- Summary

- Table Of Content

- Methodology

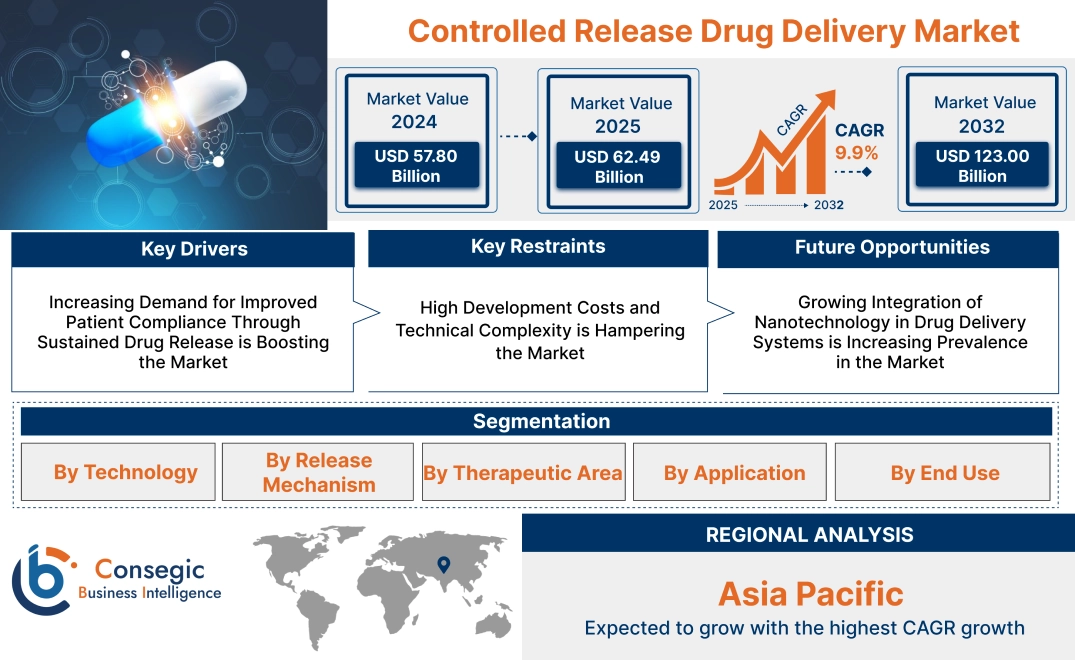

Controlled Release Drug Delivery Market Size:

Controlled Release Drug Delivery Market size is estimated to reach over USD 123.00 Billion by 2032 from a value of USD 57.80 Billion in 2024 and is projected to grow by USD 62.49 Billion in 2025, growing at a CAGR of 9.9% from 2025 to 2032.

Controlled Release Drug Delivery Market Scope & Overview:

The controlled release drug delivery are advanced systems that enable the gradual release of therapeutic agents over an extended period, optimizing efficacy and minimizing side effects. These systems include oral, injectable, transdermal, and implantable technologies, utilizing mechanisms such as diffusion, dissolution, and osmotic control to ensure precise drug delivery.

Key characteristics of controlled release drug delivery systems include improved patient compliance, reduced dosing frequency, and enhanced therapeutic outcomes. These technologies are widely used for chronic conditions like diabetes, cardiovascular diseases, cancer, and neurological disorders. The benefits include consistent drug plasma levels, reduced risk of toxicity, and better overall patient outcomes.

Applications span pharmaceuticals, biologics, and targeted therapies, addressing a wide range of therapeutic areas. End-users include pharmaceutical companies, hospitals, and research institutions, driven by increasing prevalence of chronic diseases, advancements in drug delivery technologies, and growing demand for patient-centric treatment solutions.

Controlled Release Drug Delivery Market Dynamics - (DRO) :

Key Drivers:

Increasing Demand for Improved Patient Compliance Through Sustained Drug Release is Boosting the Market

The controlled-release drug delivery market is being driven by the rising trends for drug delivery systems that enhance patient compliance. Traditional drug regimens often require frequent dosing, which can lead to non-adherence and suboptimal therapeutic outcomes. Controlled release systems, such as extended-release tablets, implants, and transdermal patches, offer consistent drug release over extended periods, reducing dosing frequency and improving adherence. This is particularly critical for managing chronic conditions such as diabetes, cardiovascular diseases, and neurological disorders, where long-term medication is necessary. Additionally, the ability of controlled release systems to minimize side effects by maintaining steady plasma drug levels makes them highly desirable, further fueling controlled release drug delivery market growth.

Key Restraints:

High Development Costs and Technical Complexity is Hampering the Market

Despite its benefits, the controlled release drug delivery market faces challenges due to the high costs and technical complexities associated with the development and manufacturing of these systems. Controlled release formulations often require advanced technologies, such as microencapsulation, nanoparticle engineering, and polymer-based matrices, which increase production expenses. Furthermore, these systems must undergo rigorous testing to ensure stability, safety, and efficacy, adhering to stringent regulatory standards. These factors not only escalate development timelines but also raise barriers for smaller pharmaceutical companies, limiting their ability to compete in the market. The high cost of controlled release products may also deter adoption in cost-sensitive regions, further restraining market growth.

Future Opportunities :

Growing Integration of Nanotechnology in Drug Delivery Systems is Increasing Prevalence in the Market

The integration of nanotechnology presents a significant opportunity for the market. Nanoparticle-based drug delivery systems enable precise targeting of diseased tissues, reducing systemic side effects and enhancing therapeutic efficacy. These systems are particularly beneficial in oncology, where targeted drug delivery to tumors minimizes harm to healthy cells. Additionally the analysis shows, advancements in nanotechnology are facilitating the development of multi-functional delivery systems, such as stimuli-responsive nanoparticles that release drugs in response to specific triggers like pH or temperature. The rising demand for personalized medicine further supports the adoption of nanotechnology in controlled release systems, as it allows for customized drug release profiles tailored to individual patient needs. Companies investing in nanotechnology-driven innovations are well-positioned to capitalize on this trend, expanding the scope of controlled release drug delivery applications.

These dynamics underscore the critical role of drug delivery systems in enhancing therapeutic outcomes and patient adherence. While challenges related to cost and complexity persist, ongoing innovations, particularly in nanotechnology, present significant opportunities for market expansion and diversification.

Controlled Release Drug Delivery Market Segmental Analysis :

By Technology:

Based on technology, the market is segmented into Wurster technique, matrix systems, transdermal systems, coacervation, osmotic delivery, and targeted delivery systems.

The targeted delivery systems segment accounted for the largest revenue in controlled release drug delivery market share in 2024.

- Targeted delivery systems enhance drug efficacy by directing medications precisely to the site of action, minimizing side effects.

- Increasing adoption in oncology and neurological disorders due to their ability to deliver high drug concentrations to specific cells or tissues is driving trends.

- Advancements in nanotechnology and antibody-drug conjugates are further propelling the adoption of targeted delivery systems.

- Rising investment in personalized medicine and precision therapeutics supports the dominance of this segment.

The transdermal systems segment is anticipated to register the fastest CAGR during the forecast period.

- Transdermal systems offer a non-invasive, controlled drug release mechanism, improving patient compliance.

- Increasing adoption in chronic conditions such as pain management and cardiovascular diseases is driving controlled release drug delivery market trends.

- Innovations in patch designs, including microneedle arrays and iontophoresis-enhanced delivery, are expanding their application scope.

- Rising preference for at-home treatments and easy-to-use solutions is expected to fuel growth in this segment.

By Release Mechanism:

Based on release mechanism, the market is segmented into diffusion-controlled, dissolution-controlled, osmotically controlled, chemically controlled, and biologically controlled systems.

The diffusion-controlled segment accounted for the largest revenue share in 2024.

- Diffusion-controlled systems ensure a steady drug release rate, making them ideal for chronic disease management.

- Their widespread application in oral and implantable drug delivery systems contributes significantly to market share.

- Advancements in polymer technologies enabling better control over drug diffusion rates are boosting adoption.

- Growing demand for reliable and cost-effective drug delivery solutions supports the dominance of this segment.

The osmotically controlled segment is anticipated to register the fastest CAGR during the forecast period.

- Osmotically controlled systems provide precise and predictable drug release over an extended period, enhancing therapeutic efficacy.

- Increasing adoption in oral formulations, particularly in diabetes and cardiovascular therapeutics, is driving advancement.

- Technological innovations enabling customizable release profiles are expanding the scope of osmotically controlled delivery systems.

- Rising focus on patient-centric drug delivery solutions is expected to propel controlled release drug delivery market growth in this segment.

By Therapeutic Area:

Based on therapeutic area, the market is segmented into cardiovascular diseases, neurological disorders, oncology, diabetes, respiratory diseases, and others.

The oncology segment accounted for the largest revenue share in 2024.

- Controlled release systems in oncology ensure sustained drug release, reducing toxicity and enhancing patient outcomes.

- Increasing prevalence of cancer globally has led to heightened trends for advanced delivery systems for chemotherapy drugs.

- Targeted delivery technologies, such as nanoparticles and liposomes, are widely used in cancer therapeutics, supporting controlled release drug delivery market trends.

- Rising research and development investments in cancer treatment are driving adoption of controlled release systems in oncology.

The diabetes segment is anticipated to register the fastest CAGR during the forecast period.

- Controlled-release systems for diabetes, such as extended-release insulin and GLP-1 receptor agonists, are gaining popularity for better glycemic control.

- Increasing adoption of drug-eluting devices and osmotic pumps in diabetes management is driving advancement.

- The rising prevalence of diabetes worldwide and the growing focus on improving patient adherence are propelling this segmental analysis.

- Ongoing advancements in drug formulations and delivery mechanisms tailored to diabetic patients are expected to boost market expansion.

By Application:

Based on application, the market is segmented into oral drug delivery (tablets and capsules), injectable drug delivery, drug-eluting stents, metered dose inhalers, transdermal and ocular patches, implantable drug delivery, and others.

The oral drug delivery segment accounted for the largest revenue in controlled release drug delivery market share in 2024.

- Oral drug delivery systems dominate the market due to their ease of administration and patient preference.

- Controlled release tablets and capsules are widely used in chronic disease management, ensuring steady therapeutic levels.

- Advancements in coating and encapsulation technologies for improved drug release profiles are supporting advancement.

- Increasing adoption of extended-release formulations for conditions such as hypertension, diabetes, and neurological disorders is boosting controlled-release drug delivery market opportunities.

The transdermal and ocular patches segment is anticipated to register the fastest CAGR during the forecast period.

- Transdermal and ocular patches offer non-invasive, controlled drug delivery, improving patient compliance and comfort.

- Growing application in chronic pain management, hormone replacement therapy, and ophthalmic conditions is driving growth.

- Technological innovations, such as sustained-release ocular patches and enhanced drug absorption in transdermal systems, are boosting controlled release drug delivery market demand.

- Rising preference for at-home treatments and patient-friendly drug delivery options is expected to propel this segment.

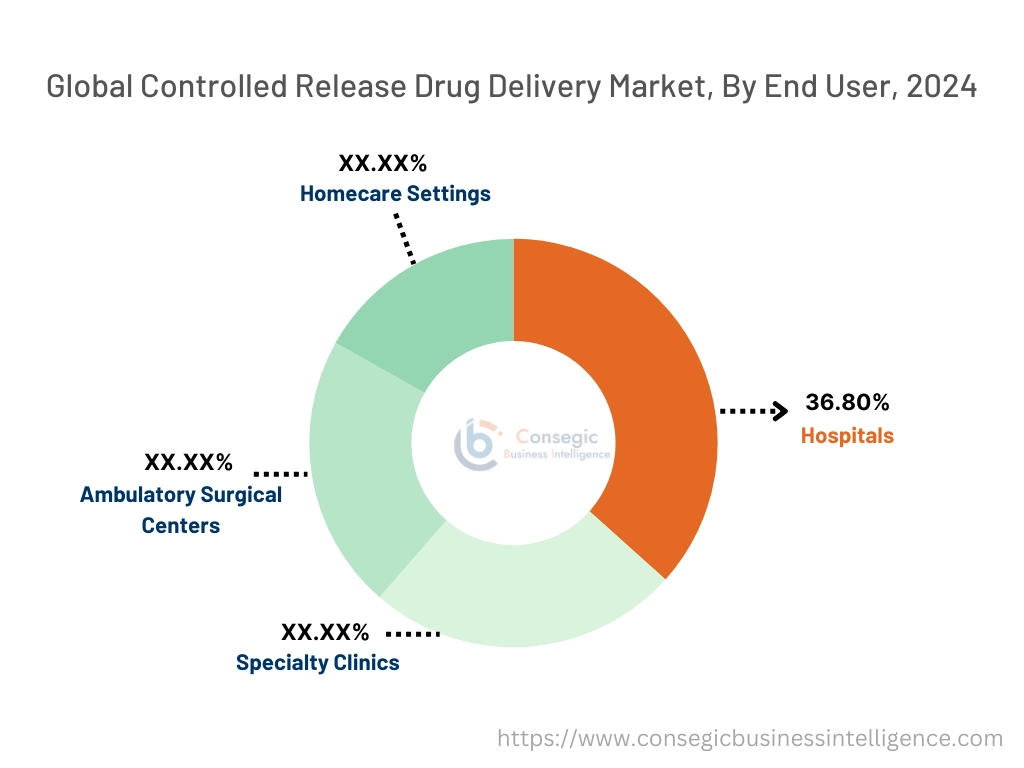

By End-User:

Based on end-use, the market is segmented into hospitals, specialty clinics, ambulatory surgical centers, and homecare settings.

The hospitals segment accounted for the largest revenue share of 36.80% in 2024.

- Hospitals remain the primary setting for administering controlled release drug delivery systems, particularly for complex and acute conditions.

- Availability of advanced equipment and expertise in hospitals ensures effective drug delivery management.

- Increasing hospital admissions for chronic diseases requiring controlled drug therapies is driving trends in this segment.

- Growing collaborations between hospitals and pharmaceutical companies to introduce innovative drug delivery solutions are further supporting growth.

The homecare settings segment is anticipated to register the fastest CAGR during the forecast period.

- Rising preference for self-administered and home-based therapies, such as transdermal patches and drug-eluting devices, is driving advancement in this segment.

- Increasing availability of user-friendly controlled release drug delivery systems for chronic disease management is boosting demand.

- Expanding telehealth infrastructure and remote patient monitoring are enhancing the adoption of homecare drug delivery solutions.

- Growing awareness about cost-effective and convenient treatment options in homecare settings is expected to propel controlled release drug delivery market opportunities.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

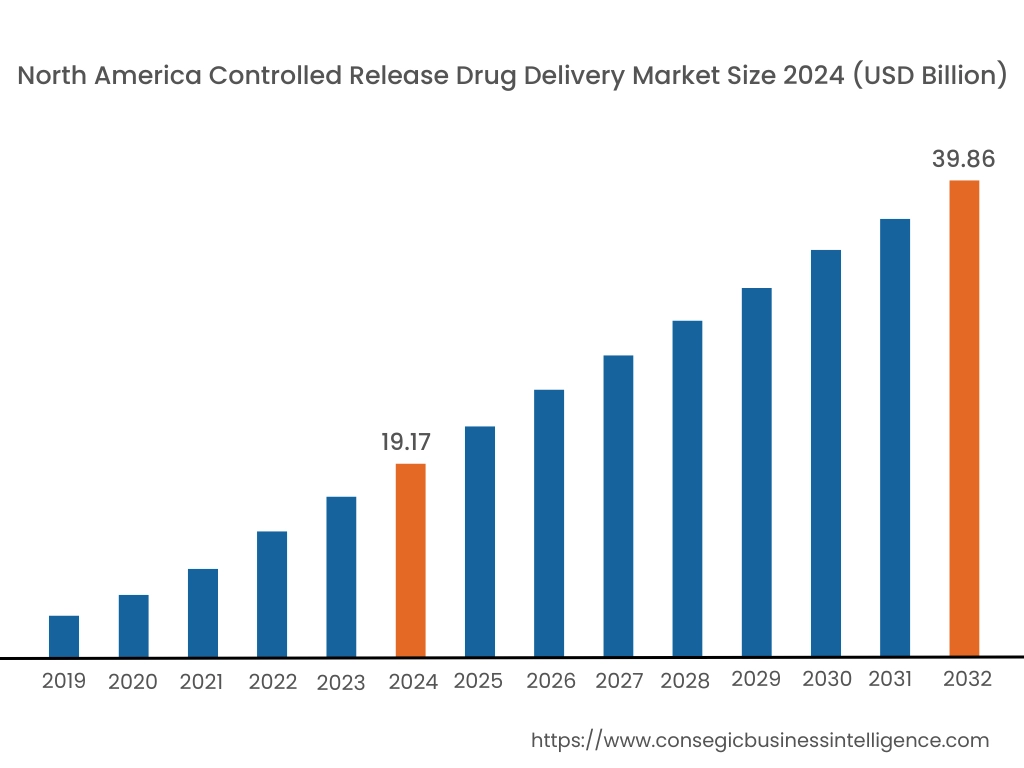

In 2024, North America was valued at USD 19.17 Billion and is expected to reach USD 39.86 Billion in 2032. In North America, the U.S. accounted for the highest share of 70.60% during the base year of 2024. North America holds a significant stake in the global controlled release drug delivery market, driven by the increasing prevalence of chronic diseases such as diabetes, cardiovascular disorders, and cancer, along with a strong focus on advanced drug delivery technologies. The U.S. dominates the region due to its robust pharmaceutical industry, high adoption of innovative controlled release systems, and significant investment in R&D for personalized medicine. As per the controlled release drug delivery market analysis, Canada contributes with rising trends for controlled release formulations to improve patient compliance and outcomes. However, the high cost of developing advanced drug delivery systems may pose challenges to widespread adoption.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 10.4% over the forecast period. The controlled release drug delivery market analysis shows, it is fueled by rapid urbanization, increasing prevalence of chronic diseases, and growing investments in healthcare infrastructure in China, India, and Japan. China dominates the market with rising trends for controlled-release formulations to address its growing diabetic and cardiovascular patient population. India’s expanding pharmaceutical manufacturing sector supports the development of cost-effective controlled-release drugs for domestic and international markets. Japan focuses on advanced drug delivery technologies for aging-related diseases, leveraging its strong pharmaceutical R&D capabilities. However, affordability and access to advanced healthcare facilities remain challenges in rural areas.

Europe is a prominent market for controlled release drug delivery, supported by an aging population, increasing prevalence of chronic diseases, and strong regulatory frameworks for innovative pharmaceutical products. Countries like Germany, France, and the UK are key contributors. In the regional analysis, Germany drives demand through its advanced healthcare infrastructure and focus on precision medicine, leveraging controlled-release formulations for chronic disease management. France emphasizes the use of sustained-release drug delivery systems in oncology and pain management. The UK focuses on expanding R&D activities and early adoption of cutting-edge drug delivery technologies. However, stringent regulatory requirements may increase time-to-market for new products in the region.

The Middle East & Africa region is witnessing steady growth in the controlled release drug delivery market, driven by increasing investments in healthcare infrastructure and the rising prevalence of chronic conditions such as diabetes and hypertension. Countries like Saudi Arabia and the UAE are adopting controlled-release formulations in hospitals and specialty clinics to improve patient compliance and outcomes. In Africa, South Africa is an emerging market, focusing on expanding access to affordable controlled-release drugs for chronic disease management. However, limited local manufacturing capabilities and reliance on imports may restrict broader controlled release drug delivery market expansion in the region.

Latin America is an emerging market, with Brazil and Mexico leading the region. Brazil’s growing healthcare sector and increasing focus on improving patient compliance drive controlled release drug delivery market demand for sustained and controlled release formulations for chronic diseases. Mexico emphasizes partnerships with pharmaceutical companies to introduce advanced drug delivery systems in public healthcare facilities. The region is also exploring opportunities in transdermal and implantable drug delivery systems. However, economic instability and inconsistent regulatory frameworks may pose challenges to market expansion in smaller economies.

Top Key Players and Market Share Insights:

The controlled release drug delivery market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the controlled release drug delivery market. Key players in the controlled release drug delivery industry include -

- Johnson & Johnson (United States)

- Merck & Co., Inc. (United States)

- Sanofi S.A. (France)

- Hoffmann-La Roche AG (Switzerland)

- AbbVie Inc. (United States)

- Bristol Myers Squibb (United States)

- Novartis AG (Switzerland)

- Pfizer Inc. (United States)

- GlaxoSmithKline plc (United Kingdom)

- AstraZeneca plc (United Kingdom)

Recent Industry Developments :

Patents:

- In September 2022, Laxxon Medical was granted U.S. Patent 11,419,824 B2 for their 3D screen-printed drug delivery system. This system enables the controlled administration of one or more active pharmaceutical ingredients (APIs) within oral dosage forms, allowing for customized release profiles tailored to patient needs.

Controlled Release Drug Delivery Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 123.00 Billion |

| CAGR (2025-2032) | 9.9% |

| By Technology |

|

| By Release Mechanism |

|

| By Therapeutic Area |

|

| By Application |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected size of the Controlled Release Drug Delivery Market by 2032? +

Controlled Release Drug Delivery Market size is estimated to reach over USD 123.00 Billion by 2032 from a value of USD 57.80 Billion in 2024 and is projected to grow by USD 62.49 Billion in 2025, growing at a CAGR of 9.9% from 2025 to 2032.

What drives the growth of the Controlled Release Drug Delivery Market? +

Key drivers include increasing demand for sustained drug release to enhance patient compliance, rising prevalence of chronic diseases, and advancements in drug delivery technologies such as nanotechnology and targeted delivery systems.

What challenges does the market face? +

Challenges include high development costs, technical complexities in manufacturing controlled-release systems, and regulatory hurdles, which can increase time-to-market and limit adoption in cost-sensitive regions.

Which technology dominates the market? +

The targeted delivery systems segment leads the market due to its precision in delivering drugs directly to the site of action, reducing side effects and enhancing therapeutic outcomes.

Which segment is expected to grow the fastest? +

The transdermal systems segment is anticipated to register the fastest CAGR, driven by non-invasive applications, innovations in patch designs, and growing use in chronic disease management.