- Summary

- Table Of Content

- Methodology

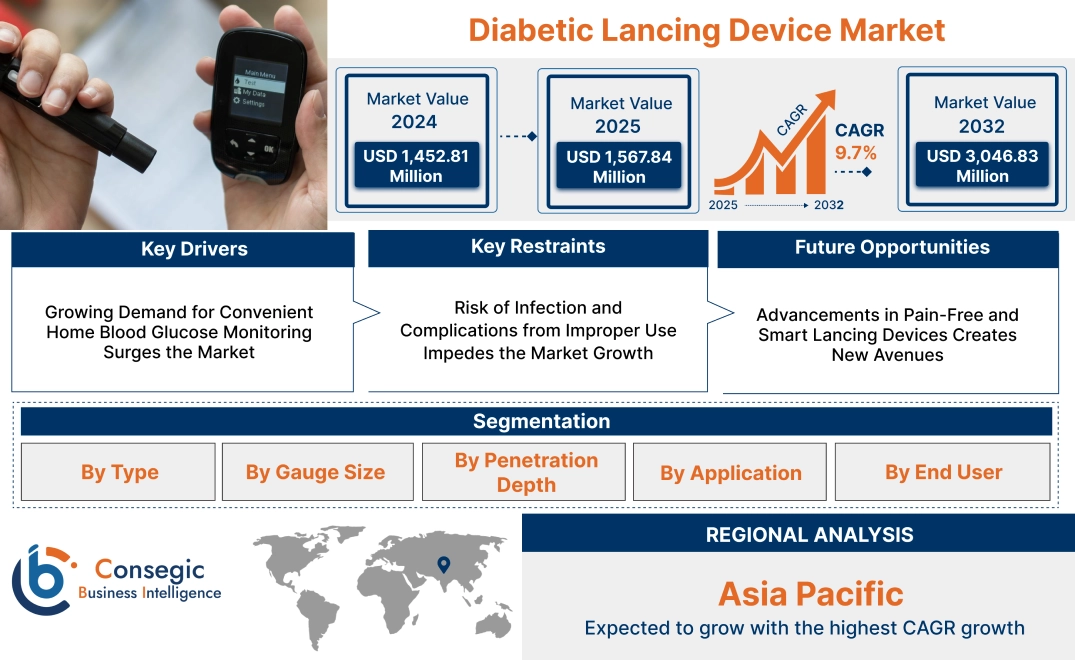

Diabetic Lancing Device Market Size:

Diabetic Lancing Device Market size is estimated to reach over USD 3,046.83 Million by 2032 from a value of USD 1,452.81 Million in 2024 and is projected to grow by USD 1,567.84 Million in 2025, growing at a CAGR of 9.7% from 2025 to 2032.

Diabetic Lancing Device Market Scope & Overview:

Diabetic lancing devices are used for obtaining blood samples through a small puncture in the skin. These devices help in monitoring blood glucose levels in individuals with diabetes. Key features include precision, comfort, and ease of use, which minimize pain during testing. The devices often feature adjustable depths, multiple settings, and ergonomic designs for patient convenience.

The benefits of diabetic lancing devices include accurate glucose monitoring, enhanced patient compliance, and reduced discomfort. These devices are essential in diabetes management, aiding patients in better controlling their condition. Diabetic lancing devices are primarily used in home healthcare settings, hospitals, and clinics. They are crucial in personal health management, particularly for diabetes patients across the healthcare sector.

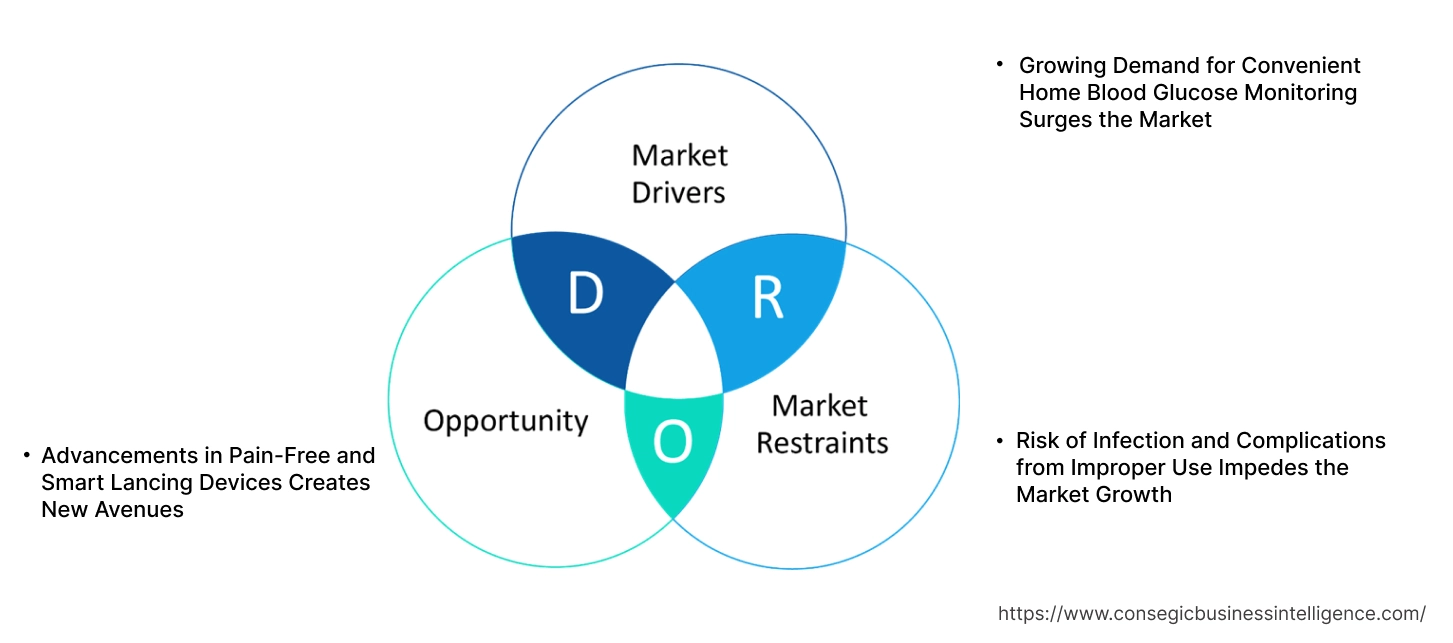

Diabetic Lancing Device Market Dynamics - (DRO) :

Key Drivers:

Growing Demand for Convenient Home Blood Glucose Monitoring Surges the Market

As diabetes prevalence continues to rise globally, there is a growing diabetic lancing device market demand for efficient and convenient blood glucose monitoring solutions. Diabetic lancing devices, designed for use at home, play a crucial role in managing diabetes by enabling patients to test their blood glucose levels regularly and accurately. These devices provide a less painful and more precise option for people who need to monitor their glucose levels consistently. For example, the Accu-Chek Softclix system utilizes advanced technology to ensure a quick, accurate blood sample with minimal discomfort.

The increasing need for self-management of diabetes, particularly among people with type 2 diabetes, is driving the demand for lancing devices. As patients prefer to monitor their glucose levels at home to avoid frequent clinic visits, this trend significantly boosts the market for diabetic lancing devices.

Key Restraints:

Risk of Infection and Complications from Improper Use Impedes the Market Growth

Despite the convenience of diabetic lancing devices, improper use or poor hygiene practices can lead to potential risks, including infections or complications at the puncture site. For example, reusing lancets or using a contaminated device can increase the risk of infections. Additionally, incorrect technique can lead to inaccurate readings, further complicating diabetes management.

These health risks associated with the use of lancing devices discourage some individuals from regularly using them, which limits the widespread adoption of these devices. Consequently, the fear of adverse effects hinders the diabetic lancing device market growth.

Future Opportunities:

Advancements in Pain-Free and Smart Lancing Devices Creates New Avenues

Future advancements in diabetic lancing devices are expected to address current limitations, particularly pain and discomfort. Emerging technologies, such as microneedle devices and robotic assistance, promise to deliver virtually pain-free blood sampling. Smart lancing devices equipped with Bluetooth and integrated with smartphone applications could also enable real-time monitoring and data sharing with healthcare providers.

As these innovations become more accessible and effective, they are poised to drive demand for diabetic lancing devices in the coming years. The development of smarter, more comfortable devices presents a significant diabetic lancing device market opportunity for growth.

Diabetic Lancing Device Market Segmental Analysis :

By Type:

Based on type, the market is segmented into Safety Lancets (Push-Button Safety Lancets, Pressure-Activated Safety Lancets, and Side-Button Safety Lancets) and Standard Lancets.

The safety lancet sector accounted for the largest revenue in diabetic lancing device market share in 2024.

- Safety lancets are widely used in hospitals, diagnostic centers, and home care settings due to their pre-loaded, single-use design that reduces contamination risks.

- These lancets feature an automatic retraction mechanism, enhancing patient safety and preventing accidental needle-stick injuries.

- The segment benefits from stringent infection control guidelines that mandate the use of safety lancets in medical and laboratory settings.

- As per market analysis, increasing awareness about needlestick injury prevention and patient safety measures supports the high adoption of safety lancets.

- Therefore, according to diabetic lancing device market analysis, many regulatory bodies emphasize the use of safety lancets in point-of-care testing and blood glucose monitoring, further strengthening their dominance in the market.

The standard lancet sector is anticipated to register the fastest CAGR during the forecast period.

- Standard lancets are widely used for self-monitoring blood glucose (SMBG) among diabetic patients, driving their increasing adoption in homecare settings.

- These lancets are cost-effective and compatible with a wide range of lancing devices, making them accessible for routine blood sampling.

- The segment benefits from growing awareness about diabetes management and the rising prevalence of lifestyle-related disorders requiring frequent blood testing.

- As per market trends, manufacturers are developing ultra-thin and pain-minimizing standard lancets, improving patient comfort and boosting market adoption.

- Thus, according to diabetic lancing device market analysis, the increasing availability of bulk purchase options through pharmacies and online channels is further fueling the adoption of standard lancets.

By Gauge Size:

Based on gauge size, the market is segmented into 17/18G, 21G, 23G, 25G, 28G, 30G, and others.

The 28G segment accounted for the largest revenue in diabetic lancing device market share in 2024.

- The 28G lancets are known for their fine needle size, which is ideal for diabetic patients requiring frequent testing.

- They provide a balance between comfort and effective blood sample collection, minimizing pain and discomfort.

- The wide availability and lower cost of 28G lancets compared to smaller sizes make them a go-to option for both home care and clinical environments.

- Therefore, according to market analysis, these factors, along with growing adoption among users, contribute to the dominance of the 28G lancet segment in the market.

The 30G segment is anticipated to register the fastest CAGR during the forecast period.

- The 30G lancet, being even finer, is gaining traction for its minimal discomfort during testing, making it highly sought after by patients with sensitive skin.

- It is especially favored for its ability to provide accurate blood samples while minimizing pain, an important factor for patients with diabetes requiring daily blood testing.

- As the demand for more comfortable and less invasive devices increases, the 30G lancet segment is expected to grow rapidly.

- Thus, according to market analysis, the 30G segment is poised for the fastest diabetic lancing device market trend due to its appeal for pain-free testing, making it a preferred choice for diabetic patients.

By Penetration Depth:

Based on penetration depth, the market is segmented into 0.8 mm to 1.0 mm, 1.1 mm to 1.5 mm, 1.6 mm to 2.0 mm, 2.1 mm to 2.5 mm, 2.6 mm to 3.0 mm, and others.

The 0.8 mm to 1.0 mm segment accounted for the largest revenue share in 2024.

- Lancets with a penetration depth of 0.8 mm to 1.0 mm are commonly used for everyday blood glucose monitoring.

- This range is ideal for achieving consistent results while minimizing discomfort, which is crucial for patients managing diabetes at home.

- The availability of lancets within this penetration range, along with their ability to suit a wide range of skin types and sensitivities, leads to their widespread adoption.

- Therefore, according to market analysis, these factors have resulted in the 0.8 mm to 1.0 mm segment capturing the largest share of the diabetic lancing device market.

The 1.1 mm to 1.5 mm segment is expected to register the fastest CAGR during the forecast period.

- Lancets in this penetration depth range are particularly effective for individuals who require deeper samples for more accurate glucose readings.

- The growing focus on precision in diabetes care is expected to drive demand for lancets in this range, particularly for clinical testing and advanced home monitoring systems.

- As the demand for more robust testing tools rises, this segment is projected to experience the fastest trend in the market.

- Thus, according to market analysis, the 1.1 mm to 1.5 mm segment is anticipated to grow rapidly due to its suitability for both home care and clinical applications, driven by the increasing need for precise glucose measurement.

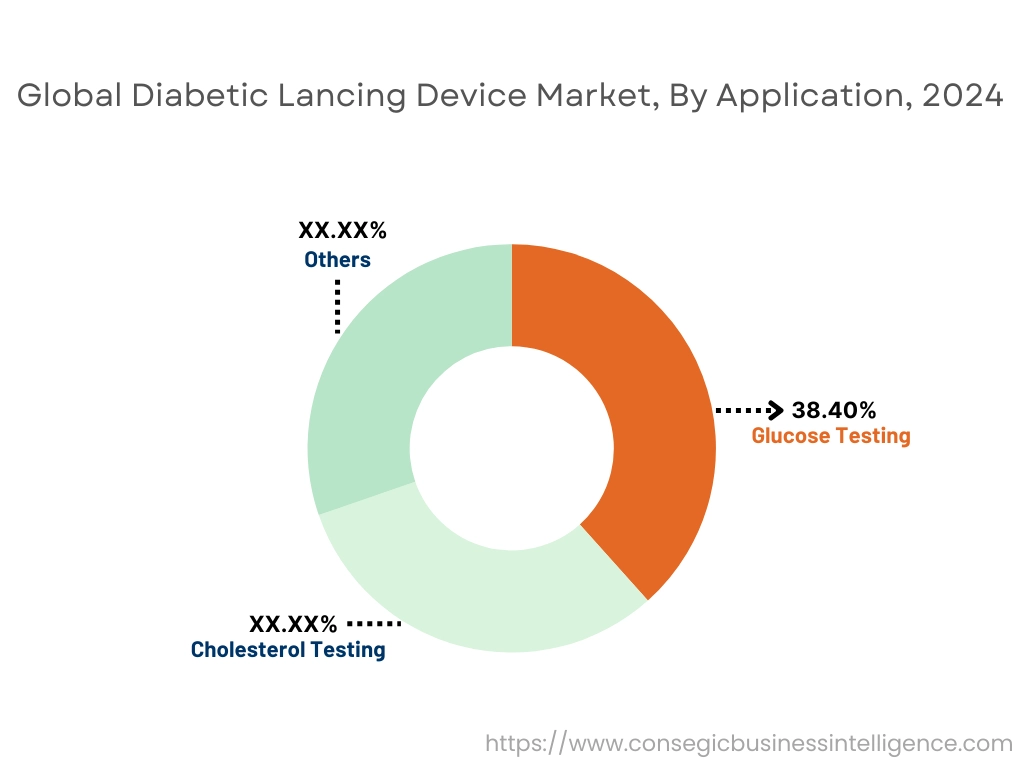

By Application:

Based on application, the market is segmented into Glucose Testing, Cholesterol Testing, and Others.

The glucose testing segment accounted for the largest revenue share by 38.40% in 2024.

- Glucose testing is the primary application for diabetic lancing devices, as individuals with diabetes require regular monitoring of blood glucose levels.

- The increasing prevalence of diabetes worldwide and the demand for continuous self-monitoring have significantly contributed to the dominance of the glucose testing application.

- This segment is expected to maintain its lead in revenue share due to the essential role of blood glucose testing in managing diabetes effectively.

- Therefore, according to market analysis, glucose testing remains the dominant application in the market, driven by the necessity for regular glucose monitoring in diabetes management.

The cholesterol testing segment is anticipated to register the fastest CAGR during the forecast period.

- Although less common than glucose testing, cholesterol testing is gaining momentum as individuals with diabetes are at higher risk for cardiovascular issues.

- The growing awareness of the link between diabetes and cardiovascular diseases is contributing to the increase in cholesterol testing.

- This trend is expected to fuel rapid trend in the cholesterol testing segment, making it the fastest-growing application.

- Thus, according to market analysis, the cholesterol testing application is expected to grow at the fastest rate, driven by the rising awareness of cardiovascular risks associated with diabetes.

By End-User:

Based on end-user, the market is segmented into Hospitals & Clinics, Home Care & Home Diagnostics, Diagnostic Centers & Medical Institutions, Research & Academic Laboratories, and Others.

The home care & home diagnostics segment accounted for the largest revenue share in 2024.

- The home care segment has witnessed substantial trend as patients prefer the convenience of conducting regular glucose testing from home.

- This segment benefits from the increasing adoption of home monitoring devices, as well as the growing trend of remote healthcare services.

- The convenience, cost-effectiveness, and autonomy offered by home care solutions are expected to keep this segment as the largest revenue generator.

- Therefore, according to market analysis, home care & home diagnostics is the largest revenue-generating segment, fueled by the rising demand for self-management of diabetes and home-based diagnostic tools.

The diagnostic centers & medical institutions segment is expected to register the fastest CAGR during the forecast period.

- Diagnostic centers are increasingly adopting diabetic lancing devices as part of comprehensive diabetes management programs.

- The need for accurate and efficient glucose testing in clinical settings, as well as advancements in diagnostic technologies, are contributing to the growth of this segment.

- As the global healthcare infrastructure improves, diagnostic centers are expected to experience the fastest growth in demand for lancing devices.

- Thus, according to market analysis, diagnostic centers & medical institutions are expected to grow at the fastest rate due to their essential role in professional diabetes care and the expansion of healthcare services.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

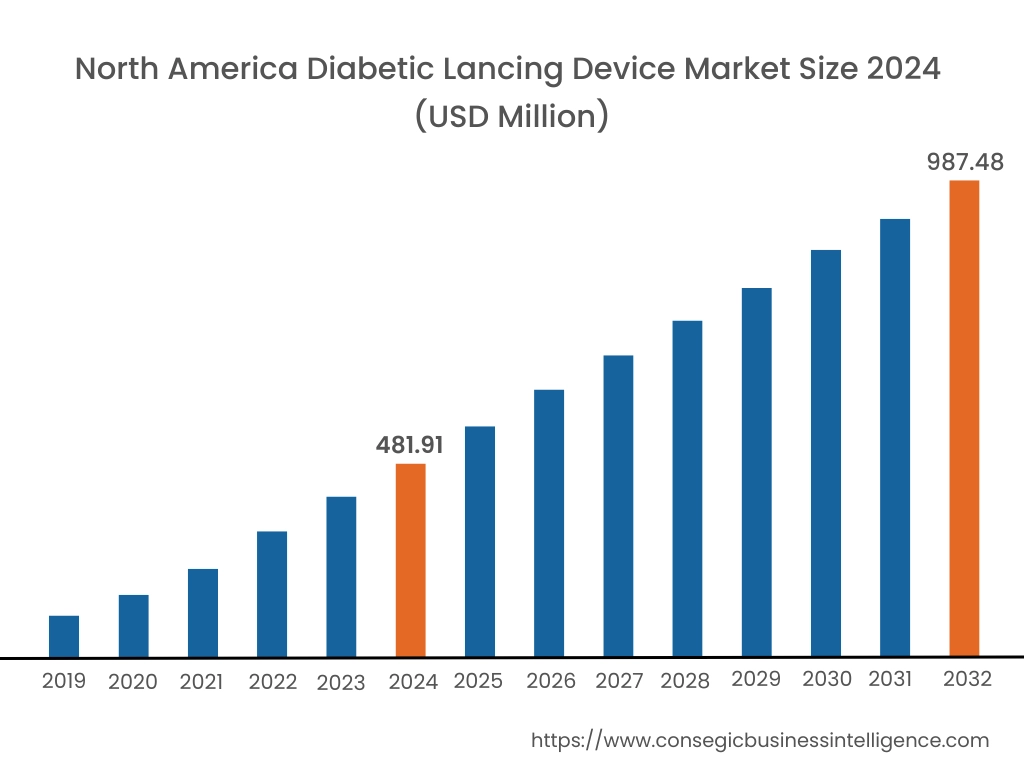

In 2024, North America was valued at USD 481.91 Million and is expected to reach USD 987.48 Million in 2032. In North America, the U.S. accounted for the highest share of 72.65% during the base year of 2024. North America dominates the diabetic lancing device market, driven by high diabetes prevalence and advanced healthcare infrastructure. The United States leads the market due to widespread access to healthcare, strong demand for home-based blood glucose monitoring, and a large diabetic patient population. Additionally, the presence of key market players and high adoption rates of technologically advanced lancing devices fuel market growth. However, healthcare costs and regulatory hurdles remain key challenges.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 10.2% over the forecast period. The Asia-Pacific region is witnessing significant diabetic lancing device market expansion. Rapid urbanization, rising disposable income, and increasing awareness about diabetes management contribute to the growing demand for these devices. Countries like China and India exhibit high diabetes rates, leading to greater use of lancing devices for blood glucose monitoring. However, affordability and limited healthcare access in rural areas pose challenges to widespread adoption.

In Europe, the diabetic lancing device market benefits from a well-established healthcare system and high demand for non-invasive diabetes management tools. Germany, the United Kingdom, and France are key markets due to the increasing diabetic population and strong healthcare infrastructure. Regulatory approvals and reimbursement policies across European countries are favorable for the market. However, regional disparities in healthcare access may affect the market's full potential, particularly in Eastern Europe.

The Middle East and Africa region shows steady growth in the diabetic lancing device market. Increasing healthcare awareness, rising diabetic cases, and improvements in healthcare infrastructure drive diabetic lancing device market demand, particularly in countries like Saudi Arabia and the UAE. However, limited access to advanced healthcare technologies, especially in sub-Saharan Africa, hinders market penetration. High costs and limited insurance coverage further restrict access in some areas.

In Latin America, the diabetic lancing device market is growing steadily, with Brazil and Mexico leading demand. Increased healthcare access, rising disposable income, and government initiatives aimed at improving diabetes management contribute to the market’s growth. However, disparities in healthcare infrastructure and limited access to affordable diabetes care in rural areas may impact market expansion. Despite this, rising awareness of diabetes and better access to medical devices in urban regions support market development.

Top Key Players & Market Share Insights:

The Global Diabetic Lancing Device Market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the Global Diabetic Lancing Device Market. Key players in the Diabetic Lancing Device industry include-

- Roche Diagnostics (Switzerland)

- Abbott Laboratories (United States)

- Nipro Corporation (Japan)

- GlucoRx (United Kingdom)

- Easy Touch (United States)

- Becton, Dickinson and Company (United States)

- Terumo Corporation (Japan)

- Medtronic PLC (Ireland)

- Ascensia Diabetes Care (Germany)

- Smiths Medical (United Kingdom)

Recent Industry Developments :

Partnerships & Collaborations:

- In November 2023, Terumo partnered with HTL-Strefa to strengthen its presence in the European lancing device market, leveraging HTL-Strefa's expertise and distribution network.

Diabetic Lancing Device Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 3,046.83 Million |

| CAGR (2025-2032) | 9.7% |

| By Type |

|

| By Gauge Size |

|

| By Penetration Depth |

|

| By Application |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Diabetic Lancing Device Market? +

In 2024, the Diabetic Lancing Device Market was USD 1,452.81 million.

What will be the potential market valuation for the Diabetic Lancing Device Market by 2032? +

In 2032, the market size of Diabetic Lancing Device Market is expected to reach USD 3,046.83 million.

What are the segments covered in the Diabetic Lancing Device Market report? +

The type, gauge size, penetration depth, application, and end-user are the segments covered in this report.

Who are the major players in the Diabetic Lancing Device Market? +

Roche Diagnostics (Switzerland), Abbott Laboratories (United States), Becton, Dickinson and Company (United States), Terumo Corporation (Japan), Medtronic PLC (Ireland), Ascensia Diabetes Care (Germany), Smiths Medical (United Kingdom), Nipro Corporation (Japan), GlucoRx (United Kingdom), Easy Touch (United States) are the major players in the Diabetic Lancing Device market.