- Summary

- Table Of Content

- Methodology

Data Compression Software Market Size:

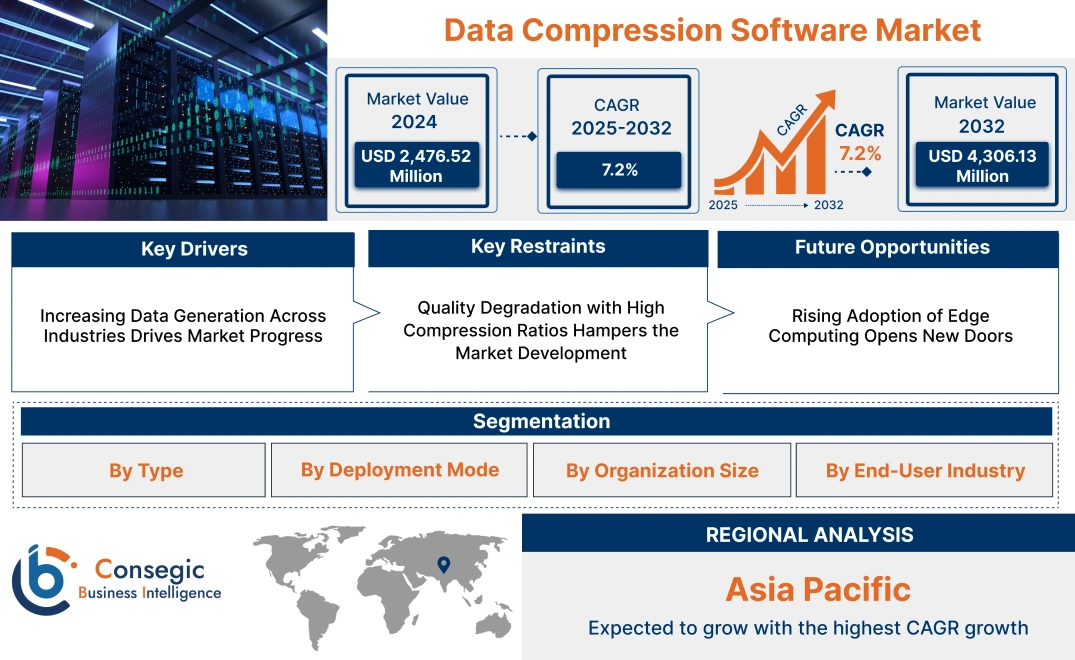

Data Compression Software Market size is estimated to reach over USD 4,306.13 Million by 2032 from a value of USD 2,476.52 Million in 2024 and is projected to grow by USD 2,609.71 Million in 2025, growing at a CAGR of 7.2% from 2025 to 2032.

Data Compression Software Market Scope & Overview:

Data compression software refers to tools designed to reduce the size of digital files and datasets without significant loss of information or quality. These solutions enable efficient storage, faster transmission, and optimized utilization of bandwidth in various applications, including data management, communication, and storage systems. By compressing files into smaller formats, this software enhances storage efficiency and improves data handling capabilities.

These tools support multiple compression methods, including lossless and lossy techniques, to cater to different operational needs. They are compatible with various file types such as text, images, videos, and databases, ensuring versatility and broad applicability. Advanced features in modern compression software include encryption, real-time compression, and integration with cloud storage systems, enabling seamless functionality and security.

End-users of data compression software include enterprises, data centers, media and entertainment companies, and government organizations that require efficient data storage and transmission. These solutions play a critical role in optimizing digital workflows and improving overall operational efficiency.

Data Compression Software Market Dynamics - (DRO) :

Key Drivers:

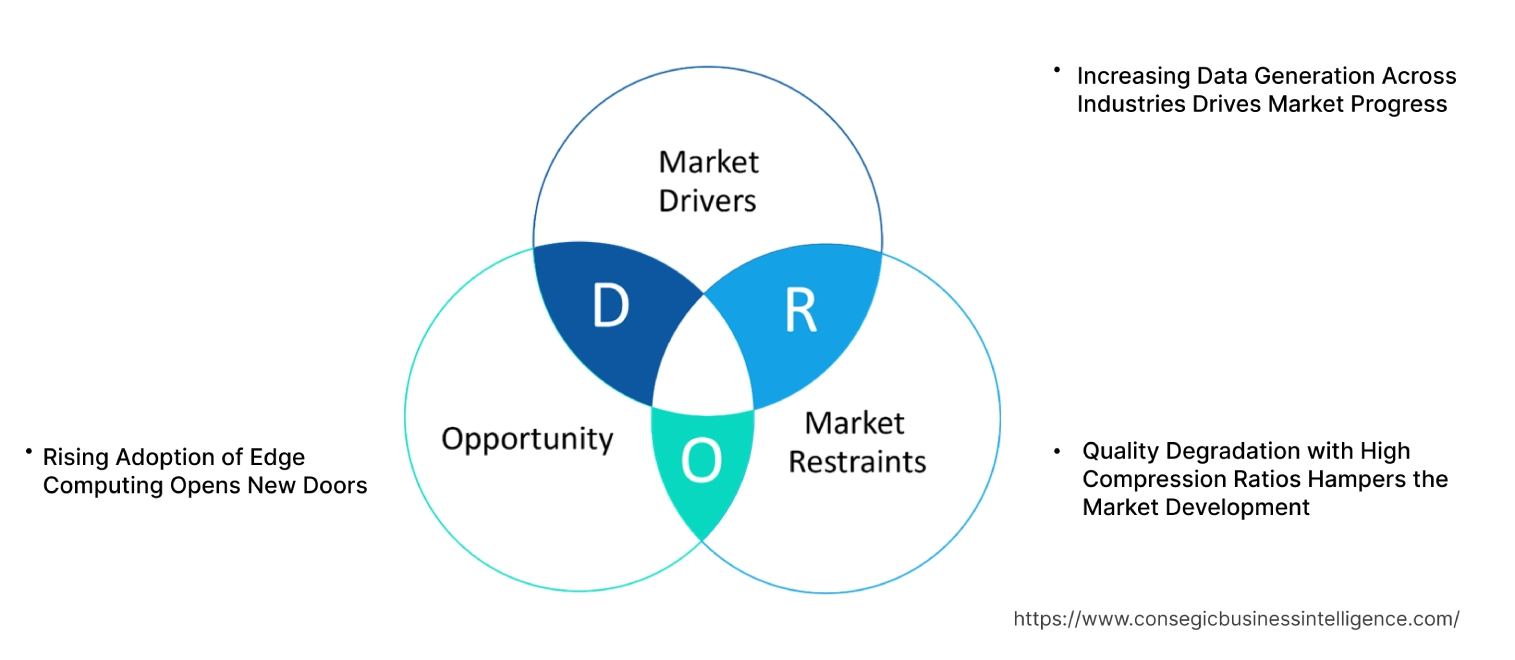

Increasing Data Generation Across Industries Drives Market Progress

The exponential growth of digital data across industries such as healthcare, finance, e-commerce, and entertainment has created an urgent need for efficient storage and transmission solutions. The surge in activities like electronic health records, online transactions, video streaming, and big data analytics generates massive datasets, challenging existing storage and network infrastructures. Compression tools play a critical role in addressing these challenges by reducing data size without compromising quality or integrity.

By optimizing storage requirements and improving transmission efficiency, these tools ensure smoother workflows and reduced operational costs. Industries relying on high-volume data processing benefit from faster data transfer, streamlined storage, and enhanced accessibility. As data generation continues to escalate, the demand for advanced compression technologies tailored to specific use cases is expected to grow, making these tools indispensable for managing the complexities of modern data ecosystems. Thus, the aforementioned factors are driving the data compression software market growth.

Key Restraints:

Quality Degradation with High Compression Ratios Hampers the Market Development

A major limitation of compression software is the significant quality degradation that occurs when high compression ratios are applied. This is especially problematic for images, where excessive compression leads to reduced visual fidelity and clarity, rendering the data less useful for applications that demand precision. Lossy compression methods exacerbate this issue by permanently discarding data to reduce file size, making it impossible to fully restore the original quality. Such limitations pose significant restraints for industries like healthcare, media, and design, where high-quality visuals are essential, hindering the data compression software market demand.

Future Opportunities :

Rising Adoption of Edge Computing Opens New Doors

The growth of edge computing has created a significant demand for efficient data handling solutions, as processing and storing data closer to its source reduces latency and enhances operational efficiency.

Data compression technologies play a vital role in these environments by minimizing data size, enabling faster transfer, and reducing storage requirements. This capability is particularly critical in edge applications like IoT devices, healthcare monitoring systems, and automotive operations, where large volumes of data must be processed in real-time. By optimizing bandwidth usage and improving response times, compression tools facilitate seamless operations in resource-constrained edge infrastructures. As the edge computing ecosystem continues to expand across industries, the integration of compression solutions is becoming indispensable, driving data compression software market opportunities.

Data Compression Software Market Segmental Analysis :

By Type:

Based on type, the market is segmented into lossless compression and lossy compression.

The lossless compression segment held the largest revenue of the total data compression software market share in 2024.

- Lossless compression ensures data integrity by retaining the original information, making it essential for industries like BFSI and healthcare where accuracy is critical.

- This segment is widely adopted in professional applications, including data archiving, backup solutions, and enterprise file management.

- Its popularity is driven by regulatory requirements and the need for high-fidelity data preservation across industries.

- The dominance of lossless compression is further attributed to its integration into business workflows for compressing sensitive files without compromising their quality, contributing to the data compression software market expansion.

The lossy compression segment is anticipated to grow at the fastest CAGR during the forecast period.

- Lossy compression is extensively used in media and entertainment applications, such as video streaming and image storage, where data size reduction is prioritized over precision.

- This segment is supported by the increasing adoption of streaming platforms and the growth in consumption of multimedia content worldwide.

- Technological advancements in algorithms for lossy compression ensure reduced data sizes while maintaining acceptable quality for end-users.

- As per market analysis, the expanding use of lossy compression in consumer applications like social media platforms and mobile apps further boosts data compression software market growth.

By Deployment Mode:

Based on deployment mode, the market is categorized into on-premise and cloud-based.

The cloud-based segment accounted for the largest revenue of the total data compression software market share in 2024 and is projected to grow at the fastest CAGR during the forecast period..

- Cloud-based data compression solutions offer scalability and remote accessibility, making them ideal for distributed enterprises and SMEs.

- Their adoption is fueled by the growing shift toward cloud environments for secure and flexible data management.

- Integration with leading cloud storage platforms like AWS, Google Cloud, and Azure enhances the efficiency and usability of cloud-based compression tools.

- As per the data compression software market analysis, the dominance of this segment is also driven by reduced infrastructure costs and the ease of updates for cloud-based applications.

By Organization Size:

Based on organization size, the market is divided into small & medium enterprises (SMEs) and large enterprises.

The large enterprises segment held the largest market share in 2024.

- Large organizations generate vast amounts of data daily, necessitating robust compression solutions to optimize storage and reduce transmission times.

- Enterprise-grade data compression software integrates advanced features like automated workflows and seamless compatibility with existing IT systems.

- The segment's dominance is supported by the growing focus on minimizing operational costs without compromising data accessibility.

- Thus, large enterprises rely on data compression for managing heavy file formats, including multimedia, big data, and enterprise applications, fueling the data compression software market demand.

The small & medium enterprises (SMEs) segment is expected to grow at the fastest CAGR during the forecast period.

- SMEs are increasingly adopting cloud-based compression solutions due to their affordability and ease of use.

- The rising trend of digital transformation among SMEs accelerates the deployment of data compression tools for streamlining operations.

- Flexible subscription models and scalable solutions make data compression software accessible to small businesses with limited IT budgets.

- Therefore, enhanced focus on improving storage efficiency and reducing costs further drives the adoption of data compression software among SMEs, creating significant data compression software market opportunities.

By End-User Industry:

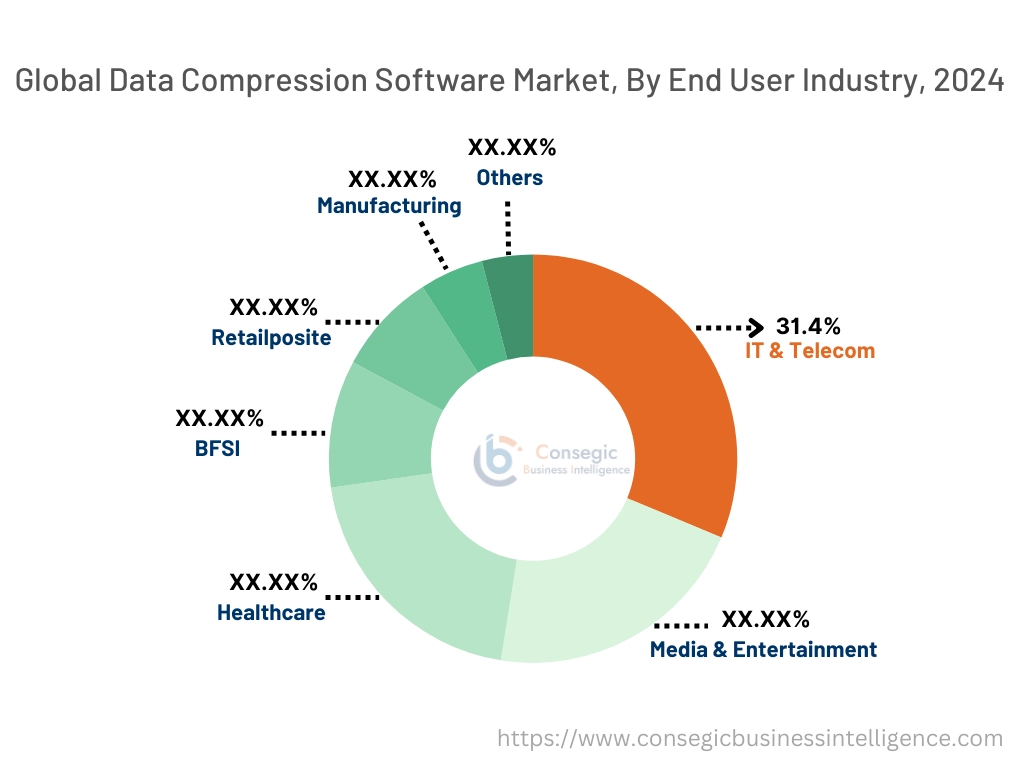

Based on the end-user industry, the market is segmented into IT & telecom, media & entertainment, healthcare, BFSI, retail, manufacturing, and others.

The IT & telecom segment held the largest revenue of 31.4% share in 2024.

- IT & telecom companies rely heavily on data compression software for reducing bandwidth usage and enhancing file transfer speeds.

- These solutions are critical for optimizing data-intensive processes like cloud computing, content delivery networks (CDNs), and enterprise communication systems.

- The segment's dominance is attributed to the growth in the need for efficient data management in telecom infrastructures and IT operations.

- As per the data compression software market analysis, advancements in telecommunication technologies, such as 5G and edge computing, further amplify the use of compression tools in this sector.

The media & entertainment segment is expected to register the fastest CAGR during the forecast period.

- The proliferation of video-on-demand platforms and online streaming services drives the need for advanced compression solutions to manage high-quality multimedia files.

- Compression tools in this sector help reduce data sizes while maintaining quality, enabling smooth playback and user experiences.

- The increasing consumption of online content, including video, images, and music, creates significant opportunities for this segment.

- As per the data compression software market trends, innovations in media compression algorithms tailored for streaming platforms and content creators further fuel the segment's growth.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

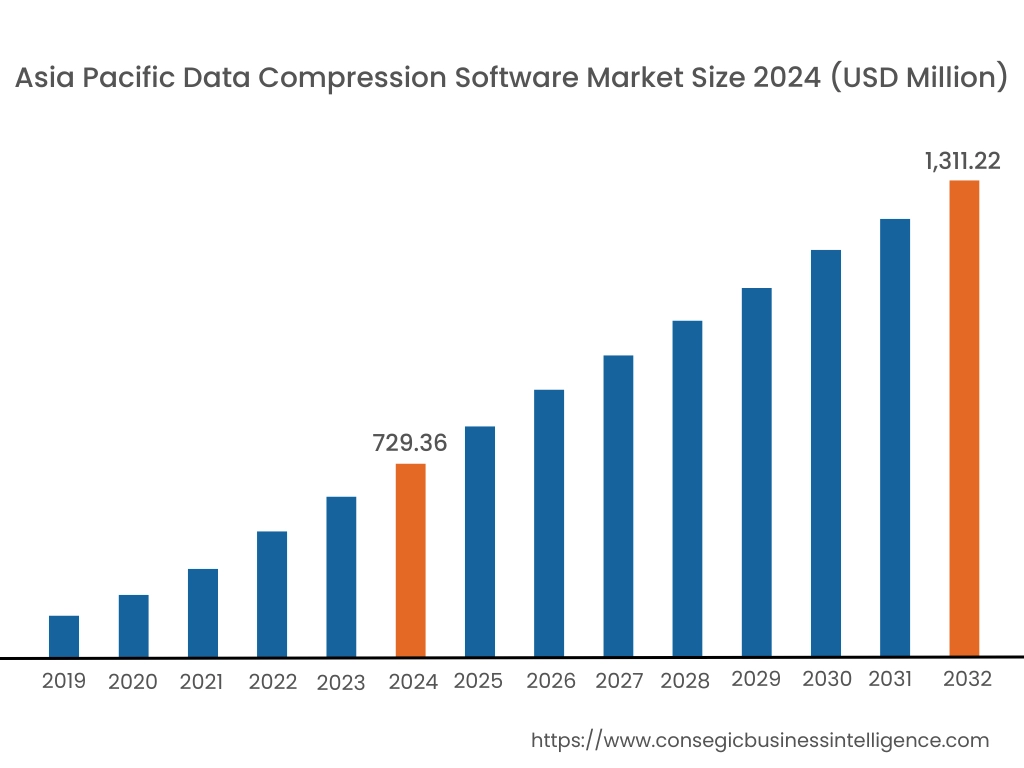

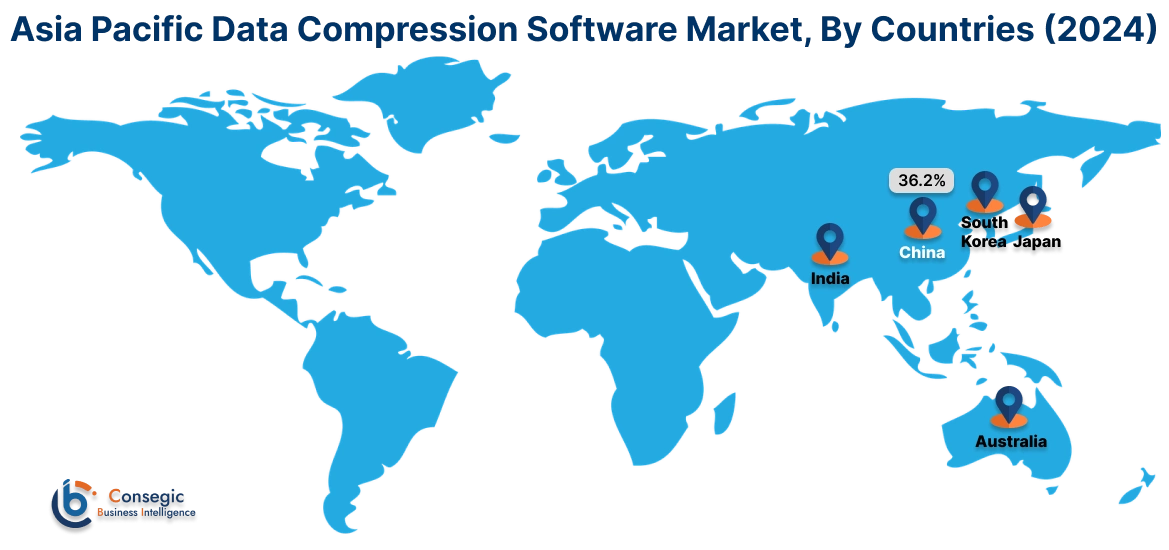

Asia Pacific region was valued at USD 729.36 Million in 2024. Moreover, it is projected to grow by USD 770.75 Million in 2025 and reach over USD 1,311.22 Million by 2032. Out of this, China accounted for the maximum revenue share of 36.2%. The Asia-Pacific region is experiencing rapid advancements in the data compression software market, driven by industrial expansion and technological progress in countries such as China, Japan, and South Korea. The proliferation of digital services and the increasing adoption of IoT devices have intensified the need for efficient data compression solutions. Government initiatives supporting digital transformation further influence data compression software market expansion.

North America is estimated to reach over USD 1,395.62 Million by 2032 from a value of USD 821.48 Million in 2024 and is projected to grow by USD 864.01 Million in 2025. This region holds a significant share of the data compression software market, driven by high data generation and a strong awareness of data management solutions. The United States and Canada are prominent markets, with technological innovations enhancing product offerings. A notable trend is the integration of advanced compression algorithms to optimize storage and transmission efficiency. Analysis indicates that the presence of key industry players and continuous investment in research and development contribute to the region's market prominence.

Europe represents a substantial segment of the global data compression software market, with countries like Germany, France, and the United Kingdom leading in adoption and innovation. The region's emphasis on data privacy and stringent regulatory frameworks has propelled the utilization of efficient data management solutions. Analysis reveals a growing trend towards deploying data compression software in cloud computing and Internet of Things (IoT) applications to optimize storage and boost network efficiency.

The Middle East & Africa region is gradually embracing data compression technologies, particularly within the telecommunications and media sectors. Nations like the United Arab Emirates are investing in modern IT solutions to enhance data management capabilities and comply with international standards. Analysis suggests an emerging trend towards adopting data compression software to optimize bandwidth utilization and improve data transmission efficiency.

Latin America is an emerging market for data compression software, with countries such as Brazil and Mexico contributing to its development. The region's focus on digital modernization and the expansion of the IT & telecommunication sector has spurred interest in data management solutions. As per the market trends, government policies aimed at enhancing technological capabilities influence market growth.

Top Key Players and Market Share Insights:

The Data Compression Software market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Data Compression Software market. Key players in the Data Compression Software industry include -

- WinZip (Canada)

- PKWARE, Inc. (USA)

- RARLAB (Eugene Roshal) (Russia)

- NEC Corporation (Japan)

- Ashampoo GmbH & Co. KG (Germany)

- Corel Corporation (Canada)

- 7-Zip (Igor Pavlov) (Russia)

- Smith Micro Software, Inc. (USA)

- Cloudflare, Inc. (USA)

Recent Industry Developments:

Partnerships & Collaborations:

- In December 2024, Reticulate Micro and K2 Endeavor partnered to create RMX, a company combining military-grade video compression technology with decades of telecom expertise. RMX aims to revolutionize commercial data compression by enhancing bandwidth efficiency, reducing costs, and delivering superior streaming. This innovation targets growing global data demands, redefining connectivity and efficiency across industries.

Product Enhancements:

- In June 2024, STMicroelectronics enhances TouchGFX 4.22 with advanced lossless image compression, optimizing memory usage with algorithms like L4, RLE1, and LZW9, achieving up to 99% compression. This feature helps designers reduce hardware costs by allowing smaller flash ICs without compromising performance or quality. Additionally, the new Live Callouts feature offers real-time tips and insights within the design environment, enhancing usability and productivity.

Data Compression Software Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 4,306.13 Million |

| CAGR (2025-2032) | 7.2% |

| By Type |

|

| By Deployment Mode |

|

| By Organization Size |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Data Compression Software market? +

The Data Compression Software Market size is estimated to reach over USD 4,306.13 Million by 2032 from a value of USD 2,476.52 Million in 2024 and is projected to grow by USD 2,609.71 Million in 2025, growing at a CAGR of 7.2% from 2025 to 2032.

What are the key segments in the Data Compression Software market? +

The Data Compression Software market is segmented by type, deployment mode, organization size, end-user industry, and region. The market is divided into lossless compression and lossy compression based on type. Deployment mode includes on-premise and cloud-based solutions. By organization size, it includes small & medium enterprises (SMEs) and large enterprises. The end-user industries include IT & telecom, media & entertainment, healthcare, BFSI, retail, manufacturing, and others. The regional segments are Asia-Pacific, Europe, North America, Latin America, and the Middle East & Africa.

Which segment is expected to grow the fastest in the Data Compression Software market? +

The lossless compression segment is expected to hold the largest revenue share in 2024 due to its critical role in industries such as BFSI and healthcare, where data integrity is essential. However, the lossy compression segment is expected to grow at the fastest CAGR during the forecast period, driven by its widespread use in media and entertainment, especially in video streaming and image storage applications.

Who are the major players in the Data Compression Software market? +

Key players in the Data Compression Software market include WinZip (Canada), PKWARE, Inc. (USA), Corel Corporation (Canada), 7-Zip (Igor Pavlov) (Russia), Smith Micro Software, Inc. (USA), Cloudflare, Inc. (USA), Ashampoo GmbH & Co. KG (Germany), RARLAB (Eugene Roshal) (Russia), and NEC Corporation (Japan).