- Summary

- Table Of Content

- Methodology

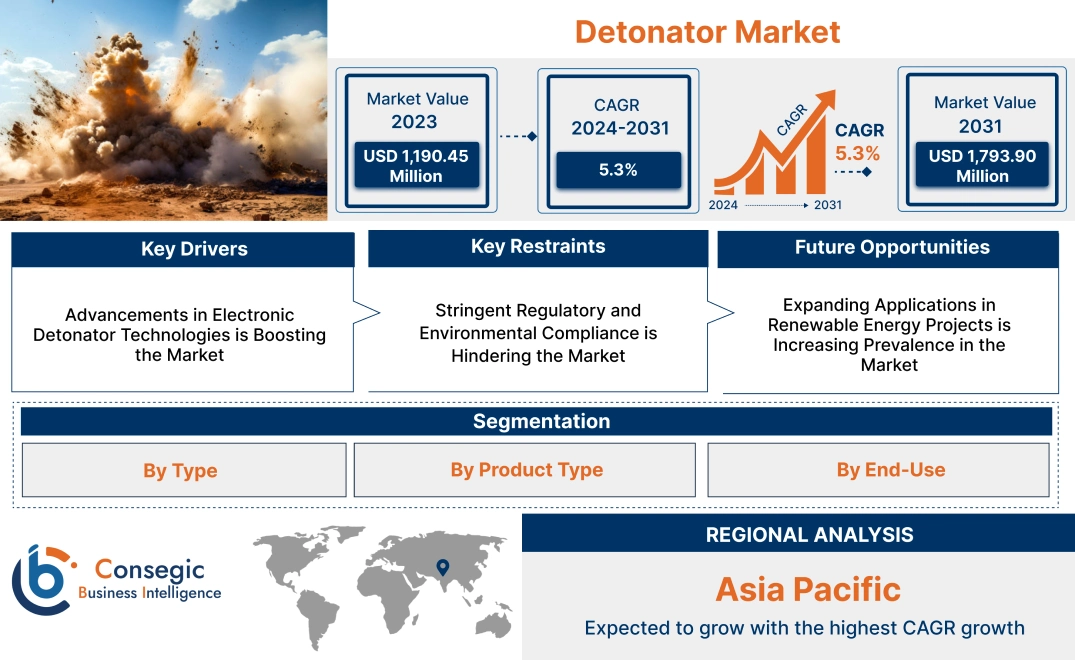

Detonator Market Size:

Detonator Market size is estimated to reach over USD 1,793.90 Million by 2031 from a value of USD 1,190.45 Million in 2023 and is projected to grow by USD 1,231.86 Million in 2024, growing at a CAGR of 5.3% from 2024 to 2031.

Detonator Market Scope & Overview:

The detonator is a device designed to initiate controlled explosions in mining, construction, defense, and demolition applications. Detonators are critical components in explosive systems, ensuring precise timing and reliable activation of explosive charges. Key types include electric, electronic, and non-electric detonators, each tailored to specific operational needs. Key characteristics of detonators include high reliability, precision in ignition, and compatibility with various explosive materials. The benefits include enhanced safety, improved operational efficiency, and the ability to execute complex blasting sequences. Applications span mining and quarrying, oil and gas exploration, military operations, and infrastructure development. End-users include mining companies, construction firms, and defense organizations, driven by increasing demand for minerals and energy resources, advancements in blasting technologies, and the growing need for controlled demolition solutions in urban environments.

Detonator Market Dynamics - (DRO) :

Key Drivers:

Advancements in Electronic Detonator Technologies is Boosting the Market

Electronic detonator technologies are transforming blasting operations by delivering unmatched precision and safety. Unlike traditional systems, electronic detonators enable precise control over blast timing, reducing the risk of misfires and improving fragmentation quality. Their ability to synchronize multiple detonations with high accuracy makes them essential for complex applications in mining, construction, and infrastructure projects.

Trends in digital transformation and automation are further enhancing these technologies. Integration with remote monitoring systems and real-time analytics tools provides operators with critical insights, optimizing blasting efficiency and minimizing environmental impact. The analysis highlights that industries increasingly prioritize safer and more reliable blasting solutions, making electronic detonators a preferred choice for critical operations.

Key Restraints:

Stringent Regulatory and Environmental Compliance is Hindering the Market

The detonator market operates under strict regulatory oversight to ensure the safe production, transport, and use of explosives. Compliance with these regulations requires extensive documentation, specialized storage facilities, and adherence to stringent safety protocols. While these measures are essential for mitigating risks, they add significant complexity and cost to operations.

Environmental compliance poses additional challenges, particularly in regions with rigorous standards. Blasting activities must minimize noise, vibrations, and dust emissions to protect surrounding communities and ecosystems. These constraints can limit detonator usage in certain areas and necessitate continuous investment in technology and process improvements to meet evolving regulatory requirements.

Future Opportunities :

Expanding Applications in Renewable Energy Projects is Increasing Prevalence in the Market

Renewable energy projects, such as geothermal energy extraction, wind farm construction, and hydropower development, are creating new opportunities for detonators. Controlled blasting is often required during site preparation, especially in terrains where excavation and rock removal are critical. Detonators ensure precision and safety, supporting efficient project execution in these energy sectors.

Trends in sustainable energy emphasize environmentally friendly practices, encouraging the development of detonators with reduced vibrations and minimal ecological impact. Manufacturers focusing on tailored solutions for renewable energy applications can align with these trends and capture emerging market segments. As the renewable energy sector continues to expand globally, detonators will play a pivotal role in enabling critical infrastructure development.

Detonator Market Segmental Analysis :

By Type:

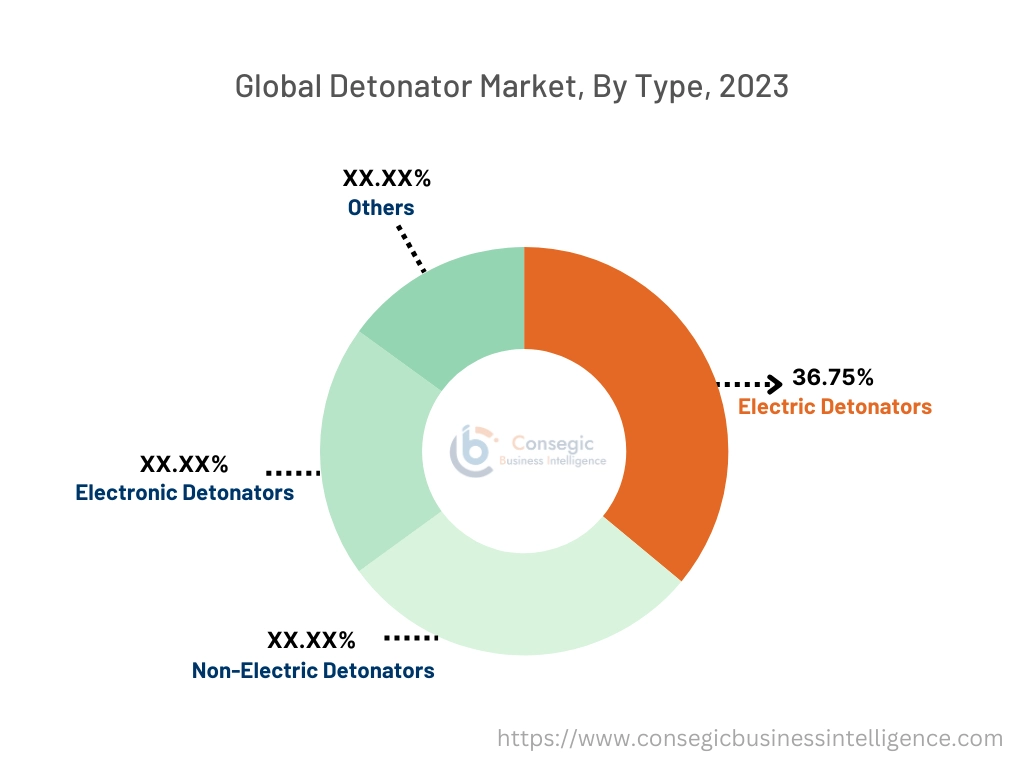

Based on type, the detonators market is segmented into electric detonators, non-electric detonators, electronic detonators, and others.

The electric detonators segment accounted for the largest revenue of 36.75% in detonators market share in 2023.

- Electric detonators are widely used in mining, construction, and defense applications due to their reliability and precision in initiating controlled explosions.

- These detonators are powered by an electrical current, ensuring accurate timing and enhanced safety in operations.

- Their extensive use in large-scale mining and construction projects, where precision and control are critical, has driven their trends in the market.

- Additionally, the rising analysis shows adoption of electric detonators in emerging economies, fueled by increasing mining activities and infrastructure development, has further strengthened their market position.

The electronic detonators segment is anticipated to register the fastest CAGR during the forecast period.

- Electronic detonators are gaining traction due to their advanced features, including programmable delays and high accuracy.

- These detonators are increasingly adopted in applications requiring precise blast control, such as in tunneling, hydropower projects, and high-precision mining.

- The growing focus on reducing vibration and environmental impact during blasting operations is driving the trends for electronic detonators.

- Moreover, analysis portrays the advancements in digital technologies and increasing investments in automation in mining and construction sectors are expected to propel the detonators market growth of the electronic detonators segment.

By Product Type:

Based on product type, the market is segmented into industrial electric detonators, shock tube detonators, and others.

The shock tube detonators segment accounted for the largest revenue in detonators market share in 2023.

- Shock tube detonators are highly preferred for their safety, simplicity, and reliability in initiating explosions.

- These detonators are widely used in mining and quarrying operations, as they eliminate the risks associated with electric currents and electromagnetic interference.

- Their ability to provide consistent and delayed explosions makes them ideal for complex blasting sequences.

- The growing trends for cost-effective and robust blasting solutions in mining and construction have driven the adoption of shock tube detonators, establishing them as the leading product type in the detonator market expansion.

The industrial electric detonators segment is anticipated to register the fastest CAGR during the forecast period.

- Industrial electric detonators are extensively used in large-scale industrial applications, including hydropower projects, quarrying, and construction.

- Their ability to provide precise control and high performance in challenging environments makes them indispensable for critical operations.

- The increasing demand for efficient and reliable detonators in infrastructure development projects, particularly the analysis that portrays the emerging market trends, is expected to drive the rapid growth of the industrial electric detonators segment.

By End-Use:

Based on end-use, the market is segmented into mining, quarrying, construction, hydraulic & hydropower, oil & gas exploration, defense, and others.

The mining segment accounted for the largest revenue share in 2023.

- Mining operations rely heavily on detonators for controlled blasting to extract minerals and ores efficiently.

- Detonators are crucial in ensuring the safety, precision, and cost-effectiveness of mining activities.

- The increasing detonators market opportunities for precious metals, rare earth minerals, and coal have driven significant growth in mining activities globally, thereby boosting the detonators market trends.

- Additionally, advancements in blasting technologies and the rising adoption of electronic and shock tube detonators in the mining sector have reinforced this segment’s dominance in the market analysis.

The hydraulic & hydropower segment is anticipated to register the fastest CAGR during the forecast period.

- Hydraulic and hydropower projects involve complex blasting operations for constructing dams, tunnels, and reservoirs.

- Detonators play a critical role in ensuring precise and safe blasting in these large-scale projects.

- The growing trends analysis for renewable energy sources and the increasing investments in hydropower infrastructure globally are driving the adoption of advanced detonators in this segment.

- Furthermore, the need for high-precision detonators to minimize environmental impact and enhance operational efficiency is expected to propel the detonators market growth of the hydraulic & hydropower segment.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

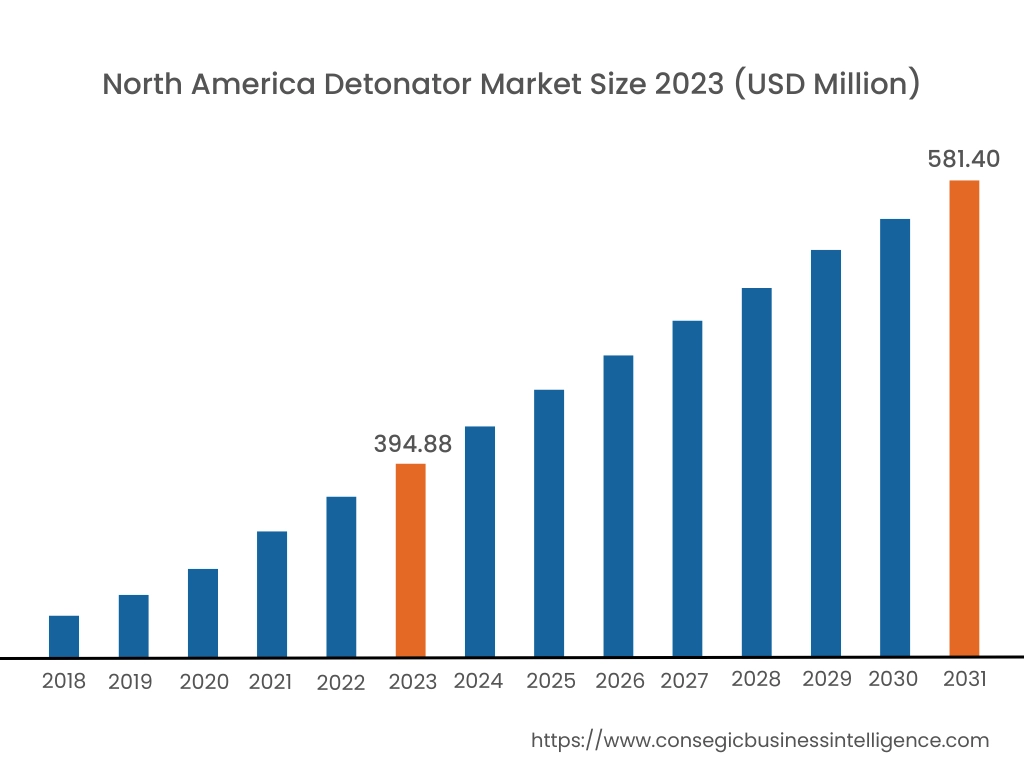

In 2023, North America was valued at USD 394.88 Million and is expected to reach USD 581.40 Million in 2031. In North America, the U.S. accounted for the highest share of 71.70% during the base year of 2023. North America holds a significant share in the detonator market analysis, driven by increasing opportunities from the mining, construction, and defense sectors. The U.S. leads the region due to its extensive mining activities, particularly for coal, metals, and minerals, which require precise and reliable blasting solutions. The construction of large infrastructure projects also supports the use of detonators in controlled blasting. Canada contributes to the market expansion with its robust mining industry, particularly in gold and diamond extraction, driving the detonators market demand for advanced electronic and electric detonators. However, stringent regulations on explosives handling and environmental concerns regarding blasting activities may impact market growth.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 5.7% over the forecast period. Asia-Pacific is the fastest-growing region in the detonator market analysis, fueled by rapid industrialization, urbanization, and increasing mining and infrastructure development in China, India, and Australia. China dominates the market with large-scale mining operations and expanding infrastructure projects that require advanced blasting solutions. India’s growing mining sector and rising investments in large infrastructure projects, such as highways and railways, boost demand for detonators. Australia, known for its mining expertise, heavily utilizes detonators for mineral extraction and coal mining. However, fluctuating raw material costs and safety concerns in blasting operations may hinder the market in certain areas.

Europe is a prominent market for detonators, supported by the region's well-established mining and construction industries. Countries like Germany, Russia, and the UK are key contributors. Russia's extensive mining operations, particularly in gold and precious metals, drive the demand for detonators in large-scale blasting projects. Germany emphasizes the use of advanced detonators in tunneling and infrastructure development, while the UK sees adoption in both construction and defense applications. However, increasing environmental regulations and strict safety standards for explosives may pose challenges for detonator manufacturers in the region.

The Middle East & Africa region is witnessing steady growth in the detonator market, driven by increasing mining activities and infrastructure development. In the Middle East, countries like Saudi Arabia and the UAE are adopting detonators for large-scale construction projects, including tunnels and urban development. In Africa, South Africa is a leading market due to its extensive gold and diamond mining operations, which heavily rely on precise blasting techniques. However, limited access to advanced detonator technologies and challenges in ensuring safety compliance may restrict market growth in some parts of the region.

Latin America is an emerging market for detonators, with Brazil and Chile leading the region. Brazil’s construction and mining sectors, particularly in iron ore and gold extraction, drive the trends for detonators in blasting applications. Chile’s copper mining industry heavily relies on detonators for efficient ore extraction. The region is also witnessing investments in infrastructure projects, further boosting the detonators market trends for blasting solutions. However, economic instability and inconsistent regulatory frameworks for explosives handling may pose challenges for broader market adoption.

Top Key Players and Market Share Insights:

The Detonator market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Detonator market. Key players in the Detonator industry include -

- Orica Limited (Australia)

- Dyno Nobel (U.S.)

- EPC Groupe (France)

- Sasol (South Africa)

- Solar Industries India Limited (India)

- MAXAM (Spain)

- Yunnan Civil Explosive (China)

- China North Industries Group Corporation (CNIGC) (China)

- Austin Powder GmbH (Germany)

- AEL Intelligent Blasting (South Africa)

Detonator Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 1,793.90 Million |

| CAGR (2024-2031) | 5.3% |

| By Type |

|

| By Product Type |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected size of the Detonator Market by 2031? +

Detonator Market size is estimated to reach over USD 1,793.90 Million by 2031 from a value of USD 1,190.45 Million in 2023 and is projected to grow by USD 1,231.86 Million in 2024, growing at a CAGR of 5.3% from 2024 to 2031.

What are detonators, and why are they essential? +

Detonators are devices designed to initiate controlled explosions. They are essential in mining, construction, defense, and demolition, ensuring precision and reliability in explosive systems.

Which type of detonator dominates the market? +

Electric detonators hold the largest revenue share due to their reliability, precision, and extensive use in mining, construction, and defense applications.

What is the fastest-growing segment by type? +

The electronic detonators segment is expected to grow at the fastest CAGR, driven by features such as programmable delays and high precision for complex blasting operations.