica to enhance water utility solutions by integrating Idrica’s data management and analytics with Xylem Vue. This partnership focuses on addressing challenges like water scarcity and aging infrastructure through real-time insights and streamlined operations. The integration aims to simplify and optimize utility management, reducing costs and improving efficiency.

- In November 2024, Ecolab acquired Barclay Water Management, expanding its water safety solutions portfolio. Barclay’s iChlor Monochloramine System addresses Legionella in drinking water, enhancing water quality and asset longevity with continuous monitoring. The integration with Ecolab’s ECOLAB3D digital platform creates a comprehensive solution for water safety and efficiency. The acquisition brings innovative offerings to North America, aiming to improve water and energy use while ensuring safety and operational performance.

Partnerships & Collaborations:

- In October 2024, Digital Realty partnered with Ecolab to pilot an AI-powered water conservation solution in 35 U.S. data centers, aiming to enhance water use efficiency and reduce environmental impact. The AI solution identifies inefficiencies in cooling systems, potentially saving up to 126 million gallons of potable water annually. Building on a decade-long collaboration, this initiative complements Digital Realty's broader sustainability efforts, including reducing water use intensity and achieving significant CO2 emissions and plastic waste reductions.

Product Launches:

- In September 2024, DuPont introduced the Water Solutions Sustainability Navigator, a digital tool that evaluates the sustainability impacts of various water treatment technologies, including carbon emissions, chemical usage, wastewater, and solid waste. Third-party verified by LRQA, the tool adheres to ISO standards and enables users to compare technologies like reverse osmosis, ultrafiltration, ion exchange resins, and membrane bioreactors. It helps identify solutions with lower environmental impact and operational costs, promoting sustainability in water treatment.

Key Questions Answered in the Report

What is the size of the Digital Water Solutions Market? +

The Digital Water Solutions Market size is estimated to reach over USD 2,690.43 Million by 2032 from a value of USD 1,137.62 Million in 2024 and is projected to grow by USD 1,246.58 Million in 2025, growing at a CAGR of 11.4% from 2025 to 2032.

What are the key segments in the Digital Water Solutions Market? +

The Digital Water Solutions market is segmented by solution type (hardware, software, services), technology (IoT, AI & machine learning, cloud computing, digital twin, others), application (water quality monitoring, leak detection, pressure management, others), end-user industry (municipal, industrial, residential, commercial), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which segment is expected to grow the fastest in the Digital Water Solutions Market? +

The services segment is expected to register the fastest CAGR during the forecast period. This growth is driven by the increasing demand for consulting, integration, and maintenance services to deploy and manage complex water management technologies, particularly as utilities and industries seek efficiency and sustainability in their water systems.

Who are the major players in the Digital Water Solutions Market? +

Key players in the Digital Water Solutions market include Siemens AG (Germany), Schneider Electric (France), ABB Ltd. (Switzerland), Xylem Inc. (USA), SUEZ Group (France), Emerson Electric Co. (USA), General Electric Company (GE) (USA), IBM Corporation (USA), Bentley Systems, Inc. (USA), and Honeywell International Inc. (USA).