- Summary

- Table Of Content

- Methodology

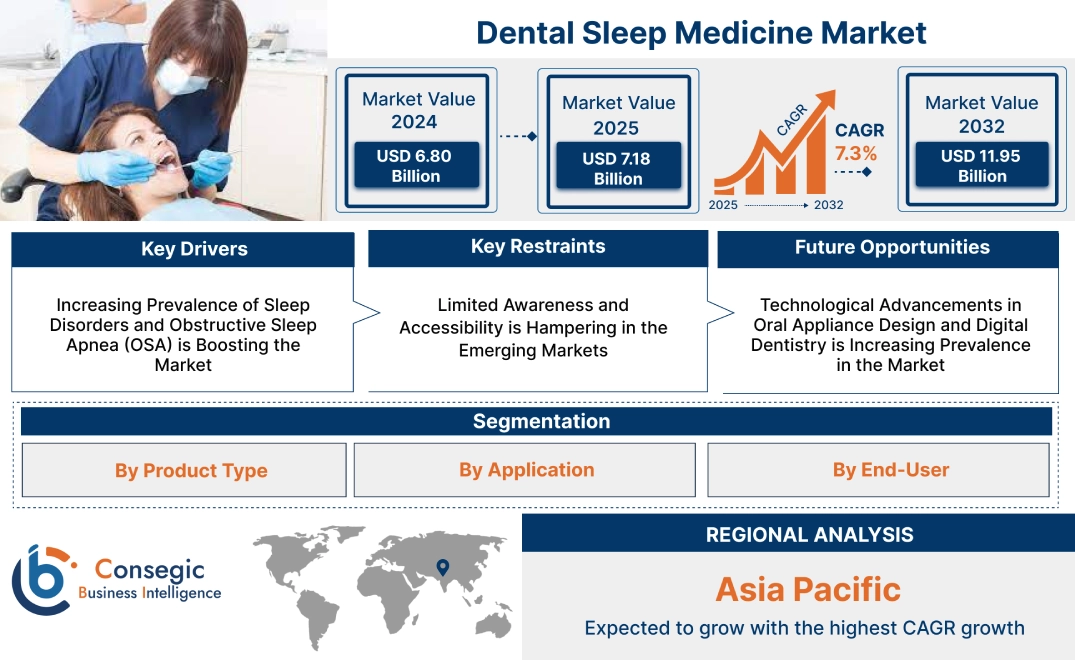

Dental Sleep Medicine Market Size:

Dental Sleep Medicine Market size is estimated to reach over USD 11.95 Billion by 2032 from a value of USD 6.80 Billion in 2024 and is projected to grow by USD 7.18 Billion in 2025, growing at a CAGR of 7.3% from 2025 to 2032.

Dental Sleep Medicine Market Scope & Overview:

The dental sleep medicine are dental-based solutions for diagnosing and treating sleep-related disorders, particularly obstructive sleep apnea (OSA) and snoring. This market includes oral appliances, diagnostic tools, and therapeutic interventions that improve airway patency and enhance sleep quality. Key products include mandibular advancement devices (MADs), tongue-retaining devices (TRDs), and advanced digital diagnostic tools like polysomnography and portable sleep monitors.

Key characteristics of these sleep medicine solutions include non-invasive designs, ease of use, and patient-specific customization for maximum comfort and efficacy. The benefits include improved breathing during sleep, enhanced patient compliance compared to CPAP devices, and better overall quality of life.

Applications span the management of mild to moderate obstructive sleep apnea, snoring, and adjunctive therapy for severe cases. End-users include dental sleep specialists, general dentists, sleep centers, and patients, driven by increasing awareness of sleep-related disorders, advancements in oral appliance technology, and the rising prevalence of conditions like OSA globally.

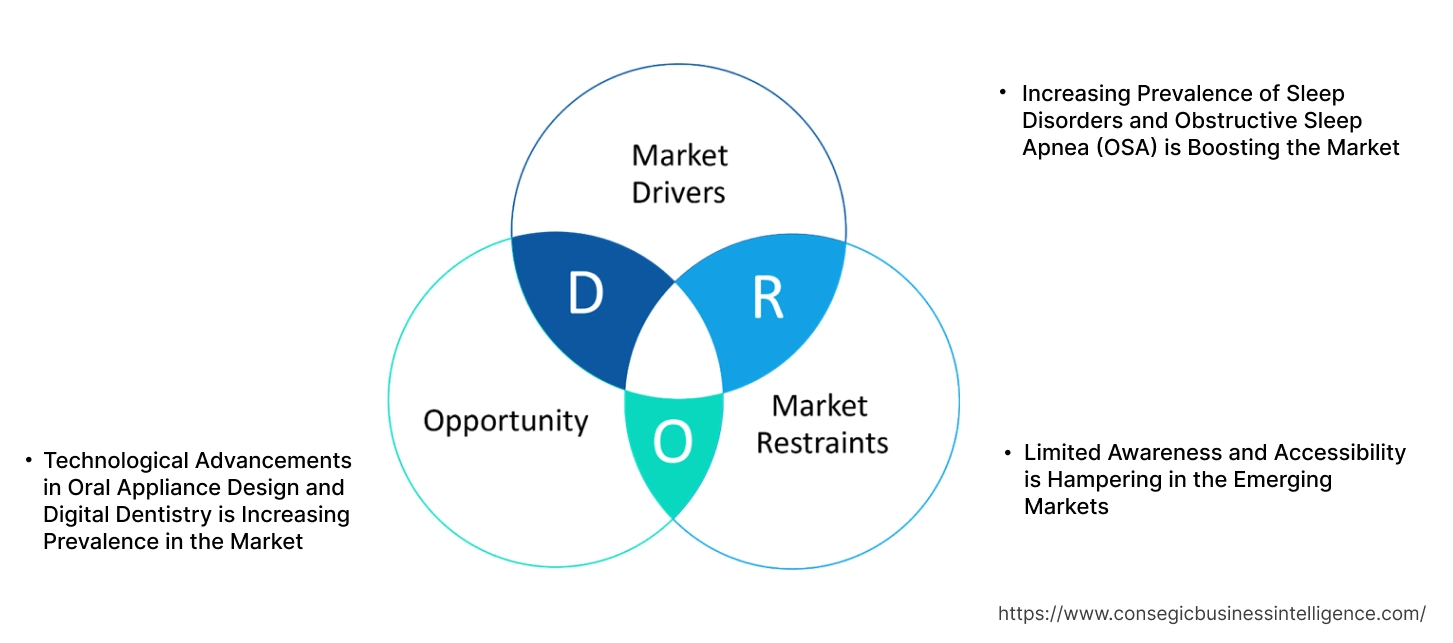

Dental Sleep Medicine Market Dynamics - (DRO) :

Key Drivers:

Increasing Prevalence of Sleep Disorders and Obstructive Sleep Apnea (OSA) is Boosting the Market

The growing prevalence of sleep disorders, particularly obstructive sleep apnea (OSA), is a significant driver for the dental medicine market. OSA, a condition characterized by repeated airway blockages during sleep, affects Billions globally and has been linked to severe health issues such as cardiovascular disease, diabetes, and stroke. Dental sleep medicine offers non-invasive treatment solutions, such as oral appliances, which are effective in managing mild to moderate OSA and snoring. The increasing awareness of the health risks associated with untreated sleep apnea, combined with the rising demand for patient-friendly and cost-effective alternatives to continuous positive airway pressure (CPAP) therapy, is propelling the market forward. Furthermore, the growing number of referrals from sleep specialists to dental practitioners for oral appliance therapy is boosting adoption and expanding the scope of medicines.

Key Restraints:

Limited Awareness and Accessibility is Hampering in the Emerging Markets

Despite its benefits, the dental sleep medicine faces challenges related to limited awareness of oral appliance therapy and its effectiveness in managing sleep disorders, particularly in emerging markets. Many patients remain unaware of dental sleep medicine as a viable treatment option, while healthcare providers may lack the necessary training to integrate oral appliance therapy into sleep disorder management. Additionally, the high initial cost of custom-fitted oral appliances and limited insurance coverage for dental sleep treatments further hinder market growth. These barriers reduce the penetration in regions with underdeveloped healthcare infrastructure, limiting its accessibility to a broader population.

Future Opportunities :

Technological Advancements in Oral Appliance Design and Digital Dentistry is Increasing Prevalence in the Market

The integration of advanced technologies in oral appliance design presents significant opportunities for the dental sleep medicine. Innovations such as 3D printing, CAD/CAM technology, and digital intraoral scanning are enhancing the precision, comfort, and customization of oral appliances. These technologies streamline the production process, reduce chair time, and improve patient satisfaction, making oral appliance therapy more accessible and appealing. Additionally, advancements in smart oral appliances equipped with sensors to monitor sleep patterns and therapy effectiveness are gaining traction, offering real-time feedback to patients and practitioners. The adoption of teledentistry platforms further supports the expansion by improving access to consultations and follow-up care, particularly in underserved areas. Companies and practitioners investing in these technological innovations are well-positioned to capitalize on the growing trends for effective and patient-centered sleep disorder treatments.

These dynamics highlight the critical role of dental sleep medicine in addressing the growing burden of sleep disorders, particularly obstructive sleep apnea. While challenges related to awareness and accessibility remain, advancements in oral appliance technology and digital dentistry present significant growth for the market, enabling improved patient outcomes and expanding the reach of dental sleep solutions globally.

Dental Sleep Medicine Market Segmental Analysis :

By Product Type:

Based on product type, the market is segmented into oral appliances, CPAP (Continuous Positive Airway Pressure) accessories, and monitoring devices.

The oral appliances segment accounted for the largest revenue in dental sleep medicine market share in 2024.

- Oral appliances, including mandibular advancement devices (MADs) and tongue retaining devices (TRDs), are widely used for managing obstructive sleep apnea (OSA) and snoring.

- Increasing preference for non-invasive treatment solutions, particularly among patients with mild to moderate OSA, drives segment dominance.

- Rising advancements in custom-fitted and adjustable oral appliances enhance treatment efficacy and patient comfort.

- Growing adoption of MADs and TRDs in dental clinics and homecare settings supports this segment's growth.

The CPAP accessories segment is anticipated to register the fastest CAGR during the forecast period.

- CPAP accessories, including masks, tubing, and humidifiers, are critical components of PAP therapy, driving steady demand.

- Increasing diagnosis of moderate to severe OSA and subsequent adoption of CPAP therapy support trends in this segmental analysis.

- Advancements in CPAP accessories, including noise reduction and improved comfort designs, enhance patient compliance.

- Growing awareness campaigns about sleep apnea management are expected to propel this segment's trends.

By Application:

Based on application, the market is segmented into obstructive sleep apnea (OSA), snoring management, bruxism, temporomandibular joint disorders (TMJ), and others.

The obstructive sleep apnea (OSA) segment accounted for the largest revenue in dental sleep medicine market share in 2024.

- OSA is the primary focus of dental sleep medicine, with high prevalence rates driving demand for effective diagnostic and treatment solutions.

- Increasing awareness about the health risks associated with untreated OSA boosts adoption of oral appliances and PAP therapy.

- Rising availability of cost-effective and non-invasive solutions for OSA management supports this segment's dominance.

- Expanding efforts by healthcare organizations to enhance early diagnosis and treatment of OSA drive dental sleep medicine market growth.

The snoring management segment is anticipated to register the fastest CAGR during the forecast period.

- Snoring management devices, including oral appliances, are increasingly preferred due to their effectiveness and convenience.

- Growing consumer awareness about the impact of snoring on sleep quality and overall health drives demand.

- Technological advancements, such as adjustable oral devices, improve treatment outcomes and patient satisfaction.

- Rising adoption of snoring management solutions in homecare settings supports dental sleep medicine market trends in this segmental analysis.

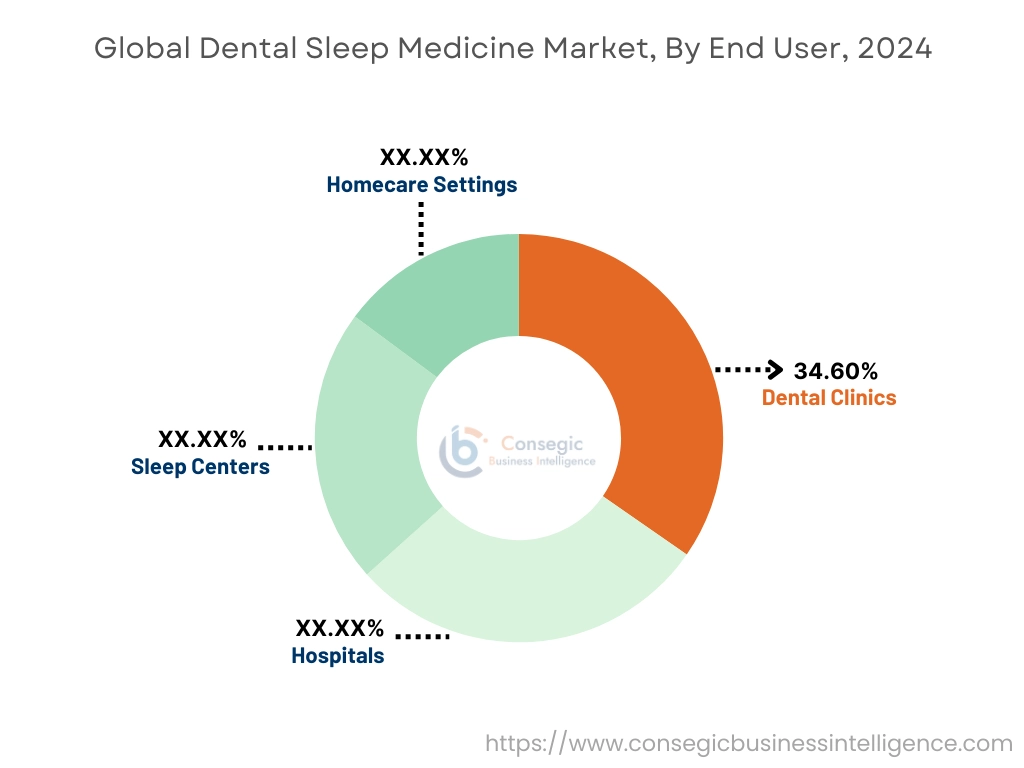

By End User:

Based on end-user, the market is segmented into dental clinics, hospitals, sleep centers, and homecare settings.

The dental clinics segment accounted for the largest revenue share of 34.60% in 2024.

- Dental clinics are the primary providers of custom-fitted oral appliances, driving their dominance in the dental medicine market.

- Increasing collaborations between dental professionals and sleep specialists enhance the role of clinics in sleep apnea management.

- Rising adoption of advanced diagnostic tools in dental clinics for early detection of sleep disorders supports dental sleep medicine market growth.

- Expanding consumer preference for personalized and accessible treatment options at dental clinics fuels this segment's trends.

The homecare settings segment is anticipated to register the fastest CAGR during the forecast period.

- Growing preference for at-home management of sleep disorders, including OSA and snoring, drives dental sleep medicine market demand for homecare solutions.

- Increasing availability of portable oral appliances and PAP devices supports adoption in homecare settings.

- Advancements in telemedicine and remote monitoring technologies enhance patient convenience and treatment compliance.

- Rising awareness campaigns and education initiatives about managing sleep disorders at home are expected to propel this segment's growth.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

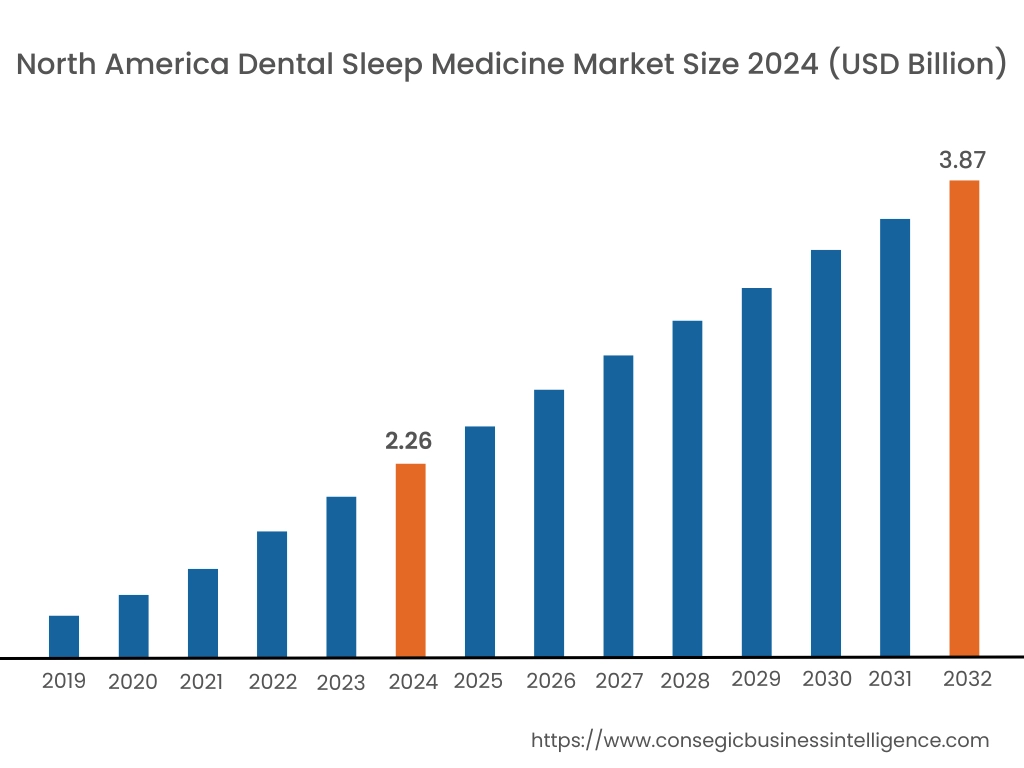

In 2024, North America was valued at USD 2.26 Billion and is expected to reach USD 3.87 Billion in 2032. In North America, the U.S. accounted for the highest share of 73.40% during the base year of 2024. North America holds a significant share in the global dental sleep medicine market, driven by the rising prevalence of sleep disorders such as obstructive sleep apnea (OSA) and bruxism, as well as advanced healthcare infrastructure. The U.S. leads the region due to increasing adoption of oral appliances for managing sleep apnea and strong support from dental associations promoting this market. Canada contributes with growing awareness about the importance of treating sleep-related disorders and increasing access to dental sleep therapies. However, high costs of custom oral appliances may limit adoption among certain patient groups.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 7.7% over the forecast period. The dental sleep medicine market analysis, is fueled by increasing awareness about sleep health, improving healthcare infrastructure, and rising prevalence of OSA in China, India, and Japan. China dominates the market with growing trends for oral appliances and increasing focus on addressing untreated sleep apnea cases. India’s expanding dental healthcare sector supports the adoption of cost-effective therapies, particularly in urban areas. Japan emphasizes precision dental solutions and advanced oral appliances for managing sleep disorders, leveraging its strong R&D capabilities. However, limited awareness in rural areas and affordability challenges may hinder dental sleep medicine market expansion in some parts of the region.

Europe is a prominent for dental sleep medicine market trends, supported by a growing elderly population, increasing prevalence of sleep disorders, and strong collaboration between dental and medical professionals. Countries like Germany, the UK, and France are key contributors. Germany drives demand with its advanced dental care infrastructure and focus on oral appliance therapies for OSA. As per the analysis UK emphasizes public awareness campaigns and expanding access to this specific market in primary care settings, while France invests in integrating dental solutions with multidisciplinary sleep disorder treatments. However, fragmented reimbursement policies across the region may pose challenges to dental sleep medicine market opportunities.

The Middle East & Africa region is witnessing steady growth in the market, driven by increasing investments in healthcare infrastructure and rising awareness about the impact of untreated sleep disorders. Countries like Saudi Arabia and the UAE are adopting advanced oral appliance therapies to manage OSA and bruxism, supported by government-led healthcare modernization initiatives. In Africa, South Africa is emerging as a key market, focusing on improving access to dental care and promoting awareness about sleep health. However, limited availability of trained dental professionals specializing in sleep medicine may restrict market expansion in certain parts of the region.

Latin America is an emerging market, with Brazil and Mexico leading the region. Brazil’s growing healthcare sector and increasing prevalence of OSA and bruxism drive demand for dental sleep therapies, including mandibular advancement devices. As per the dental sleep medicine market analysis, Mexico focuses on raising awareness about the importance of treating sleep disorders and improving access to affordable dental sleep solutions. The region also benefits from collaborations with international dental organizations to train professionals in dental sleep medicine. However, economic instability and inconsistent access to advanced technologies may pose challenges to dental sleep medicine market opportunities.

Top Key Players & Market Share Insights:

The dental sleep medicine market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global dental sleep medicine market. Key players in the dental sleep medicine industry include -

- Koninklijke Philips N.V. (Netherlands)

- ResMed Inc. (United States)

- Vatech Co., Ltd. (South Korea)

- Whole You, Inc. (United States)

- Itamar Medical Ltd. (Israel)

- SomnoMed Ltd. (Australia)

- ProSomnus Sleep Technologies, Inc. (United States)

- Fisher & Paykel Healthcare Corporation Limited (New Zealand)

- Panthera Dental (Canada)

- Airway Management, Inc. (United States)

Dental Sleep Medicine Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 11.95 Billion |

| CAGR (2025-2032) | 7.3% |

| By Product Type |

|

| By Application |

|

| By End User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected size of the Dental Sleep Medicine Market by 2032? +

Dental Sleep Medicine Market size is estimated to reach over USD 11.95 Billion by 2032 from a value of USD 6.80 Billion in 2024 and is projected to grow by USD 7.18 Billion in 2025, growing at a CAGR of 7.3% from 2025 to 2032.

What factors are driving the growth of the Dental Sleep Medicine Market? +

The market growth is driven by the rising prevalence of sleep disorders such as obstructive sleep apnea (OSA) and bruxism, increasing adoption of non-invasive oral appliance therapies, and advancements in dental technologies like CAD/CAM systems and 3D printing.

What challenges are restraining the market? +

Limited awareness about dental sleep medicine solutions, particularly in emerging markets, and high costs of custom-fitted oral appliances coupled with inadequate insurance coverage are significant barriers to market growth.

What opportunities exist in the market? +

Technological advancements, including the integration of 3D printing, digital workflows, and smart oral appliances equipped with sensors, offer significant opportunities for market expansion. Additionally, teledentistry platforms are improving access to consultations and follow-up care in underserved areas.

Which product type dominates the market? +

The Oral Appliances segment, including mandibular advancement devices (MADs) and tongue retaining devices (TRDs), dominates the market due to their effectiveness in managing mild to moderate OSA and snoring.