- Summary

- Table Of Content

- Methodology

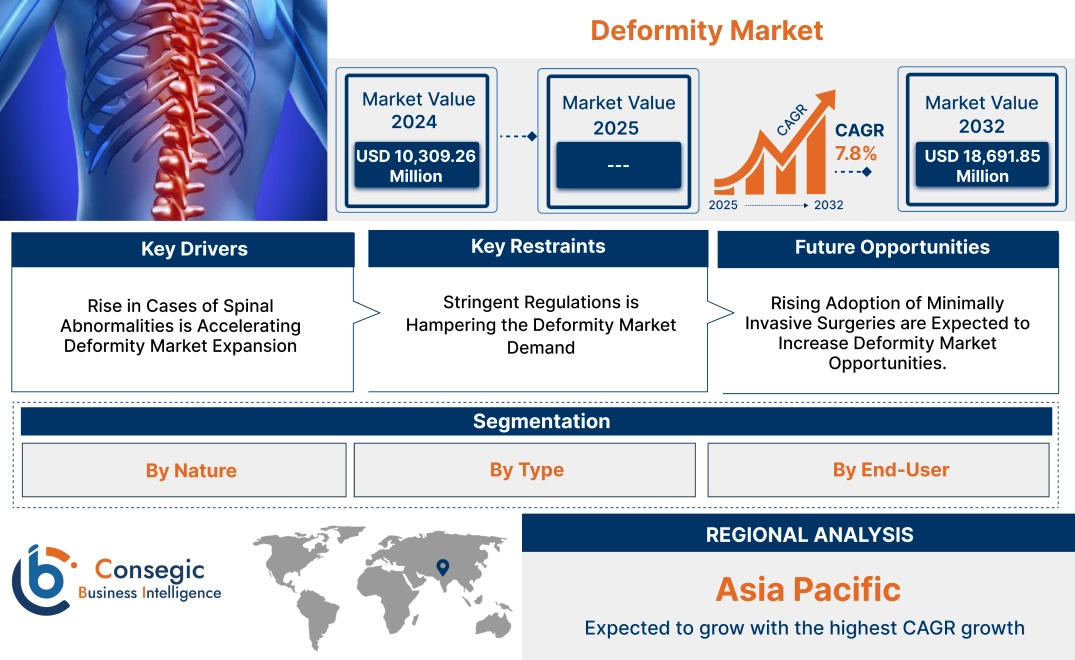

Deformity Market Size:

Deformity Market size is growing with a CAGR of 7.8% during the forecast period (2025-2032), and the market is projected to be valued at USD 18,691.85 Million by 2032 from USD 10,309.26 Million in 2024.

Deformity Market Scope & Overview:

A deformity is an abnormality in the shape or structure of a body part. It results from various factors. By nature, it is categorized into congenital, which is present at birth, resulting from genetic or developmental issues during fetal development, and acquired, which is developed after birth due to factors such as injury, disease, or aging amongst others. By types, it includes spinal deformities (such as scoliosis, kyphosis, and lordosis), limb deformities (such as clubfoot, bowlegs, and knock-knees), and joint deformities (such as osteoarthritis and rheumatoid arthritis) amongst others. Treatment varies depending on the type and severity. Options include surgical procedures (such as spinal fusion, joint replacement, and craniofacial surgery), non-surgical interventions (such as physical therapy, bracing, and medications), and a combination of approaches.

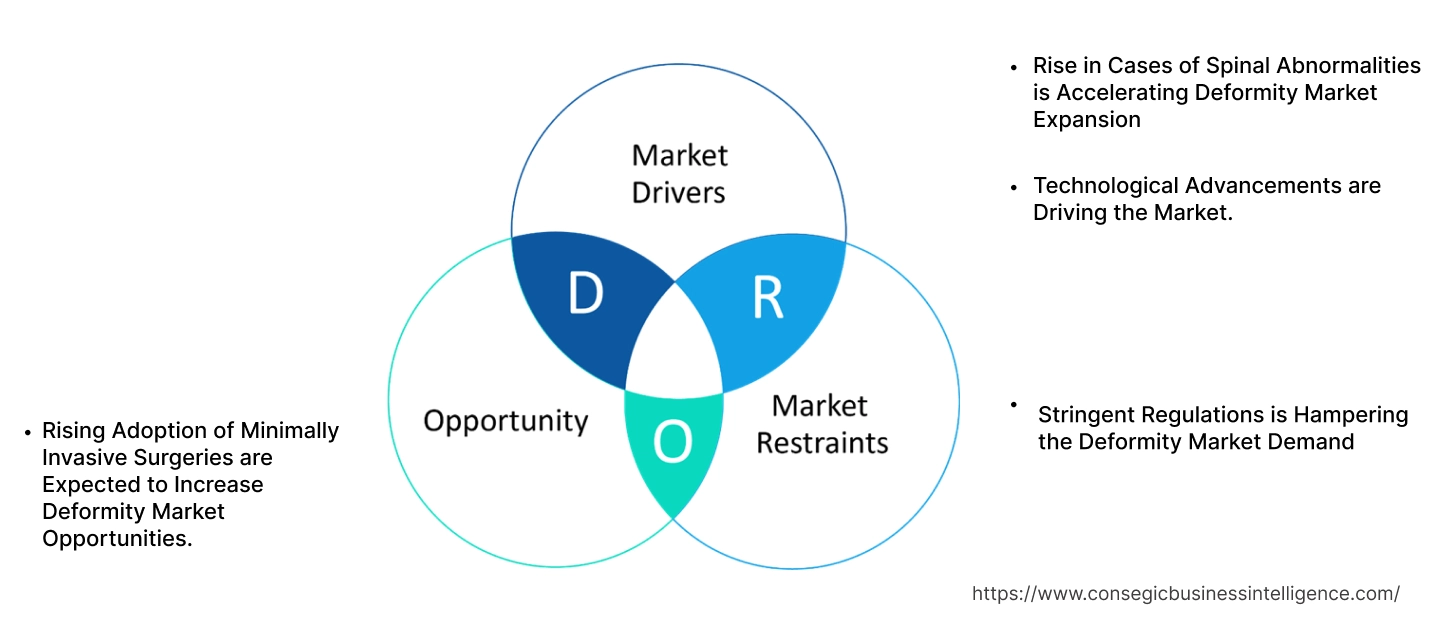

Deformity Market Dynamics - (DRO) :

Key Drivers:

Rise in Cases of Spinal Abnormalities is Accelerating Deformity Market Expansion

Spinal abnormalities refer to irregular curvatures in the spine that disrupt its natural alignment and functionality. The three most common types are scoliosis, kyphosis, and lordosis. Scoliosis is characterized by a sideways curvature of the spine, appearing during adolescence. Kyphosis referred to as a "hunchback," involves an excessive outward curvature of the upper back. Lordosis, also known as "swayback," occurs when the lower back curves excessively inward. These conditions cause pain, difficulty breathing, and limited mobility, affecting daily activities and overall quality of life.

The natural aging process results in degenerative changes such as disc herniation and spinal stenosis, which contribute to spinal defects. Moreover, degenerative diseases such as osteoarthritis and osteoporosis, weaken spinal bones and discs, further contributing to abnormalities. Trauma, such as accidents or falls, also causes spinal fractures leading to structure disturbance. All these factors have led to a higher number of reported cases of spinal abnormalities.

For instance,

- According to an article published by ScoliSMART Clinics, in 2024, approximately 3 million new scoliosis cases are identified annually in the United States. This surge has led to a heightened demand for treatment as well, thereby positively influencing the overall deformity market trends.

Overall, the high increase in spinal abnormalities cases is significantly boosting the deformity market expansion.

Technological Advancements are Driving the Market.

Technological advancements in the market are primarily focused on improving treatment precision, efficiency, and patient outcomes. One key development is the use of advanced imaging technologies. Tools such as 3D imaging are becoming increasingly vital in diagnosing abnormalities and planning corrective surgeries. These technologies allow healthcare providers to visualize the spine, joints, or affected areas in greater detail, ensuring more accurate assessments and treatment plans. Moreover, another significant advancement is the integration of computer-assisted design (CAD) and 3D printing.

For instance,

- According to an article published in ScienceDirect, in 2024, CAD software enables the design of tailored solutions based on a patient’s specific anatomy, which 3D printing then produces. This combination enhances the fitting and functionality of prosthetics and orthotic devices, offering better support and comfort for patients with deformities. This increased its applications, positively influencing the deformity market trends.

Additionally, robotic-assisted surgery has made a significant impact on abnormality correction procedures. Robots provide greater precision in the placement of implants and in performing complex spinal and joint surgeries. This minimizes the risk of complications and enhances recovery times.

Overall, technological advancements, including advanced imaging, 3D printing, and robotic-assisted surgery are accelerating the global deformity market growth.

Key Restraints:

Stringent Regulations is Hampering the Deformity Market Demand

Regulatory hurdles are one of the significant barriers to market growth. Medical devices, implants, and biologics used in treatments are subject to strict regulations by authorities such as the U.S. FDA, the European Medicines Agency (EMA), and other national regulatory bodies. These regulations ensure the safety, efficacy, and quality of products, but they also slow down the time to market for new treatments and devices.

The approval process for orthopedic implants, prosthetics, and surgical tools is lengthy and costly. Manufacturers must conduct extensive clinical trials, demonstrate compliance with safety standards, and prove the effectiveness of their products before they receive approval. This process not only delays the availability of new technologies but also increases the cost of development, which is ultimately passed on to consumers and healthcare providers.

In addition, variations in regulatory standards across different regions further complicate market entry for companies. What is approved in one country takes additional time or requires modifications in another, making it difficult for global companies to maintain a seamless product launch strategy.

Overall, analysis shows that the stringent regulatory requirements, lengthy approval processes, and varying regulatory standards across different regions are hampering the deformity market demand.

Future Opportunities :

Rising Adoption of Minimally Invasive Surgeries are Expected to Increase Deformity Market Opportunities.

As patients increasingly seek less traumatic procedures, the shift towards minimally invasive surgeries (MIS) is gaining popularity. These procedures involve smaller incisions and less disruption to surrounding tissues. Moreover, these procedures carry a lower risk of complications such as infections, which improves patient satisfaction and reduces overall healthcare costs. Additionally, they offer several other benefits over traditional open surgeries.

For instance,

- According to an article published by National Center for Biotechnology Information, in 2025, MIS for deformities offers benefits such as reduced scar length, less postoperative pain, and potentially better correction of severe deformities with lower recurrence rates. This has increased the need for specialized surgical instruments and implants designed for MIS techniques, creating potential for the market.

Furthermore, minimally invasive surgeries aim to address the underlying bony abnormality directly, rather than solely relying on soft tissue corrections. They typically result in shorter hospital stays and faster recovery times, making them an attractive option for patients.

Overall, the rising adoption of minimally invasive surgeries is expected to increase deformity market opportunities.

Deformity Market Segmental Analysis :

By Nature:

Based on nature, the market is categorized into congenital, acquired, and others.

Trends in Nature:

- Acquired deformities due to trauma, arthritis, and degenerative conditions are a growing area of concern.

- Rising prevalence of congenital deformities due to improved prenatal diagnostics and neonatal care.

The acquired segment accounted for the largest market share in 2024

- Acquired deformities develop after birth due to various factors such as injuries, diseases, or aging. Common types include limb length discrepancies, joint contractures, scoliosis, and joint dislocations.

- They significantly impact on a person's quality of life. They cause pain, stiffness, limited range of motion, and difficulty with daily activities. These abnormalities also lead to psychological distress, affecting self-esteem and body image.

- Treatment includes non-surgical approaches such as physical therapy, occupational therapy, bracing, and medications. Surgical interventions involve procedures such as joint replacement, bone grafting, tendon transfers, and corrective surgeries. Health awareness initiatives and public health campaigns are being conducted worldwide.

- For instance, in 2024, Endo, Inc. launched a new TV commercial and disease awareness campaign called "Reminders." This campaign aims to help patients actively participate in their treatment decisions for Dupuytren's contracture, a hand-acquired deformity, affecting millions of Americans. This has increased its reach for patients, a driving segment in the market.

- Overall, as per the market analysis, increasing disease awareness campaigns are driving segmental growth.

The congenital segment is expected to grow at the fastest CAGR over the forecast period.

- Congenital deformities are abnormalities present at birth, resulting from genetic or developmental issues during fetal development. Common types include clubfoot, cleft lip and palate, spina bifida, and certain types of heart defects.

- These abnormalities significantly impact a child's physical and emotional development, affecting their mobility, speech, and social interactions.

- Treatment for congenital abnormalities involves a multidisciplinary approach, including surgery, physical therapy, occupational therapy, and speech therapy. Early intervention and ongoing support are crucial for optimal outcomes.

- As per the market analysis, advancements in surgical techniques and technologies, growing need for improved quality of life, and increasing access to healthcare in developing countries will drive the segment for the upcoming years.

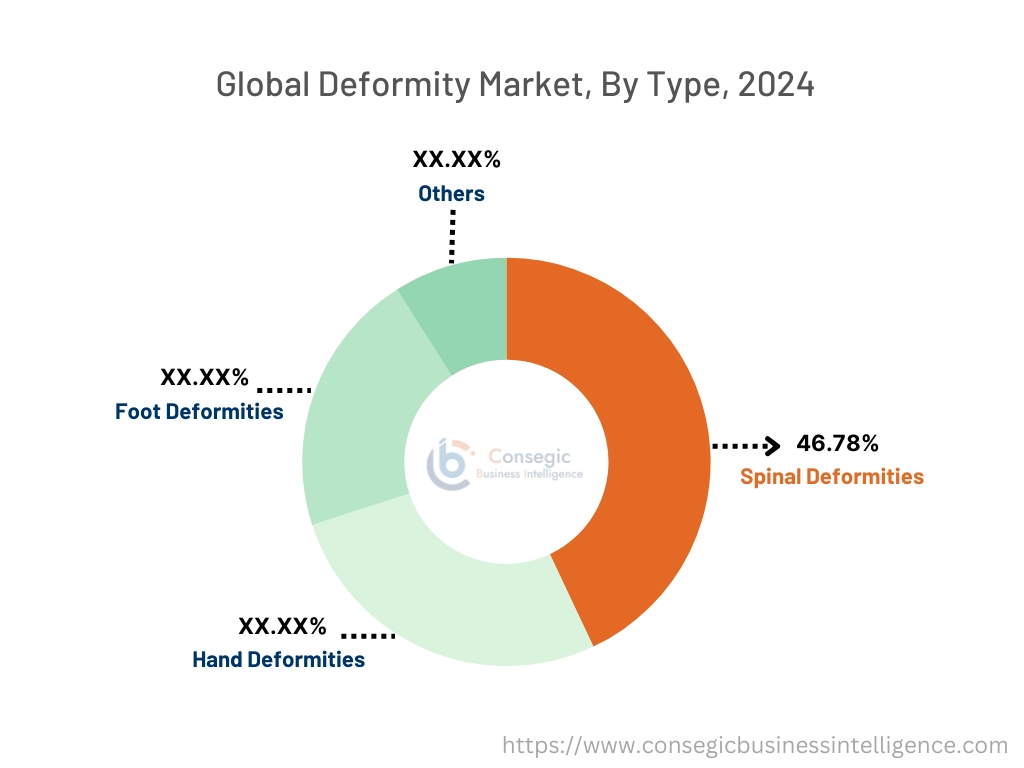

By Type:

The type segment is categorized into spinal deformities, hand deformities, foot deformities, and others.

Trends in the Type:

- Scoliosis continues to be a major focus of research and development within spinal deformities.

- Foot deformities are experiencing growth due to the rising prevalence of diabetes and obesity.

The spinal deformities segment accounted for the largest market share of 46.78% 2024.

- Spinal deformities include conditions such as scoliosis, an abnormal sideways curvature of the spine; kyphosis, an exaggerated forward rounding of the upper spine; and lordosis, an excessive inward curve in the lower back.

- The causes are congenital, arising from birth defects, or acquired, due to aging, trauma, or conditions such as osteoporosis. Poor posture, obesity, and degenerative diseases also contribute. These spinal abnormalities significantly impact quality of life, causing chronic pain, mobility issues, and reduced physical activity.

- Severe cases lead to complications such as nerve compression, breathing difficulties, and emotional distress due to physical appearance. Technological advancements such as the development of innovative spinal implants and instrumentation are driving the segment.

- For instance, in May 2023, the FDA approved Globus Medical, Inc. REFLECT Scoliosis Correction System, a humanitarian device. This system aims to correct spinal curvature in growing children while potentially avoiding the need for spinal fusion surgery. This has increased treatment options, further driving the segment.

- Overall, as per the market analysis advancements in treatment options are driving this segmental growth in the deformity industry.

The foot deformities segment is expected to grow at the fastest CAGR over the forecast period.

- Foot deformities are abnormalities in the structure or function of the foot. Some common foot abnormalities include hammertoes and bunions. Less common abnormalities include conditions such as fused toes (tarsal coalition), clubfoot, flat foot (pes planus), or mallet toes.

- Causes are congenital, acquired (due to injuries or diseases), or related to lifestyle factors such as wearing ill-fitting shoes.

- Foot abnormalities significantly affect the body by altering posture, balance, and gait mechanics. This leads to chronic pain in the feet, knees, hips, or lower back due to improper weight distribution.

- Over time, untreated foot abnormalities contribute to joint degeneration, reduced mobility, and an increased risk of falls or injuries.

- Treatment options include conservative measures such as orthotics, shoe modifications, and physical therapy, as well as surgical interventions in severe cases.

- The rising prevalence of chronic diseases such as diabetes and arthritis, an aging global population, and increasing sports-related injuries create the potential for the segment in the upcoming years.

By End-User:

The end-user segment is categorized into hospitals, clinics, ambulatory surgical centers, and others.

Trends in End-User:

- Technological advancements are driving efficiency and patient outcomes in hospitals.

- The role of rehabilitation centers is expanding in the post-operative care pathway.

The hospital's segment accounted for the largest market share in 2024.

- Hospitals are large healthcare institutions serving as primary treatment centers for complex and severe cases requiring specialized interventions for all types of deformities.

- Hospitals dominate the market due to their superior diagnostic and therapeutic capabilities. They house advanced imaging systems such as MRI and skilled orthopedic surgeons, neurologists, and physiotherapists specialists for accurate diagnosis and effective treatment planning. Additionally, hospitals are better equipped to perform surgical procedures, including minimally invasive ensuring comprehensive care.

- Their dominance is further driven by the high influx of patients due to referral systems, insurance coverage, and the trust associated with hospital-based treatments. The development of healthcare industry infrastructure, especially in emerging economies, also boosts the requirements.

- For instance, according toCEIC, the number of hospitals in China increased by 3.85% from 2022 to 2023, rising from 36 million units to 38 million units. Consequently, this surge in hospitals has contributed to a higher volume of diagnostics and treatments related to deformities, positively driving the segment in the market.

- Overall, high patient volume, advanced infrastructure, and a rising number of hospitals are driving the segment.

The ambulatory surgical centers segment is expected to grow at the fastest CAGR over the forecast period.

- Ambulatory surgical centers (ASCs) are rapidly emerging in the market due to their cost-effective, efficient, and patient-centric approach to treatment. ASCs specialize in performing procedures for conditions such as bunions, hammertoes, and certain spinal abnormalities, making them an attractive option for both patients and healthcare providers.

- With lower overhead costs compared to hospitals, ASCs offer procedures at reduced prices, addressing the rising demand for affordable healthcare solutions. Additionally, ASCs provide a less intimidating, more personalized environment than hospitals, enhancing patient satisfaction.

- A key factor driving the growth of ASCs is the increasing adoption of minimally invasive techniques, which require shorter recovery times and allow patients to return home on the same day. This convenience has boosted patient preference, especially for outpatient procedures.

- Advances in medical technology, such as robotic-assisted surgeries and improved anesthesia protocols, have further expanded the scope of these deformities’ treatments available at ASCs.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

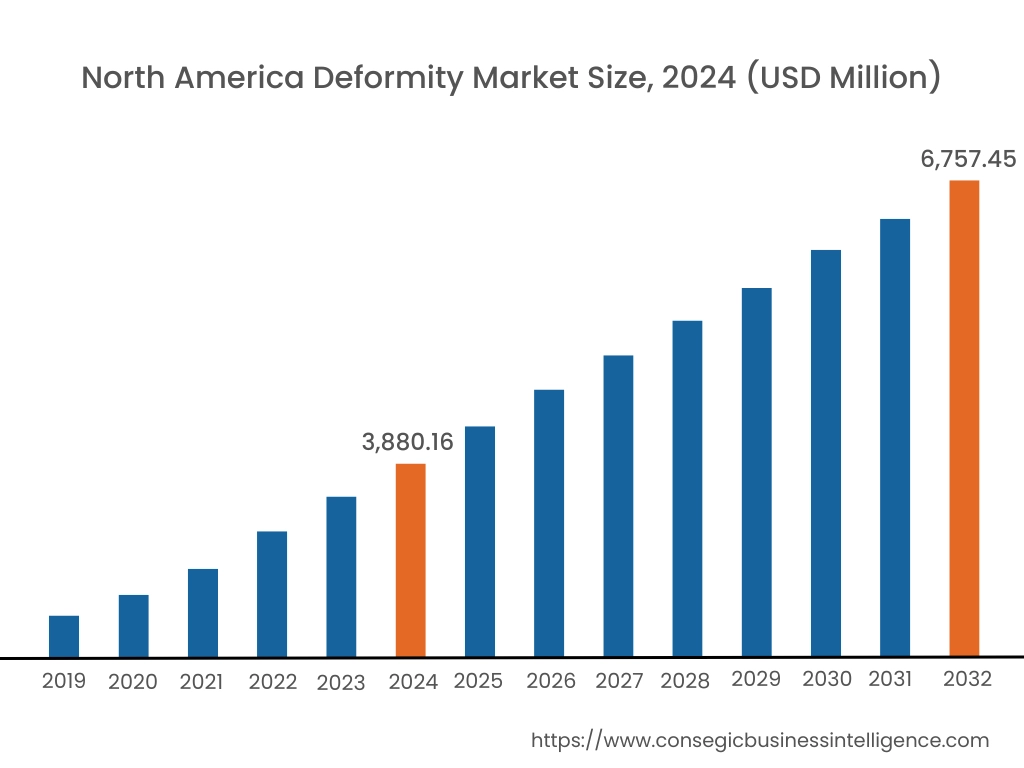

In 2024, North America accounted for the highest deformity market share at 37.64% and was valued at USD 3,880.16 Million and is expected to reach USD 6,757.45 Million in 2032. In North America, the U.S. accounted for the highest deformity market share of 71.11% during the base year of 2024. The market is driven by several key trends. The region has a well-established healthcare system with access to state-of-the-art diagnostic and treatment facilities, making it a global leader in managing complex abnormalities such as scoliosis, kyphosis, and foot abnormalities. Moreover, the aging population in the region is a significant driver, as older individuals are more prone to acquired deformities such as degenerative spinal conditions and osteoarthritis-related issues. Additionally, lifestyle factors such as obesity and sedentary habits contribute to the rising incidence of deformities in the region. Furthermore, the development of new devices, implants, and biologics, further boosts the market.

- In 2024, Eminent Spine announced 510(k) clearance by the FDA for their scoliosis deformity pedicle screw system, thereby expanding treatment options for patients, and positively impacting the market.

Overall, a robust healthcare system, an aging population, lifestyle factors, and continuous advancements in medical technology, exemplified by innovations, are driving the market in the region.

In Asia Pacific, the deformity market is experiencing the fastest growth with a CAGR of 8.8% over the forecast period. The market is driven by its large and aging population, which drives the need for spinal and joint abnormalities treatments. Countries such as China, Japan, and India have rapidly growing elderly populations, who are more susceptible to acquired deformities such as kyphosis and osteoarthritis-related joint issues, driving the market. Moreover, governments in countries such as China and India are investing in expanding healthcare infrastructure, which includes specialized facilities for diagnosis and treatment. Additionally, the growing middle-class population in APAC is increasingly seeking advanced treatments for functional and cosmetic deformities, further driving the market. Furthermore, APAC is also experiencing a rise in trauma-related abnormalities due to high road traffic accidents and workplace injuries, particularly in developing countries. This has led to increased requirements for surgical and non-surgical interventions, bolstering the market.

Europe's deformity market analysis states that several trends are responsible for the progress of the market in the region. Aging populations in countries such as Germany, Italy, and France are driving the demand for abnormality treatments, particularly for spinal conditions and osteoarthritis-related joint abnormalities. Another driving factor is the high healthcare standards and advanced medical technologies available across Europe. Countries with well-established healthcare systems, such as the UK and Switzerland, offer access to cutting-edge treatments, including minimally invasive surgeries and robotic-assisted procedures. Additionally, European governments' strong emphasis on public health policies and initiatives aimed at improving the quality of life for the elderly contribute to the market. The region's innovative medical device manufacturers continue to develop effective and affordable solutions for abnormality management, further stimulating the market.

The Middle East and Africa (MEA) deformity market analysis states that the region is also witnessing a notable surge. The market is driven by growing healthcare investments and the rise of private healthcare sectors in countries such as the UAE, Saudi Arabia, and South Africa. These nations have heavily invested in expanding medical facilities and infrastructure, enabling improved access to advanced abnormality treatments. Moreover, the increasing prevalence of chronic diseases such as osteoarthritis and scoliosis, along with a growing geriatric population, contributes significantly to the market. Additionally, government health initiatives and reimbursement programs in the MEA region support the affordability of treatments. The region's rising awareness about orthopedic care and abnormalities prevention, especially among the middle class, has fueled the need for more accessible treatment options.

Latin America's deformity market size is also emerging. Countries such as Brazil and Mexico are investing heavily in expanding healthcare infrastructure and improving access to deformity treatments. As disposable incomes rise, individuals are increasingly seeking specialized care for abnormalities such as scoliosis and joint issues. Another important factor is the growing prevalence of trauma-related abnormalities due to accidents, which are common in the region due to high road traffic incidents. This increases the need for surgical interventions and rehabilitation services. Additionally, improvements in medical technology and the development of more accessible orthotic devices are further stimulating the market. Aging populations in countries such as Argentina and Chile are also contributing to the market. This demographic trend is pushing the need for both surgical and non-surgical treatment options.

Top Key Players and Market Share Insights:

The Deformity market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D) and product innovation to hold a strong position in the global Deformity market. Key players in The Deformity industry include-

- NuVasive (U.S.)

- Spinal Technology, LLC. (U.S.)

- Pfizer (U.S.)

- Chaneco Orthopaedic (UK)

- Zimmer Biomet (U.S.)

- OrthoPediatrics (U.S.)

- DePuy Synthes (U.S.)

- Bristol Myers Squibb (U.S.)

- Braun (Germany)

- Stryker Corporation (U.S.)

Recent Industry Developments :

Product Launch:

- In July 2023, Globus Medical launched their new MARVEL Growing Rod System, designed specifically for the treatment of early-onset scoliosis.

- In January 2023, Orthofix Medical officially launched its Mariner deformity pedicle screw system for commercial use.

Deformity Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 18,691.85 Million |

| CAGR (2025-2032) | 7.8% |

| By Nature |

|

| By Type |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Deformity market? +

In 2024, the Deformity market is USD 10,309.26 Million.

Which is the fastest-growing region in the Deformity market? +

Asia Pacific is the fastest-growing region in the Deformity market.

What specific segmentation details are covered in the Deformity market? +

Nature and Type segmentation details are covered in the Deformity market.

Who are the major players in the Deformity market? +

NuVasive (U.S.), Spinal Technology, LLC. (U.S.), OrthoPediatrics (U.S.), DePuy Synthes (U.S.), Bristol Myers Squibb (U.S.), B.Braun (Germany), Stryker Corporation (U.S.), Pfizer (U.S.), Chaneco Orthopaedic (UK), and Zimmer Biomet (U.S.).