- Summary

- Table Of Content

- Methodology

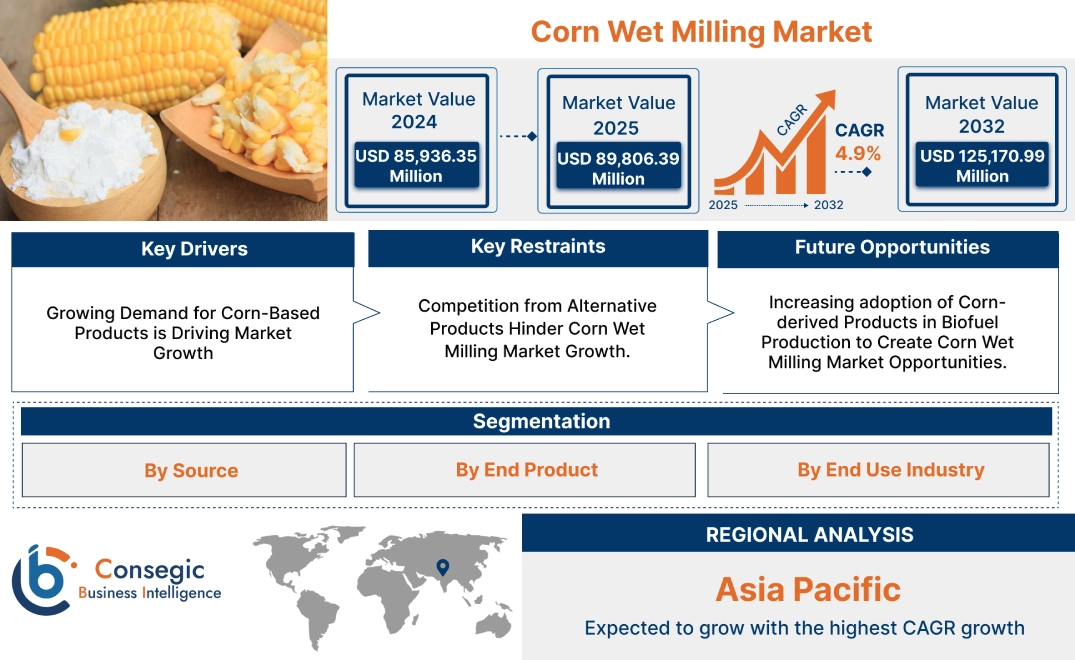

Corn Wet Milling Market Size:

The Corn Wet Milling Market size is growing with a CAGR of 4.9% during the forecast period (2025-2032), and the market is projected to be valued at USD 125,170.99 Million by 2032 from USD 85,936.35 Million in 2024. Additionally, the market value for 2025 is attributed to USD 89,806.39 Million.

Corn Wet Milling Market Scope & Overview:

Corn wet milling is a process that converts corn kernels into end products such as starch, germ, fiber, amongst others. This involves soaking the corn in warm water with sulfur dioxide to soften the kernels. The softened kernels are then processed through a series of steps. These steps include grinding, washing, and centrifuging, to separate the different parts. The resulting products have diverse applications across various industries. The end product starch is widely used in food, paper, and textiles. Gluten used in animal feed and other end products for a wide range of end use industries. This efficient process ensures the full utilization of the corn kernel, yielding valuable end products for a wide range of industries.

Corn Wet Milling Market Dynamics - (DRO) :

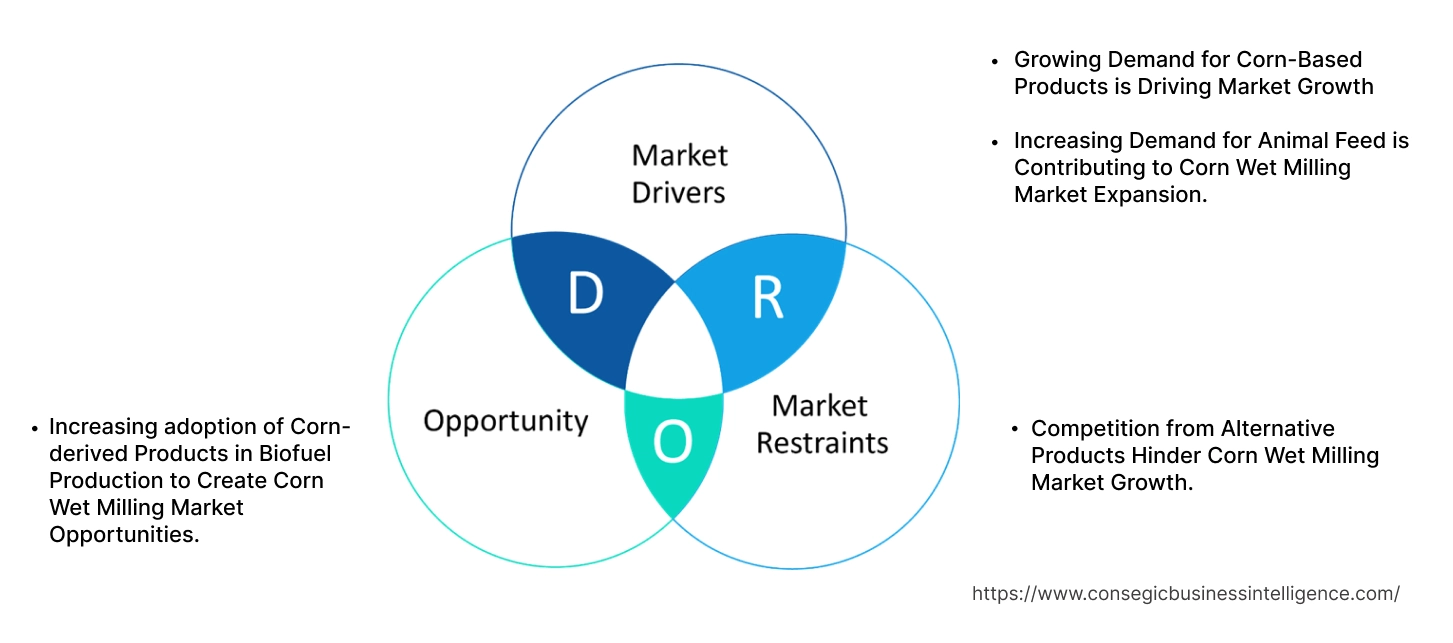

Key Drivers:

Growing Demand for Corn-Based Products is Driving Market Growth

The adaptability of corn-derived products makes them essential for several key industries. A few of these corn-derived products are starch, sweeteners, ethanol, animal feed components, amongst others. Rise in the food and beverage sector, expanding livestock sector are a few of the key factors that contribute to this requirement.

- For instance, according to NCBI, in U.S., around 10% of the corn that is harvested undergoes wet milling process to produce end products such as starch and sweeteners along with other additional end products as well in 2022.

Thus, due to the above-mentioned factors, market requirement for corn-based products through wet milling is increasing.

Increasing Demand for Animal Feed is Contributing to Corn Wet Milling Market Expansion.

Corn is one of the key ingredients for animal nutrition. The wet milling process of corn yields several important byproducts that are essential components of livestock diets. These byproducts include protein-rich corn gluten meal, high-fiber corn gluten feed, amongst others. They provide necessary nutrients for various animal species, from poultry and swine to cattle and aquatic creatures. This requirement for corn-based animal feed is directly linked to the development of the global livestock sector.

- For instance, according to IFIF, the feed demand for poultry increased from 140.8 Million MT to 142.7 Million MT in 2023 across the globe. This shows an increase of roughly 1.3% from 2022 to 2023.

Thus, as per the market analysis, the increasing requirement for animal feed contributes to the increase in requirement for end products produced from corn through wet milling process, in turn driving corn wet milling market expansion.

Key Restraints:

Competition from Alternative Products Hinder Corn Wet Milling Market Growth.

There is wide availability of alternatives to the end products derived from corn. In the sweetener market, high fructose corn syrup (HFCS) has alternate options such as traditional sugar (sucrose) along with the increasing popularity of natural sweeteners like stevia in the food and beverage sector hampers market. Similarly, corn starch, a primary product of wet milling, has alternative options such as starches extracted from other sources including tapioca, potato, wheat, and rice that offers similar properties and characteristics as of the corn starch. In addition to this, price sensitivity among consumers and the sector is further contributing to the hinderance in the market requirement. Hence, the aforementioned factors are restraining corn wet milling market growth.

Future Opportunities :

Increasing adoption of Corn-derived Products in Biofuel Production to Create Corn Wet Milling Market Opportunities.

Corn acts as a primary feedstock for ethanol production. The wet milling process provides necessary starch for fermentation and generating valuable byproducts like corn gluten feed and DDGS. They enhance the sustainability and efficiency of ethanol production. Government mandates initiatives such as renewable fuel standards and tax benefits along with growing awareness of renewable energy. This in turn is leading to an increase in the requirement for biofuels.

- For instance, according to GTBharat, India is expected to increase its corn production to around 650 tons by 2030 with a major focus on their utilization for biofuel production

This increased utilization of corn in biofuel production directly benefits the corn wet milling market.

Corn Wet Milling Market Segmental Analysis :

By Source:

Based on Source, the market is categorized into dent and waxy.

Trends in Source:

- The utilization of dent corn due to its high starch content and availability are contributing to its popularity.

- The requirement for waxy corn-derived starches due to the growing popularity of processed foods is increasing.

The dent segment accounted for the largest corn wet milling market share in 2024 and is expected to be the fastest growing segment over the forecast period.

- Dent corn's offers high starch content. This makes it a cost-effective source for a wide array of corn-derived products. Its flexibility allows for the production of starch, sweeteners, ethanol, amongst others that are catering to diverse industry needs.

- The global availability of dent corn along with established processing infrastructure further contributes to market development.

- For instance, according to Iowa Grown, dent corn attributes to roughly 99% of the corn that is planted in Iowa, United States.

- Continuous improvements in dent corn varieties and processing technologies further enhance their yields contributing to the development of the market.

- As per the analysis, based on the above-mentioned factors, the dent segment is dominating the corn wet milling market demand as well as expected to grow as the fastest CAGR over the forecast period.

By End Product:

The end product segment is categorized into starch, sweeteners, ethanol, corn gluten meal, and others

Trends in the End Product:

- Modified starches with tailor-specific properties catering to specific food and industrial needs are gaining popularity.

- The increase in government initiatives towards usage of biofuel is creating an increase in requirement for corn-based ethanol.

The starch segments accounted for the corn wet milling market share in 2024.

- Corn starch acts as an ingredient across a diverse range of sectors. One of the key sectors is food and beverages.

- In addition to the food and beverage sector, corn starch acts as a thickener, stabilizer, and texturizer, to various industrial applications like paper, textiles, adhesives, and the emerging field of bioplastics.

- This broad applicability translates into consistently high requirement, establishing starch as the dominant end-product.

- For instance, in 2023, according to S. Grain Council, the increase in percentage of starch yield on a yearly basis leads to an increase in substantial revenue for corn wet milling plants situated across the globe

- Thus, as per the Corn Wet Milling market analysis, due to the above-mentioned factors, the starch segment is dominating the Corn Wet Milling market trends.

The ethanol segment is expected to be the fastest growing segment over the forecast period.

- This increase in the requirement for ethanol is directly proportional to the increase in global demand for biofuels. These are supported by government mandates in promoting renewable energy, amongst others.

- Corn serves as a primary feedstock for ethanol production, with the wet milling process playing an important role in enhancing the process's sustainability.

- Technological advancements aimed at improving ethanol production efficiency and developing advanced biofuels from diverse corn sources are further contributing to the corn wet milling market demand.

- In addition to this, the increase in the requirement for ethanol in turn is contributing to the market need for corn-derived ethanol.

- Therefore, as per analysis and trends, the ethanol segment is expected to be lucrative over the forecast period.

By End-Use Industry:

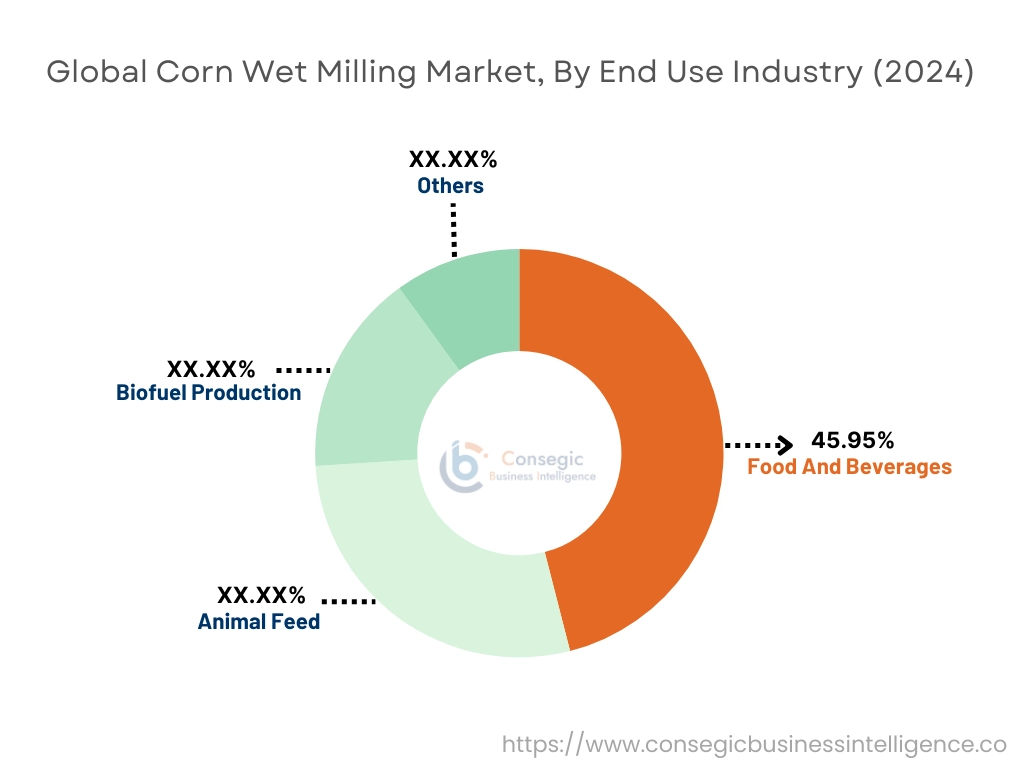

The End Use Industry segment is categorized into food and beverages, animal feed, biofuel production and others.

Trends in the End Use Industry:

- The increase in consumer preference towards clean label and natural ingredients.

- The focus on R&D related to advanced biofuels from corn sources to enhance sustainability.

The food and beverages segments accounted for the largest market share of 45.95% in 2024.

- Corn starch's functionalities such as a thickener, stabilizer, binder, and texturizer make it a preferable option in several types of food products.

- Furthermore, corn-derived sweeteners like HFCS, glucose, and dextrose are prevalent in beverages and processed foods.

- Additionally, the change in consumer preferences, including the growing emphasis on clean labels, health and wellness, and the increasing consumption of convenience foods are contributing to the requirement for corn-based products.

- For instance, in 2022, Cargill invested in a new plant in Indonesia. This plant is introduced specifically to cater to the requirements of starches and sweeteners for the increasing demand in the food sector in Asia.

- Thus, as per the corn wet milling market analysis, due to the above-mentioned factors and trends, the food and beverages segment is dominating the Corn Wet Milling market trends.

The biofuel production segment is expected to be the fastest growing segment over the forecast period.

- This increase in government initiatives such as renewable fuel standards that ensure a consistent market for ethanol are contributing to the development of biofuel production in turn driving the market requirement for corn-based ethanol.

- Technological advancements focused on improving ethanol production efficiency and developing advanced biofuels from corn sources further contributing to the market development.

- In addition to this, the focus of key players for investments in production facilities and distribution networks are catering to the rising requirement for corn-based products for biofuel production.

- Therefore, as per analysis and trends, the biofuel production segment is expected to be lucrative over the forecast period.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

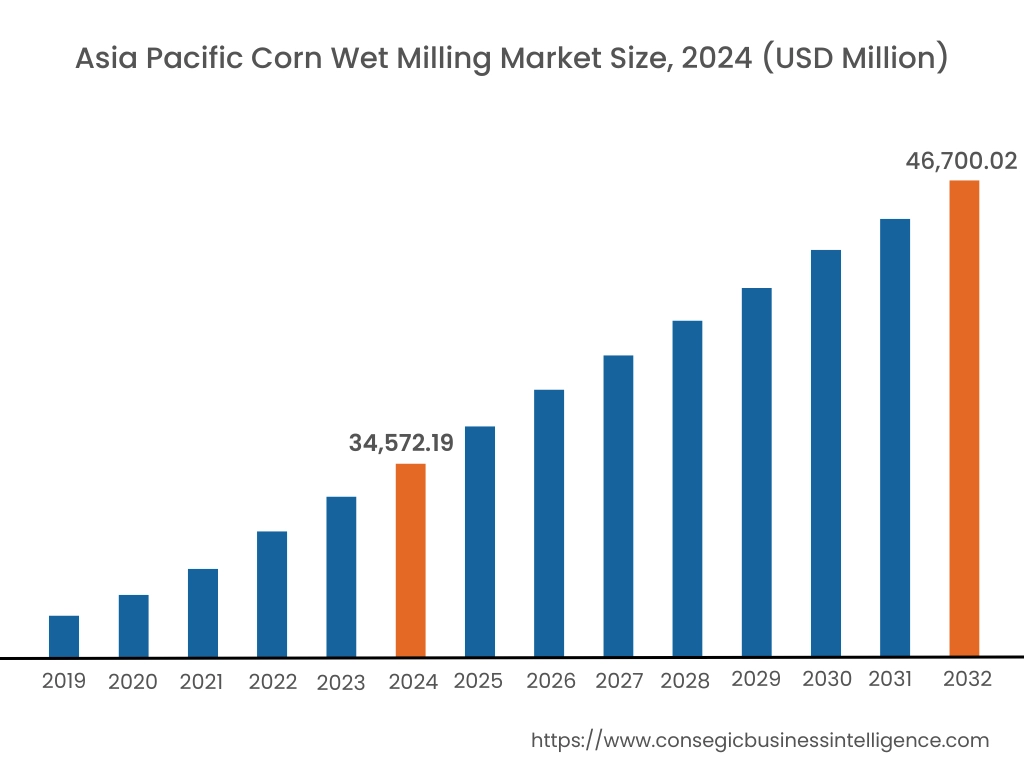

In 2024, Asia Pacific accounted for the highest market share at 40.23% and was valued at USD 34,572.19 Million and is expected to reach USD 46,700.02 Million in 2032. In Asia Pacific, China accounted for the market share of 35.11% during the base year of 2024.

The increase in population, particularly in countries such as China, India amongst others is leading to an increase in consumption of processed foods, beverages, and animal protein. This leads to a drive in the requirement for corn-derived ingredients. The region's food and beverage sector rely on corn starch, sweeteners, and additives. Simultaneously, the development of the livestock sector and rising meat consumption are increasing the need for corn-based animal feed for dairy feed, cattle feed amongst others.

- For instance, according to the Feed Additive, in 2023, there was an increase of 4.52% in the feed production for dairy in Asia Pacific region.

These factors create a strong trajectory for the Asia Pacific corn wet milling market, positioning it as a key region for players.

In North America, the Corn Wet Milling industry is experiencing the fastest growth with a CAGR of 6.9% over the forecast period. Biofuel production, particularly ethanol, plays an important part in the North American market. Ethanol, derived predominantly from corn, benefits significantly from the US Renewable Fuel Standard. These standard mandates biofuel blend into gasoline, creating a substantial and stable market. North America's abundant corn supply ensures a readily available and cost-effective feedstock for ethanol production. In addition to this, the well-established infrastructure and ongoing investments in research and development further contribute towards market growth in North America.

The European region focuses on high-quality animal products and efficient livestock farming sustains a requirement for specialized animal feed. Dairy farming also contributes substantially to the need for animal feed. European farmers prioritize animal health and productivity where corn-derived products like corn gluten meals and feed play are important. In addition to this, the aquaculture sector in Europe also utilizes corn-based feed ingredients at a smaller level when compared to the livestock sector. These factors collectively support the use of corn in animal feed, having a positive impact on the European corn milling market.

In the Latin American region, the growing population along with consumer preference towards evolving dietary habits that favor processed foods and beverages are having positive requirement for corn-derived ingredients. The growing food processing sector, with its investments in new facilities and technologies, further drives this requirement. The region's significant corn production, particularly in countries like Brazil and Argentina, provides a readily available feedstock, attracting corn wet milling companies. These combined factors create a favorable environment for the growth of the market within Latin America's dynamic food and beverage landscape.

Sustainable practices in the Middle East and Africa (MEA) market are still developing, though growing in importance. As the environmental regulations vary across MEA countries, a rising awareness of sustainability is gaining popularity. This presents opportunities for innovative and sustainable technologies, particularly in water management and waste reduction. Currently, some MEA corn wet milling companies are implementing water recycling systems and exploring energy efficiency measures. These include renewable energy sources as well. In addition to this, sustainable sourcing of corn is another emerging trend. As awareness grows, the adoption of these practices is expected to increase, creating lucrative corn wet milling market opportunities over the forecast period.

Top Key Players and Market Share Insights:

The Global Corn Wet Milling Market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D) and product innovation to hold a strong position in the global Corn Wet Milling market. Key players in the Corn Wet Milling industry include

- Tate & Lyle PLC (UK)

- Archer Daniels Midland Company (US)

- Bio-Chem Technology Group Company Limited (Hong Kong)

- Grain Processing Corporation (US)

- Bunge Limited (US)

- Cargill Incorporated (US)

- Ingredion Incorporated (US)

- Agrana Beteiligungs-AG (Austria)

- The Roquette Freres (France)

- China Agri-Industries Holding Limited (China)

Corn Wet Milling Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 125,170.99 Million |

| CAGR (2025-2032) | 4.9% |

| By Source |

|

| By End Product |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Corn Wet Milling market? +

In 2024, the Corn Wet Milling market is USD 85,936.35 Million.

Which is the fastest-growing region in the Corn Wet Milling market? +

North America is the fastest-growing region in the Corn Wet Milling market.

What specific segmentation details are covered in the Corn Wet Milling market? +

By Source, End Product, and End Use Industry segmentation details are covered in the Corn Wet Milling market.

Who are the major players in the Corn Wet Milling market? +

Tate & Lyle PLC (UK), Archer Daniels Midland Company (US), Cargill Incorporated (US) are some of the major players in the market.