- Summary

- Table Of Content

- Methodology

Data Center Structured Cabling Market Size:

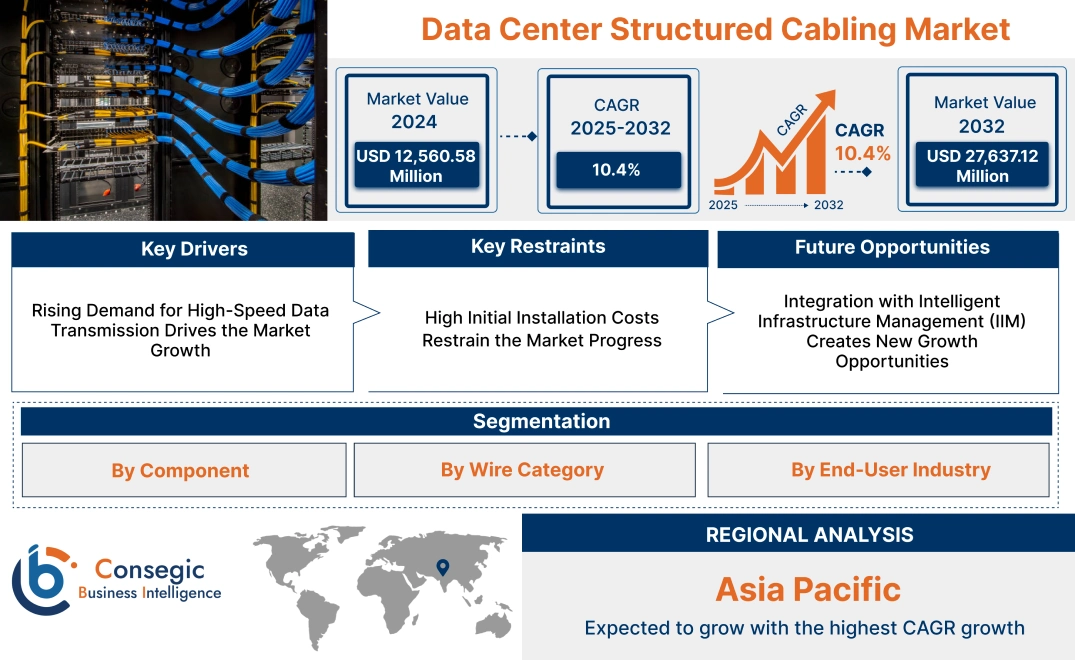

Data Center Structured Cabling Market size is estimated to reach over USD 27,637.12 Million by 2032 from a value of USD 12,560.58 Million in 2024 and is projected to grow by USD 13,638.05 Million in 2025, growing at a CAGR of 10.4% from 2025 to 2032.

Data Center Structured Cabling Market Scope & Overview:

The data center structured cabling focuses on systems designed to organize and manage cabling infrastructure within data centers efficiently. These systems ensure seamless connectivity between servers, storage devices, and networking equipment, supporting high-performance computing and data transmission. Structured cabling provides a standardized approach to cabling management, simplifying maintenance and reducing downtime.

These cabling solutions include components such as fiber optic cables, copper cables, patch panels, and racks, tailored to meet the specific requirements of data centers. They are designed for scalability, enabling data centers to adapt to future expansions and evolving technology. By maintaining organized cabling layouts, these systems enhance airflow, reduce clutter, and improve overall operational efficiency.

End-users include hyperscale data centers, colocation facilities, and enterprise data centers that require reliable and organized cabling systems for uninterrupted operations. These solutions play a vital role in ensuring the reliability and efficiency of modern data center infrastructure.

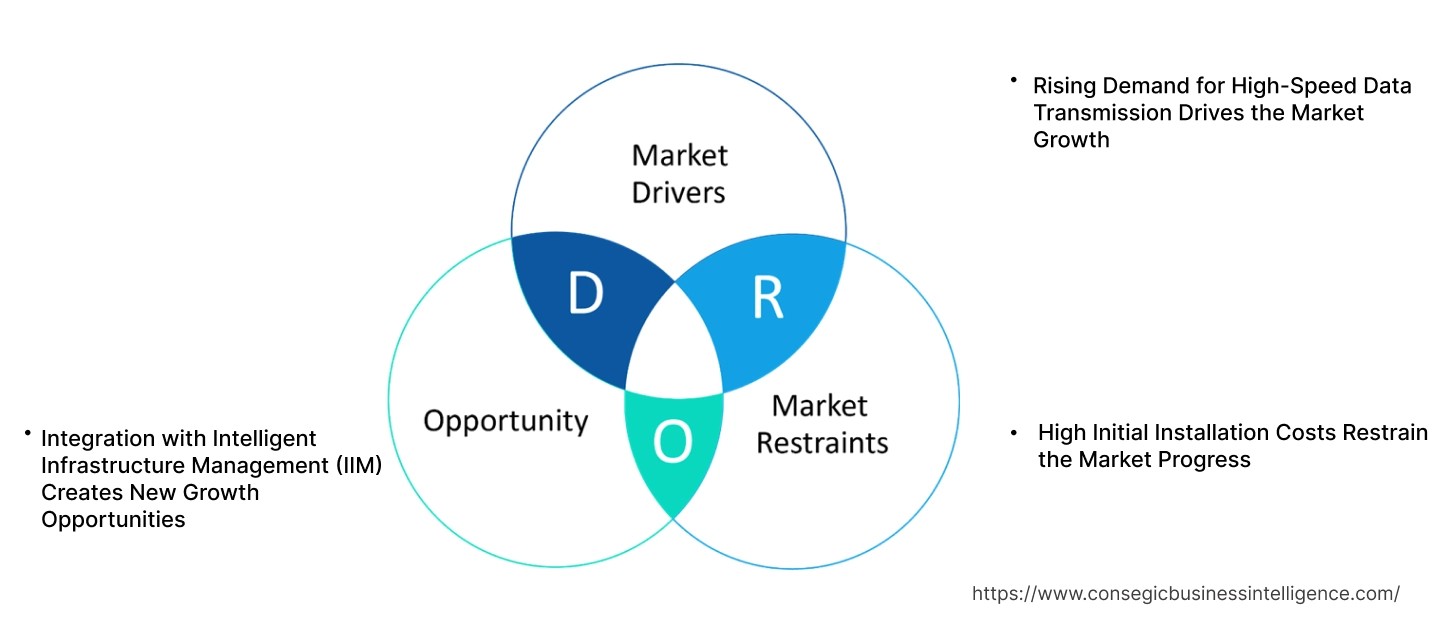

Data Center Structured Cabling Market Dynamics - (DRO) :

Key Drivers:

Rising Demand for High-Speed Data Transmission Drives the Market Growth

The rapid expansion of data-intensive industries, such as cloud computing, IoT, and big data analytics, is fueling the requirement for high-speed data transmission. Modern applications require networks that handle massive data volumes with minimal latency, ensuring uninterrupted performance. Structured cabling systems provide a robust and standardized framework for seamless data flow across high-performance environments, enabling faster communication and reduced signal interference. Their scalability and reliability make them indispensable for next-generation network infrastructure, where speed and efficiency are critical.

As businesses increasingly adopt digital transformation strategies, the need for efficient cabling solutions to support advanced technologies like artificial intelligence and 5G networks continues to rise. This growing reliance on data-driven systems underscores the importance of structured cabling in meeting evolving connectivity demands, enhancing operational efficiency, and future-proofing network infrastructure. Therefore, the aforementioned factors are driving the data center structured cabling market growth.

Key Restraints:

High Initial Installation Costs Restrain the Market Progress

Structured cabling systems involve substantial upfront costs, including expenses for high-quality cables, connectors, and related hardware. The complexity of planning and installation further adds to the overall investment, as it requires skilled labor and meticulous design to ensure optimal performance. These high initial costs often deter smaller data centers or emerging businesses that operate on limited budgets, creating a barrier to entry.

For startups or organizations with constrained financial resources, the long-term benefits of structured cabling do not outweigh the immediate financial burden. This financial constraint restricts the widespread adoption of structured cabling systems, particularly in markets where cost efficiency is a primary concern. As a result, the high capital expenditure remains a critical restraint in the market, limiting its accessibility to larger enterprises or well-established data centers. Thus, the above mentioned factors hamper the data center structured cabling market demand.

Future Opportunities :

Integration with Intelligent Infrastructure Management (IIM) Creates New Growth Opportunities

The integration of structured cabling systems with Intelligent Infrastructure Management (IIM) software is revolutionizing data center operations. These smart cabling solutions enable real-time monitoring of the entire network infrastructure, providing insights into cable performance and connectivity issues. Features such as automated alerts and notifications for faults or disruptions enhance operational efficiency by enabling quick troubleshooting and minimizing downtime.

Additionally, IIM-supported systems streamline cable management, ensuring optimal space utilization and reducing the risk of human errors during installation or upgrades. This integration is particularly valuable for large-scale data centers managing complex and high-density cabling networks. By leveraging IIM, operators achieve greater transparency, enhanced reliability, and efficient maintenance, aligning with industry trends focused on automation and intelligent infrastructure. The ability to optimize network performance while reducing operational inefficiencies positions these solutions as a critical driver, creating significant data center structured cabling market opportunities.

Data Center Structured Cabling Market Segmental Analysis :

By Component:

Based on components, the market is segmented into hardware, software, and professional services.

The hardware segment accounted for the largest revenue of the total data center structured cabling market share in 2024.

- Hardware components such as cables, connectors, and patch panels form the backbone of data center infrastructure, ensuring seamless data transmission.

- The increasing deployment of high-capacity data centers across industries has driven the need for robust and reliable hardware solutions.

- Advanced cabling solutions with high-speed capabilities and minimal signal loss are critical for meeting modern data center requirements.

- The dominance of hardware is attributed to its indispensability in creating efficient and scalable network architectures, enabling businesses to handle massive data loads effectively, and contributing to the data center structured cabling market expansion.

The professional services segment is expected to grow at the fastest CAGR during the forecast period.

- Professional services include installation, design, and maintenance, ensuring that structured cabling systems function optimally.

- Growth in investments in modernizing existing data center facilities has amplified the need for expert consulting and support services.

- Customized cabling solutions tailored to specific organizational needs are enhancing the relevance of professional services.

- As per the data center structured cabling market analysis, the rapid extension of professional services reflects the need for expertise in integrating advanced cabling solutions with emerging technologies.

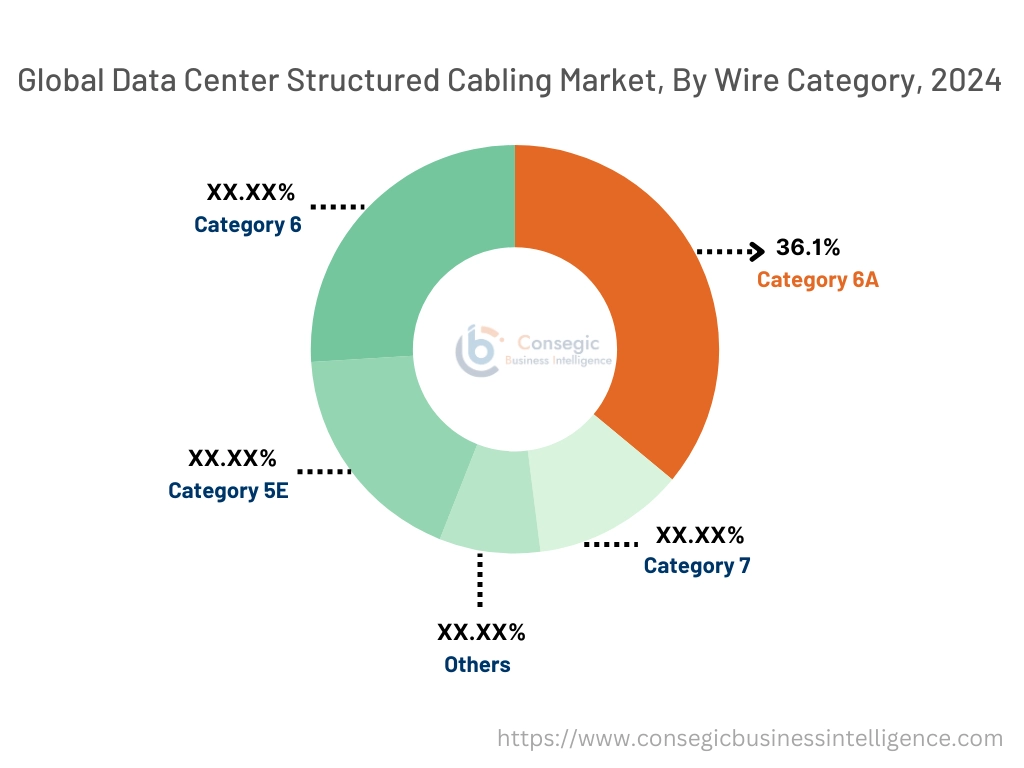

By Wire Category:

Based on the wire category, the market is segmented into Category 5E, Category 6, Category 6A, Category 7, and others.

The Category 6A segment held the largest revenue of 36.1% of the total data center structured cabling market share in 2024.

- Category 6A cables offer superior performance in terms of data transfer rates and bandwidth, making them ideal for modern data center applications.

- These cables are widely used in high-speed networks to support 10Gbps and higher data transmission speeds.

- Increasing need for high-performance cabling in hyperscale and enterprise data centers drives the adoption of Category 6A solutions.

- As per the data center structured cabling market trends, the dominance of this segment reflects its capability to support low latency and high-frequency applications critical for data-intensive industries.

The Category 7 segment is projected to grow at the fastest CAGR during the forecast period.

- Category 7 cables provide enhanced shielding to reduce crosstalk and electromagnetic interference, ensuring reliable network performance.

- The segment's rapid growth is driven by the increasing deployment of next-generation networks requiring high bandwidth and robust data integrity.

- Requirement for Category 7 cabling solutions is further fueled by their ability to future-proof data center infrastructure against evolving technological needs.

- As businesses prioritize efficient data transmission, the adoption of Category 7 solutions across various industries continues to rise significantly, driving the data center structured cabling market demand.

By End-User Industry:

Based on the end-user industry, the market is segmented into IT & telecom, BFSI, healthcare, retail & e-commerce, manufacturing, government, and others.

The IT & telecom segment accounted for the largest revenue share in 2024.

- The IT & telecom sector requires robust cabling infrastructure to support seamless data transfer across large-scale networks.

- Rising demand for cloud services, video conferencing, and 5G deployment has significantly boosted the need for structured cabling solutions.

- Enterprises in this sector are investing heavily in hyperscale data centers, further driving the need for advanced cabling systems.

- The data center structured cabling market analysis shows that the dominance of this segment is attributed to its reliance on efficient data center operations to meet global connectivity demands.

The healthcare segment is anticipated to grow at the fastest CAGR during the forecast period.

- Healthcare facilities are increasingly adopting data centers to store and manage electronic health records and medical imaging data.

- Structured cabling solutions play a vital role in ensuring data security and seamless communication within healthcare networks.

- Advancements in telemedicine and IoT-enabled healthcare devices are driving the need for efficient data management systems.

- The data center structured cabling market trends depict that the segment’s rapid growth is supported by the integration of AI and big data analytics into healthcare operations, further enhancing cabling requirements.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

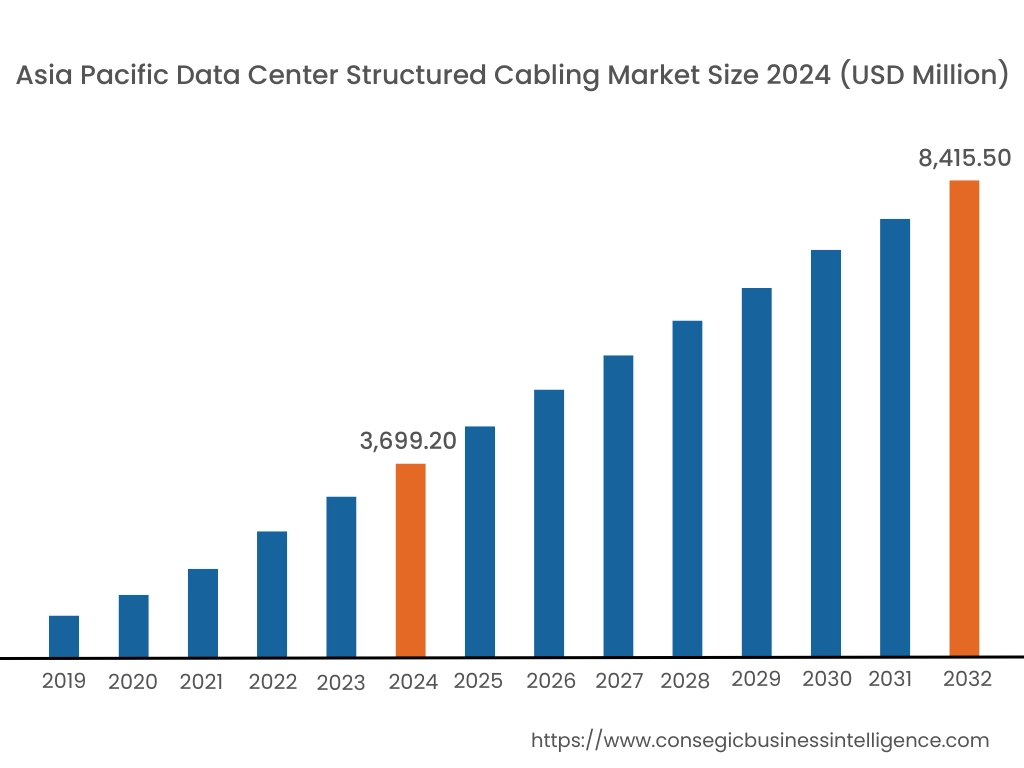

Asia Pacific region was valued at USD 3,699.20 Million in 2024. Moreover, it is projected to grow by USD 4,027.87 Million in 2025 and reach over USD 8,415.50 Million by 2032. Out of this, China accounted for the maximum revenue share of 34.3%. The Asia-Pacific region is witnessing rapid advancements in the data center structured cabling market, driven by industrial enlargement and technological progress in countries such as China, Japan, and India. The proliferation of digital services and the increasing demand for scalable IT infrastructure have intensified the adoption of structured cabling solutions. The analysis of market trends shows that the government initiatives promoting advanced infrastructure and digitization further influence data center structured cabling market growth.

North America is estimated to reach over USD 8,957.19 Million by 2032 from a value of USD 4,166.45 Million in 2024 and is projected to grow by USD 4,515.21 Million in 2025. This region commands a substantial share of the data center structured cabling market, propelled by the early adoption of advanced IT infrastructure and the presence of major technology enterprises. The United States, in particular, has integrated structured cabling solutions across sectors such as finance, healthcare, and retail. A notable trend is the shift towards modular data centers, which necessitates structured cabling systems that are easily integrated and scalable to meet evolving requirements. Analysis indicates that the continuous investment in research and development, along with the need for high-speed data transmission, reinforces the region's data center structured cabling market expansion.

Europe represents a significant segment of the global data center structured cabling market, with countries like Germany, France, and the United Kingdom leading in adoption and innovation. The region's emphasis on digital transformation and stringent data protection regulations has accelerated the deployment of structured cabling solutions to ensure compliance and operational efficiency. Analysis reveals a growing trend towards utilizing fiber optic cables over traditional copper cables due to their superior performance in terms of bandwidth, speed, and distance.

The Middle East & Africa region is gradually embracing data center structured cabling technologies, particularly within the telecommunications and financial sectors. Nations like the United Arab Emirates are investing in innovative IT solutions to enhance service delivery and comply with international standards. Analysis suggests an emerging trend towards adopting structured cabling systems to improve data management efficiency and support digital transformation initiatives.

Latin America is an emerging market for data center structured cabling, with countries such as Brazil and Mexico contributing to its development. The region's focus on modernizing IT infrastructure and improving business agility has spurred interest in structured cabling solutions. As per the market trends, government policies aimed at enhancing technological capabilities influence data center structured cabling market opportunities.

Top Key Players and Market Share Insights:

The Data Center Structured Cabling market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Data Center Structured Cabling market. Key players in the Data Center Structured Cabling industry include -

- CommScope (USA)

- Panduit (USA)

- Furukawa Electric Co., Ltd. (Japan)

- R&M (Reichle & De-Massari AG) (Switzerland)

- Siemon (USA)

- Corning Inc. (USA)

- Legrand (France)

- Nexans (France)

- Schneider Electric (France)

- Belden Inc. (USA)

Recent Industry Developments :

Product Launches:

- In January 2024, CommScope introduced SYSTIMAX 2.0, an enhanced structured cabling portfolio designed for agile, reliable, and future-ready network infrastructure. Key innovations include the GigaSPEED XL5 for multigigabit Ethernet and the VisiPORT for real-time port monitoring. The SYSTIMAX Assurance program now offers 24/7 premium support, backed by a 25-year warranty. This next-gen solution integrates fiber, copper, and edge architectures, emphasizing performance, intelligence, and global support to meet evolving connectivity needs in data centers, buildings, and campuses.

Data Center Structured Cabling Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 27,637.12 Million |

| CAGR (2025-2032) | 10.4% |

| By Component |

|

| By Wire Category |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Data Center Structured Cabling Market? +

The Data Center Structured Cabling Market size is estimated to reach over USD 27,637.12 Million by 2032 from a value of USD 12,560.58 Million in 2024 and is projected to grow by USD 13,638.05 Million in 2025, growing at a CAGR of 10.4% from 2025 to 2032.

What are the key segments in the Data Center Structured Cabling Market? +

The market is segmented by component (hardware, software, professional services), wire category (Category 5E, Category 6, Category 6A, Category 7, others), end-user industry (IT & telecom, BFSI, healthcare, retail & e-commerce, manufacturing, government, others), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which segment is expected to grow the fastest in the Data Center Structured Cabling Market? +

The Category 7 segment is expected to grow at the fastest CAGR during the forecast period. This growth is driven by its enhanced shielding capabilities, making it suitable for next-generation networks requiring high bandwidth and robust data integrity.

Who are the major players in the Data Center Structured Cabling Market? +

Major players in the market include CommScope (USA), Panduit (USA), Corning Inc. (USA), Legrand (France), Nexans (France), Schneider Electric (France), Belden Inc. (USA), Furukawa Electric Co., Ltd. (Japan), R&M (Reichle & De-Massari AG) (Switzerland), and Siemon (USA).