- Summary

- Table Of Content

- Methodology

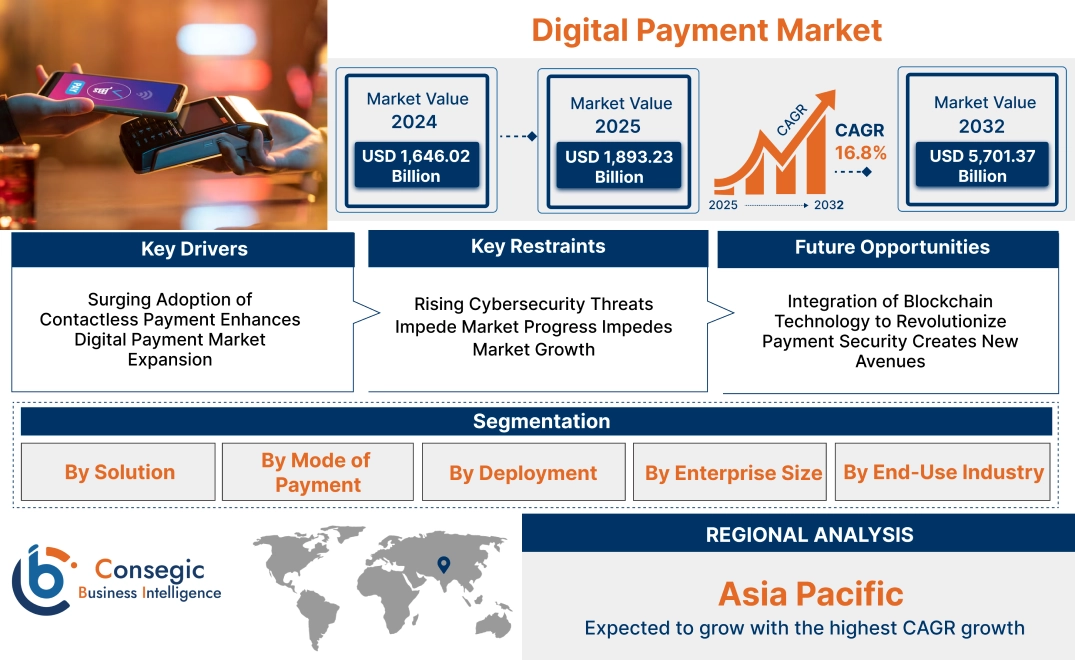

Digital Payment Market Size:

Digital Payment Market size is estimated to reach over USD 5,701.37 Billion by 2032 from a value of USD 1,646.02 Billion in 2024 and is projected to grow by USD 1,893.23 Billion in 2025, growing at a CAGR of 16.8% from 2025 to 2032.

Digital Payment Market Scope & Overview:

Digital payment refers to the process of making transactions electronically through online or mobile platforms, replacing traditional methods like cash or checks. These payments are secure, fast, and convenient, offering features such as encryption for data protection and integration with various financial services.

Their benefits include increased transaction speed, enhanced security, and reduced reliance on physical currency. They simplify payments for both consumers and businesses, improving overall efficiency.

They are used in e-commerce, retail, financial services, and government transactions. They are integral to industries such as banking, telecommunications, and transportation, where they streamline operations and provide seamless customer experiences.

Digital Payment Market Dynamics - (DRO) :

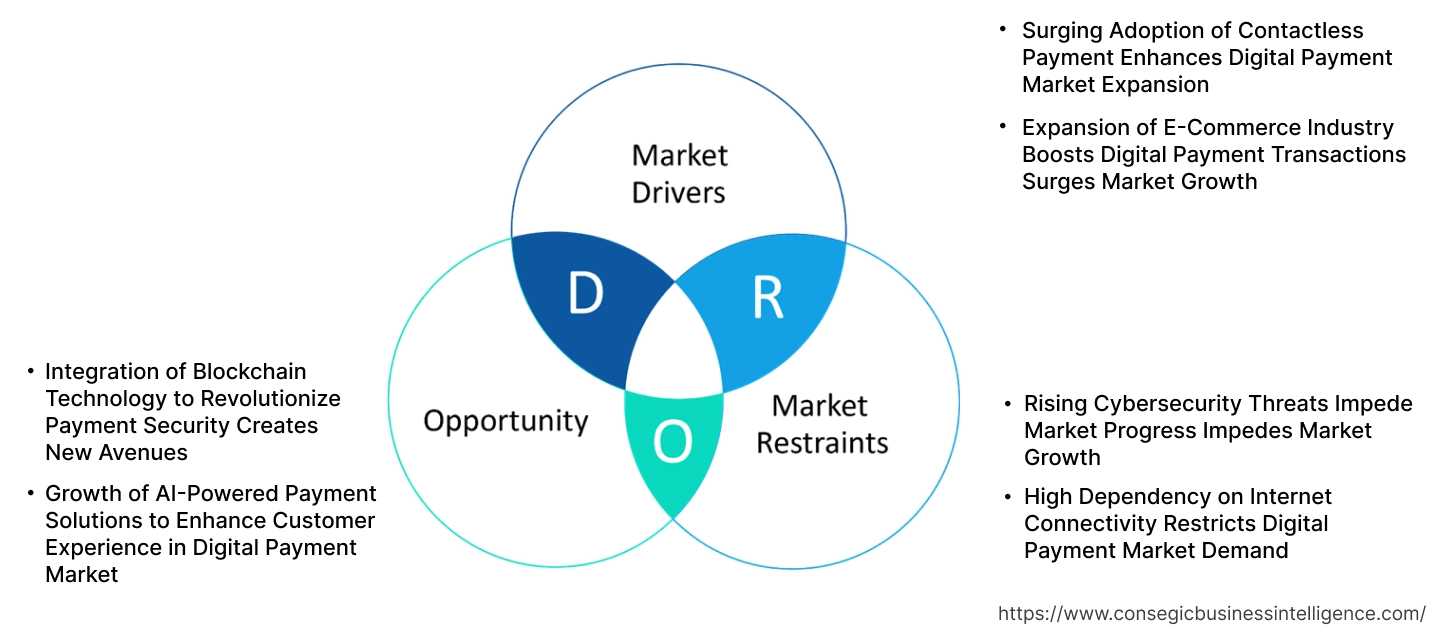

Key Drivers:

Surging Adoption of Contactless Payment Enhances Digital Payment Market Expansion

The widespread adoption of contactless payment technology is transforming digital transactions, enhancing convenience, security, and speed. Contactless payments use Near Field Communication (NFC) and Radio Frequency Identification (RFID) technology, enabling users to complete transactions quickly without inserting a card or entering a PIN. Businesses are integrating this technology to offer seamless transactions, reducing customer wait times at retail stores, restaurants, and transit systems. Governments and financial institutions are promoting contactless payment adoption to drive cashless economies. For instance, major retailers and public transport systems worldwide are upgrading their payment infrastructure to support tap-and-go payments, fostering the trend of such solutions.

Therefore, the growing acceptance of contactless transactions is accelerating digital payment market growth.

Expansion of E-Commerce Industry Boosts Digital Payment Transactions Surges Market Growth

The rapid expansion of the e-commerce industry is significantly increasing the demand for these solutions. Online retail platforms rely on secure and efficient payment gateways to process transactions, ensuring seamless shopping experiences. Digital wallets, UPI-based payments, and Buy Now Pay Later (BNPL) options are being widely integrated into e-commerce platforms, offering customers multiple payment choices. Additionally, the rise of mobile shopping applications is further fueling digital transactions. Companies are investing in AI-powered fraud detection systems to enhance security, promoting digital payments among consumers. For example, global e-commerce giants like Amazon and Alibaba are continuously enhancing their payment infrastructures to improve checkout experiences.

Therefore, the growing e-commerce sector is propelling its adoption.

Key Restraints:

Rising Cybersecurity Threats Impede Market Progress Impedes Market Growth

The increasing incidence of cyberattacks, data breaches, and fraudulent activities poses a major challenge for the digital payment industry. Hackers continuously exploit vulnerabilities in online payment gateways, mobile wallets, and banking applications, leading to financial losses and data theft. Businesses must invest heavily in cybersecurity measures such as multi-factor authentication, encryption, and real-time fraud detection to mitigate risks. Additionally, regulatory compliance requirements further complicate operations for providers. For instance, stringent data protection laws like the General Data Protection Regulation (GDPR) in Europe and the California Consumer Privacy Act (CCPA) in the U.S. impose strict penalties for security lapses.

These growing cybersecurity risks are hindering the seamless expansion of digital payment solutions.

High Dependency on Internet Connectivity Restricts Digital Payment Market Demand

The effectiveness of these solutions depends on stable and high-speed internet connectivity. Regions with poor network infrastructure face significant challenges in adopting digital transactions, limiting market penetration in rural and underdeveloped areas. Users in such locations often experience transaction failures, delays, and connectivity issues, discouraging them from adopting these methods. Additionally, network downtimes during peak transaction hours can lead to business losses and customer dissatisfaction. Developing economies continue to struggle with internet accessibility, creating a barrier to its seamless adoption.

Therefore, internet connectivity issues act as a significant restraint to the digital payment market.

Future Opportunities :

Integration of Blockchain Technology to Revolutionize Payment Security Creates New Avenues

The adoption of blockchain technology in digital payments is expected to enhance transaction security, transparency, and efficiency. Blockchain eliminates intermediaries, reducing transaction costs and processing times while ensuring secure peer-to-peer transactions. Financial institutions and fintech companies are exploring decentralized payment systems to combat fraud, increase trust, and facilitate cross-border transactions. For instance, global payment giants like Visa and Mastercard are investing in blockchain-based solutions to improve transaction reliability and security. The adoption of Central Bank Digital Currencies (CBDCs) is also gaining traction, further supporting blockchain integration.

Therefore, the rise of blockchain-based payment solutions is poised to create lucrative digital payment market opportunities.

Growth of AI-Powered Payment Solutions to Enhance Customer Experience in Digital Payment Market

Artificial Intelligence (AI) is expected to revolutionize the landscape by offering predictive analytics, fraud detection, and personalized payment experiences. AI-driven chatbots, virtual assistants, and biometric authentication are enhancing user convenience and security. Businesses are leveraging AI to analyze spending patterns, optimize payment processing, and offer real-time customer support. Additionally, AI-powered fraud detection algorithms are improving risk assessment and preventing unauthorized transactions. For instance, PayPal and Stripe have integrated AI-driven security features to enhance fraud prevention.

Therefore, AI-powered innovations are set to unlock significant digital payment market opportunities.

Digital Payment Market Segmental Analysis :

By Solution:

Based on the solution, the market is segmented into payment processing, payment gateway, payment security and fraud management, and point of sale (POS) solutions.

Payment Processing accounted for the largest revenue in digital payment market share in 2024.

- Payment processing is the backbone of this ecosystem, enabling transactions to be completed between buyers and sellers.

- It involves various components such as merchant services, payment gateways, and acquiring banks.

- The need for seamless, fast, and secure transactions is driving the trend of payment processing solutions, particularly in e-commerce and retail sectors.

- In addition, technological advancements like tokenization, encryption, and integration with AI are further improving payment processing services.

- Payment processing is essential for ensuring a smooth user experience, with high efficiency and minimal delays in financial transactions.

- Therefore, according to digital payment market analysis, payment processing dominates the segment in terms of revenue and will continue to be the foundational solution for such systems.

Payment Security and Fraud Management is anticipated to register the fastest CAGR during the forecast period.

- As cyber threats and digital fraud increase, businesses are increasingly prioritizing security measures to protect their customers' financial information.

- Payment security involves encryption, two-factor authentication, and fraud detection systems to safeguard against unauthorized transactions.

- Fraud management solutions are key to reducing the risk of chargebacks and financial losses, ensuring that digital transactions are safe and secure.

- Regulatory bodies and industry standards are pushing for stronger security measures to ensure consumer confidence in the digital system.

- With the trend of digital currencies and the rising volume of e-commerce transactions, the need for robust fraud management is expected to increase.

- Thus, according to digital payment market analysis, the surge in cybersecurity concerns makes payment security and fraud management the fastest-growing subsegment.

By Mode of Payment:

Based on the mode of payment, the market is segmented into bank cards, digital currencies, digital wallets, net banking, and others.

Bank Cards accounted for the largest revenue in digital payment market share in 2024.

- Bank cards, including credit, debit, and prepaid cards, remain the most common mode of payment worldwide due to their wide acceptance and ease of use.

- These cards are often integrated with advanced security measures such as EMV chip technology and contactless payment options, enhancing consumer convenience and trust.

- The continued trend of e-commerce, along with the increasing adoption of mobile payments, has boosted the use of bank cards in digital transactions.

- Moreover, bank card usage is supported by financial institutions offering rewards, discounts, and loyalty programs to consumers.

- This mode of payment is highly standardized and widely recognized across various industries, which ensures its dominance in the market.

- Therefore, according to the market analysis, bank cards lead in revenue share due to their established presence and acceptance across multiple platforms.

Digital Wallets is expected to register the fastest CAGR during the forecast period.

- Digital wallets offer the convenience of storing and accessing payment information directly on smartphones, enabling users to make quick, secure payments through apps.

- The trend of e-commerce, mobile-based transactions, and contactless payments are driving the adoption of digital wallets.

- They also provide additional features like loyalty rewards, gift cards, and bill payments, increasing their appeal to consumers.

- Major digital wallet platforms, including Apple Pay, Google Pay, and PayPal, are rapidly expanding their market reach.

- As mobile penetration and smartphone usage continue to rise, digital wallets are expected to gain more traction in the ecosystem.

- Thus, according to the market analysis, digital wallets are growing rapidly as the preferred mode of payment in mobile-first economies.

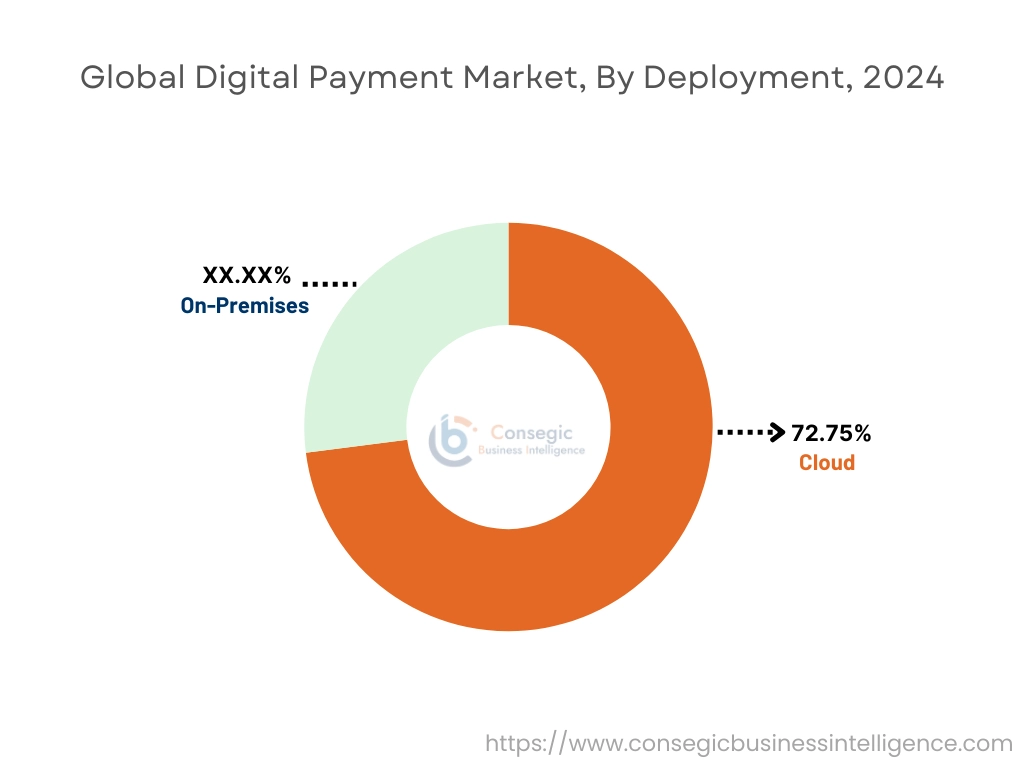

By Deployment:

Based on deployment, the market is segmented into on-premises and cloud.

Cloud accounted for the largest revenue share by 72.75% in 2024.

- Cloud deployment is increasingly preferred due to its scalability, cost-effectiveness, and ease of integration with existing systems.

- Cloud-based solutions offer flexible and on-demand services, allowing businesses to scale their operations without investing in additional infrastructure.

- The adoption of cloud solutions also simplifies maintenance and updates, ensuring that payment systems stay current with the latest security protocols.

- Cloud deployment is particularly beneficial for small and medium enterprises (SMEs) that need cost-effective solutions without the overhead of managing on-premises infrastructure.

- Additionally, cloud technology supports data analytics, enabling businesses to better understand consumer behavior and optimize payment processing.

- Therefore, according to the market analysis, cloud deployment dominates due to its flexibility and scalability, with growing ask from SMEs.

On-Premises is expected to register the fastest CAGR during the forecast period.

- On-premises deployment involves maintaining and managing payment infrastructure within the organization’s premises, providing greater control over data security and operational processes.

- Large enterprises with strict data privacy and security requirements prefer this model as it reduces dependence on third-party cloud service providers.

- With increasing concerns over data breaches and regulatory requirements, on-premises solutions offer a higher level of control, making them suitable for high-risk industries like banking and healthcare.

- Additionally, the cost structure of on-premises solutions is often more predictable, making it an appealing option for businesses with stable payment processing needs.

- Thus, according to the market analysis, on-premises solutions are experiencing a rapid increase in adoption, driven by the need for greater control and security.

By Enterprise Size:

Based on enterprise size, the market is segmented into large enterprises and small & medium enterprises (SMEs).

Large Enterprises accounted for the largest revenue share in 2024.

- Large enterprises typically have the resources to invest in such advanced systems, often integrating multiple payment solutions for global operations.

- These organizations require highly secure and scalable payment infrastructures to handle large volumes of transactions across diverse markets.

- Furthermore, large enterprises benefit from strong partnerships with financial institutions, allowing for seamless and efficient cross-border payments.

- Their scale and global presence also allow them to leverage economies of scale, negotiating lower transaction fees with payment processors.

- The complexity and volume of transactions at large enterprises contribute significantly to their share in the market.

- Therefore, according to the market analysis, large enterprises maintain dominance in revenue share due to their vast operations.

Small & Medium Enterprises (SMEs) is anticipated to register the fastest CAGR during the forecast period.

- SMEs are increasingly adopting these systems to streamline their financial transactions, improve customer experiences, and enhance operational efficiency.

- Cloud-based and low-cost payment solutions are enabling SMEs to compete with larger enterprises without the need for heavy upfront investments.

- As SMEs embrace e-commerce and online sales platforms, these systems become essential for their growth, allowing them to reach broader consumer bases.

- Moreover, governments and financial institutions are offering incentives and support to SMEs for digital adoption, driving the segment's growth.

- Thus, according to the market analysis, SMEs are rapidly adopting digital solutions, indicating a shift towards broader market participation.

By End-Use Industry:

Based on end-use industry, the market is segmented into BFSI, healthcare, IT and telecom, media and entertainment, retail and e-commerce, transportation, and others.

BFSI (Banking, Financial Services, and Insurance) accounted for the largest revenue share in 2024.

- The BFSI sector relies heavily on them for everything from everyday banking transactions to complex financial services, making it the largest contributor to the market.

- Digital payment solutions provide secure and efficient methods for consumers and businesses to perform financial transactions, such as loans, money transfers, and insurance payments.

- Moreover, the sector’s constant innovation in payment technologies, such as blockchain and real-time payments, helps drive trend in the BFSI segment.

- The sector’s regulatory requirements for security and compliance also fuel demand for advanced fraud prevention and transaction monitoring systems.

- With the increasing shift towards cashless transactions, BFSI is set to dominate the digital payment market demand.

- Therefore, according to the market analysis, BFSI remains the largest revenue contributor due to the scale and complexity of financial transactions.

Retail and E-commerce is expected to register the fastest CAGR during the forecast period.

- E-commerce platforms and online retailers are adopting them to facilitate faster, secure, and more convenient transactions for consumers.

- The rise of mobile shopping, online marketplaces, and subscription-based services is propelling the demand for seamless solutions.

- Moreover, e-commerce businesses are increasingly integrating digital wallets, QR codes, and point-of-sale systems to enhance customer experience and improve transaction efficiency.

- As online shopping continues to grow, particularly in emerging markets, the retail and e-commerce sector is poised to expand its market share.

- Thus, according to the market analysis, the retail and e-commerce sector is experiencing rapid growth, driven by the increasing preference for online shopping and mobile payments.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

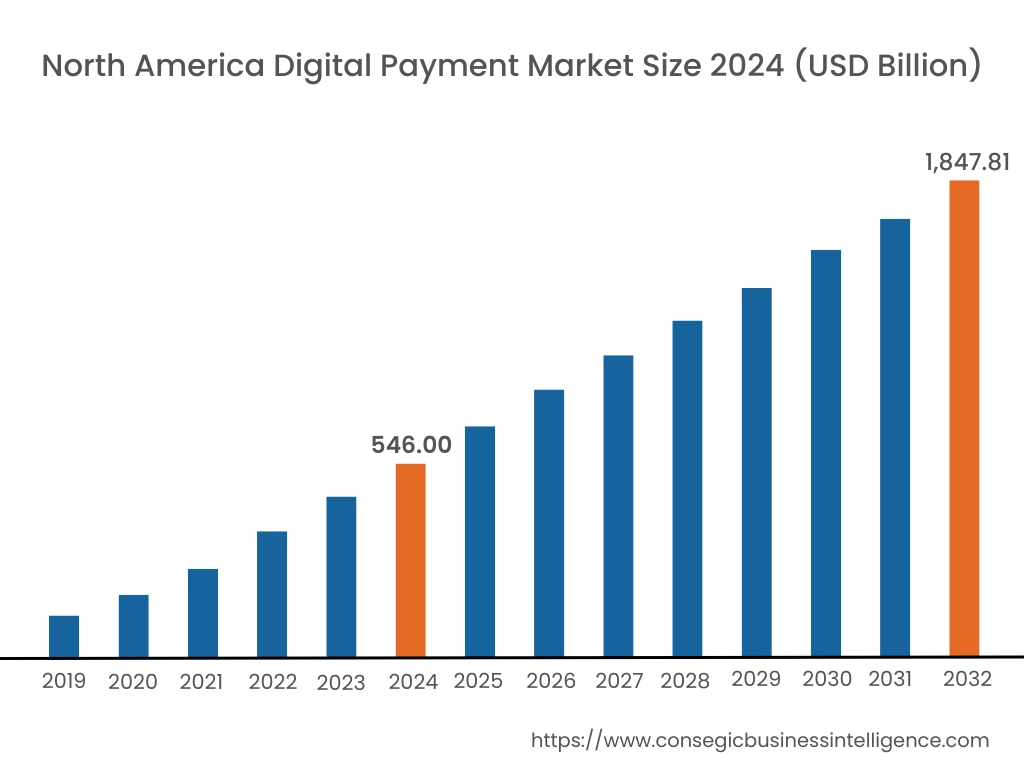

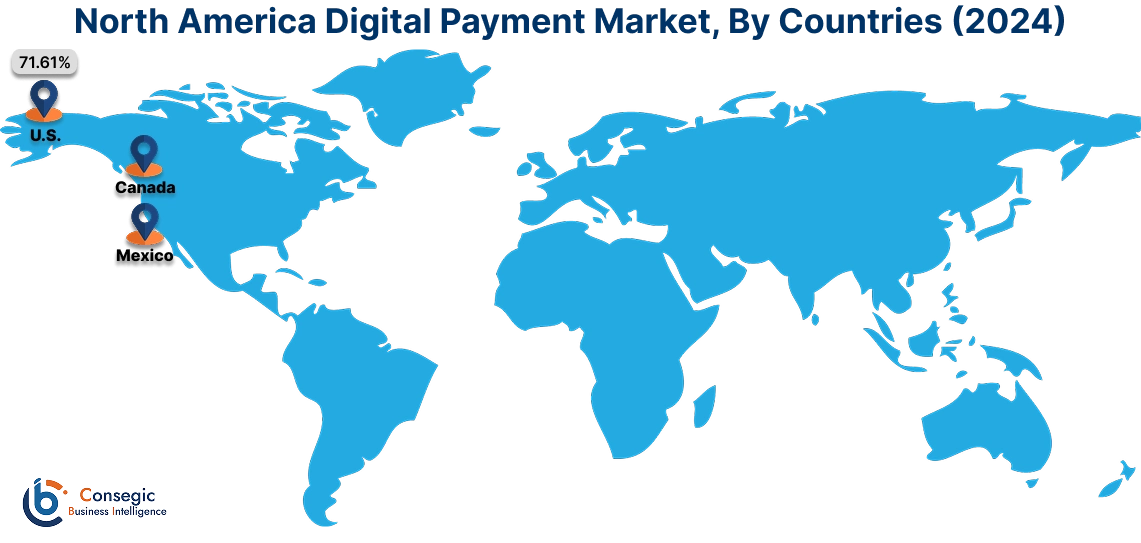

In 2024, North America was valued at USD 546.00 Billion and is expected to reach USD 1,847.81 Billion in 2032. In North America, the U.S. accounted for the highest share of 71.61% during the base year of 2024. North America dominates the digital payment industry, led by the United States and Canada. The region benefits from advanced technological infrastructure, high smartphone penetration, and widespread internet access. Increasing adoption of contactless payments and digital wallets contributes to the market’s strong performance. Additionally, the presence of major payment service providers and fintech companies enhances digital payment market growth. Strict cybersecurity regulations and a rising demand for secure digital transactions further fuel the expansion of the market in North America.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 17.3% over the forecast period. Asia-Pacific holds the largest share of the digital payment market, driven by countries like China, India, and Japan. The region’s rapid digital transformation and high mobile phone usage significantly impact the market. In China, mobile payment solutions, including Alipay and WeChat Pay, dominate the market. India’s increasing shift towards cashless transactions, supported by government initiatives like Digital India, contributes to market expansion. The growing e-commerce sector and increasing internet penetration in emerging markets further strengthen its landscape in Asia-Pacific.

Europe exhibits steady demand, with the United Kingdom, Germany, and France leading the market. The region has seen widespread adoption of such methods, including credit and debit cards, digital wallets, and contactless payments. The European Union’s regulatory frameworks, such as PSD2, ensure secure transactions and promote digital payment market trend. In addition, the increasing popularity of mobile payment systems and e-commerce platforms in Europe enhances its adoption. Furthermore, the ongoing shift from cash to digital payments in many European countries supports market momentum.

The Middle East and Africa (MEA) region is witnessing its rapid adoption, particularly in the UAE, Saudi Arabia, and South Africa. Governments in the region are implementing required infrastructure to promote cashless transactions and financial inclusion. The growth of e-commerce, increased smartphone penetration, and supportive government policies are driving market expansion. The UAE’s Vision 2021 and Saudi Arabia’s Vision 2030 initiatives focus on developing digital economies, creating a favorable environment for such solutions. However, challenges related to cybersecurity and limited internet access in some regions may affect market performance.

Latin America is experiencing strong demand for such solutions, especially in Brazil, Mexico, and Argentina. The region’s increasing e-commerce adoption, alongside the rise of mobile payment services, contributes to digital payment market trend. Government initiatives, including financial inclusion programs and digital banking services, support its landscape. Additionally, the rapid penetration of smartphones and internet access drives cashless transactions. While security concerns and economic instability pose challenges, the region’s growing middle class and digital infrastructure developments provide opportunities for digital payment market expansion.

Top Key Players & Market Share Insights:

The global digital payment market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global digital payment market. Key players in the Digital Payment industry include-

- PayPal Holdings, Inc. (United States)

- Visa Inc. (United States)

- Mastercard Incorporated (United States)

- Google LLC (Google Pay) (United States)

- Samsung Electronics Co., Ltd. (Samsung Pay) (South Korea)

- Square, Inc. (Block, Inc.) (United States)

- Adyen N.V. (Netherlands)

- Alipay (Ant Group) (China)

- WeChat Pay (Tencent Holdings Ltd.) (China)

- Apple Inc. (Apple Pay) (United States)

Recent Industry Developments :

Product Enhancements:

- IN February 2025, Elon Musk announced plans to revitalize his social media platform, X, by integrating payment functionalities in partnership with Visa. This strategic move aims to transform X into an "everything app," similar to China's WeChat, combining messaging, social networking, and payment services. Users will be able to link their debit cards and perform peer-to-peer payments directly within the app.

Digital Payment Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 5,701.37 Billion |

| CAGR (2025-2032) | 16.8% |

| By Solution |

|

| By Mode of Payment |

|

| By Deployment |

|

| By Enterprise Size |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Digital Payment Market? +

In 2024, the Digital Payment Market was USD 1,646.02 Billion.

What will be the potential market valuation for the Digital Payment Market by 2032? +

In 2032, the market size of Digital Payment Market is expected to reach USD 5,701.37 Billion.

What are the segments covered in the Digital Payment Market report? +

The solution, mode of payment, deployment, enterprise size, and end-use industry are the segments covered in this report.

Who are the major players in the Digital Payment Market? +

PayPal Holdings, Inc. (United States), Visa Inc. (United States), Mastercard Incorporated (United States), Square, Inc. (Block, Inc.) (United States), Adyen N.V. (Netherlands), Alipay (Ant Group) (China), WeChat Pay (Tencent Holdings Ltd.) (China), Apple Inc. (Apple Pay) (United States), Google LLC (Google Pay) (United States), Samsung Electronics Co., Ltd. (Samsung Pay) (South Korea) are the major players in the Digital Payment market.