- Summary

- Table Of Content

- Methodology

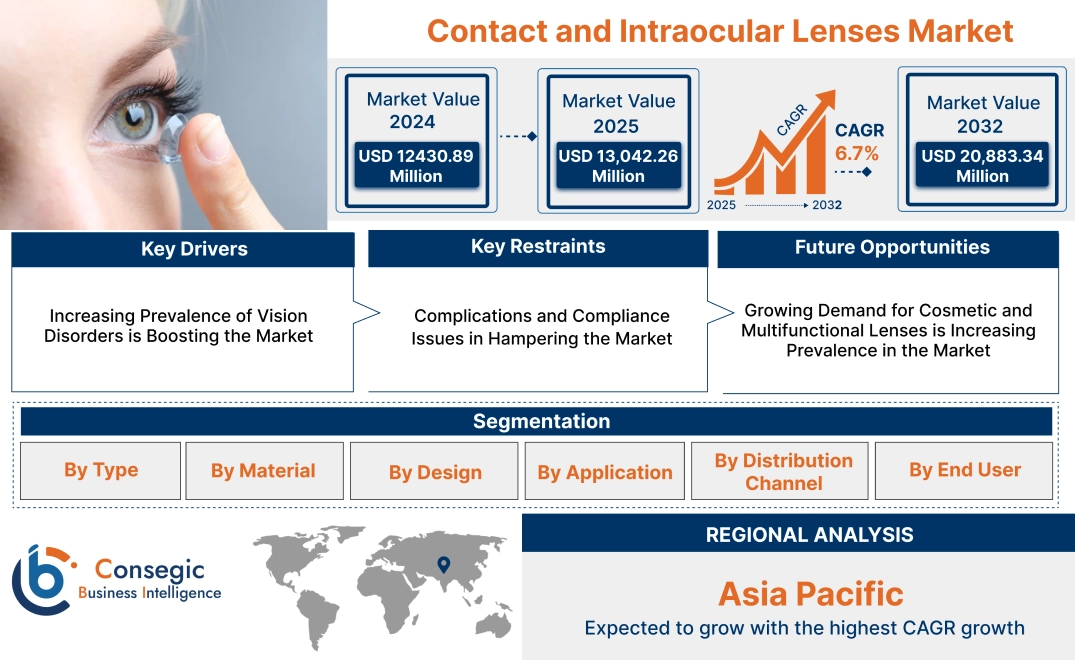

Contact and Intraocular Lenses Market Size:

Contact and Intraocular Lenses Market size is estimated to reach over USD 20,883.34 Million by 2032 from a value of USD 12430.89 Million in 2024 and is projected to grow by USD 13,042.26 Million in 2025, growing at a CAGR of 6.7% from 2025 to 2032.

Contact and Intraocular Lenses Market Scope & Overview:

The contact and intraocular lenses are designed to correct vision impairments, manage eye conditions, and enhance visual clarity. Contact lenses, worn directly on the eye's surface, and intraocular lenses (IOLs), surgically implanted inside the eye, cater to a wide range of refractive errors, including myopia, hyperopia, astigmatism, and presbyopia.

Key characteristics of these lenses include advanced materials offering high biocompatibility, enhanced oxygen permeability for comfort, and innovative designs such as multifocal and toric lenses. The benefits include improved vision quality, convenience in vision correction, and effective solutions for cataracts and other ophthalmic conditions.

Applications span vision correction, cataract surgery, and therapeutic uses, such as managing keratoconus or dry eye syndrome. End-users include ophthalmologists, optometrists, and patients, driven by rising prevalence of vision disorders, advancements in lens materials and technologies, and growing advancement for minimally invasive ophthalmic solutions.

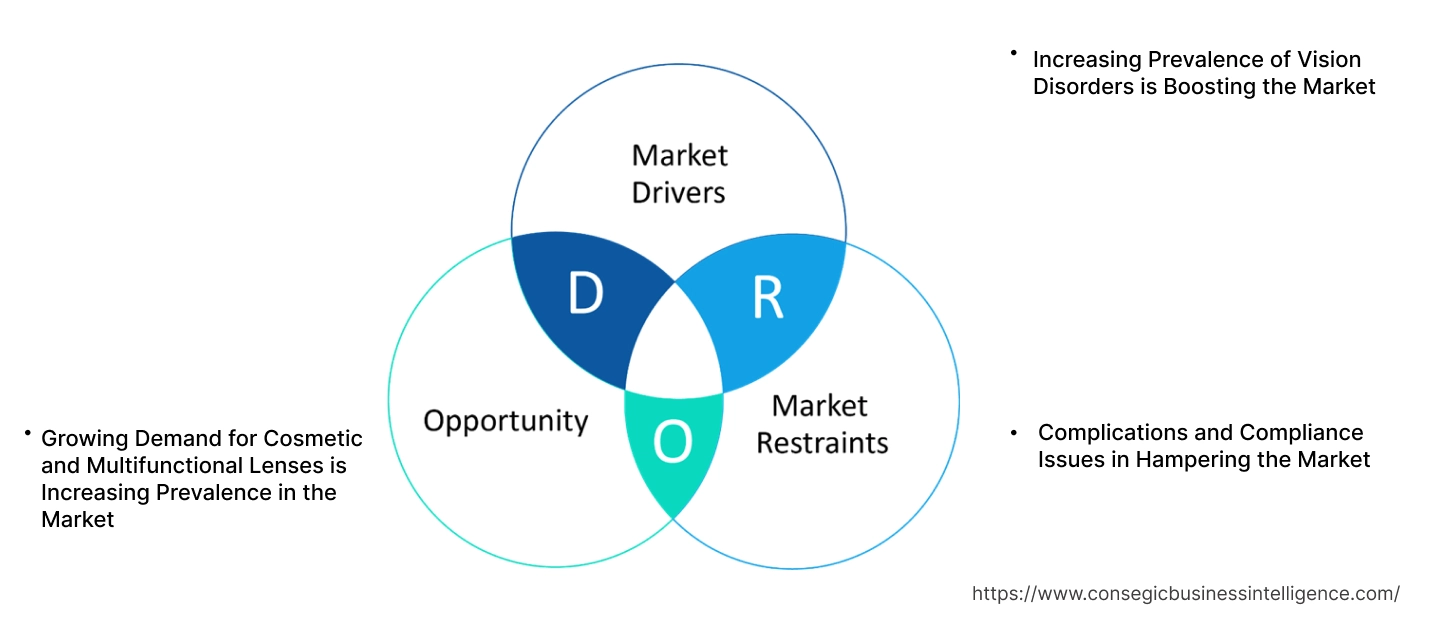

Contact and Intraocular Lenses Market Dynamics - (DRO) :

Key Drivers:

Increasing Prevalence of Vision Disorders is Boosting the Market

The rising prevalence of vision impairments, including myopia, hyperopia, presbyopia, and astigmatism, is a key driver for the contact and intraocular lenses market. Factors such as increased screen time, aging populations, and changing lifestyle habits contribute to this trend. The global surge in digital device usage, particularly among younger demographics, has led to a higher incidence of refractive errors requiring corrective solutions.

Trends in vision care emphasize early diagnosis and preventive measures, further driving the adoption of contact lenses and intraocular lenses (IOLs). Analysis indicates that the growing awareness of advanced lens technologies, along with the availability of personalized options, is enhancing accessibility and adoption across diverse patient groups.

Key Restraints:

Complications and Compliance Issues in Hampering the Market

Despite their widespread use, contact lenses can pose challenges such as eye dryness, irritation, and a heightened risk of infections, especially when maintenance protocols are not followed correctly. Many users struggle with adhering to cleaning routines or replacing lenses as recommended, leading to potential complications that can deter long-term usage.

For intraocular lenses, post-surgical complications such as halos, glare, or infections can impact patient satisfaction. These challenges underscore the need for better patient education and advancements in lens materials and designs to address comfort and safety concerns effectively.

Future Opportunities :

Growing Demand for Cosmetic and Multifunctional Lenses is Increasing Prevalence in the Market

The increasing popularity of cosmetic contact lenses, used for aesthetic enhancement such as changing eye color, represents a significant growth opportunity. These lenses are gaining traction among younger demographics and in markets where personal appearance and fashion trends drive consumer behavior.

Additionally, multifunctional lenses offering UV protection, blue light filtration, or drug delivery capabilities are becoming highly sought after. These innovations cater to the dual needs of vision correction and eye health maintenance, aligning with trends in personalized and multi-purpose healthcare solutions. Analysis highlights that the demand for such advanced features will continue to shape the market, providing manufacturers with opportunities to diversify their offerings.

Contact and Intraocular Lenses Market Segmental Analysis :

By Type:

Based on type, the market is segmented into contact lenses and intraocular lenses (IOLs).

The contact lenses segment accounted for the largest revenue share in 2024.

- Contact lenses are widely used for vision correction, offering convenience and aesthetic appeal, driving their dominance in the market.

- Advancements in contact lens technology, such as silicone hydrogel lenses, have enhanced comfort and wearability, boosting adoption.

- Growing advancement for cosmetic lenses for enhancing eye appearance has further supported segment trends.

- Increasing availability of daily disposable and extended-wear contact lenses has expanded consumer accessibility.

The intraocular lenses (IOLs) segment is anticipated to register the fastest CAGR during the forecast period.

- The rising prevalence of cataracts, particularly among the aging population, is driving demand for IOLs for post-cataract surgery.

- Technological advancements in IOLs, such as multifocal and toric lenses, are improving visual outcomes and patient satisfaction.

- Increasing adoption of premium IOLs offering better vision correction and minimal side effects is boosting contact and intraocular lenses market growth.

- Growing healthcare access in emerging economies for cataract surgeries is expected to propel the surge for IOLs.

By Material:

Based on material, the market is segmented into silicone hydrogel, hydrogel, PMMA (polymethyl methacrylate), and others.

The silicone hydrogel segment accounted for the largest revenue share in 2024.

- Silicone hydrogel lenses are widely preferred for their superior oxygen permeability, ensuring greater comfort and eye health.

- Increasing adoption of silicone hydrogel lenses for extended wear and daily disposable options is driving segment growth.

- Technological advancements enabling thinner and more flexible lenses have enhanced consumer satisfaction.

- Rising awareness about the importance of eye health and lens material quality is supporting the dominance of silicone hydrogel lenses.

The PMMA segment is anticipated to register the fastest CAGR during the forecast period.

- PMMA is widely used in rigid gas permeable (RGP) lenses and intraocular lenses, offering durability and optical clarity.

- Increasing adoption in therapeutic applications, such as keratoconus management, is driving contact and intraocular lenses market trends in this segment.

- The affordability and long-lasting nature of PMMA lenses make them a preferred choice in low- and middle-income regions.

- Rising surge for high-precision optical devices in surgical procedures is expected to boost segment progress.

By Design:

Based on design, the market is segmented into spherical, toric, multifocal, and cosmetic lenses under contact lenses, and aspheric and spherical lenses under intraocular lenses.

The spherical contact lenses segment accounted for the largest revenue share in 2024.

- Spherical lenses are commonly used for correcting myopia and hyperopia, making them the most widely adopted lens design.

- Increasing availability of daily disposable and extended-wear spherical lenses is driving surge.

- Rising consumer preference for simple and effective vision correction solutions supports the dominance of this segment.

- Technological advancements in lens coating to reduce glare and improve clarity are enhancing adoption.

The multifocal intraocular lenses segment is anticipated to register the fastest CAGR during the forecast period.

- Multifocal lenses are gaining traction for their ability to correct presbyopia and provide better near and distance vision post-cataract surgery.

- Increasing adoption of multifocal IOLs among aging populations for improved quality of life is driving contact and intraocular lenses market demand.

- Advancements in lens design reducing halos and glare have boosted patient satisfaction and contact and intraocular lenses market growth.

- Expanding healthcare infrastructure and awareness campaigns for cataract treatment in emerging markets are propelling this segment.

By Application:

Based on application, the market is segmented into vision correction (myopia, hyperopia, astigmatism, presbyopia), therapeutic, cosmetic, and post-cataract surgery.

The vision correction segment accounted for the largest revenue in contact and intraocular lenses market share in 2024.

- The high prevalence of refractive errors globally has driven the advancement for contact lenses and intraocular lenses for vision correction.

- Increasing adoption of advanced lenses, such as toric and multifocal lenses, to address specific refractive errors is supporting advancement.

- Rising awareness about vision health and increasing visits to eye care professionals are driving advancement in this segment.

- Government initiatives to reduce visual impairment, particularly in developing regions, are further boosting adoption.

The post-cataract surgery segment is anticipated to register the fastest CAGR during the forecast period.

- Increasing prevalence of cataracts among the elderly population is driving contact and intraocular lenses market demand for IOLs for post-surgical vision restoration.

- Advancements in premium IOLs offering better vision correction with minimal side effects are boosting segment trends.

- Rising access to affordable cataract surgeries in emerging economies is expanding the market for post-cataract lenses.

- Growing adoption of minimally invasive surgical techniques has enhanced patient outcomes, further supporting this segment.

By Distribution Channel:

Based on distribution channel, the market is segmented into hospital pharmacies, retail optical stores, online retailers, and clinics.

The retail optical stores segment accounted for the largest revenue in contact and intraocular lenses market share in 2024.

- Retail optical stores remain the primary distribution channel for contact lenses due to their accessibility and personalized fitting services.

- Increasing availability of a wide range of lens types and brands in retail stores has strengthened their market position.

- Growing consumer preference for in-person consultations and immediate purchase options is driving advancement in this segment.

- Expanding retail chains in developing regions are further boosting market progress.

The online retailers segment is anticipated to register the fastest CAGR during the forecast period.

- Online platforms offer convenience, competitive pricing, and a wide range of options, driving surge in this segment.

- Increasing adoption of e-commerce for medical devices, including lenses, is fueling progress.

- Rising awareness about trusted online retailers and subscription-based models for regular lens replacement are supporting expansion.

- Growing internet penetration and consumer preference for home delivery services are expected to propel advancement in this segment.

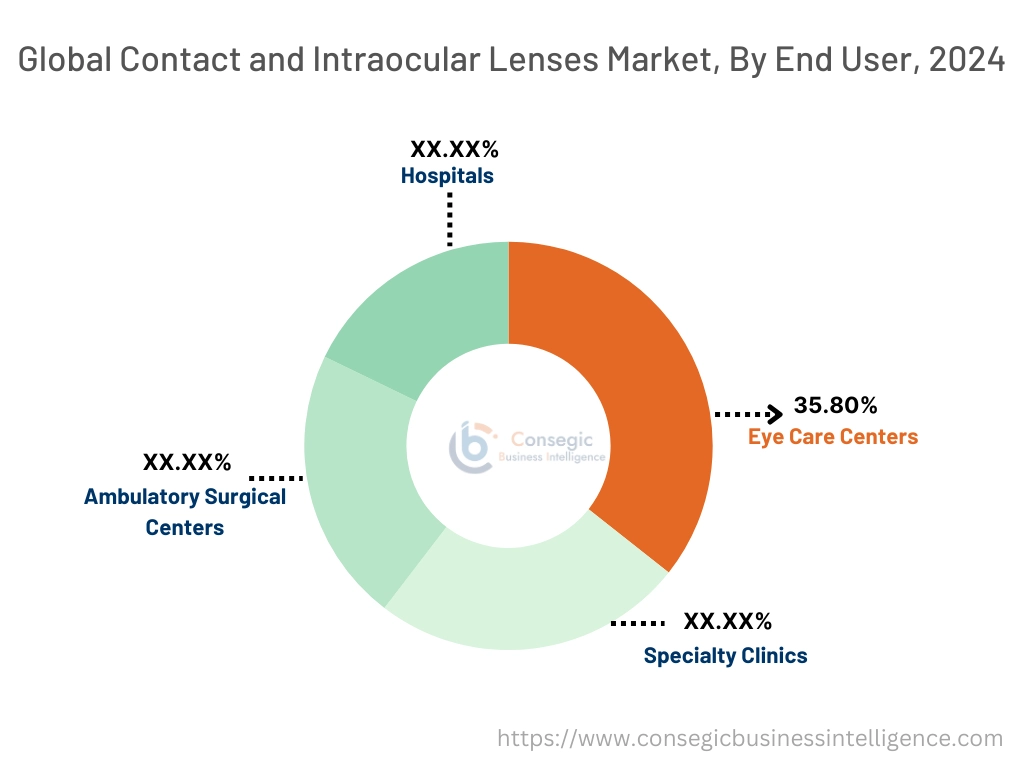

By End-User:

Based on end-user, the market is segmented into hospitals, specialty clinics, ambulatory surgical centers, and eye care centers.

The eye care centers segment accounted for the largest revenue share of 35.80% in 2024.

- Eye care centers specialize in vision correction and post-surgical care, making them the preferred choice for lens fitting and purchase.

- Increasing patient preference for expert consultations and personalized care at dedicated centers is driving contact and intraocular lenses market trends.

- Rising awareness about comprehensive eye care services and increasing accessibility of eye care centers are boosting demand.

- Partnerships between lens manufacturers and eye care centers to offer advanced products and technologies are supporting this segment.

The specialty clinics segment is anticipated to register the fastest CAGR during the forecast period.

- Specialty clinics focusing on refractive errors and surgical corrections offer tailored care, driving development in this segment.

- Expanding clinic networks in urban and semi-urban regions are improving access to advanced eye care solutions.

- Growing adoption of premium lenses in specialty clinics for enhanced patient outcomes is fueling growth.

- Increased collaborations with ophthalmologists and healthcare providers for advanced diagnostic and treatment solutions are expected to propel this segment.

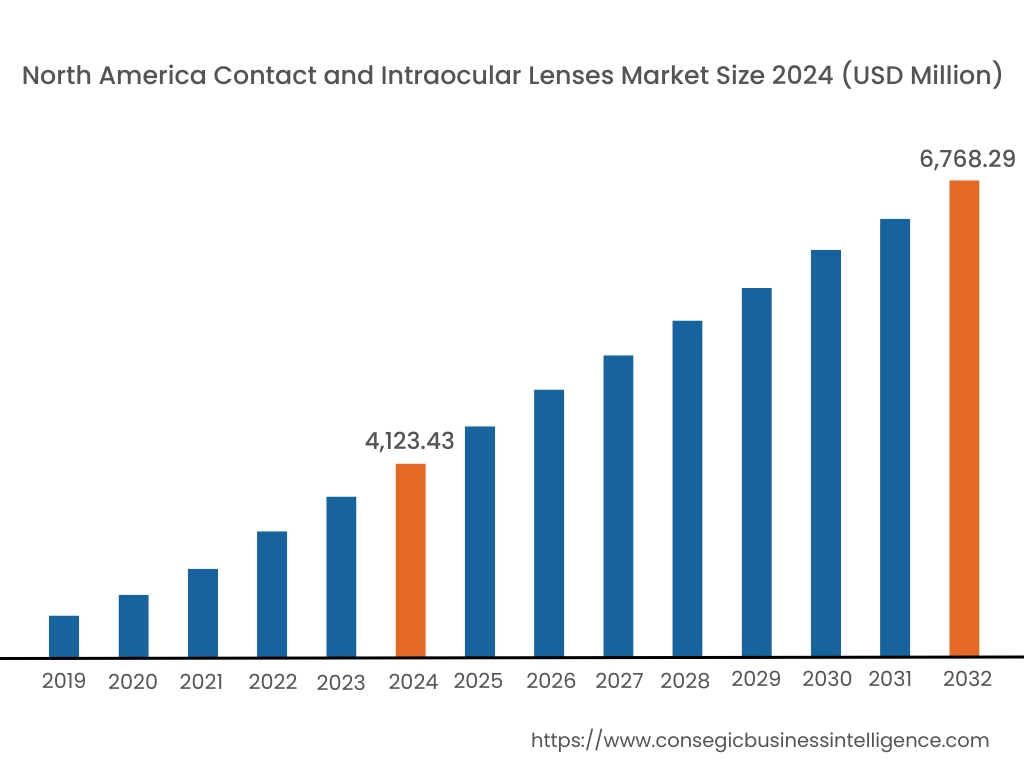

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

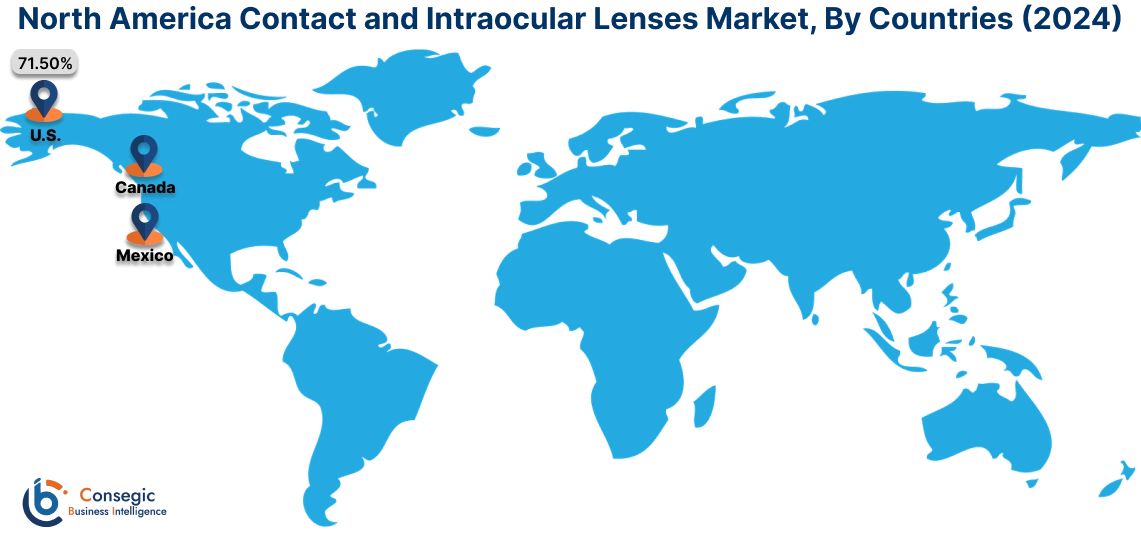

In 2024, North America was valued at USD 4,123.43 Million and is expected to reach USD 6,768.29 Million in 2032. In North America, the U.S. accounted for the highest share of 71.50% during the base year of 2024. North America holds a significant stake in the global contact and intraocular lenses market, driven by high prevalence of vision disorders, advanced healthcare infrastructure, and widespread adoption of corrective eyewear. The U.S. dominates the region with growing need for contact lenses for both vision correction and cosmetic purposes, along with increasing adoption of intraocular lenses (IOLs) for cataract surgeries. As per the contact and intraocular lenses market analysis, Canada contributes with rising awareness about eye health and expanding availability of advanced IOLs and multifocal contact lenses. However, the high cost of premium lenses and surgical procedures may limit access for some patient groups.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 7.1% over the forecast period. The contact and intraocular lenses market analysis, is fueled by increasing prevalence of refractive errors and cataracts, improving healthcare infrastructure, and growing awareness about eye health in China, India, and Japan. China dominates the region with rising adoption of contact lenses among the younger population for both corrective and cosmetic purposes, and increasing contact and intraocular lenses market opportunities for IOLs due to a high cataract burden. India’s expanding healthcare sector supports trends for affordable lenses and advanced IOLs, particularly in urban areas. Japan emphasizes high-quality contact lenses and advanced cataract surgery solutions, leveraging its strong medical device industry. However, limited access to eye care in rural areas may hinder contact and intraocular lenses market expansion in some parts of the region.

Europe is a prominent market for contact and intraocular lenses, supported by an aging population, increasing prevalence of eye disorders, and advanced ophthalmic care facilities. As per the countries analysis like Germany, France, and the UK are key contributors. Germany drives demand through its strong focus on cataract surgeries and adoption of advanced IOL technologies, including toric and multifocal lenses. France emphasizes the use of daily disposable and specialty contact lenses for better eye health, while the UK invests in public awareness campaigns and innovative eyewear solutions. However, strict EU regulations on medical devices may pose challenges for manufacturers in the region.

The Middle East & Africa region is witnessing steady growth in the global contact and intraocular lenses market, driven by increasing investments in healthcare infrastructure and rising prevalence of vision impairment. Countries like Saudi Arabia and the UAE are adopting advanced ophthalmic care solutions, including premium IOLs and specialty contact lenses, supported by government initiatives to improve eye health. In Africa, South Africa is emerging as a key market, focusing on improving access to affordable contact lenses and cataract surgeries through public-private partnerships. However, limited availability of advanced ophthalmic care in many parts of the region may restrict broader market expansion.

Latin America is an emerging market for contact and intraocular lenses, with Brazil and Mexico leading the region. Brazil’s growing healthcare sector and increasing adoption of cataract surgeries drive trends for premium IOLs and multifocal lenses. Mexico focuses on expanding access to affordable contact lenses and eye care services, supported by public health initiatives to address vision disorders. The region is also witnessing rising advancement for cosmetic contact lenses among younger populations. However, economic instability and inconsistent healthcare infrastructure in smaller economies may pose challenges to contact and intraocular lenses market expansion.

Top Key Players and Market Share Insights:

The contact and intraocular lenses market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the contact and intraocular lenses market. Key players in the contact and intraocular lenses industry include -

- Johnson & Johnson Vision Care, Inc. (United States)

- Alcon, Inc. (Switzerland)

- STAAR Surgical Company (United States)

- Rayner Surgical Group (United Kingdom)

- Menicon Co., Ltd. (Japan)

- Bausch + Lomb (United States)

- CooperVision, Inc. (United States)

- Carl Zeiss Meditec AG (Germany)

- Hoya Corporation (Japan)

- EssilorLuxottica (France)

Contact and Intraocular Lenses Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 20,883.34 Million |

| CAGR (2025-2032) | 6.7% |

| By Type |

|

| By Material |

|

| By Design |

|

| By Application |

|

| By Distribution Channel |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the estimated size of the Contact and Intraocular Lenses Market by 2032? +

Contact and Intraocular Lenses Market size is estimated to reach over USD 20,883.34 Million by 2032 from a value of USD 12430.89 Million in 2024 and is projected to grow by USD 13,042.26 Million in 2025, growing at a CAGR of 6.7% from 2025 to 2032.

What are the key types of lenses in this market? +

The market includes Contact Lenses and Intraocular Lenses (IOLs). Contact lenses are primarily used for vision correction and cosmetic purposes, while IOLs are surgically implanted to address conditions like cataracts.

What drives the growth of this market? +

Key drivers include the rising prevalence of vision disorders such as myopia, hyperopia, presbyopia, and astigmatism, technological advancements in lens materials and designs, and increasing demand for minimally invasive ophthalmic solutions.

What challenges does the market face? +

Challenges include complications such as eye dryness and irritation associated with contact lenses, post-surgical issues like halos and glare with IOLs, and compliance issues with lens care and maintenance.

What is the estimated size of the Contact and Intraocular Lenses Market by 2032? +

Contact and Intraocular Lenses Market size is estimated to reach over USD 20,883.34 Million by 2032 from a value of USD 12430.89 Million in 2024 and is projected to grow by USD 13,042.26 Million in 2025, growing at a CAGR of 6.7% from 2025 to 2032.

What are the key types of lenses in this market? +

The market includes Contact Lenses and Intraocular Lenses (IOLs). Contact lenses are primarily used for vision correction and cosmetic purposes, while IOLs are surgically implanted to address conditions like cataracts.

What drives the growth of this market? +

Key drivers include the rising prevalence of vision disorders such as myopia, hyperopia, presbyopia, and astigmatism, technological advancements in lens materials and designs, and increasing demand for minimally invasive ophthalmic solutions.

What challenges does the market face? +

Challenges include complications such as eye dryness and irritation associated with contact lenses, post-surgical issues like halos and glare with IOLs, and compliance issues with lens care and maintenance.