- Summary

- Table Of Content

- Methodology

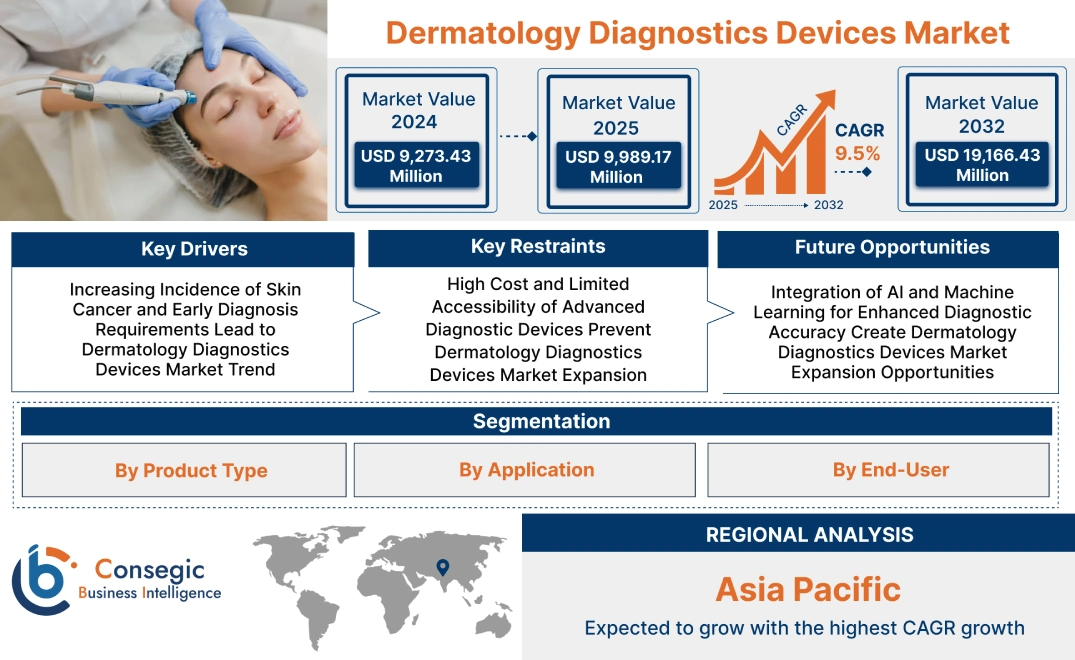

Dermatology Diagnostics Devices Market Size:

Dermatology Diagnostics Devices Market size is estimated to reach over USD 19,166.43 Million by 2032 from a value of USD 9,273.43 Million in 2024 and is projected to grow by USD 9,989.17 Million in 2025, growing at a CAGR of 9.5% from 2025 to 2032.

Dermatology Diagnostics Devices Market Scope & Overview:

Dermatology diagnostic devices are specialized tools used for identifying and assessing various skin conditions and disorders. These devices provide accurate and detailed evaluations, aiding in effective treatment planning.

These devices are characterized by advanced imaging capabilities, non-invasive operation, and user-friendly interfaces. They offer benefits such as early detection of skin abnormalities, precise diagnosis, and enhanced patient outcomes.

Applications include the detection of skin cancer, psoriasis, eczema, and cosmetic dermatology treatments. The devices are widely used in hospitals, dermatology clinics, research institutes, and academic settings, addressing both clinical and aesthetic dermatology needs.

Dermatology Diagnostics Devices Market Dynamics - (DRO) :

Key Drivers:

Increasing Incidence of Skin Cancer and Early Diagnosis Requirements Lead to Dermatology Diagnostics Devices Market Trend

The rising incidence of skin cancer, particularly melanoma, has significantly increased the demand for dermatology diagnostic devices. Early diagnosis is crucial for effective treatment and improving patient outcomes. Dermatology diagnostic devices, including digital dermatoscopes and imaging systems, enable clinicians to detect early signs of skin cancer and other dermatological conditions with high precision. These tools allow for better assessment of moles, lesions, and other skin abnormalities, which enhances the accuracy of diagnosis and the subsequent treatment approach.

As the awareness surrounding the importance of early detection grows, the demand for advanced dermatology diagnostic devices continues to rise.

Key Restraints:

High Cost and Limited Accessibility of Advanced Diagnostic Devices Prevent Dermatology Diagnostics Devices Market Expansion

The cost of advanced dermatology diagnostic devices, such as high-resolution imaging systems and specialized equipment, remains a major obstacle to dermatology diagnostics devices market growth. These devices require significant investment, making them unaffordable for smaller clinics or dermatologists in developing regions. Additionally, the high costs associated with maintenance and training further limit accessibility. Consequently, the adoption of these devices is hindered in certain markets, especially where healthcare budgets are limited or where infrastructure for advanced diagnostic technologies is insufficient.

Thus, the cost-related barriers restrict the widespread adoption of dermatology diagnostic devices in several regions.

Future Opportunities:

Integration of AI and Machine Learning for Enhanced Diagnostic Accuracy Create Dermatology Diagnostics Devices Market Expansion Opportunities

The integration of artificial intelligence (AI) and machine learning (ML) into dermatology diagnostic devices presents a promising opportunity for the market. AI and ML algorithms can analyze skin images with remarkable precision, aiding in the early detection and accurate diagnosis of skin conditions, including various types of skin cancers. For instance, AI-powered algorithms can process dermatoscopic images to detect abnormal patterns that may indicate malignancy. This technology also has the potential to significantly reduce diagnostic errors and improve treatment outcomes.

With continued advancements in AI and ML, these technologies are set to revolutionize the dermatology diagnostics landscape, enhancing the capabilities of existing devices and driving demand in the near future.

Dermatology Diagnostics Devices Market Segmental Analysis :

By Product Type:

Based on product type, the dermatology diagnostic devices market is segmented into imaging devices, dermatoscopes, and microscopes.

The imaging devices segment accounted for the largest revenue in dermatology diagnostics devices market share in 2024.

- Imaging devices are utilized extensively for capturing high-resolution images of the skin, aiding in accurate diagnosis.

- These devices include advanced technologies such as 3D imaging and reflectance confocal microscopy, enhancing the visualization of skin conditions.

- They are primarily used in hospitals and specialized clinics for skin cancer detection, cosmetic analysis, and chronic dermatological condition monitoring.

- The adoption of imaging devices is rising due to their non-invasive nature, high accuracy, and ability to provide rapid diagnostic results.

- Therefore, according to dermatology diagnostics devices market analysis, the imaging devices segment dominates the market due to its wide application in diagnostics and its capability to enhance clinical outcomes in dermatology practices.

The dermatoscopes segment is anticipated to register the fastest CAGR during the forecast period.

- Dermatoscopes are handheld tools designed for magnified visualization of skin lesions and moles, aiding in early-stage detection of skin cancer.

- Technological advancements, such as integration with smartphone applications and AI-based diagnostic support, are expanding their usability.

- Dermatoscopes are increasingly adopted by general practitioners and dermatologists for cost-effective and portable diagnostic solutions.

- Thus, according to dermatology diagnostics devices market analysis, the increasing dermatology diagnostics devices market demand for advanced and portable diagnostic tools is driving the dermatology diagnostics devices market growth of the dermatoscopes segment, making it the fastest-growing product type in the market.

By Application:

Based on application, the market is segmented into skin cancer diagnosis., psoriasis diagnosis, and other diagnostic applications.

The skin cancer diagnosis segment accounted for the largest revenue in dermatology diagnostics devices market share in 2024.

- This segment benefits from rising skin cancer prevalence globally, with early detection being critical for successful treatment outcomes.

- Devices like imaging systems and dermatoscopes are extensively used for identifying malignant and benign lesions.

- Awareness campaigns by healthcare organizations and advancements in diagnostic accuracy contribute to the segment's dominance.

- Therefore, according to market analysis, the skin cancer diagnosis segment leads the market, fueled by increasing incidences of skin cancer and the growing adoption of advanced diagnostic tools.

The psoriasis diagnosis segment is anticipated to register the fastest CAGR during the forecast period.

- Psoriasis diagnosis requires comprehensive analysis of skin scales and redness patterns, often achieved through imaging devices and dermatoscopes.

- Growing awareness of chronic dermatological conditions and advancements in diagnostic protocols are propelling segment growth.

- Thus, according to market analysis, the psoriasis diagnosis segment is growing rapidly, driven by an increased focus on chronic skin condition management and improved diagnostic capabilities.

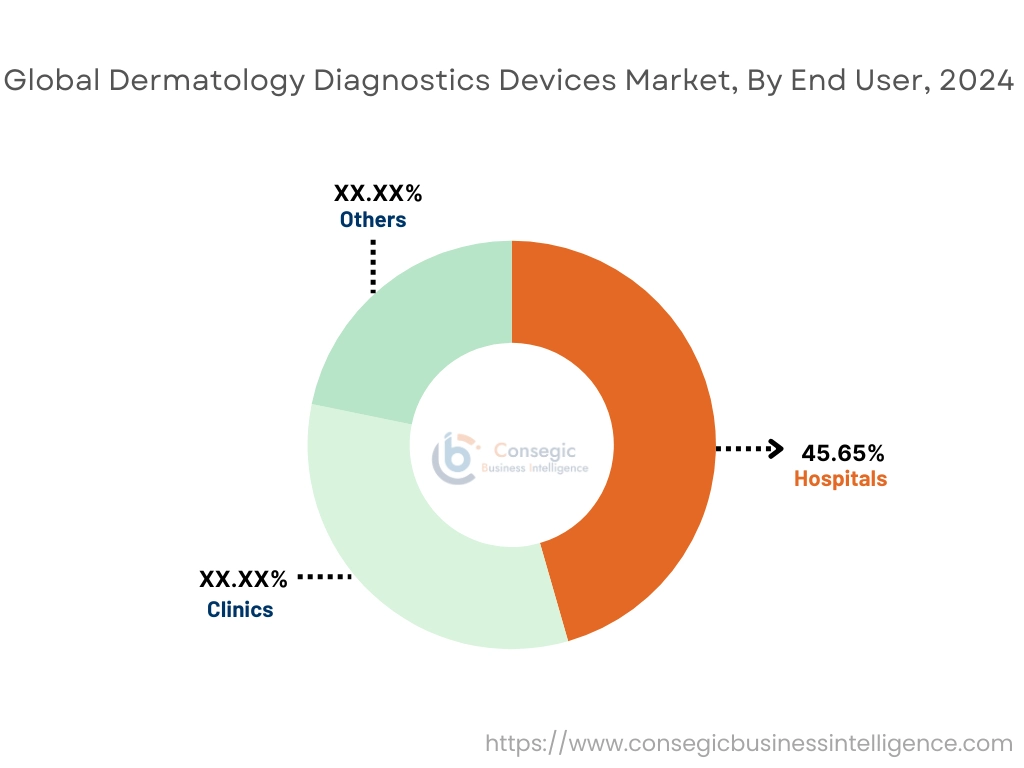

By End-User:

Based on end user, the market is segmented into hospitals, clinics, and others.

The hospitals segment accounted for the largest revenue share by 45.65% in 2024.

- Hospitals serve as the primary facilities for advanced diagnostic procedures and specialized treatments.

- The availability of comprehensive dermatology departments and access to high-end diagnostic devices are key contributors to this segment’s dominance.

- Collaboration with research institutions for clinical trials and diagnostic innovations further solidifies their market position.

- Therefore, according to market analysis, the hospitals segment dominates the market due to its extensive resources and ability to offer specialized dermatological care.

The clinics segment is anticipated to register the fastest CAGR during the forecast period.

- Clinics are increasingly adopting portable and cost-effective diagnostic tools to meet the demand for outpatient dermatological care.

- Convenience, shorter waiting times, and personalized care offered by clinics attract a growing patient base.

- Thus, according to market analysis, the clinics segment is expected to grow rapidly, driven by the dermatology diagnostics devices market demand for accessible and efficient dermatology diagnostic services.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

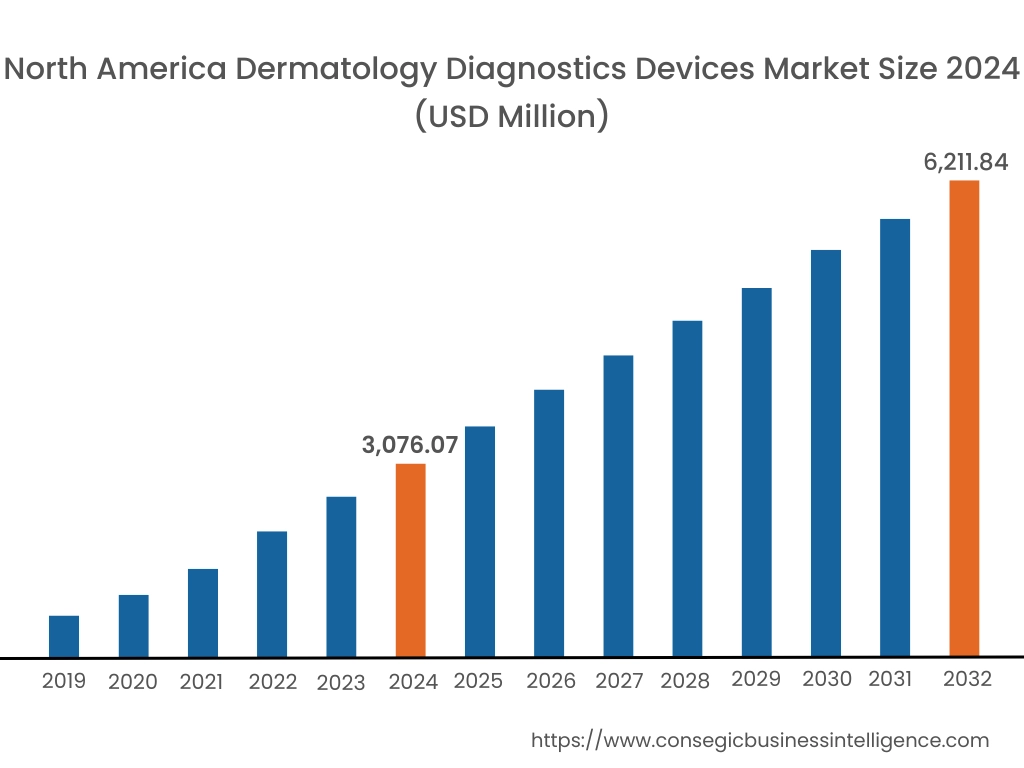

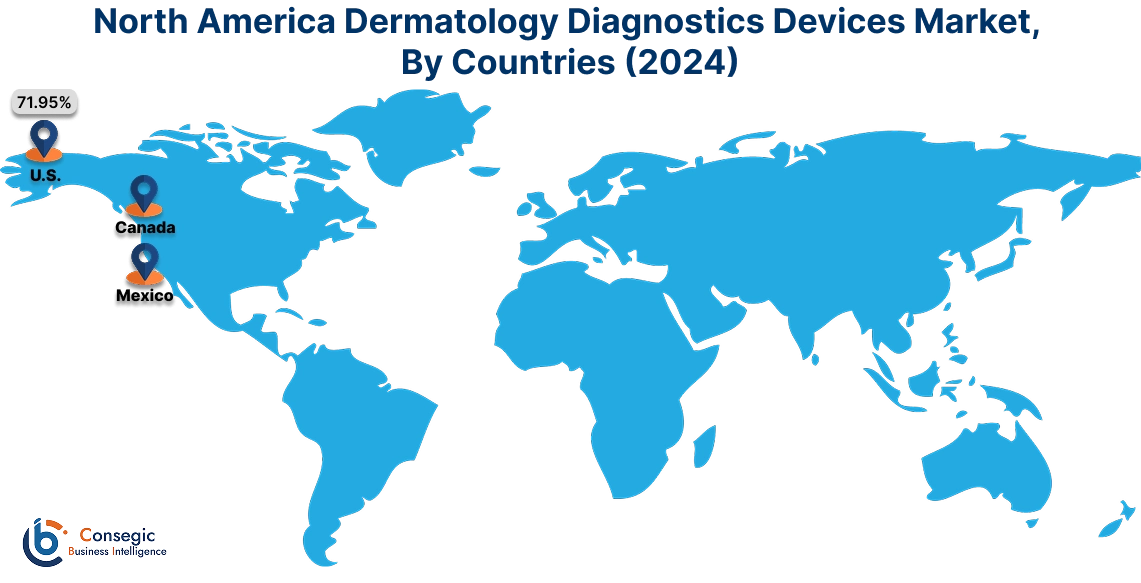

In 2024, North America was valued at USD 3,076.07 Million and is expected to reach USD 6,211.84 Million in 2032. In North America, the U.S. accounted for the highest share of 71.95% during the base year of 2024.

North America holds a significant share of the dermatology diagnostic devices market due to advanced healthcare infrastructure and increased prevalence of skin-related conditions. The region benefits from substantial investments in research and development for innovative diagnostic devices. The United States is a key contributor, driven by high dermatology diagnostics devices market trend for non-invasive diagnostic technologies and an increasing focus on early detection of skin disorders. Rising awareness about skin health and the presence of established manufacturers further strengthen the market.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 10.0% over the forecast period.

The Asia-Pacific region is witnessing steady market development due to the rising incidence of skin diseases and growing adoption of advanced diagnostic technologies. Countries like China, India, and Japan are key contributors, supported by expanding healthcare infrastructure and increasing healthcare expenditure. Dermatology diagnostic devices are gaining popularity among urban populations due to rising awareness about skin health. However, challenges include a lack of skilled dermatologists and limited access to advanced diagnostic solutions in rural areas.

Europe is a prominent region in the dermatology diagnostic devices market due to the presence of established healthcare systems and high prevalence of skin disorders. Germany, the United Kingdom, and France are leading markets, driven by the adoption of advanced imaging technologies for skin diagnosis. The focus on early detection of conditions like skin cancer and the implementation of stringent healthcare regulations further enhance the market. The availability of skilled dermatologists and research-driven innovation contributes to the growth in this region.

The Middle East and Africa region demonstrates moderate market activity, with significant growth potential in developed economies like the United Arab Emirates and Saudi Arabia. Increasing investments in healthcare infrastructure and a rising focus on dermatological health awareness are supporting the market. Limited access to advanced diagnostic devices in African countries remains a challenge, along with economic constraints that affect healthcare spending. However, government initiatives to improve healthcare accessibility provide dermatology diagnostics devices market opportunities for development.

The dermatology diagnostic devices market in Latin America is gradually expanding due to increasing awareness about skin health and rising adoption of advanced medical technologies. Brazil and Mexico are key contributors, supported by growing healthcare infrastructure and demand for innovative diagnostic solutions. The prevalence of dermatological conditions, including skin cancer, is prompting the adoption of modern diagnostic tools. However, challenges include inconsistent healthcare access and limited resources in smaller economies within the region.

Top Key Players & Market Share Insights:

The Global Dermatology Diagnostics Devices Market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the Global Dermatology Diagnostics Devices Market. Key players in the Dermatology Diagnostics Devices industry include-

- Canfield Scientific, Inc. (United States)

- HEINE Optotechnik GmbH & Co. KG (Germany)

- AMD Global Telemedicine, Inc. (United States)

- Roche Diagnostics (Switzerland)

- Strata Skin Sciences, Inc. (United States)

- FotoFinder Systems GmbH (Germany)

- 3Gen DermLite (United States)

- Hill-Rom Holdings, Inc. (United States)

- Bio-Therapeutic, Inc. (United States)

- Michelson Diagnostics Ltd. (United Kingdom)

Recent Industry Developments :

Partnerships & Collaborations:

- In August 2024, L'Oréal acquired a 10% stake in Galderma, marking its return to the anti-wrinkle injectables market after a decade. This €1.7 billion deal includes a scientific partnership to develop anti-aging skin technologies, reflecting L'Oréal's strategic move into medical aesthetics.

- In September 2024, European private-equity firm ArchiMed made its first investment in Asia by acquiring South Korea's Jeisys Medical for approximately $742 million. Jeisys specializes in energy-based devices for aesthetic treatments, including wrinkle reduction and acne therapy. This acquisition aligns with the growing consumer demand for non-invasive, age-defying treatments.

- In November 2023, Perfect Corp. partnered with Sona Dermatology to integrate AI-powered skin diagnostic technology into patient consultations. This collaboration aims to provide personalized treatment recommendations, enhancing patient engagement and experience.

Dermatology Diagnostics Devices Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 19,166.43 Million |

| CAGR (2025-2032) | 9.5% |

| By Product Type |

|

| By Application |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Dermatology Diagnostics Devices Market? +

In 2024, the Dermatology Diagnostics Devices Market was USD 9,273.43 million.

What will be the potential market valuation for the Dermatology Diagnostics Devices Market by 2032? +

In 2032, the market size of Dermatology Diagnostics Devices Market is expected to reach USD 19,166.43 million.

What are the segments covered in the Dermatology Diagnostics Devices Market report? +

The product type, application, and end-user are the segments covered in this report.

Who are the major players in the Dermatology Diagnostics Devices Market? +

Canfield Scientific, Inc. (United States), HEINE Optotechnik GmbH & Co. KG (Germany), FotoFinder Systems GmbH (Germany), 3Gen DermLite (United States), Hill-Rom Holdings, Inc. (United States), Bio-Therapeutic, Inc. (United States), Michelson Diagnostics Ltd. (United Kingdom), AMD Global Telemedicine, Inc. (United States), Roche Diagnostics (Switzerland), Strata Skin Sciences, Inc. (United States) are the major players in the Dermatology Diagnostics Devices market.