- Summary

- Table Of Content

- Methodology

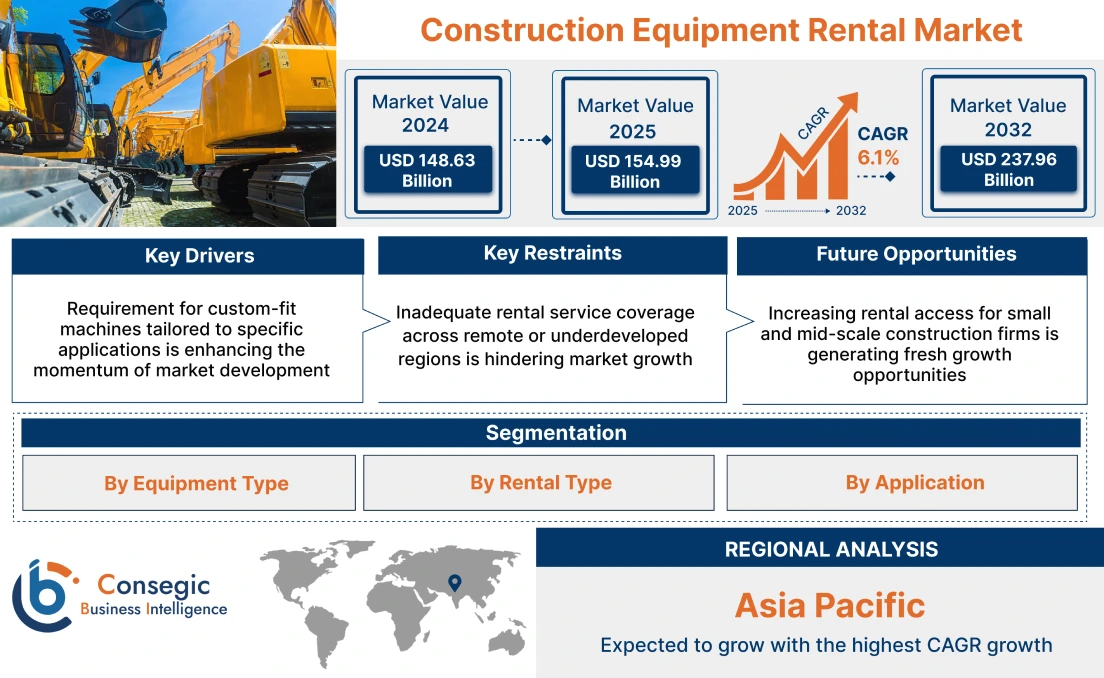

Construction Equipment Rental Market Size:

Construction Equipment Rental Market size is estimated to reach over USD 237.96 Billion by 2032 from a value of USD 148.63 Billion in 2024 and is projected to grow by USD 154.99 Billion in 2025, growing at a CAGR of 6.1% from 2025 to 2032.

Construction Equipment Rental Market Scope & Overview:

Construction equipment rental refers to the temporary use of heavy machines, tools, and vehicles needed to carry out construction work. This service gives contractors, builders, and infrastructure firms access to equipment without having to buy it. Rental options are available through equipment dealers, rental companies, or online platforms, and cover a wide range of machines such as cranes, excavators, pavers, loaders, and compactors used for different types of building projects.

Rental contracts are often tailored based on project length, equipment type, usage hours, and required attachments. Fleet operators ensure machines are maintained according to operational safety and performance standards, with pre-dispatch inspections and service records often included. Some rental providers offer machine delivery, setup, and operator training as part of the service package. Digital platforms for equipment booking may include features like real-time availability, maintenance alerts, and usage tracking.

Construction equipment rental allows project teams to manage costs and scale their equipment use depending on the job complexity and timeline. End-users include general contractors, subcontractors, and project managers who require flexible access to a wide range of machinery suited for site-specific requirements.

Construction Equipment Rental Market Dynamics - (DRO) :

Key Drivers:

Requirement for custom-fit machines tailored to specific applications is enhancing the momentum of market development.

Projects requiring cranes, excavators, and bulldozers for specific tasks, such as heavy lifting, underground construction, or complex structural work, often demand specialized equipment in niche construction projects. Many construction companies prefer renting these specialized machines instead of making large investments in equipment that may only be needed for a short period. Renting provides flexibility by allowing contractors to access the latest models with advanced features, without the long-term financial commitment of ownership. This approach is particularly beneficial for projects that require high-tech equipment for specific, short-term tasks.

- For instance, in April 2025, AKTIO Corporation, in collaboration with Toko Electric Construction, TA Lift, and Kitagawa Iron Works, launched the rental service for the newly developed JCW1250 tower crane designed specifically for wind turbine construction. This advanced crane eliminates the need for foundation work thanks to its foldable cross-base, significantly reducing site area requirements. This launch aligns with AKTIO’s broader strategy of “Rensalting,” combining rental and consulting services to deliver value-added solutions through both equipment and expert support.

As construction tasks become more specialized and intricate, the need for such rental services grows, offering an efficient and cost-effective solution for contractors. The increasing complexity of construction work, particularly in urban infrastructure and specialized industries, continues to drive the construction equipment rental market growth for specialized construction machinery.

Key Restraints:

Inadequate rental service coverage across remote or underdeveloped regions is hindering market growth.

Rural areas and remote places pose as a significant barrier to the widespread adoption of construction equipment rentals. These locations often lack the infrastructure to support efficient delivery, servicing, and maintenance of rental equipment. For contractors in such areas, the inability to access high-quality machinery when needed can severely impact their ability to complete projects on time and within budget. Moreover, the logistics involved in transporting and maintaining rental equipment in less accessible regions increase the overall cost of service, making rentals less attractive. Furthermore, the higher transportation and maintenance expenses faced by rental companies operating in rural areas are passed on to customers, which in turn reduces market penetration. As a result, the disparity between urban and rural access to construction equipment rental services remains a barrier.

Future Opportunities :

Increasing rental access for small and mid-scale construction firms is generating fresh growth opportunities.

Rising construction industry open new avenues for the market particularly among small and medium-scale contractors. Many of these businesses are unable to afford the high upfront costs of purchasing advanced machinery, such as cranes, bulldozers, and excavators. Renting offers an affordable and flexible solution, enabling these companies to access high-quality equipment without the financial burden of ownership. By offering tailored rental terms, such as short-term leases or pay-per-use options, rental companies can cater to the specific needs of small and medium-scale projects. This market segment is particularly important in emerging economies, where small-scale construction and infrastructure development are on the rise.

- For instance, in March 2025, Sunstate Equipment Co., LLC announced the acquisition of AJ Rental, a Dallas-based equipment rental company known for its strong customer relationships and reliable service. This acquisition enhances Sunstate’s presence in the Dallas-Fort Worth area, adding to its fleet and expanding service capabilities in one of the fastest-growing construction markets in the U.S. AJ Rental’s team and operations will be integrated into Sunstate’s network, ensuring continued local service excellence while benefiting from Sunstate’s national resources and support systems.

Providing affordable, high-quality equipment for smaller operations allows rental companies to capture a larger share of the market and supports the growth of construction projects in developing regions. The continued expansion into this niche presents significant growth, driving the global construction equipment rental market opportunities.

Construction Equipment Rental Market Segmental Analysis :

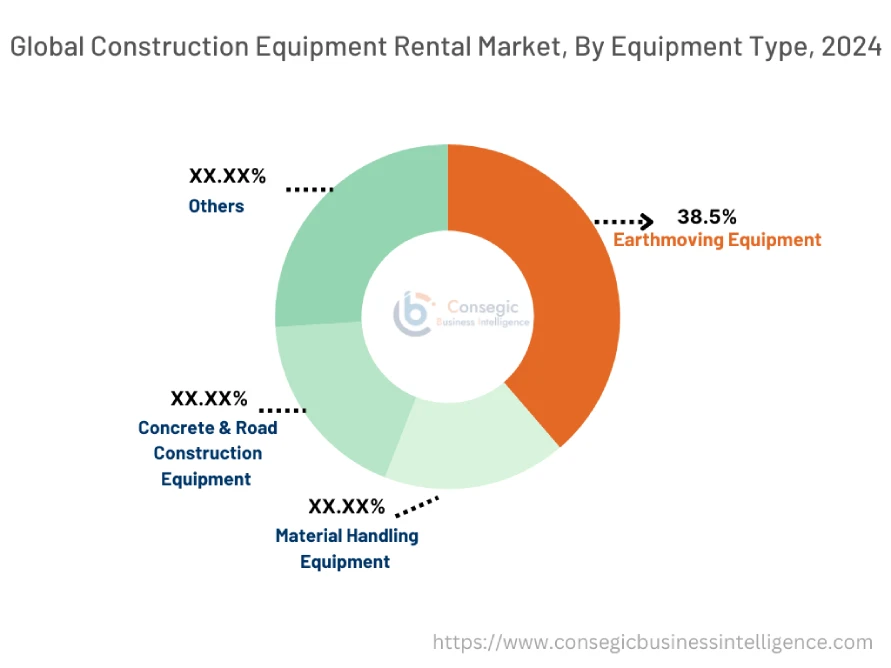

By Equipment Type:

Based on Equipment Type, the market is segmented into Earthmoving Equipment (Excavators, Loaders, Bulldozers, Backhoes), Material Handling Equipment (Cranes, Forklifts, Telehandlers), Concrete & Road Construction Equipment (Concrete Mixers, Pavers, Road Rollers), and Others (Compactors, Aerial Work Platforms).

The Earthmoving Equipment segment holds the largest revenue of the overall Construction Equipment Rental Market share of 38.5% in the year 2024.

- Earthmoving equipment remains the most rented category due to its essential use in foundational excavation, site grading, and terrain preparation.

- Excavators and Loaders lead rental activity due to their utility across residential, infrastructure, mining, and industrial construction.

- Backhoes are in high demand in small-to-medium urban projects where space-constrained digging and material transport are required.

- For instance, in November 2023, H&E Equipment Services completed the acquisition of Giffin Equipment, a respected rental and sales company based in California. This strategic move expanded H&E’s footprint in the West Coast market, particularly in Santa Barbara, Ventura, and San Luis Obispo counties. Giffin Equipment brings a strong regional presence and a loyal customer base, along with a diverse fleet of aerial lifts, earthmoving equipment, and material handling machines.

- According to the construction equipment rental market analysis, its consistent year-round requirement and relatively high return on asset (ROA), earthmoving equipment remains the largest segment, fueling the construction equipment rental market expansion.

The Concrete & Road Construction Equipment segment is expected to grow at the fastest CAGR during the forecast period.

- This segment is gaining traction due to rising investments in public infrastructure such as roads, bridges, airports, and transport terminals.

- Concrete Mixers and Road Rollers are frequently rented during urban transit projects and highway rehabilitation programs.

- Equipment in this category is typically used for specific project phases, making rental a preferred cost-effective option.

- As per the market analysis, the national governments prioritize sustainable and time-bound infrastructure upgrades in construction equipment, fueling the global construction equipment rental market development.

By Rental Type:

Based on Rental Type, the market is categorized into Short-Term Rental and Long-Term Rental.

The Short-Term Rental segment holds the largest revenue share of the overall Construction Equipment Rental Market in the year 2024.

- Short-term rentals typically spanning days to a few months are ideal for seasonal projects, emergency infrastructure works, and peak activity periods.

- Contractors prefer short-term rentals for flexibility, quick access to specialized machines, and project-specific fleet adjustments.

- Equipment such as mini-excavators, skid-steer loaders, and portable generators are particularly popular in short-term rental contracts.

- Thus, the adaptability and ease of procurement, short-term rental remains the most dominant structure, significantly drives the construction equipment rental market trends.

The Long-Term Rental segment is expected to grow at the fastest CAGR during the forecast period.

- Long-term rentals—extending to annual or multi-year contracts—are gaining popularity for large infrastructure and industrial development projects.

- Such contracts offer cost predictability, maintenance inclusivity, and long-term equipment availability without large capital expenditures.

- Large firms and public-private partnership (PPP) projects are increasingly adopting long-term rental models to secure reliable equipment pipelines.

- According to the market analysis, with infrastructure projects becoming larger and more complex, the long-term rental segment is projected to grow, significantly fueling the global construction equipment rental market expansion.

By Application:

Based on Application, the market is segmented into Residential, Commercial, Industrial, and Infrastructure.

The Infrastructure segment holds the largest revenue of the overall Construction Equipment Rental Market share in the year 2024.

- Infrastructure development, including highways, airports, railways, and public utilities drives the majority of construction equipment rental requirement globally.

- Rental companies cater to large EPC contractors that need fleets of heavy-duty machinery over specific phases of multi-year projects.

- Governments' focus on rebuilding critical infrastructure post-pandemic and investing in sustainable transportation accelerates rental fleet extension.

- According to the construction equipment rental market analysis, due to its sheer scale and capital intensity, infrastructure remains the largest application segment for rented construction equipment, significantly fuels the construction equipment rental market growth.

The Commercial segment is expected to grow at the fastest CAGR during the forecast period.

- Rising investments in office spaces, shopping malls, data centers, and hospitality sectors are fueling demand for equipment rental in commercial construction.

- Flexible rental terms help small-to-medium contractors manage fluctuating equipment needs across commercial fit-outs and redevelopment projects.

- New market players, including tech-enabled rental platforms, are offering commercial contractors bundled services including delivery, on-site servicing, and fuel management.

- The rising trend for urbanization and development in retail and office infrastructure, have substantially driven the global construction equipment rental market demand.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

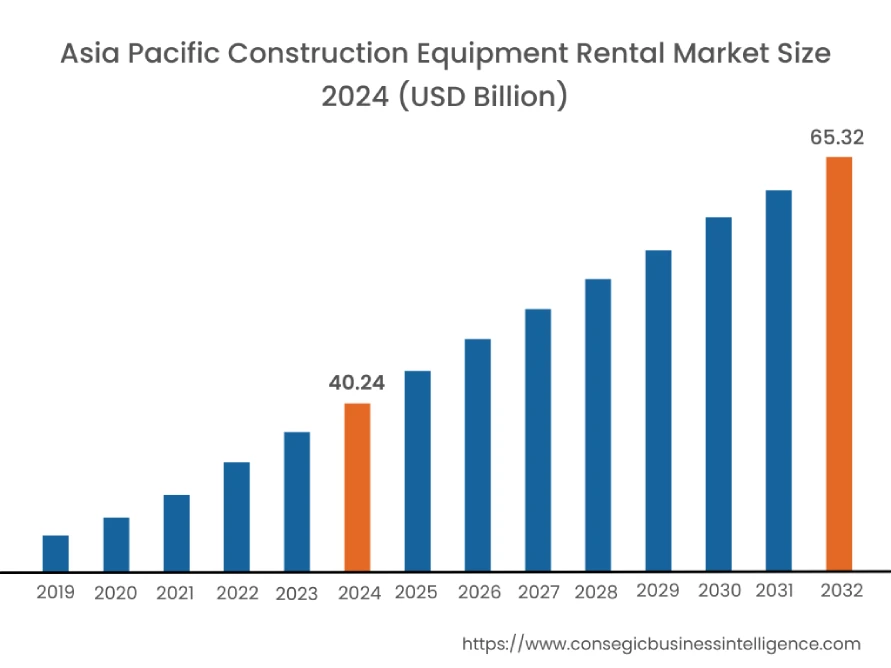

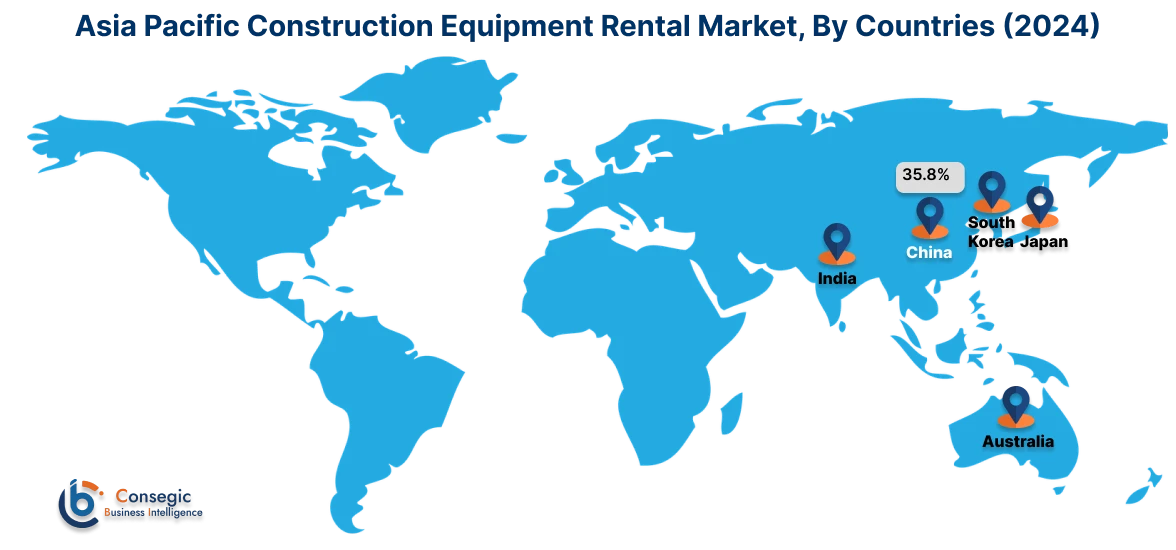

Asia Pacific region was valued at USD 40.24 Billion in 2024. Moreover, it is projected to grow by USD 42.01 Billion in 2025 and reach over USD 65.32 Billion by 2032. Out of this, China accounted for the maximum revenue share of 45.5%.

Asia-Pacific region is dominated by the government‑led mechanization policies and direct investment in rental infrastructure. The China’s mechanization mandates and India’s rental marketplace innovations are propelling market adoption, while Japan’s aging workforce and Australia’s mining renewal projects are driving uptake of smart rental solutions. Notable trends like the deployment of IoT‑connected sensors for real‑time equipment monitoring and predictive maintenance and the bundled service offerings like operator training, preventive maintenance, and logistics propels market demand.

- In February 2024, Coates, Australia’s leading equipment hire and solutions provider, acquired GTH Equipment, a well-established access equipment rental company based in Sydney. This strategic acquisition strengthened Coates’ position in the access equipment market by expanding its fleet of telehandlers, boom lifts, and scissor lifts, while enhancing its service capabilities across New South Wales. The move aligns with Coates’ broader strategy to deliver comprehensive, high-quality rental solutions across the construction and infrastructure sectors.

Furthermore, joint ventures between local distributors and global rental companies are essential for adapting services to local regulations and terrain, significantly driving the construction equipment rental market demand.

North America is estimated to reach over USD 79.26 Billion by 2032 from a value of USD 49.41 Billion in 2024 and is projected to grow by USD 51.54 Billion in 2025.

Across North America, the United States’ federal infrastructure modernization programs and Canada’s rural development financing schemes are encouraging widespread equipment leasing, while Mexico’s emergence of digital lending platforms is lowering entry barriers for small contractors. Additionally, the shifting trend towards the integration of telematics‑enabled fleet management systems that optimize utilization and cost tracking and app‑based, on‑demand reservation services that align equipment availability with project timelines drive market progress.

- For instance, in March 2024, United Rentals announced the introduction of Tower Crane Battery Energy Systems into its North American rental fleet, marking a step forward in advancing cleaner energy solutions for construction sites. These battery systems are designed to power tower cranes efficiently, helping reduce diesel fuel use, noise, and emissions while supporting grid-independent operation. The new addition aligns with United Rentals’ sustainability goals by providing customers with low-carbon alternatives that enhance energy efficiency and environmental performance on job sites.

Furthermore, supportive regulatory frameworks and strategic partnerships between rental firms and OEMs significantly driving the construction equipment rental industry in this region.

Europe exhibits a strong presence in the market due to the stringent environmental directives and national infrastructure funding act that promote efficient resource utilization in this region. Germany’s green building incentives and France’s urban redevelopment grants are driving rental fleet modernization, with Spain’s logistics hub proliferations and Italy’s tourism infrastructure projects following suit. Additionally, the growing usage‑based billing models enabled by embedded telematics and the rise of cooperative rental hubs in rural areas that pool resources among small and mid-scale contractors drive market progress. Analysis of the market showed that collaborations between equipment manufacturers and construction consortia refine service customization for diverse site requirements, significantly boosting the construction equipment rental market in this region.

Across the Middle East and Africa, the United Arab Emirates’ mega‑project developments and South Africa’s metro extension initiatives are anchoring equipment rental growth, with Kenya’s affordable housing schemes and Morocco’s resilience‑focused infrastructure programs also supporting uptake. A significant trend observed in this region is the specialized fleets outfitted with desert‑resilient modifications and water‑efficient accessories, while another trend highlights mobile maintenance units that service equipment on remote sites. Analysis of the market showed that state‑backed construction programs and resource‑optimization mandates are driving adoption, fueling the construction equipment rental market in this region.

In Latin America, the shifting trend for sustainable finance schemes and national infrastructure investment strategies is a major driving factor. Brazil’s agribusiness modernization and Argentina’s rural infrastructure upgrades set the pace for rental adoption, while Mexico’s industrial zone partnerships and Colombia’s pipeline rehabilitation projects follow industry trends in equipment leasing. Additionally, the introduction of cloud‑based reservation systems for real‑time inventory management and the integrated offerings that bundle preventive maintenance and operator training with rental agreements drives construction equipment rental market trends in this region.

Top Key Players and Market Share Insights:

The Construction Equipment Rental Market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Construction Equipment Rental Market. Key players in the Construction Equipment Rental industry include -

- United Rentals (USA)

- Sunbelt Rentals (Ashtead Group) (USA)

- Herc Rentals Inc. (USA)

- H&E Equipment Services (USA)

- Maxim Crane Works (USA)

- Sunstate Equipment Co. (USA)

- Boels Rental (Netherlands)

- Aktio Corporation (Japan)

- Coates Hire (Australia)

- Zeppelin Rental GmbH (Germany)

Recent Industry Developments :

Collaborations and Partnerships:

- In February 2025, BOELS Rental and JCB announced a landmark deal in which BOELS placed their largest-ever order with JCB, investing £65 million (€78 million) in a new fleet of construction machinery. The order includes a wide range of equipment such as micro and mini excavators, site dumpers, Loadalls, and compaction machines, all designed to meet the needs of BOELS’ extensive rental operations across Europe. The machines will be supported through JCB’s dealer network and are part of BOELS’ strategy to modernize its fleet with reliable, fuel-efficient, and high-performance equipment.

Construction Equipment Rental Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 237.96 Billion |

| CAGR (2025-2032) | 6.1% |

| By Equipment Type |

|

| By Rental Type |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Construction Equipment Rental Market? +

Construction Equipment Rental Market size is estimated to reach over USD 237.96 Billion by 2032 from a value of USD 148.63 Billion in 2024 and is projected to grow by USD 154.99 Billion in 2025, growing at a CAGR of 6.1% from 2025 to 2032.

What specific segments are covered in the Construction Equipment Rental Market? +

The Construction Equipment Rental Market specific segments for Equipment Type, Rental Type, Application, and Region.

Which is the fastest-growing region in the Construction Equipment Rental Market? +

Asia pacific is the fastest growing region in the Construction Equipment Rental Market.

What are the major players in the Construction Equipment Rental Market? +

The key players in the Construction Equipment Rental Market are United Rentals (USA), Sunbelt Rentals (Ashtead Group) (USA), Herc Rentals Inc. (USA), H&E Equipment Services (USA), Maxim Crane Works (USA), Sunstate Equipment Co. (USA), Boels Rental (Netherlands), Aktio Corporation (Japan), Coates Hire (Australia), Zeppelin Rental GmbH (Germany), and others.