- Summary

- Table Of Content

- Methodology

Digestible Sensors Market Size:

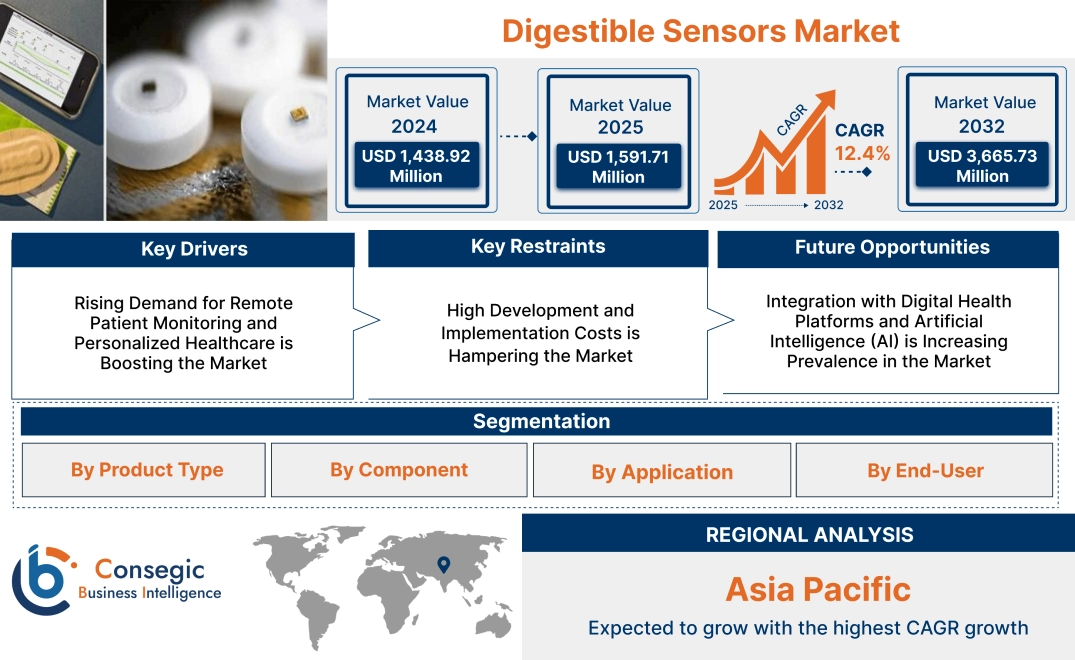

Digestible Sensors Market size is estimated to reach over USD 3,665.73 Million by 2032 from a value of USD 1,438.92 Million in 2024 and is projected to grow by USD 1,591.71 Million in 2025, growing at a CAGR of 12.4%from 2025 to 2032.

Digestible Sensors Market Scope & Overview:

The digestible sensors works on ingestible medical devices designed to monitor internal health conditions and transmit real-time data to external devices for diagnostic and therapeutic purposes. These sensors, often encapsulated in a pill-sized form, are used to track various physiological parameters such as medication adherence, pH levels, core body temperature, and gastrointestinal health. They are widely integrated with digital health platforms for continuous patient monitoring and personalized healthcare.

Key characteristics of digestible sensors include high biocompatibility, wireless communication capabilities, and safe biodegradation or excretion after use. The benefits include enhanced patient compliance, early detection of health anomalies, improved treatment outcomes, and reduced healthcare costs through remote monitoring.

Applications span chronic disease management, gastrointestinal diagnostics, drug delivery monitoring, and personalized medicine. End-users include hospitals, diagnostic laboratories, pharmaceutical companies, and research institutions, driven by advancements in smart healthcare technologies, growing demand for remote patient monitoring, and increasing focus on personalized and preventive healthcare solutions.

Digestible Sensors Market Dynamics - (DRO) :

Key Drivers:

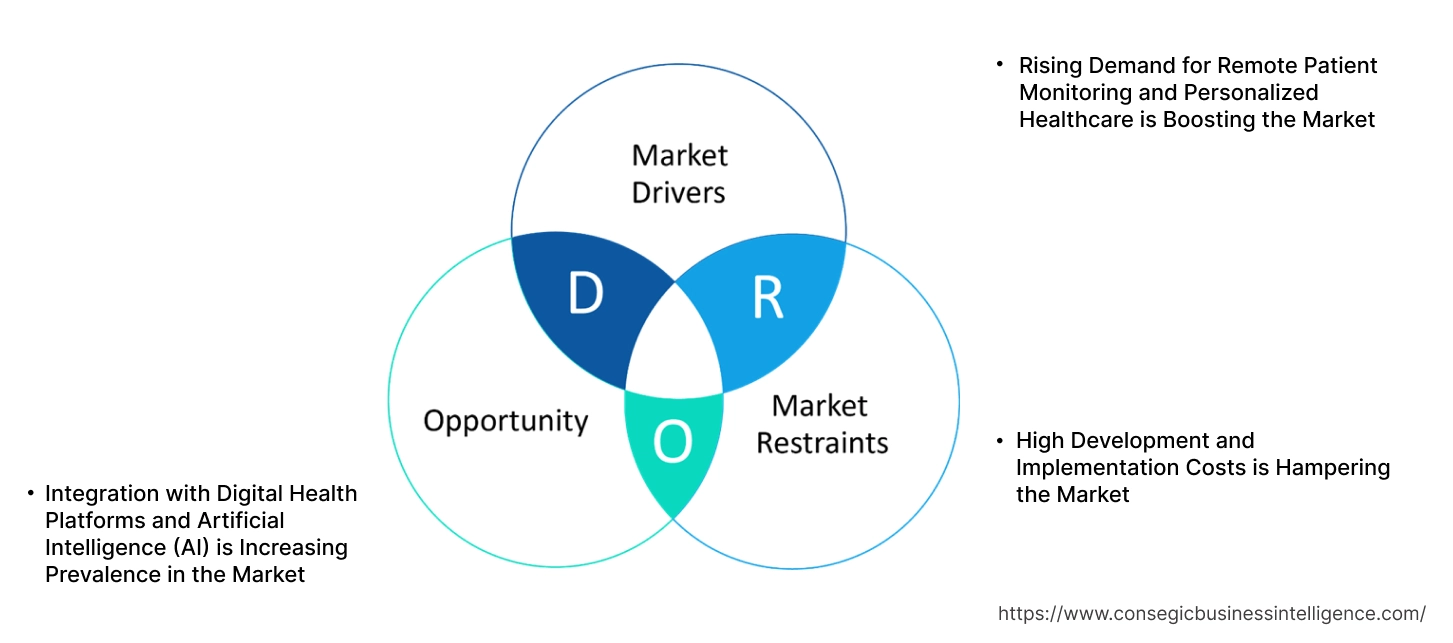

Rising Demand for Remote Patient Monitoring and Personalized Healthcare is Boosting the Market

The increasing development for remote patient monitoring (RPM) and personalized healthcare solutions is a significant driver of the digestible sensors market demand. Digestible sensors, also known as ingestible sensors, are swallowed devices that transmit real-time physiological data from within the body, enabling continuous monitoring of critical health parameters such as medication adherence, gastrointestinal health, and core body temperature. These sensors are particularly valuable for managing chronic diseases, where real-time data collection improves treatment outcomes and patient compliance. The growing elderly population and the rising prevalence of chronic conditions such as diabetes, cardiovascular diseases, and gastrointestinal disorders have further fueled the adoption of digestible sensors as part of integrated health monitoring solutions. Healthcare providers are increasingly leveraging this technology to enhance patient engagement, reduce hospital readmissions, and streamline disease management.

Key Restraints:

High Development and Implementation Costs is Hampering the Market

Despite their clinical potential, the widespread adoption of digestible sensors is restrained by high development and deployment costs. The production of biocompatible, miniaturized sensors with reliable wireless communication systems involves advanced manufacturing processes and substantial R&D investment. Additionally, ensuring these sensors meet stringent regulatory requirements for safety and efficacy adds to development expenses. Healthcare systems, particularly in low- and middle-income countries, may find it challenging to integrate this technology due to cost constraints. Moreover, the high cost of these sensors can limit their accessibility, especially for patients in regions without adequate insurance coverage or reimbursement frameworks for advanced digital health technologies.

Future Opportunities:

Integration with Digital Health Platforms and Artificial Intelligence (AI) is Increasing Prevalence in the Market

The integration of digestible sensors with digital health platforms and artificial intelligence (AI) presents significant opportunities for market growth. By combining data from ingestible sensors with AI-driven analytics, healthcare providers can gain deeper insights into patient health, enabling early detection of medical issues and more precise treatment adjustments. For example, AI algorithms can analyze sensor data to detect irregular medication intake patterns or early signs of gastrointestinal complications, prompting timely medical interventions. Additionally, the expansion of Internet of Medical Things (IoMT) ecosystems supports the seamless integration of digestible sensors with smartphones and cloud-based health systems, allowing patients and clinicians to monitor health metrics remotely. This technological convergence is driving the development of holistic healthcare solutions that are proactive, personalized, and data-driven.

These dynamics highlight the transformative potential of digestible sensors in reshaping healthcare delivery through real-time, internal monitoring solutions. While high development and implementation costs pose challenges, the integration with digital health technologies and AI-driven analytics offers promising pathways for innovation and market expansion.

Digestible Sensors Market Segmental Analysis :

By Product Type:

Based on product type, the market is segmented into temperature sensors, pressure sensors, pH sensors, image sensors, and chemical sensors.

The temperature sensors segment accounted for the largest revenue in digestible sensors market share in 2024.

- Temperature sensors are extensively used in gastrointestinal and metabolic monitoring, enabling real-time internal temperature assessment.

- Increasing trends for early detection of infections and inflammation drive the adoption of ingestible temperature sensors.

- These sensors are critical for monitoring core body temperature in sports medicine and post-surgical recovery.

- Advancements in wireless communication technology enhance the accuracy and efficiency of temperature sensors in digestible devices.

The pH sensors segment is anticipated to register the fastest CAGR during the forecast period.

- pH sensors are widely used for gastrointestinal monitoring, particularly for diagnosing acid reflux, ulcers, and other digestive conditions.

- Rising prevalence of gastrointestinal disorders and growing awareness of gut health drive trends for ingestible pH sensors.

- Non-invasive pH monitoring solutions reduce patient discomfort compared to traditional diagnostic methods.

- Integration of pH sensors with real-time data transmission technology supports precise and continuous health monitoring.

By Component:

Based on component, the market is segmented into sensors, data recorders, transmitters, and software & services.

The sensors segment accounted for the largest revenue share in 2024.

- Sensors are the core component of digestible devices, responsible for capturing critical physiological data.

- Growing trends for advanced biosensors that can monitor multiple parameters simultaneously drives digestible sensors market growth.

- Continuous innovation in miniaturized and biocompatible sensor technologies supports this segment's dominance.

- Expanding applications in diagnostics and patient monitoring enhance the trends for high-performance sensors.

The software & services segment is anticipated to register the fastest CAGR during the forecast period.

- Software platforms facilitate data collection, analysis, and visualization from ingestible devices, enhancing clinical decision-making.

- Growing integration of artificial intelligence (AI) and machine learning in health data analytics boosts digestible sensors market trends.

- Increasing use of cloud-based solutions for real-time monitoring and data storage supports growth.

- Rising need for data security and patient data management fuels demand for advanced software and services in the healthcare sector.

By Application:

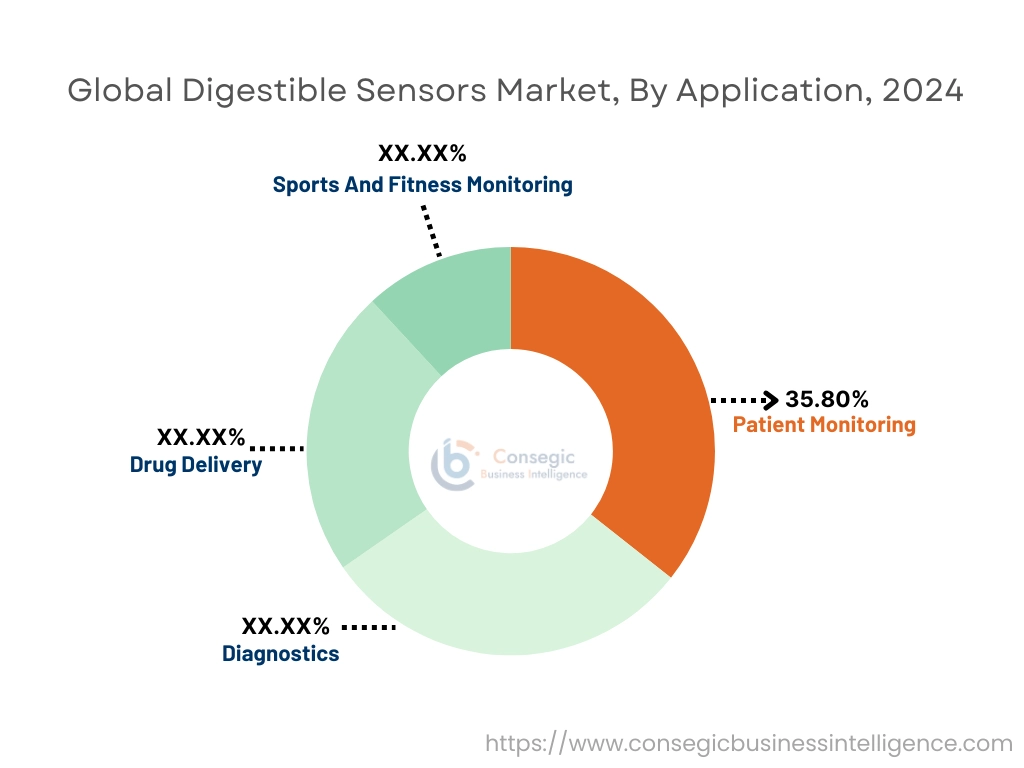

Based on application, the market is segmented into patient monitoring (gastrointestinal monitoring, cardiovascular monitoring, drug adherence monitoring), diagnostics, drug delivery, and sports and fitness monitoring.

The patient monitoring segment accounted for the largest revenue in digestible sensors market share of 35.80% in 2024.

- It is widely used for continuous monitoring of gastrointestinal and cardiovascular health.

- Growing prevalence of digestive disorders and heart conditions fuels digestible sensors market demand for ingestible monitoring solutions.

- Drug adherence monitoring through digestible sensors improves medication compliance, especially in chronic disease management.

- Integration of real-time data analytics enhances early detection of health abnormalities, supporting the segment's trends.

The sports and fitness monitoring segment is anticipated to register the fastest CAGR during the forecast period.

- Increasing digestible sensors market opportunities for personalized fitness and performance tracking drives the adoption of ingestible sensors in the sports industry.

- Athletes use these sensors to monitor hydration, electrolyte balance, and core body temperature for optimal performance.

- Rising popularity of wearable and ingestible technologies for real-time health monitoring supports this segmental analysis.

- Advancements in non-invasive sensors for metabolic and nutritional tracking fuel digestible sensors market growth in sports and fitness applications.

By End-User:

Based on end-user, the market is segmented into hospitals, clinics, homecare settings, ambulatory surgical centers, and sports and fitness centers.

The hospitals segment accounted for the largest revenue share in 2024.

- Hospitals extensively utilize digestible sensors for diagnosing and monitoring complex gastrointestinal and cardiovascular conditions.

- Increasing hospital admissions for chronic diseases and digestive disorders drives digestible sensors market trends for advanced diagnostic tools.

- Adoption of minimally invasive diagnostic procedures in hospital settings supports the dominance of this segment.

- Integration of ingestible devices with hospital information systems (HIS) enhances patient care and clinical outcomes.

The sports and fitness centers segment is anticipated to register the fastest CAGR during the forecast period.

- Growing focus on athlete health optimization and performance enhancement drives the use of digestible sensors in sports centers.

- Increasing investment in sports technology and bio-monitoring solutions supports trends in this segmental analysis.

- Expanding fitness industry and rising consumer interest in health tracking technologies contribute to segment expansion.

- Partnerships between sports organizations and health tech companies are accelerating the adoption of ingestible monitoring devices.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

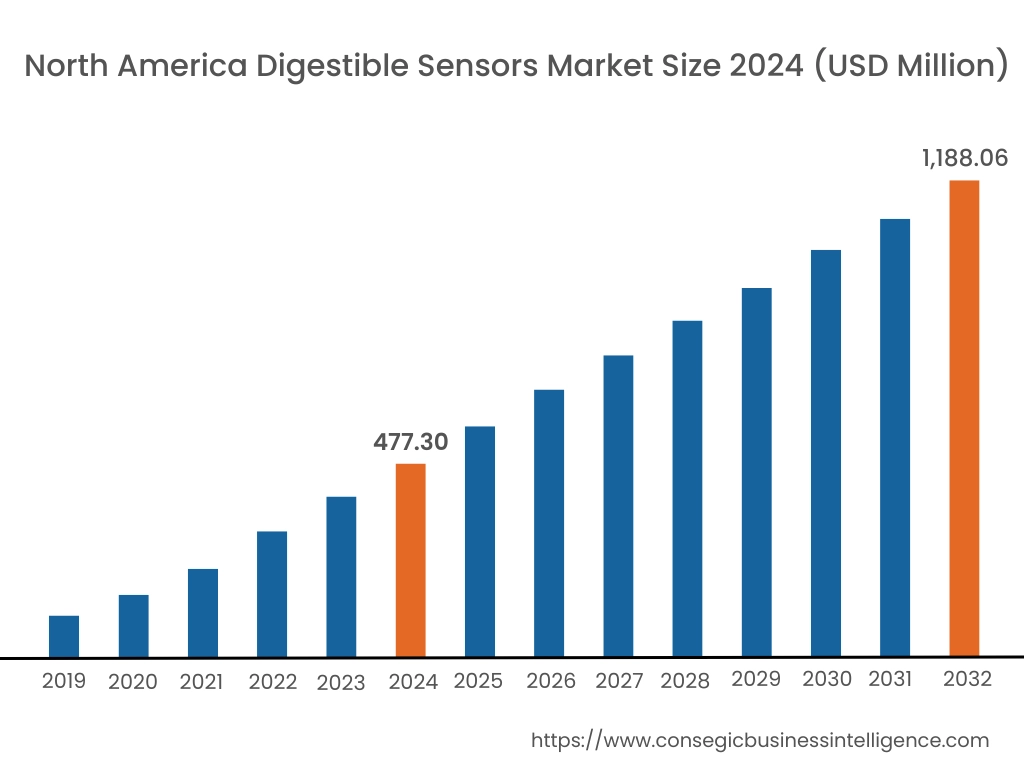

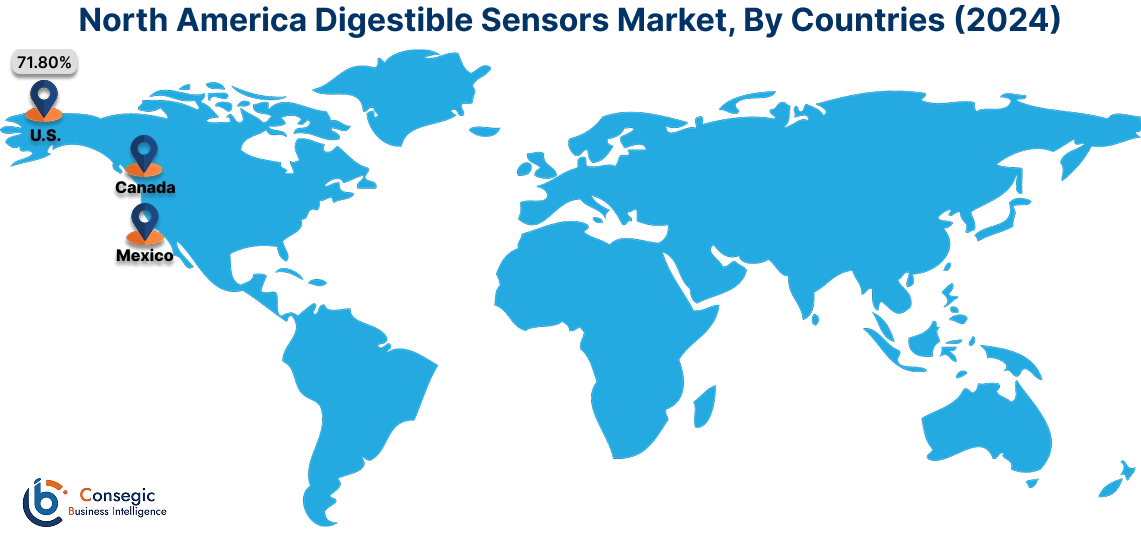

In 2024, North America was valued at USD 477.30 Million and is expected to reach USD 1,188.06 Million in 2032. In North America, the U.S. accounted for the highest share of 71.80% during the base year of 2024. North America holds a dominant share in the global digestible sensors market, driven by advanced healthcare infrastructure, high adoption of innovative medical technologies, and rising demand for personalized healthcare solutions. The U.S. leads the region due to substantial investments in digital health technologies, increasing prevalence of chronic diseases, and strong collaboration between technology firms and healthcare providers. The growing use of digestible sensors for remote patient monitoring, drug adherence, and gastrointestinal diagnostics further fuels digestible sensors market expansion. As per the analysis, Canada contributes through rising adoption of digital health solutions and supportive regulatory frameworks. However, concerns over data privacy and high costs of advanced technologies may limit market enlargement.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 12.9% over the forecast period. The digestible sensors market analysis, is fueled by rapid advancements in healthcare technology, increasing healthcare expenditure, and rising awareness of preventive healthcare in China, India, and Japan. China dominates the market with growing investments in smart healthcare devices and expanding digital health infrastructure. India’s rising burden of chronic diseases and expanding healthcare access drive for cost-effective digestible sensors for real-time health monitoring. Japan emphasizes technological innovation in medical devices and precision healthcare solutions, leveraging its strong R&D capabilities. However, limited awareness in rural areas and affordability challenges may hinder market growth in certain parts of the region.

Europe is a prominent market for digestible sensors, supported by a growing aging population, increasing prevalence of chronic diseases, and significant investments in digital health innovations. Countries like Germany, the UK, and France are key contributors. Germany leads the region with its focus on integrating advanced medical technologies into healthcare systems and strong R&D in smart medical devices. In the digestible sensors market analysis, the UK emphasizes remote patient monitoring and personalized healthcare solutions through digestible sensors, while France promotes the use of innovative diagnostic tools in public healthcare programs. However, stringent regulatory frameworks for medical devices and data security concerns may slow down adoption in some regions.

The Middle East & Africa region is witnessing steady growth in the global digestible sensors market, driven by increasing investments in healthcare infrastructure and growing interest in innovative medical technologies. Countries like Saudi Arabia and the UAE are adopting digestible sensors for monitoring chronic conditions and enhancing personalized medicine, supported by healthcare modernization initiatives. In Africa, South Africa is emerging as a key market, focusing on improving access to smart healthcare solutions for chronic disease management. However, limited technological infrastructure and high costs of advanced medical devices may restrict market enlargement in some parts of the region.

Latin America is an emerging market for digestible sensors, with Brazil and Mexico leading the region. Brazil’s growing healthcare sector and increasing focus on preventive care drive demand for innovative health monitoring devices. Mexico is expanding the adoption of digital health technologies through public health initiatives and partnerships with international healthcare providers. The region also benefits from growing awareness about chronic disease management and personalized healthcare. However, economic instability and inconsistent regulatory frameworks may pose challenges to market growth in smaller economies.

Top Key Players & Market Share Insights:

The digestible sensors market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global digestible sensors market. Key players in the digestible sensors industry include -

- Medtronic plc (Ireland)

- CapsoVision, Inc. (United States)

- Otsuka Holdings Co., Ltd. (Japan)

- BodyCap (France)

- Proteus Digital Health, Inc. (United States)

- Philips Healthcare (Netherlands)

- Given Imaging Ltd. (Israel)

- Check-Cap Ltd. (Israel)

- IntroMedic Co., Ltd. (South Korea)

- RF Co., Ltd. (Japan)

Recent Industry Developments :

Research & Development:

- In February 2023, researchers at MIT and Caltech developed an advanced ingestible sensor designed to track movement through the gastrointestinal (GI) tract. This non-invasive device uses magnetic fields to precisely pinpoint GI motility issues, offering a safer and more efficient alternative to traditional diagnostic methods. This innovation marks a significant advancement in the Digestible Sensors Market, enhancing early detection and treatment of GI disorders.

Digestible Sensors Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 3,665.73 Million |

| CAGR (2025-2032) | 12.4% |

| By Product Type |

|

| By Component |

|

| By Application |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected market size of the Digestible Sensors Market by 2032? +

Digestible Sensors Market size is estimated to reach over USD 3,665.73 Million by 2032 from a value of USD 1,438.92 Million in 2024 and is projected to grow by USD 1,591.71 Million in 2025, growing at a CAGR of 12.4%from 2025 to 2032.

What are the key drivers fueling the growth of the Digestible Sensors Market? +

Factors such as increasing demand for remote patient monitoring, advancements in personalized healthcare, and rising prevalence of chronic diseases are identified as major growth drivers.

Which challenges are restraining the growth of the Digestible Sensors Market? +

High development and manufacturing costs, stringent regulatory approvals, and limited awareness in emerging markets are highlighted as significant market restraints.

Which product type holds the largest market share in the Digestible Sensors Market? +

The report identifies the leading product type in the market, with temperature sensors currently dominating due to their extensive use in internal body monitoring.