- Summary

- Table Of Content

- Methodology

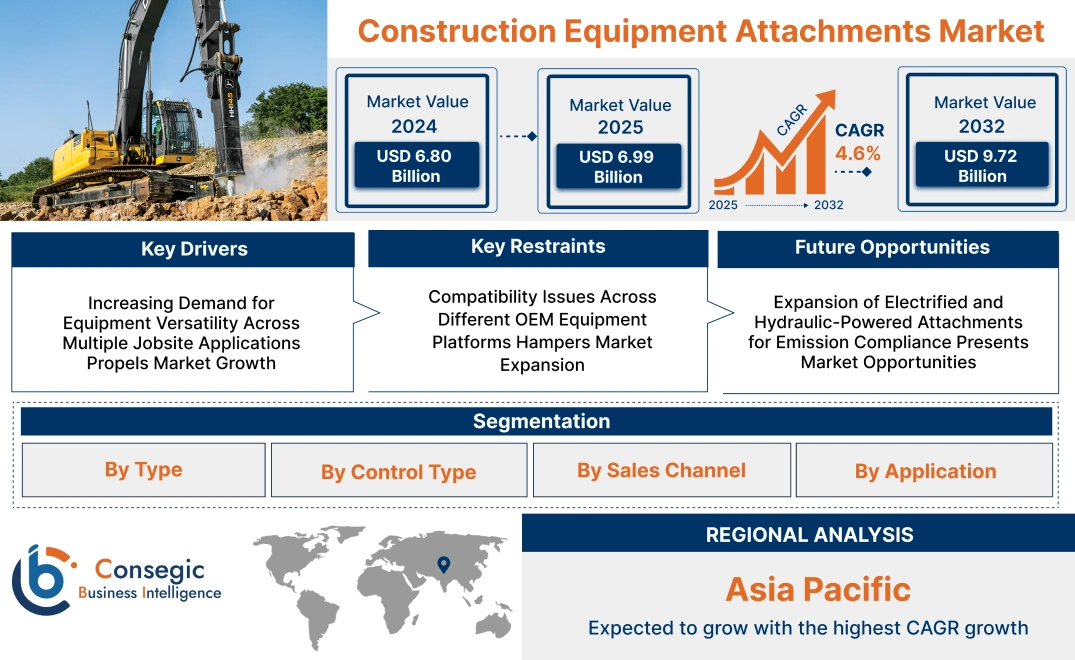

Construction Equipment Attachments Market Size:

Construction Equipment Attachments Market size is estimated to reach over USD 9.72 Billion by 2032 from a value of USD 6.80 Billion in 2024 and is projected to grow by USD 6.99 Billion in 2025, growing at a CAGR of 4.6% from 2025 to 2032.

Construction Equipment Attachments Market Scope & Overview:

Construction equipment attachments are specialized tools designed to enhance the functionality and versatility of base machinery such as excavators, skid steers, loaders, and backhoes. These attachments allow a single machine to perform multiple tasks by simply interchanging components, thereby optimizing equipment usage across a wide range of applications.

Common types include buckets, augers, hammers, grapples, rippers, and trenchers—each tailored for specific operations like digging, lifting, demolition, grading, or material handling. Many attachments feature quick couplers, hydraulic integration, and reinforced build quality to ensure durability and operational efficiency under demanding jobsite conditions.

Construction equipment attachments provide increased productivity, reduced equipment downtime, and improved precision in task execution. Their adaptability to varied terrain and working conditions makes them essential for infrastructure development, utility work, landscaping, and general construction. These tools enable contractors to achieve higher flexibility while minimizing the need for multiple dedicated machines.

Construction Equipment Attachments Market Dynamics - (DRO) :

Key Drivers:

Increasing Demand for Equipment Versatility Across Multiple Jobsite Applications Propels Market Growth

Contractors and operators are seeking greater flexibility from their heavy machinery investments, leading to rising adoption of specialized attachments that extend equipment functionality. From demolition hammers and augers to trenchers, buckets, and grapples, construction equipment attachments allow a single machine to perform diverse tasks across excavation, grading, lifting, and material handling operations. This versatility reduces the need for multiple machines on-site, optimizes fleet size, and increases operational efficiency. The growing volume of small to mid-scale construction and utility projects, especially in urban environments, emphasizes the need for adaptable solutions that enhance equipment productivity. Quick coupler systems and multi-function attachment platforms are supporting faster job transitions, minimizing downtime, and improving equipment utilization rates. As contractors focus on ROI and streamlined site logistics, the need for multifunctional toolsets is steadily rising, driving consistent construction equipment attachments market expansion.

Key Restraints:

Compatibility Issues Across Different OEM Equipment Platforms Hampers Market Expansion

A key limitation in the widespread use of construction equipment attachments lies in the lack of standardization across original equipment manufacturer (OEM) platforms. Attachments designed for a specific machine brand or model are often incompatible with other makes, limiting flexibility and requiring multiple purchases for mixed fleets. Contractors operating across various job sites face logistical challenges when interchanging attachments due to varying hydraulic coupler dimensions, control interfaces, and mounting systems. This fragmentation restricts attachment interoperability, particularly for rental companies and mid-sized operators managing diverse fleets. Additionally, the absence of universally accepted attachment standards leads to increased procurement complexity and operational inefficiencies. Despite growing demand for task-specific functionality, these compatibility concerns continue to limit broader utilization, ultimately constraining the construction equipment attachments market growth in multi-brand operating environments.

Future Opportunities :

Expansion of Electrified and Hydraulic-Powered Attachments for Emission Compliance Presents Market Opportunities

As environmental regulations tighten and construction firms prioritize sustainability, electrified and advanced hydraulic-powered attachments are gaining momentum. These solutions offer reduced emissions, lower noise levels, and greater energy efficiency, making them ideal for urban construction zones, indoor demolition, and environmentally sensitive projects. The demand for low-emission alternatives is also driving interest in battery-powered breakers, electric tiltrotators, and hydraulic compactors that align with green building initiatives. Growth in government-funded infrastructure projects with sustainability criteria is further accelerating the shift toward electrified attachment systems. Manufacturers are responding with next-generation attachments designed to integrate seamlessly with hybrid and electric machinery, enhancing operational synergy. These developments are opening new applications in sectors such as utilities, landscaping, and tunneling.

- For instance, in May 2024, Caterpillar launched three new Cat® Hydraulic Connecting CW (HCCW) coupler models, which connect seamlessly to the machine’s hydraulics, allowing operators to switch easily between the attachments from the cab. This improves productivity and saves time. The design includes improved hydraulic flow to reduce hydraulic restriction, minimizing heat build-up and reducing the engine power required.

As the construction industry embraces cleaner technologies, the transition to energy-efficient attachments is unlocking strong construction equipment attachments market opportunities driven by environmental compliance and operational growth.

Construction Equipment Attachments Market Segmental Analysis :

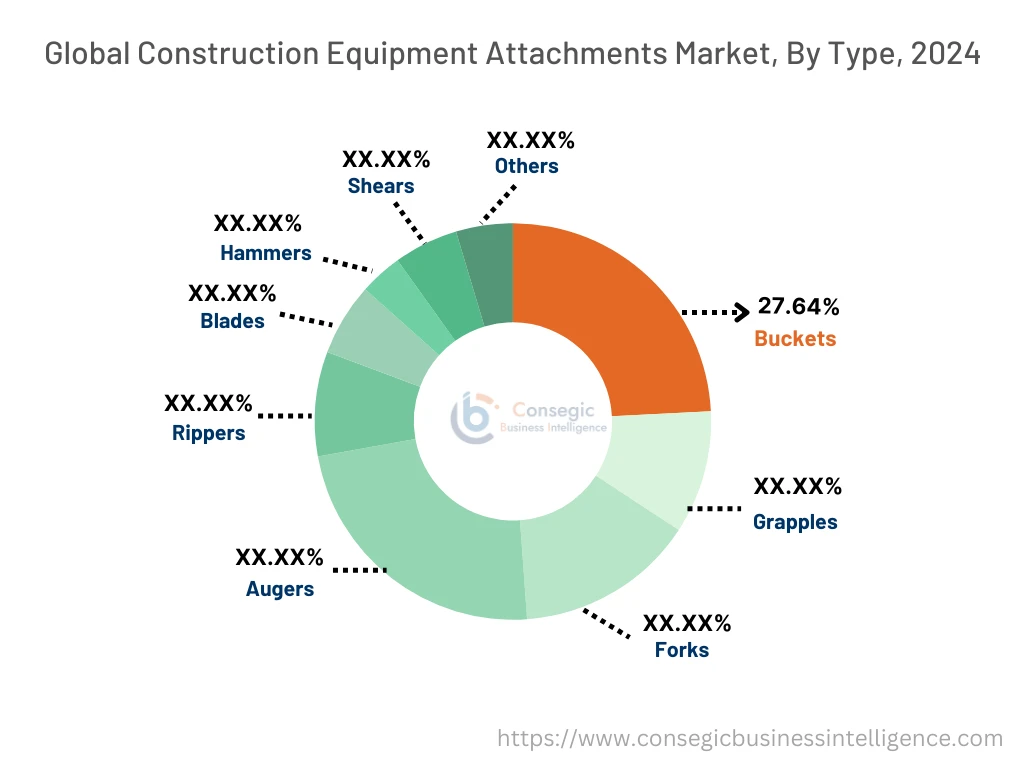

By Type:

Based on type, the market is segmented into buckets, grapples, forks, augers, rippers, blades, hammers, shears, and others.

The buckets segment accounted for the largest construction equipment attachments market share of 28.7% in 2024.

- Buckets are essential attachments for various construction equipment such as excavators and loaders.

- They are widely used in excavation, material handling, and landscaping for digging, lifting, and moving materials.

- The versatility of buckets in different sizes and configurations for specific applications, including trenching and loading, makes them indispensable in the construction and mining sectors.

- As per construction equipment attachments market analysis, the bucket segment continues to dominate due to its broad range of applications and widespread use in various industries.

The hammers segment is projected to register the fastest CAGR during the forecast period.

- Hammers are used in demolition and mining operations to break rocks, concrete, and other hard materials.

- These attachments offer increased impact force and efficiency in heavy-duty operations compared to traditional tools, making them highly valuable in construction and demolition.

- The growing demand for fast and efficient demolition in urban construction projects is driving the adoption of hammers.

- For instance, in March 2025, NPK unveiled the GHD-10 Hydraulic Hammer, the 1st model of the GHD Series to be released. It features a speed selector valve for adjustable speed depending on material types and a slip-fit lower tool bushing for easy servicing.

- According to construction equipment attachments market trends, the need for hammers is rising due to their higher productivity and cost-effectiveness in heavy-duty applications.

By Control Type:

Based on control type, the market is segmented into manual, hydraulic, and electric.

The hydraulic control segment held the largest market share in 2024.

- Hydraulic control systems are highly efficient in controlling the force and movement of attachments, making them suitable for heavy-duty equipment.

- These systems allow precise and continuous control, especially in applications like excavation, demolition, and grading, where high power and accuracy are required.

- The requirement for hydraulic-controlled attachments is supported by their ability to perform in tough environments, enhancing productivity and operational efficiency.

- For instance, in December 2024, Normet launched a hydraulic breaker for the Indian market. The MRB B24 hydraulic hammer is a reliable and cost-effective option for rock-breaking applications, including hard and soft rock, concrete, road surface, asphalt, hard or frozen ground. It features adjustable impact frequency and power for different material size and hardness ensuring versatility.

- As per construction equipment attachments market analysis, hydraulic systems continue to dominate due to their flexibility, power, and durability in demanding applications.

The electric control segment is expected to experience significant CAGR during the forecast period.

- Electric-powered attachments offer higher energy efficiency and lower emissions compared to hydraulic systems, making them an attractive option for green construction practices.

- These systems are becoming increasingly popular in urban construction projects, where noise reduction and environmental concerns are important.

- As the construction industry moves towards cleaner and more sustainable practices, the adoption of electric control systems is accelerating.

- According to construction equipment attachments market trends, the increase in electric-powered machinery and attachments is driven by the rising requirement for eco-friendly solutions.

By Sales Channel:

Based on sales channel, the market is segmented into OEMs and aftermarket.

The OEM segment accounted for the largest construction equipment attachments market share in 2024.

- Original Equipment Manufacturers (OEMs) supply attachments directly to construction equipment manufacturers, ensuring compatibility and high-quality standards.

- OEMs are integral in providing customized solutions, and the direct relationship with major construction equipment manufacturers drives the segment's growth.

- OEMs also offer warranties, maintenance, and technical support, which increases their attractiveness to large-scale construction companies.

- As per construction equipment attachments market demand, the OEM channel remains the dominant distribution method, driven by the need for high-quality, reliable equipment for large projects.

The aftermarket segment is expected to register the fastest CAGR during the forecast period.

- The aftermarket segment plays a crucial role in providing replacement parts, upgrades, and maintenance services for existing construction equipment attachments.

- This segment benefits from the large installed base of construction equipment that requires periodic maintenance and part replacements.

- The growing use of multi-functional equipment and attachments drives the need for specialized aftermarket services and products.

- According to segmental trends, the aftermarket segment is driving the construction equipment attachments market expansion as more equipment owners look for cost-effective solutions for maintaining their machinery.

By Application:

Based on application, the market is segmented into excavation, material handling, demolition, grading, construction, and others.

The excavation segment held the largest revenue share in 2024.

- Excavation attachments, such as buckets and augers, are essential in digging, trenching, and material removal, making them indispensable in construction, mining, and infrastructure projects.

- The versatility of excavation equipment in both small- and large-scale projects, including residential and commercial developments, continues to drive high demand.

- Excavation applications are increasingly being automated with advanced attachment technologies, further enhancing efficiency and safety.

- For instance, in May 2023, MB Crusher debuted three new padding buckets, the MB-HDS307, MB-HDS312 and MB-HDS412 for excavation purposes. Incorporating an automatic hydraulic bumper system to reduce hydraulic shock, the damage to the engine, transmission components and operating machine is minimized resulting in longer shelf life.

- Hence, excavation remains a primary driver of the construction equipment attachments market growth due to the increasing construction and urbanization activities worldwide.

The material handling segment is expected to grow at the fastest CAGR during the forecast period.

- Material handling attachments such as forks and grapples are widely used in warehouses, construction sites, and logistics operations to move materials safely and efficiently.

- The need for efficient and cost-effective material handling solutions in industries such as retail, logistics, and manufacturing is driving the expansion of this segment.

- With the rise of automated material handling systems and increased investments in warehouse and infrastructure development, the material handling segment is poised for rapid expansion.

- Thus, the material handling segment is expected to witness significant growth due to the increasing construction equipment attachments market demand.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

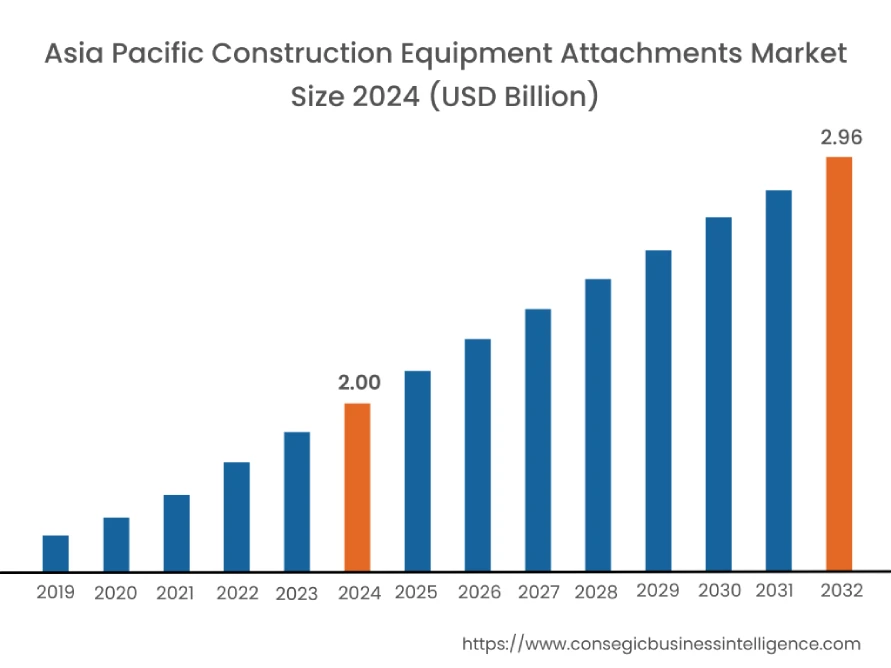

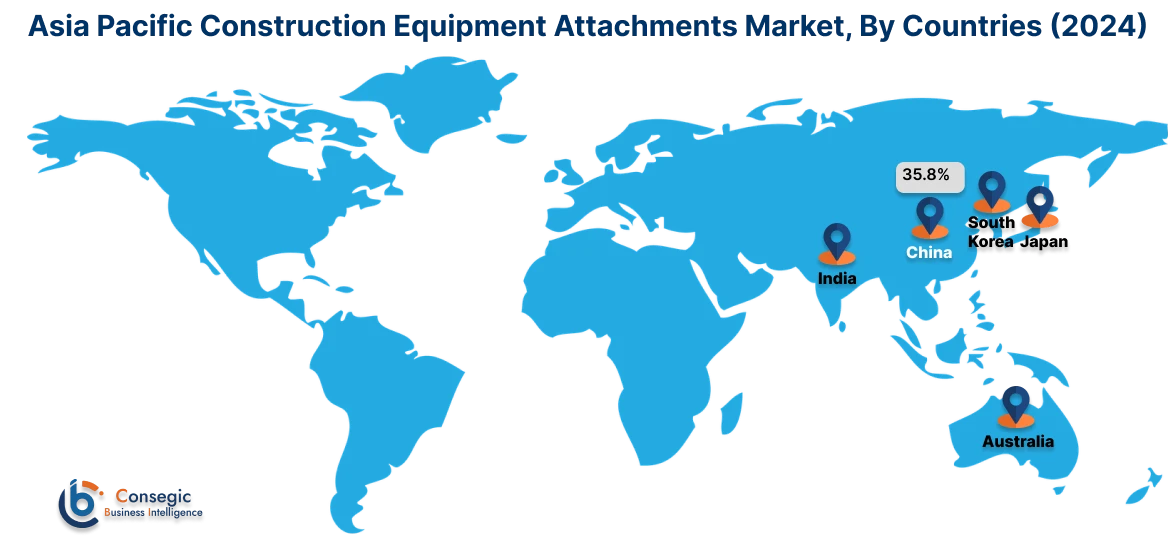

Asia Pacific region was valued at USD 2.00 Billion in 2024. Moreover, it is projected to grow by USD 2.06 Billion in 2025 and reach over USD 2.96 Billion by 2032. Out of this, China accounted for the maximum revenue share of 35.8%.Asia-Pacific is experiencing rapid growth, fueled by large-scale infrastructure expansion, industrial corridor development, and a booming construction equipment market. China, India, Japan, and South Korea are witnessing increased adoption of augers, hammers, and rippers in mining, tunneling, and commercial construction. Market analysis highlights the shift toward domestically produced attachments designed for local terrain and project requirements.

- For instance, in January 2025, Tata Hitachi launched an electric excavator, next-gen machines and advanced attachments at the BAUMA Conexpo 2024, India. The new attachments, which include a tapered ditch bucket, a jaw bucket, trencher – MT600 and a backfill blade, are designed for greater machine versatility.

Government-backed smart city initiatives and public housing projects are driving consistent demand for attachments that enable machinery to handle multiple operations across job sites with varying complexity.

North America is estimated to reach over USD 3.15 Billion by 2032 from a value of USD 2.26 Billion in 2024 and is projected to grow by USD 2.31 Billion in 2025. North America remains a dominant market, supported by a strong rental ecosystem, robust infrastructure development, and continued investment in urban renewal projects. Market analysis reveals a significant requirement for hydraulic breakers, grapples, and buckets in roadworks, demolition, and utility maintenance. The United States and Canada are increasingly incorporating quick-coupler systems and smart control interfaces to improve on-site productivity.

- For instance, in February 2024, CASE Construction Equipment launched new iron work tools and announced support to help rental companies succeed across North America. The product line includes backhoe loaders, mini excavators, mini track loaders, small articulated loaders and more.

Growth in the region is further propelled by labor shortages, leading contractors to favor multi-functional equipment that reduces idle time and optimizes fleet usage.

Europe exhibits steady adoption, particularly in renovation, underground utilities, and landscaping sectors. Countries such as Germany, France, and the United Kingdom are emphasizing compact equipment paired with specialized attachments due to space constraints and strict emissions regulations. Market analysis indicates rising deployment of tilt rotators, shears, and precision grading tools in both urban and rural applications. The construction equipment attachments market opportunity in Europe is bolstered by sustainable building practices and the push for low-noise, low-impact operations that require attachments tailored for specific site conditions and regulatory compliance.

Latin America is gradually scaling up usage, particularly in Brazil, Mexico, and Chile where construction and mining sectors are expanding. Attachments such as rock buckets, hydraulic compactors, and trenchers are gaining traction in excavation, roadwork, and utility installation. Market analysis shows that rental companies and mid-sized contractors are increasingly investing in modular attachment systems to improve cost efficiency. Growth in this region is supported by urban infrastructure upgrades and regional efforts to enhance construction productivity while managing operational costs through equipment flexibility.

The Middle East and Africa present a growing landscape for construction equipment attachments, especially in the UAE, Saudi Arabia, and South Africa. Market analysis indicates that the development of mega projects, mining operations, and utility networks is driving the adoption of high-durability attachments suited for heavy-duty applications. Couplers, blades, and lifting jibs are increasingly used to support varied terrain and climate conditions. Although adoption in parts of Africa remains nascent, need is emerging through government-backed infrastructure plans and increasing contractor awareness of operational efficiency gains through attachment-based machinery customization.

Top Key Players and Market Share Insights:

The construction equipment attachments market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global construction equipment attachments market. Key players in the construction equipment attachments industry include -

- Caterpillar Inc. (USA)

- Komatsu Ltd. (Japan)

- Volvo Construction Equipment (Sweden)

- Doosan Corporation (South Korea)

- JCB Ltd. (United Kingdom)

- <

- Liebherr Group (Germany)

- Hitachi Construction Machinery Co., Ltd. (Japan)

- CNH Industrial N.V. (CASE Construction) (United Kingdom)

- Kubota Corporation (Japan)

- SANY Group (China)

Recent Industry Developments :

Acquisitions:

- In October 2024, ZONE expanded its product portfolio with the acquisition of MultaVex. This enabled ROCK.ZONE to build on its vision to be the foremost provider of high-quality excavator attachments.

- In September 2024, Epiroc completed the acquisition of ACB+, a French manufacturer of excavator attachments for construction, scrap recycling and deconstruction purposes.

- In June 2024, the leading German manufacturer of for truck-mounted cranes, excavators and skid steer loaders, Kinshofer GmbH, acquired Eurosteel B.V., a Netherlands-based hydraulic attachments maker. This acquisition strengthens Kinshofer’s portfolio of quick couplers and buckets for excavators and wheel loaders, as well as improves Kinshofer’s distribution channels.

Partnerships:

- In February 2025, CASE Construction Equipment partnered with Stone Equipment to strengthen dealer networks in Alabama.

Construction Equipment Attachments Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 9.72 Billion |

| CAGR (2025-2032) | 4.6% |

| By Type |

|

| By Control Type |

|

| By Sales Channel |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Construction Equipment Attachments Market? +

Construction Equipment Attachments Market size is estimated to reach over USD 9.72 Billion by 2032 from a value of USD 6.80 Billion in 2024 and is projected to grow by USD 6.99 Billion in 2025, growing at a CAGR of 4.6% from 2025 to 2032.

What specific segmentation details are covered in the Construction Equipment Attachments Market report? +

The Construction Equipment Attachments market report includes specific segmentation details for type, control type, sales channel and application.

What are the applications of the Construction Equipment Attachments Market? +

The applications of the Construction Equipment Attachments Market are excavation, material handling, demolition, grading, construction, and others.

Who are the major players in the Construction Equipment Attachments Market? +

The key participants in the Construction Equipment Attachments market are Caterpillar Inc. (USA), Komatsu Ltd. (Japan), Volvo Construction Equipment (Sweden), Doosan Corporation (South Korea), JCB Ltd. (United Kingdom), Liebherr Group (Germany), Hitachi Construction Machinery Co., Ltd. (Japan), CNH Industrial N.V. (CASE Construction) (United Kingdom), Kubota Corporation (Japan) and SANY Group (China).