- Summary

- Table Of Content

- Methodology

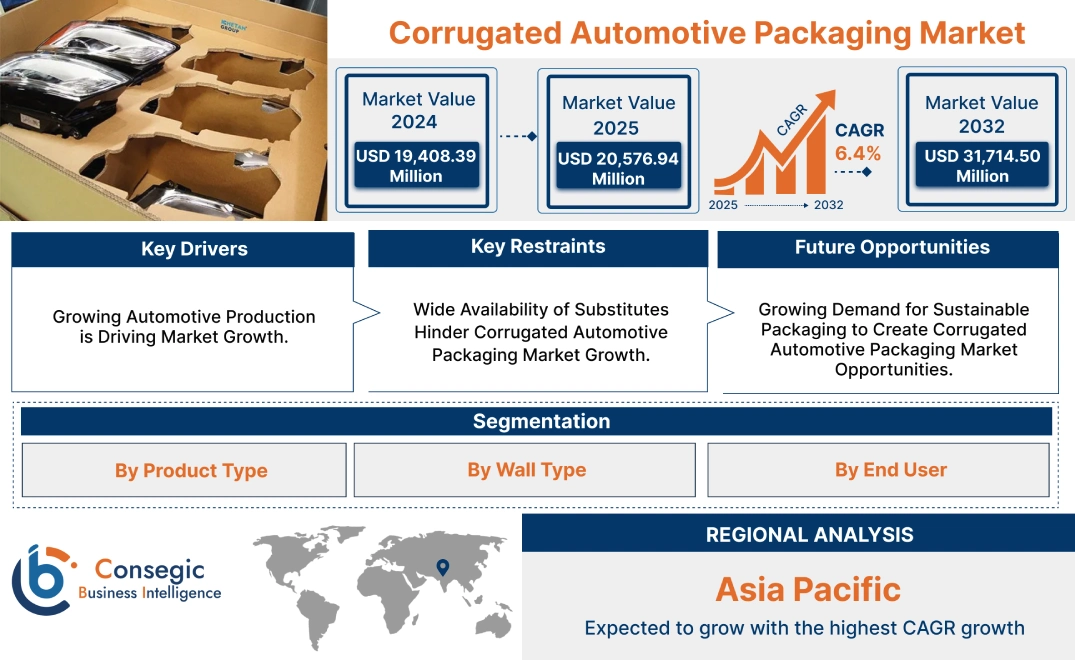

Corrugated Automotive Packaging Market Size:

The Corrugated Automotive Packaging Market size is growing with a CAGR of 6.4% during the forecast period (2025-2032), and the market is projected to be valued at USD 31,714.50 Million by 2032 from USD 19,408.39 Million in 2024. Additionally, the market value for 2025 is attributed to USD 20,576.94 Million.

Corrugated Automotive Packaging Market Scope & Overview:

Corrugated automotive packaging utilizes corrugated cardboard to create protective solutions for the automotive industry. They are widely used for transporting and storing products. They also offer important protection against shocks and vibrations during transit. Its popularity in the automotive sector is due to the several advantages that it provides such as superior protection due to the fluted layer, easy customization to fit specific part shapes and sizes, cost-effectiveness and amongst others. The versatility of corrugated packaging allows its application to a broad range of automotive parts. These include both internal parts within facilities and externally as well for shipping purposes. A few of the common examples include boxes for spare parts, large containers for bulky components, pallet packaging for efficient transport, amongst others.

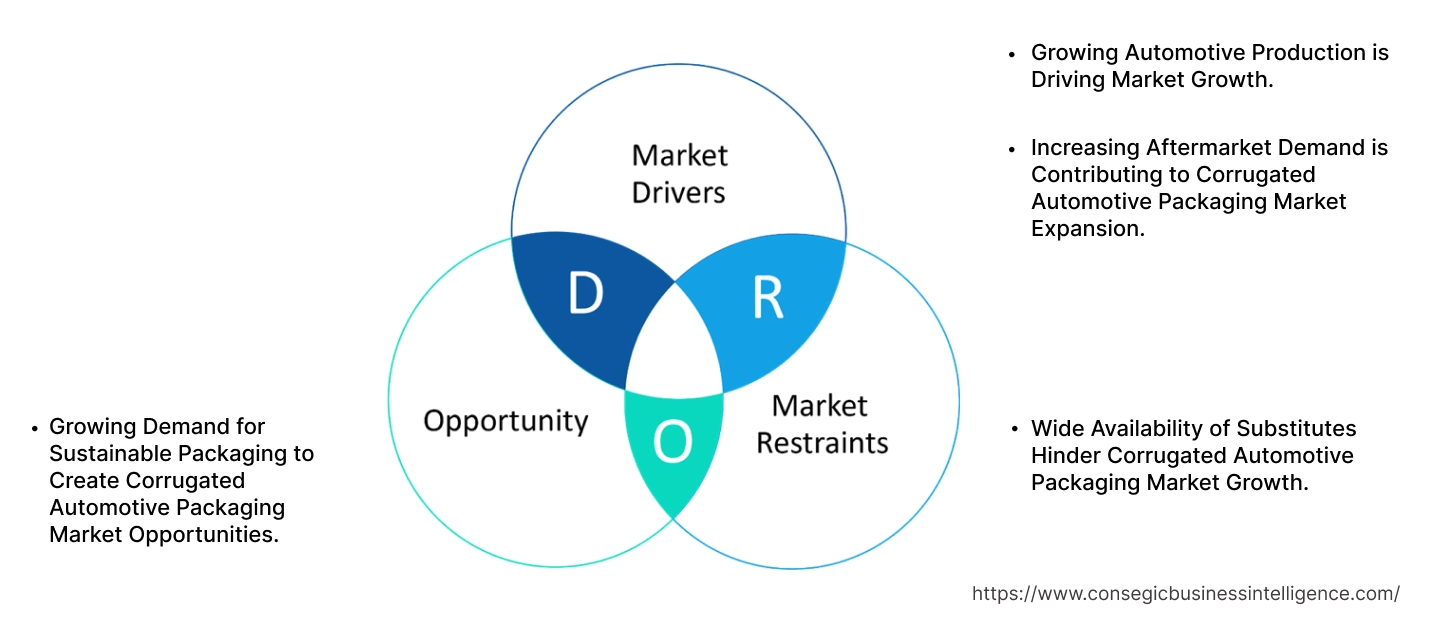

Corrugated Automotive Packaging Market Dynamics - (DRO) :

Key Drivers:

Growing Automotive Production is Driving Market Growth.

The direct correlation between vehicle manufacturing and the demand for component parts requires protective packaging solutions for everything from small to large components. This has led to an increase in production translating directly into a higher volume of parts. These parts require packaging for transport to assembly plants and aftermarket suppliers.

- For instance, according to Global Times, the total automotive production in China attributed to 31.28 million units, experiencing 3.7% increases from 2023.

Furthermore, the complex nature of modern automotive supply chains highlights the critical role of corrugated packaging in protecting these components. Thus, due to the above-mentioned factors, the market is growing.

Increasing Aftermarket Demand is Contributing to Corrugated Automotive Packaging Market Expansion.

As vehicles age and require maintenance or repairs, the need for replacement parts and accessories rises. Each of these parts typically requires packaging for safe and efficient transportation from manufacturers to repair shops and individual consumers. This requirement of replacement parts through the aftermarket creates demand for corrugated packaging.

- For instance, according to Times of India, the aftermarket in India experienced a high growth rate of roughly 25% in first and second quarter during 2021-2022 due to the improvement in performance of the automotive sector.

Furthermore, the diverse nature of aftermarket parts requires a range of corrugated packaging solutions. These factors combined are driving the corrugated automotive packaging market expansion in the aftermarket.

Key Restraints:

Wide Availability of Substitutes Hinder Corrugated Automotive Packaging Market Growth.

Wide availability of options such as plastics, wood, metal, and even textiles offer alternative solutions for packaging automotive parts. These substitutes are preferred in certain situations due to specific properties they possess. A few of these properties are such as increased durability for heavy or sharp items, better moisture resistance, amongst others. The diverse requirements for the automotive sector, including a wide range of part sizes, weights, amongst others, have led to an increase in preference for these substitute materials. These alternatives compete with corrugated packaging, thus hindering its market development. This competition has made corrugated packaging manufacturers develop new and innovative offerings which require large financial investment as well as adherence to stringent regulations. Hence, the aforementioned factors are restraining Corrugated Automotive Packaging market demand.

Future Opportunities :

Growing Demand for Sustainable Packaging to Create Corrugated Automotive Packaging Market Opportunities.

Consumers, businesses, and regulatory bodies are all focusing on environmentally friendly practices, including the packaging sector considered as one of the most important ones. Corrugated cardboard is one such product that aligns with this trend. It offers recyclability and often recycled content. The growing requirement for sustainable packaging solutions presents a distinct advantage for corrugated packaging manufacturers.

- For instance, in 2023, according to Stora Enso, it is estimated that the consumer demand for sustainable packaging across the globe is increasing, expected to reach 11 million tones over the forecast period

Automotive companies are aiming towards reducing their environmental footprint and meeting sustainability goals. They are trying to find new possibilities for eco-friendly packaging options. This creates a substantial opportunity for corrugated packaging providers in turn catering to the sustainability needs of the automotive sector and driving market development.

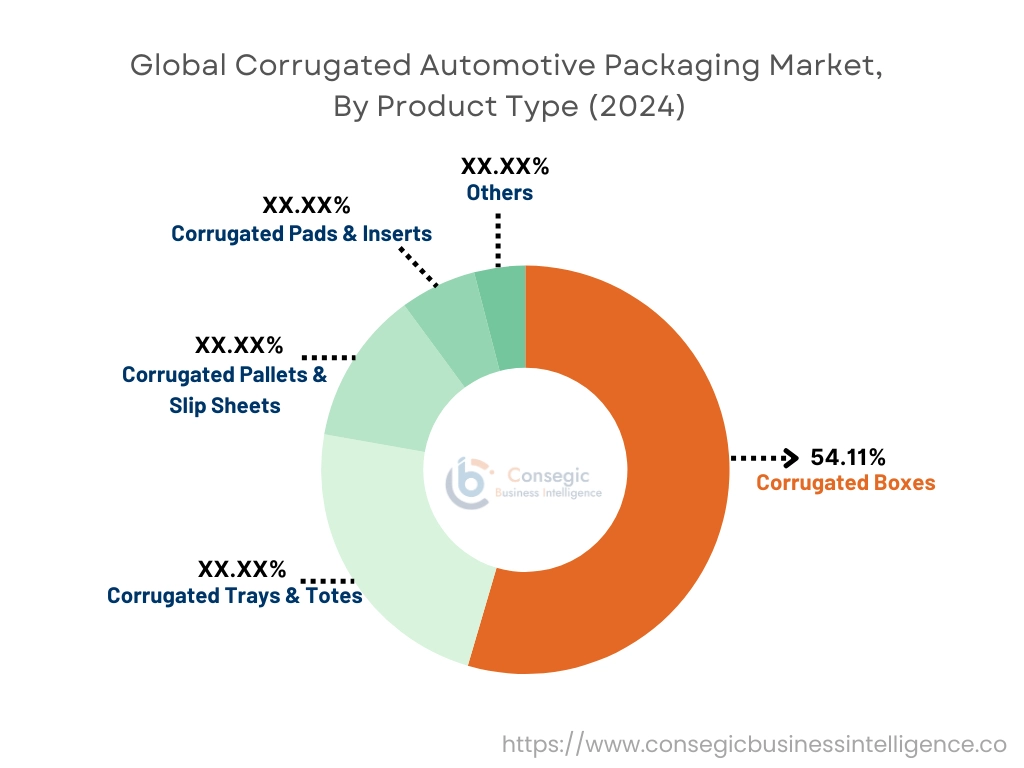

Corrugated Automotive Packaging Market Segmental Analysis :

By Product Type:

Based on product type, the market is categorized into corrugated boxes, corrugated trays & totes, corrugated pallets & slip sheets, corrugated pads & inserts, and others.

Trends in Product Type:

- The increase in the adoption of corrugated boxes for specific parts includes features like easy opening, secure locking, amongst others.

- The rise in preference for corrugated trays & totes for in-plant logistics and material handling.

The Corrugated Boxes segment accounted for the largest Corrugated Automotive Packaging market share of 54.11% in 2024.

- Corrugated boxes offer a versatile, cost-effective, and readily customizable solution for a vast range of automotive parts. It provides solutions from small components to larger components

- Their wide usage in both OEM (Original Equipment Manufacturing) and aftermarket applications solidifies their position as the largest segment within the market.

- They are widely used for logistics and transportation for overseas markets as well.

- For instance, in 2024, BMW developed PAL973 in collaboration with Project Oversea-Box. PAL973 is a single use corrugated box that is utilized to cater the shipping purposes overseas.

- As a result, based on the Corrugated Automotive Packaging market analysis, the corrugated boxes segment dominates the Corrugated Automotive Packaging market demand.

The Corrugated Trays & Totes segment is expected to be the fastest growing segment over the forecast period.

- The increasing focus on in-plant efficiency along with the rise of automation and robotics in manufacturing are contributing to the segmental development.

- These drive the requirement for standardized and durable containers like corrugated trays and totes. These trays and totes integrate seamlessly with these advanced systems.

- Furthermore, the automotive sector's focus towards sustainability has contributed to the need for reusable packaging solutions including corrugated trays and totes.

- Their customizability for specific parts and alignment with lean manufacturing principles further contributes to the expansion of this segment.

- Therefore, based on the corrugated automotive packaging market analysis and trends, the corrugated trays & totes segment is expected to be lucrative over the forecast period.

By Wall type:

The wall type segment is categorized into single-wall corrugated, double-wall corrugated, and triple-wall corrugated

Trends in Wall type:

- The incorporation of single-wall corrugated used for lighter and less fragile parts is growing

- The consumer preference towards double-wall corrugated due to better protection and affordability features.

The single-wall corrugated segments accounted for the largest corrugated automotive packaging market share in 2024.

- Single-wall corrugated offers features such as cost-effectiveness and suitability for a large volume of parts.

- Additionally, the increasing requirement for packaging solutions within the rapidly expanding electric vehicle (EV) sector is contributing to the development of the segment.

- EV parts, such as wiring harnesses, sensors, and smaller electronic components, are protected by single-wall corrugated boxes.

- For instance, in 2023, according to IBEF, the sale of electric vehicles attributed to 88,619 units, experiencing a growth rate of approximately 28% from 2021

- Thus, as per the market analysis, due to the above-mentioned factors, the single-wall corrugated segment dominates the corrugated automotive Packaging market trends.

The double-wall corrugated segment is expected to be the fastest growing segment over the forecast period.

- Double-wall corrugated segment offers enhanced protection during transit when compared with the single-wall.

- It provides a balance between cost and performance which makes it an attractive option for a wide range of parts as well as for varied types of manufacturers.

- Additionally, the continued development of automotive aftermarket further fuels requirement for durable packaging solutions like double-wall corrugated, particularly for individual part shipments.

- Its adaptability with respect to varying sizes, weights, and fragility levels in terms of handling it is further contributing to the segment development.

- Therefore, as per analysis and trends, the double-wall corrugated segment for corrugated automotive packaging is expected to be lucrative over the forecast period.

By End User:

The End User segment is categorized into OEM and Aftermarket.

Trends in the End User:

- The requirement for OEMs is increasing as they automate their manufacturing processes utilizing robotic handling systems.

- The rise in the adoption of corrugated packaging in the aftermarket as customers need parts quickly.

The OEM segments accounted for the largest market share in 2024.

- OEMs (Original Equipment Manufacturers) produce components in large volumes that translate directly to a substantial requirement for corrugated packaging.

- This large volume of parts required by OEMs makes them a significant consumer of corrugated packaging.

- Their need for consistent, reliable, and customized packaging solutions further contributes to their dominance in this market segment.

- For instance, Maruti Suzuki, an OEM sold 165,483 units of cars in India for the FY 2022. It has a market share of roughly 42% of the passenger vehicle segment

- Thus, as per the market analysis, due to the above-mentioned factors, the OEM segment is dominating the Corrugated Automotive Packaging market trends.

The aftermarket segment is expected to be the fastest growing segment over the forecast period.

- The high growth in e-commerce for auto parts requires protective packaging for individual shipments, with corrugated cardboard being a preferred choice in the aftermarket.

- A growing number of older vehicles increases the requirement for replacement parts, which in turn drives the need for packaging.

- The rise of DIY repairs and independent repair shops further contributes to this trend.

- The aftermarket's characteristic variety and high volume of parts create consistent requirements for corrugated packaging.

- Additionally, the cost-effectiveness of corrugated cardboard makes it ideal for aftermarket players.

- Therefore, as per analysis, the aftermarket segment for corrugated automotive packaging is expected to be lucrative over the forecast period.

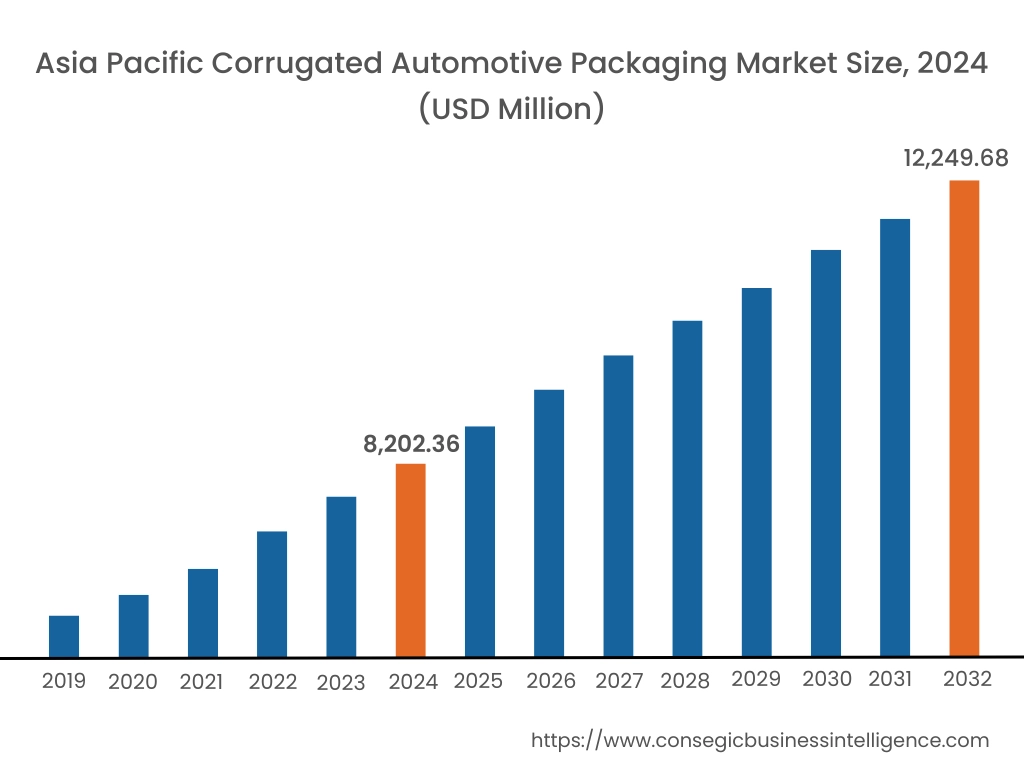

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

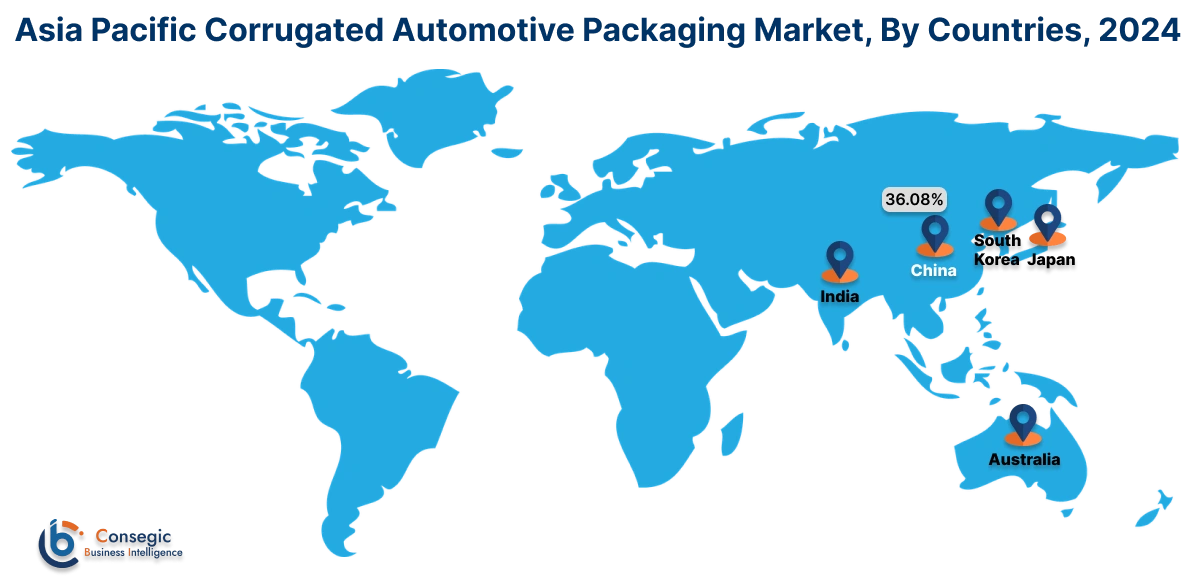

In 2024, Asia Pacific accounted for the highest market share of 42.27% and was valued at USD 8,202.36 Million and is expected to reach USD 12,249.68 Million in 2032. In Asia Pacific, China accounted for the market share of 36.08% during the base year of 2024.

The vehicle manufacturing across the region, particularly in countries such as China, Japan, South Korea, and India are increasing, in turn increasing the requirement for protective packaging solutions. These create a lot of requirements for corrugated packaging with these key manufacturing countries becoming major consumers. This development strengthens the automotive parts supply chain and presents significant potential for corrugated packaging players.

- For instance, according to Just Auto, in 2023, the Asia Pacific region produced 51.6 million units, showcasing roughly 10% increase on a yearly basis. China and Japan were the primary contributors for the production purposes.

Thus, due to the aforementioned factors, the requirement for corrugated packaging in automotive industry is surging in the Asia Pacific Region

In Europe, the Corrugated Automotive Packaging industry is experiencing the fastest growth with a CAGR of 8.7% over the forecast period. The European market is experiencing a significant increase in the requirement for sustainable solutions due to the stringent EU regulations promoting waste reduction and recycling amongst others. These drivers are motivating corrugated packaging players to innovate by incorporating recycled content, optimizing packaging design for lightweighting, ensuring easy recyclability, amongst others. These factors combined are the primary drivers towards European corrugated automotive packaging market growth

In the North American market, there is a growing requirement for aftermarket products as the average age of vehicles are increasing. In addition to this, the need for replacement parts and service cost are increasing in turn contributing to the need for cost-effective packaging solutions including corrugated packaging. Moreover, sustainability trends are contributing further to the adoption of environmentally friendly material. This leads to the wide adoption of corrugated packaging as it offers an environmentally friendly alternative. Thus, these above-mentioned factors combined contribute to the market development of corrugated automotive packaging in North America

The Latin American market is experiencing a focus towards advanced corrugated materials. This is supported by the region’s growing automotive sector. This has led to a need for enhanced protection of parts during transport. Additionally, the need for lighter packaging to reduce costs and fuel consumption, along with the requirement for customized solutions for diverse automotive parts, is contributing to the market development. Moreover, material innovation, advanced manufacturing techniques, amongst other advancements are creating potential in the region's automotive packaging sector.

The Middle East and African corrugated automotive packaging market is focusing on catering to the dynamic nature of automotive parts. Each automotive part requires specialized packaging for optimal protection. Manufacturers are also trying to find new ways to differentiate their brands through unique packaging, while customized solutions contribute to supply chain efficiency. Furthermore, players are offering a wide array of customization options, from varied box styles, sizes, and fluting configurations to high-quality printing and labeling for branding. Special features like inserts and partitions, along with a selection of materials to meet performance are contributing to the enhancement of the customization possibilities in turn creating corrugated automotive packaging market opportunities.

Top Key Players and Market Share Insights:

The Global Corrugated Automotive Packaging Market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D) and product innovation to hold a strong position in the global Corrugated Automotive Packaging market. Key players in the Corrugated Automotive Packaging industry include-

- International Paper Company (U.S.)

- WestRock Company (U.S.)

- Sonoco Products Company (U.S.)

- Mondi Group Plc (UK)

- Sealed Air Corporation (U.S.)

- Greif Inc. (U.S.)

- DS Smith Plc (UK)

- Smurfit Kappa Group Plc (Ireland)

- Nefab Group (Sweden)

- Elsons International (U.S.)

Corrugated Automotive Packaging Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 31,714.50 Million |

| CAGR (2025-2032) | 6.4% |

| By Product Type |

|

| By Wall Type |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Corrugated Automotive Packaging market? +

In 2024, the Corrugated Automotive Packaging market is USD 19,408.39 Million.

Which is the fastest-growing region in the Corrugated Automotive Packaging market? +

Europe is the fastest-growing region in the Corrugated Automotive Packaging market.

What specific segmentation details are covered in the Corrugated Automotive Packaging market? +

By Product Type, Wall Type and End User segmentation details are covered in the Corrugated Automotive Packaging market.

Who are the major players in the Corrugated Automotive Packaging market? +

International Paper Company (U.S.), WestRock Company (U.S.), Greif Inc. (U.S.), DS Smith Plc (UK), Smurfit Kappa Group Plc (Ireland), Nefab Group (Sweden) are some of the major players in the market.