- Summary

- Table Of Content

- Methodology

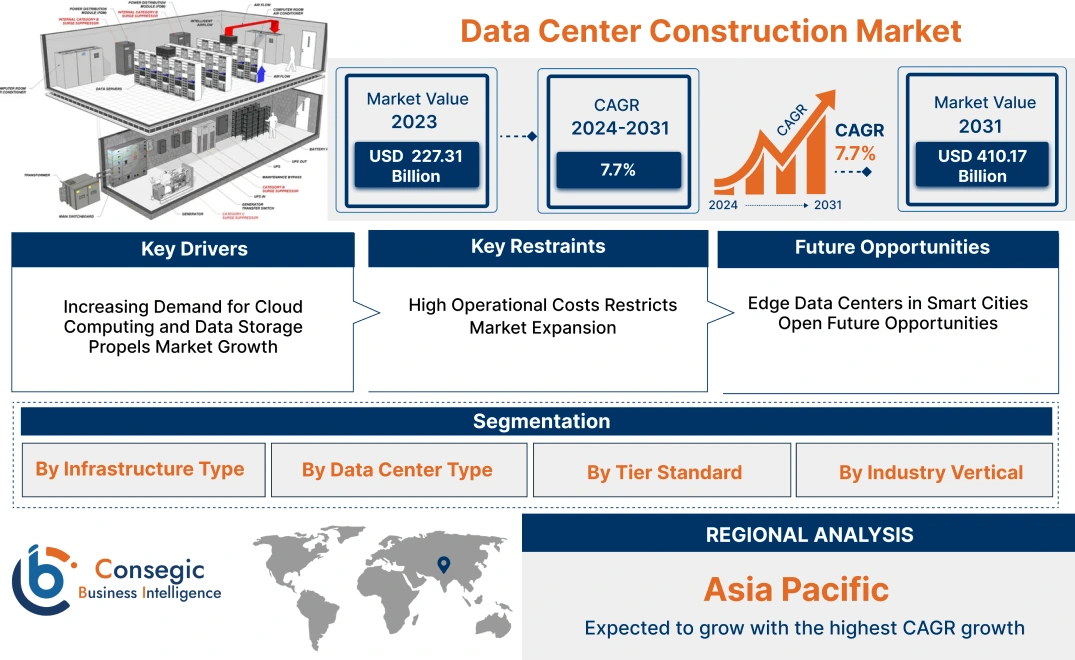

Data Center Construction Market Size:

Data Center Construction Market size is estimated to reach over USD 410.17 Billion by 2031 from a value of USD 227.31 Billion in 2023 and is projected to grow by USD 240.67 Billion in 2024, growing at a CAGR of 7.7% from 2024 to 2031.

Data Center Construction Market Scope & Overview:

The process of building and designing specialized facilities, which can include the IT infrastructure such as servers, storage, and network systems of an enterprise, is termed data center construction. The functions range from management, storage, and processing of massive amounts of data, to ensuring operational efficiency. The advantages include data management improvement, better security, and scalability. The key users include IT service providers, enterprises, government agencies, and telecom companies.

Data Center Construction Market Insights:

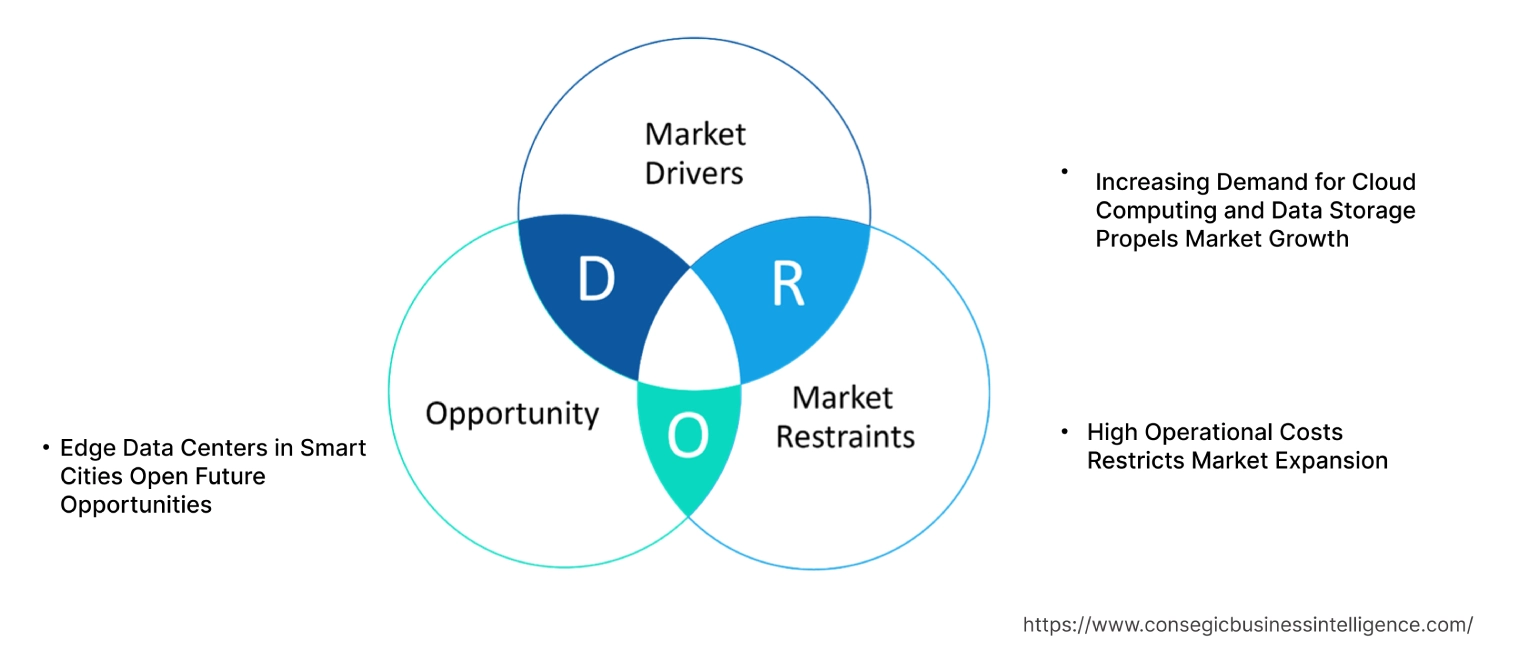

Data Center Construction Market Dynamics - (DRO) :

Key Drivers:

Increasing Demand for Cloud Computing and Data Storage Propels Market Growth

The growing urbanization and digitalization are leading to the increasing adoption of cloud computing and data storage. In order to ensure efficiency and scalability businesses are shifting towards cloud technology, which leads to the surge in requirement for data centers, as they provide secure and scalable environments, in order to process and store data.

Additionally, in order to meet the demands of industries like e-commerce, finance, and healthcare, companies are significantly investing in data centers.

- In July 2022, an $8bn investment to build data centers was announced by Blackstone and QTS. This is to meet the growing artificial intelligence needs and the resulting growing need for land for construction.

Therefore, the scalability and efficiency requirements across organizations drive the data center construction market growth.

Key Restraints :

High Operational Costs Restricts Market Expansion

The operations, including energy consumption, cooling systems, and maintenance and construction of data centers require a hefty investment. The costs can be extremely high for small businesses, considering the expensive resources, making it unaffordable. Moreover, in order to maintain operational reliability, along with energy efficiency and cooling capacity adds to the costs.

- According to the 2023 report by Uptime Institute, the rise in supply chain issues, and increase in labor and energy prices are contributing to the increase in construction and operational costs. Additionally, components including generator and UPS systems add to the cost.

Therefore, the cost-heavy investments in data center operations restrain the data center construction market demand.

Future Opportunities :

Edge Data Centers in Smart Cities Open Future Opportunities

The growing requirement for real-time data processing and the rising move towards smart cities, necessitates the computational power closer to the users, which can be achieved with edge data centers. They ensure the reduction of latency, enhanced performance, and localization of data, in order to ensure the seamless performance of time-sensitive applications, which includes IoT devices.

- For instance, Lenovo collaborated with the city of Barcelona, utilizing the Lenovo Edge Computing Technology, in order to build a smart city infrastructure . This ensures advances in technology including smart glasses, ensuring a seamless shopping experience and enhanced technology for the visually impaired. This can be ensured with the help of Lenovo's powerful servers that enable real-time data processing.

Therefore, the market trends analysis shows that the continuous shift towards smart cities and localized data processing drives data center construction market opportunities.

Data Center Construction Market Segmental Analysis :

By Infrastructure Type:

Based on infrastructure type, the market is segmented into electrical infrastructure (Power Distribution Units (PDUs), Uninterruptible Power Supply (UPS) Systems, Generators, Switchgear, Others), and mechanical infrastructure (Cooling Systems, Racks, HVAC Systems, Others).

Trends in the Infrastructure Type:

- Innovations in general construction, particularly building design and site development, are focused on modular and prefabricated solutions, which have benefits such as reduced construction time and costs, also improved scalability for data centers.

- Structural support advancements, such as earthquake-resistant building technologies and enhanced load-bearing frameworks, make sure that data centers can be built in diverse geographical locations, even in areas prone to natural disasters.

Electrical Infrastructure accounted for the largest revenue share in 2023

- Electrical infrastructure includes Power Distribution Units (PDUs), Uninterruptible Power Supply (UPS) systems, generators, and switchgear, which are important for maintaining power availability in data centers.

- These systems are responsible for uninterrupted operations, making them important in environments where power reliability is vital, such as banking, healthcare, and cloud services.

- The growth of the hybrid IT environment is increasing the requirement for advanced UPS systems and PDUs, which are essential for optimizing power usage and reducing operational costs.

- Power infrastructure enhancements like advanced PDUs with intelligent monitoring capabilities offer greater control of the overall system which also aligns with energy-efficient operations in large data centers.

- In 2022, the core EcoStruxure™ Power platform updates were released by Schneider Electric, in order to enhance the energy and operational efficiency. The updates include EcoStruxure Panel Server connectivity to EcoStruxure Asset Advisor & Resource Advisor, EcoStruxure Extended Reality Operator Advisor, EcoStruxure™ Cybersecurity, and ETAP Operator Training Software (OTS).

- In conclusion, the segmental trends analysis depicts that the essential role of electrical infrastructure in ensuring power continuity and advancements in energy-efficient technologies solidifies the data center construction market growth.

Mechanical Infrastructure is anticipated to register the fastest CAGR during the forecast period.

- Mechanical infrastructure includes systems such as cooling, HVAC, and racks, which are vital for maintaining optimal temperatures inside the data centers which is needed for preventing overheating of sensitive equipment.

- Cooling systems, particularly liquid cooling and free cooling technologies are gaining popularity due to their energy efficiency and effectiveness in high-density data centers.

- The increasing use of AI and machine learning applications is the driving factor for higher power density which has downsides such as requiring more advanced cooling systems to prevent hardware degradation.

- The shift toward edge computing and hyperscale data centers makes the need for more sophisticated cooling infrastructure much higher, especially in regions with hot climates or where energy costs are high.

- In 2023, the collaboration for Intel® Gaudi®3 AI Accelerator Platform was announced between Vertiv and Intel. The integration of Vertiv™ liquid-cooled data center infrastructure solutions and Intel's next-generation AI accelerators enables the growing adoption of AI.

- In conclusion, the rapid advancements in cooling technologies and the rise of high-density computing environments contribute to the data center construction market opportunities.

By Data Center Type:

Based on data center type, the market is segmented into enterprise, hyperscale, colocation, and edge data centers.

Trends in the Data Center Type:

- Innovations in enterprise data centers are focused on hybrid cloud strategies, which allow businesses to seamlessly integrate on-premises infrastructure with cloud services, enabling them to improve their flexibility and reduce operational costs.

- Colocation data centers are adopting renewable energy solutions, such as on-site solar and wind power, to reduce their carbon footprint and meet the growing requirement for sustainable data center operations.

Hyperscale Data Centers accounted for the largest revenue share of the total data center construction market share in 2023.

- Hyperscale data centers are large-scale facilities designed to support cloud computing, big data processing, and large-scale storage applications. These centers can house thousands of servers and are primarily used by major technology companies.

- They are special because of their ability to efficiently manage high workloads, along with scalable infrastructures that allow rapid expansion without compromising performance.

- The growing requirement for cloud services, data analytics, and AI-driven applications has led to substantial investments in hyperscale data centers, especially in regions like North America and Asia-Pacific.

- Hyperscale data centers offer the advantage of cost savings through economies of scale, making them attractive for businesses looking to scale their operations without making significant capital investments.

- In January 2022, Equinix, Inc., and GIC entered into a US$525 million joint venture partnership. This ensures the expansion towards more than US$8 billion across 36 facilities for the global xScale data center portfolio.

- In conclusion, the growing need for cloud computing and AI applications, combined with the scalability of hyperscale data centers, ensures their dominance in the market.

Edge Data Centers are anticipated to register the fastest CAGR during the forecast period.

- Edge data centers are smaller facilities located closer to the end users to minimize latency and improve the performance of critical applications. They are becoming increasingly important for industries requiring real-time data processing, such as IoT and autonomous vehicles.

- These data centers focus on the latency issues associated with centralized cloud data centers, enabling faster data delivery and improving user experience in bandwidth-intensive applications like video streaming and gaming.

- The rise of 5G networks is accelerating the requirement for edge data centers, as they provide the necessary infrastructure to support the low-latency, high-speed requirements of 5G applications.

- Edge data centers are also important for sectors like manufacturing and healthcare, where real-time data analysis is essential for optimizing processes and improving patient care.

- In July 2022, an Edge platform was launched by Lumen in Europe. In order to support data-intensive applications, it offers ultra-low latency connectivity at the cloud edge.

- In conclusion, the increase of 5G technology and the increasing need for real-time data processing are driving the data center construction market trends.

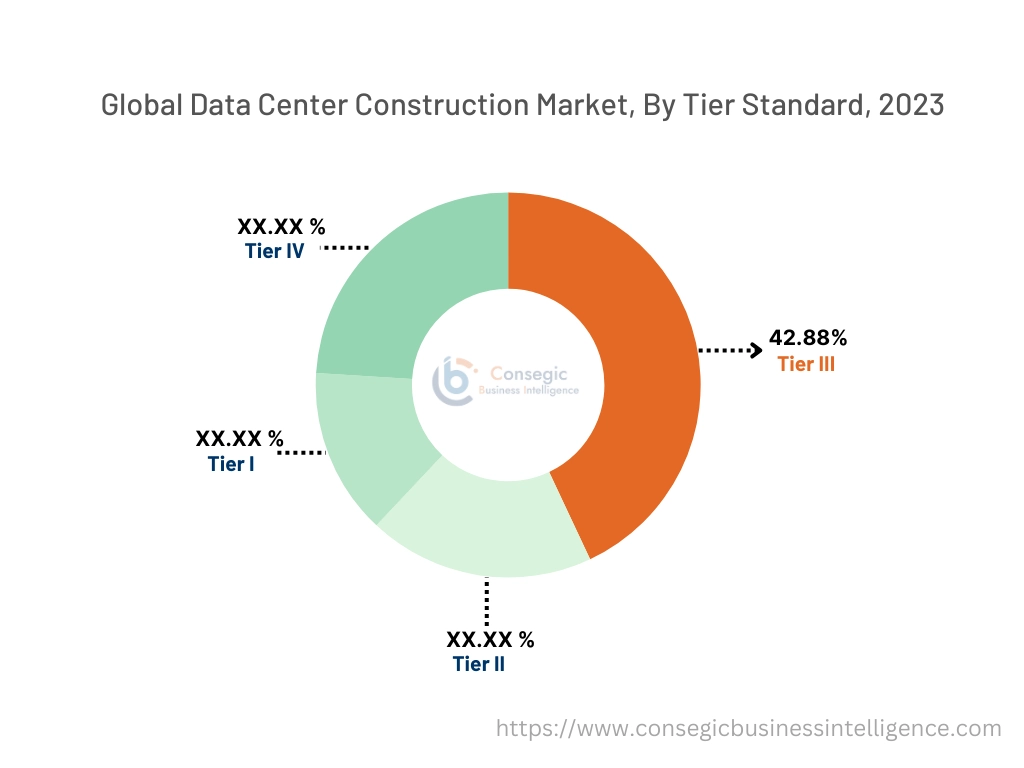

By Tier Standard:

Based on the tier standard, the market is segmented into Tier I, Tier II, Tier III, and Tier IV.

Trends in the Tier Standard:

- Tier I innovations focus more on modular data center designs that allow smaller companies to scale their operations while maintaining cost-effectiveness, making these centers more accessible to growing businesses.

- Tier II innovations include improved cooling and power management solutions, ensuring enhanced operational efficiency without compromising reliability, making them attractive for mid-sized enterprises.

The tier III segment accounted for the largest revenue of 42.88% of the overall data center construction market share in 2023.

- Tier III data centers offer redundancy for critical components like power and cooling systems, ensuring higher reliability and uptime than Tier I and II data centers.

- They are designed to support 99.982% availability, making them ideal for enterprises that require a balance between cost-effectiveness and operational reliability.

- The rising adoption of cloud computing and digital transformation initiatives across industries has increased demand for Tier III data centers, particularly for applications where downtime can have significant financial or operational repercussions.

- Tier III facilities are also preferred by financial institutions, healthcare providers, and government agencies, where high availability is critical for maintaining operations.

- In February 2021, a new purpose-built Tier III facility was opened by China Mobile International Limited in Frankfurt, Germany. It ensures seamless connectivity which is high-speed and enhancement in security, featuring dual power supply from two different stations.

- In conclusion, the balance between cost and operational reliability makes Tier III data centers the most widely adopted standard in the market.

The tier IV segment is anticipated to register the fastest CAGR during the forecast period.

- Tier IV data centers offer the highest level of reliability, with full fault tolerance and the ability to maintain operations even during maintenance or failure events.

- These centers guarantee 99.995% availability, making them essential for industries where even minimal downtime is unacceptable, such as banking, telecommunications, and critical infrastructure.

- As cybersecurity threats continue to grow, Tier IV data centers are becoming increasingly important for sectors handling sensitive data, ensuring continuous operations and data security.

- The higher operational costs associated with Tier IV facilities can be justified with the ability to prevent downtime, which is invaluable for businesses requiring constant availability.

- In conclusion, the unmatched reliability and security of Tier IV data centers drive their rapid growth, especially in sectors where uptime is mission-critical.

By Industry Vertical:

Based on industry vertical, the market is segmented into IT & Telecom, BFSI, healthcare, government & defense, energy, retail, manufacturing, media & entertainment, and others.

Trends in the Industry Vertical:

- In the BFSI sector, advancements in blockchain and fintech applications are driving needs for secure, high-performance data centers that can handle complex transactions and store sensitive financial data.

- The energy sector is adopting AI-driven predictive analytics to optimize energy production and distribution, leading to increased demand for data centers capable of processing large amounts of data in real-time.

The IT & Telecom sector accounted for the largest revenue share in 2023.

- The IT & telecom sector relies heavily on data centers for supporting cloud services, communication networks, and data storage, making it the largest consumer of data center colocation services.

- The rapid expansion of 5G networks and the increasing requirement for high-speed internet have driven significant investments in IT infrastructure, particularly in regions like North America and Europe.

- The ongoing digital transformation across businesses has further fueled demand for colocation services in this sector, as companies seek scalable, reliable infrastructure to support their growing data needs.

- The IT & telecom sector is also seeing a rise in the need for edge computing solutions, where data processing occurs closer to the source, improving speed and reducing latency.

- In October 2023, Switch Datacenters and CoolIT Systems entered into a partnership in order to accelerate the shift towards sustainable data centers. This can be achieved with the integration of Switch's data center designs which are sustainable with CoolIT's Direct Liquid Cooling (DLC) and Rear Door Heat Exchangers (RDHx).

- In conclusion, the IT & telecom sector's reliance on data centers for cloud and 5G services ensures its continued dominance as the largest segment by revenue.

The healthcare sector is anticipated to register the fastest CAGR during the forecast period.

- The healthcare sector is increasingly adopting digital health solutions, such as telemedicine, electronic health records (EHRs), and AI-driven diagnostics, driving the need for reliable data center infrastructure.

- Data security and compliance with regulations like HIPAA in the U.S. and GDPR in Europe are critical, making colocation services attractive to healthcare providers who need secure, scalable data storage solutions.

- The COVID-19 pandemic accelerated the adoption of digital healthcare technologies, leading to increased investments in IT infrastructure to support telehealth and remote patient monitoring services.

- The rising use of big data and AI in medical research and diagnostics further drives the requirement for data center colocation services, as healthcare providers need powerful computing infrastructure to process large volumes of data.

- In conclusion, the healthcare sector's rapid digital transformation and the growing need for secure, scalable infrastructure contribute to data center construction market trends.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

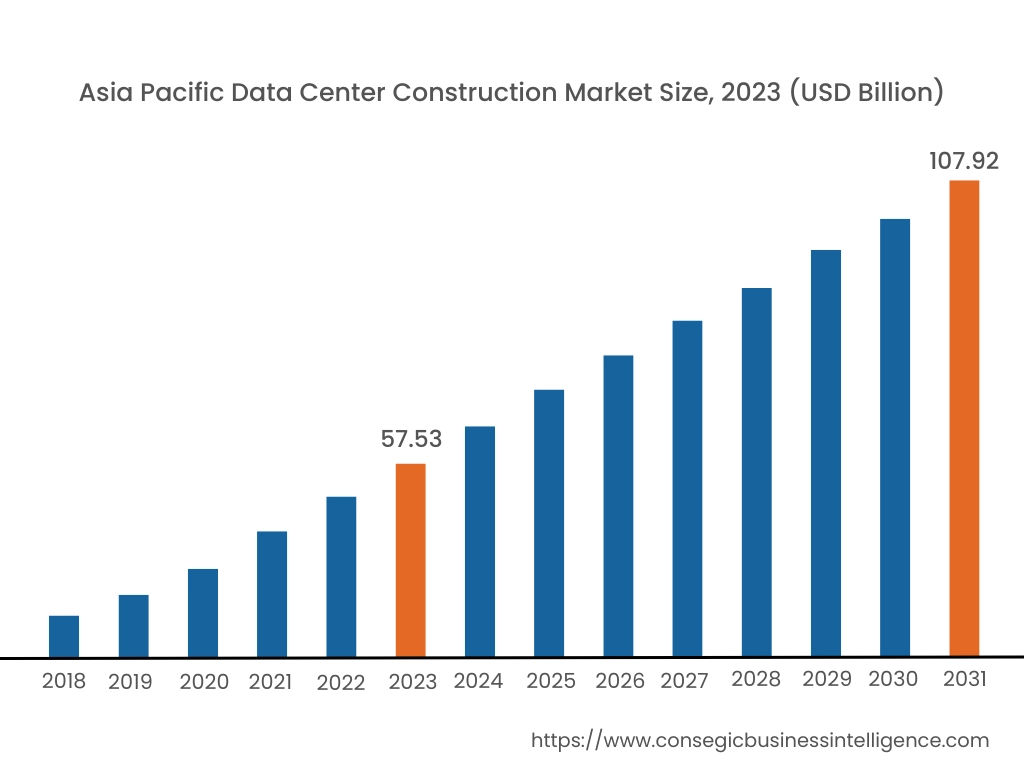

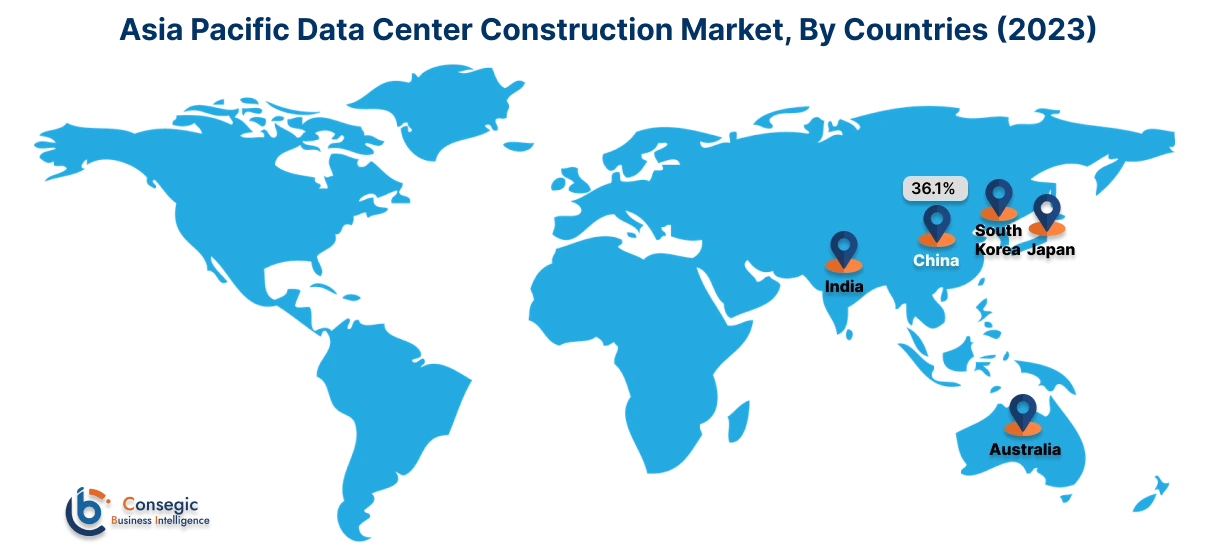

Asia Pacific region was valued at USD 57.53 Billion in 2023. Moreover, it is projected to grow by USD 61.12 Billion in 2024 and reach over USD 107.92 Billion by 2031. Out of this, China accounted for the maximum revenue share of 36.1%. The data center construction market analysis depicts that due to rapid digitalization and the shift toward the Internet, especially across countries like China and India. The smart city initiatives and the advancements in e-commerce and streaming services are contributing to the adoption of data centers. The increasing focus on the 5G network and the Internet of Things is also accelerating the data center construction market expansion.

- In February 2023, the construction of a data center in the Guian New Area in Southwest China's Guizhou province was announced by a Chinese company NetEase Inc. It will include 10,000 standard racks and 100,000 servers, with a total size of 7.3 hectares.

North America is estimated to reach over USD 138.27 Billion by 2031 from a value of USD 76.00 Billion in 2023 and is projected to grow by USD 80.52 Billion in 2024. The growth is majorly driven by the advancements in cloud services and hyperscale data centers. To support the growing requirements for cloud services, the investments in data centers have become significant in this region, by companies like Amazon Web Services (AWS), Microsoft, and Google. The need for high-performance data centers is also growing in sectors like healthcare and finance, with the integration of Artificial Intelligence and machine learning.

- In October 2023, Texas and Idaho data center constructions were resumed by Meta. This utilizes new designs, which can support the next-generation AI systems, taking up to half the construction time and 31% cheaper.

The growing focus on energy-efficient data centers is driving the data center construction market demand in Europe. The government initiatives aiming to accelerate sustainable practices and energy sources are some of the contributing factors. The data center construction market analysis portrays that in the Middle East and Africa, digitalization and the goal of achieving technologically advanced cities drive market growth. The hefty investments towards constructing these data centers are a few of the contributing factors. The regional analysis of Latin America shows that the increasing adoption of cloud computing and big data analytics is the primary driving factor. The advancements in technology and the shift towards data sovereignty are the contributing factors to the data center construction market expansion in the region.

Top Key Players & Market Share Insights:

The data center construction market is highly competitive with major players providing data center construction services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the data center construction market. Key players in the data center construction industry include-

- Turner Construction Company (USA)

- AECOM (USA)

- Schneider Electric (France)

- Huawei Technologies Co., Ltd. (China)

- Fujitsu (Japan)

- DPR Construction (USA)

- Holder Construction Group, LLC (USA)

- Jacobs (USA)

- ISG (UK)

- Legrand SA (France)

Recent Industry Developments :

Product Launches:

- In July 2024, key data infrastructure projects were launched by the Saudi Data and AI Authority (SDAIA), including the advanced data centers in Riyadh. The operational efficiency of these centers is significantly enhanced with an electricity capacity of up to 65 kilowatts per cabin.

- In March 2024, a new modular data center offering was launched by Eaton. They are available in 13 standard configurations, which are shipped pre-built, along with in-row cooling units that are pre-installed.

- In January 2024, the MAA10 data center was launched in Chennai, India by Digital Realty. It is a highly connected infrastructure that can support up to 100 megawatts of IT load capacity which is critical.

Mergers & Acquisitions:

- In June 2024, 8,590 acres in Reno, Nevada were acquired by Tract for data center park development. The land includes a range of pre-approved uses including data centers and energy production for commercial usage.

Partnerships & Collaborations:

- In May 2024, Aston and JLL entered into a partnership, in order to launch grid-independent campuses offerings to the data centers located in the US. JLL will be responsible for site selection management for the Rapid Development Program (RDP) for clean data centers, and Aston will right-size its infrastructure investments to tenants, utilizing JLL's microgrid expertise.

- In March 2024, a $800m Dallas deal was made by Mitsubishi Corporation for its first US data center investment in the US. It is a joint venture between Mitsubishi Corporation and Digital Realty, with Mitsubishi holding a 65 percent equity interest and Digital Realty will retain a 35 percent stake.

Data Center Construction Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 410.17 Billion |

| CAGR (2024-2031) | 7.7% |

| By Infrastructure Type |

|

| By Data Center Type |

|

| By Tier Standard |

|

| By Industry Vertical |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Data Center Construction Market? +

Data Center Construction Market size is estimated to reach over USD 410.17 Billion by 2031 from a value of USD 227.31 Billion in 2023 and is projected to grow by USD 240.67 Billion in 2024, growing at a CAGR of 7.7% from 2024 to 2031.

What specific segmentation details are covered in the data center construction market report? +

The data center construction market report includes specific segmentation details for infrastructure type, data center type, tier standard, industry vertical, and region.

Which is the fastest segment anticipated to impact the market growth? +

In the industry vertical segment, the healthcare sector is the fastest-growing segment during the forecast period due to its advancement in technology and the requirement to optimize patient data.

Who are the major players in the data center construction market? +

The key participants in the data center construction market are Turner Construction Company (USA), AECOM (USA), DPR Construction (USA), Schneider Electric (France), Huawei Technologies Co., Ltd. (China), Fujitsu (Japan), Holder Construction Group, LLC (USA), Jacobs (USA), ISG (UK), and Legrand SA (France).