- Summary

- Table Of Content

- Methodology

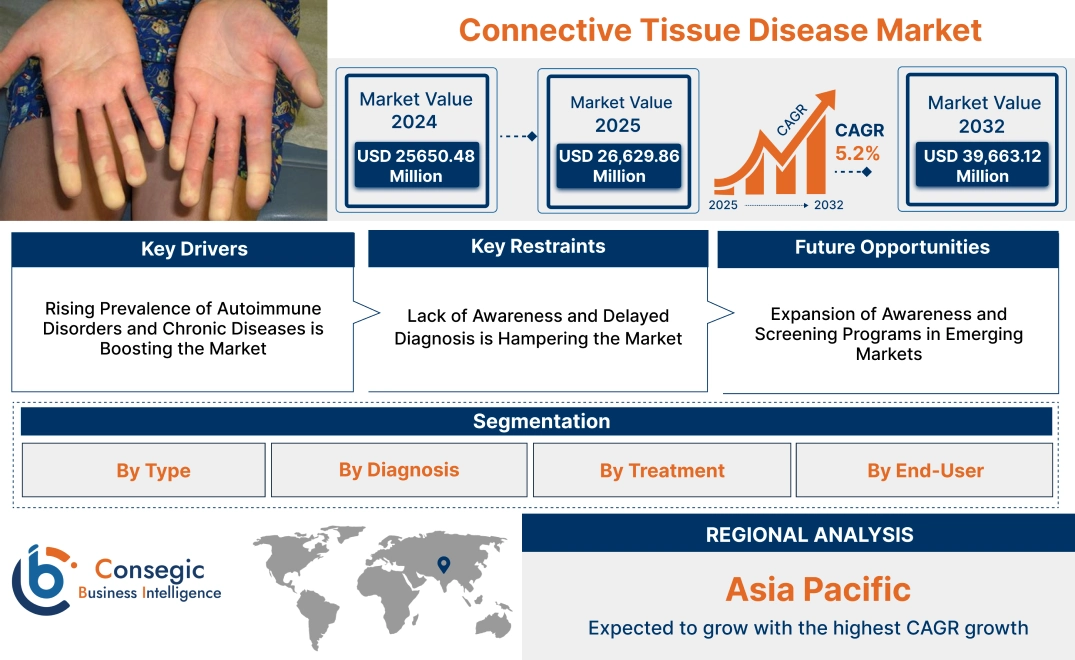

Connective Tissue Disease Market Size:

Connective Tissue Disease Market size is estimated to reach over USD 39,663.12 Million by 2032 from a value of USD 25650.48 Million in 2024 and is projected to grow by USD 26,629.86 Million in 2025, growing at a CAGR of 5.6% from 2025 to 2032.

Connective Tissue Disease Market Scope & Overview:

The connective tissue disease is a disorder affecting connective tissues, including systemic lupus erythematosus (SLE), scleroderma, rheumatoid arthritis, and mixed connective tissue disease (MCTD). This market encompasses pharmaceutical therapies, including immunosuppressants, corticosteroids, biologics, and symptomatic treatments, alongside diagnostic tools like blood tests and imaging technologies.

Key characteristics of connective tissue disease treatments include targeted approaches to modulate immune responses, advancements in biologics for precision medicine, and ongoing innovations in disease management strategies. The benefits include symptom relief, reduced disease progression, and improved patient quality of life. Applications span hospitals, specialty rheumatology clinics, and diagnostic laboratories. End-users include healthcare providers, rheumatologists, and patients, driven by the increasing prevalence of autoimmune and connective tissue disorders, advancements in therapeutic biologics, and rising awareness about early diagnosis and treatment options for managing chronic conditions.

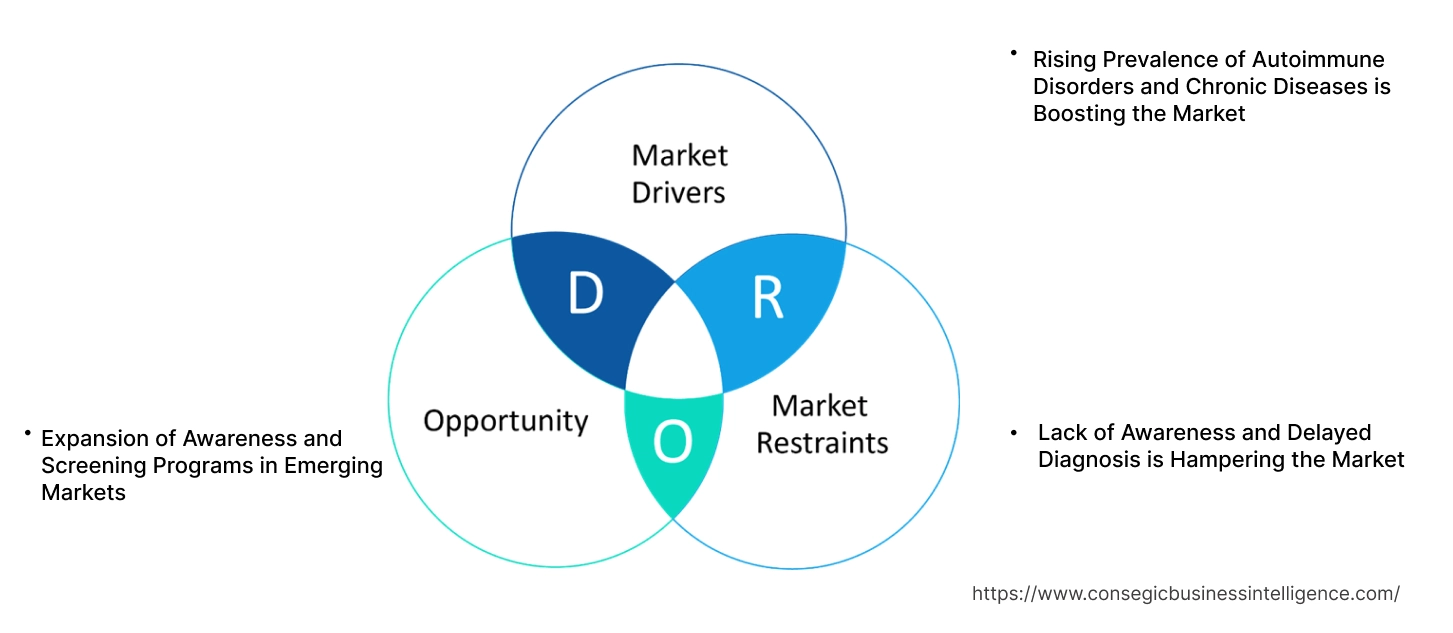

Connective Tissue Disease Market Dynamics - (DRO) :

Key Drivers:

Rising Prevalence of Autoimmune Disorders and Chronic Diseases is Boosting the Market

The increasing prevalence of autoimmune disorders, such as lupus, rheumatoid arthritis, and scleroderma, is significantly driving the connective tissue disease market. Factors such as aging populations, genetic predispositions, and environmental triggers like infections and pollution contribute to this rise. Chronic diseases affecting connective tissues are becoming more common, amplifying the need for advanced diagnostics and therapies.

Trends in healthcare highlight the importance of early diagnosis and intervention in managing these conditions effectively. Analysis indicates that improved awareness and access to specialized care are crucial in addressing the growing burden of connective tissue diseases globally.

Key Restraints:

Lack of Awareness and Delayed Diagnosis is Hampering the Market

Connective tissue diseases often present with non-specific symptoms, such as fatigue, joint pain, and skin abnormalities, which can be mistaken for less severe conditions. This leads to underdiagnosis or delayed diagnosis, especially in regions where awareness among patients and general healthcare providers is limited. Late detection increases the risk of complications and reduces the effectiveness of available treatments.

Trends in education and targeted campaigns are working to bridge these gaps, but significant efforts are still required to enhance awareness and improve early diagnosis, particularly in underserved areas.

Future Opportunities :

Expansion of Awareness and Screening Programs in Emerging Markets

Emerging markets present a significant opportunity for the connective tissue disease market, as healthcare infrastructure improves and awareness grows. Governments and healthcare organizations are increasingly prioritizing autoimmune disease screening programs and public health initiatives to address diagnostic and treatment gaps.

Trends in international collaborations and investments in healthcare systems are enabling the establishment of specialized rheumatology clinics and affordable diagnostic tools. Analysis highlights that these efforts will not only improve access to care but also drive market expansion, particularly in regions with a high unmet need for advanced treatment options.

Connective Tissue Disease Market Segmental Analysis :

By Type:

Based on type, the market is segmented into systemic lupus erythematosus (SLE), polymyositis, dermatomyositis, mixed connective tissue disease (MCTD), and others.

The systemic lupus erythematosus (SLE) segment accounted for the largest revenue in connective tissue disease market share in 2024.

- SLE is the most prevalent connective tissue disease, significantly driving demand for diagnostic and therapeutic solutions.

- Rising awareness about early detection and management of SLE has bolstered its dominance in the market.

- Advancements in biologic therapies targeting lupus-specific pathways have improved treatment outcomes, supporting this segment's growth.

- Increasing healthcare investments and supportive government initiatives for autoimmune disease management are further fueling trends.

The dermatomyositis segment is anticipated to register the fastest CAGR during the forecast period.

- Dermatomyositis is gaining attention due to its unique clinical presentation, leading to a higher focus on accurate diagnosis and management.

- Increasing adoption of advanced imaging techniques and targeted therapies for treating dermatomyositis is driving segment advancement.

- Expanding awareness among healthcare providers and patients about the importance of early intervention is boosting connective tissue disease market trends.

- Research into novel immunosuppressive and biologic therapies for dermatomyositis is expected to propel connective tissue disease market growth.

By Diagnosis:

Based on diagnosis, the market is segmented into blood tests, imaging tests, and biopsy.

The blood tests segment accounted for the largest revenue share in 2024.

- Blood tests, including autoantibody profiling and inflammatory marker analysis, are the primary diagnostic tools for connective tissue diseases.

- Their non-invasive nature, cost-effectiveness, and widespread availability make them a preferred choice in diagnostic settings.

- Increasing advancements in diagnostic accuracy through high-sensitivity assays and next-generation technologies are boosting this segment.

- Rising awareness about routine screening for autoimmune markers in high-risk populations is driving trends for blood tests.

The imaging tests segment is anticipated to register the fastest CAGR during the forecast period.

- Imaging techniques, such as MRI, ultrasound, and CT scans, are increasingly used to evaluate organ involvement and disease progression.

- Advancements in imaging modalities, such as high-resolution MRI and contrast-enhanced ultrasound, are improving diagnostic precision.

- Growing integration of imaging diagnostics in personalized treatment plans for connective tissue diseases is driving connective tissue disease market demand.

- Increased access to advanced imaging technologies in emerging economies is expected to propel trends in this segment.

By Treatment:

Based on treatment, the market is segmented into anti-inflammatory drugs, disease-modifying antirheumatic drugs (DMARDs), biologic therapies, immunosuppressive therapies, and surgery.

The biological therapies segment accounted for the largest revenue in the connective tissue disease market share in 2024.

- Biologic therapies targeting specific immune pathways, such as TNF inhibitors and IL-6 inhibitors, are revolutionizing connective tissue disease treatment.

- Increasing adoption of biologics for refractory cases and severe disease manifestations is driving this segment's dominance.

- Ongoing clinical trials and new product approvals in the biologics space are further supporting trends in this segment.

- Rising trends for personalized medicine and advancements in biologic drug delivery systems are boosting market expansion.

The immunosuppressive therapies segment is anticipated to register the fastest CAGR during the forecast period.

- Immunosuppressive therapies remain critical for managing severe and refractory cases of connective tissue diseases.

- Growing use of newer immunosuppressive agents with improved safety and efficacy profiles is driving demand.

- Increasing focus on combination therapies integrating immunosuppressants with biologics is enhancing treatment outcomes.

- Rising awareness among patients and healthcare providers about advanced immunosuppressive options is expected to propel growth.

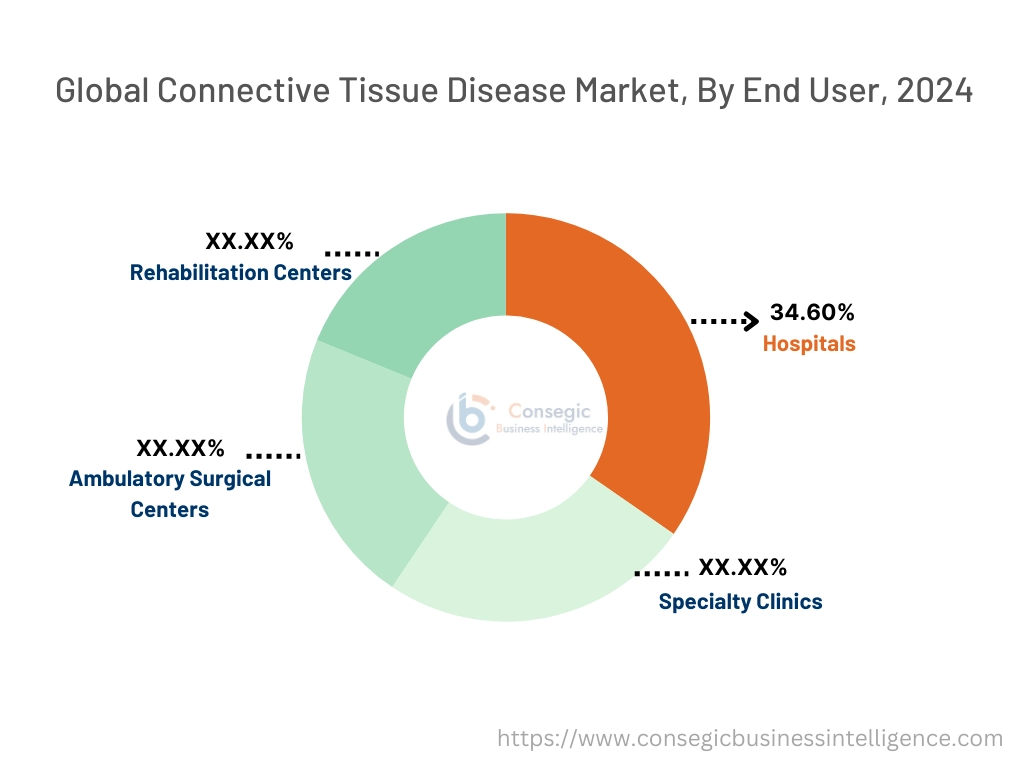

By End-User:

Based on end-users, the market is segmented into hospitals, specialty clinics, ambulatory surgical centers, and rehabilitation centers.

The hospitals segment accounted for the largest revenue share of 34.60% in 2024.

- Hospitals are primary centers for the diagnosis and management of complex connective tissue diseases, offering multidisciplinary care.

- Availability of advanced diagnostic tools, such as imaging and laboratory facilities, supports the dominance of hospital settings.

- Rising hospital admissions for severe and acute manifestations of connective tissue diseases are driving connective tissue disease market trends in this segment.

- Increasing investments in hospital infrastructure and the establishment of autoimmune disease centers are further supporting growth.

The specialty clinics segment is anticipated to register the fastest CAGR during the forecast period.

- Specialty clinics focusing on rheumatology and autoimmune diseases provide personalized care for connective tissue disease patients.

- Increasing patient preference for outpatient care in specialized settings is driving connective tissue disease market demand for specialty clinics.

- Expansion of clinic networks in urban and semi-urban areas is improving access to advanced care.

- Collaboration between specialty clinics and pharmaceutical companies to offer advanced therapies is expected to propel connective tissue disease market growth.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

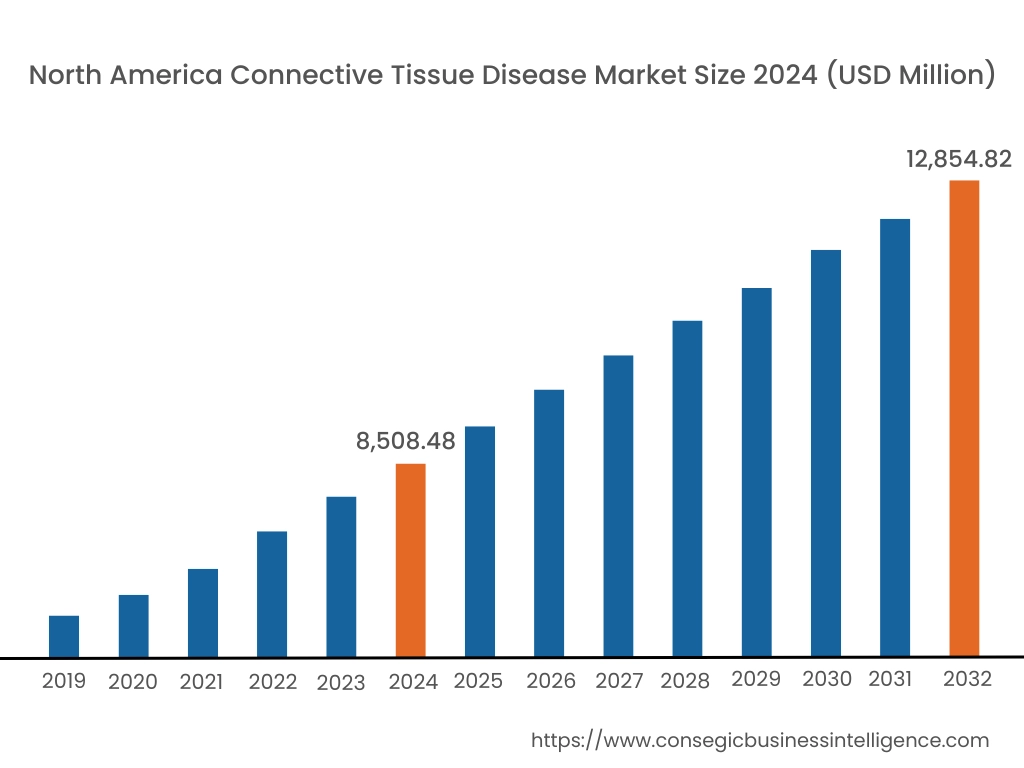

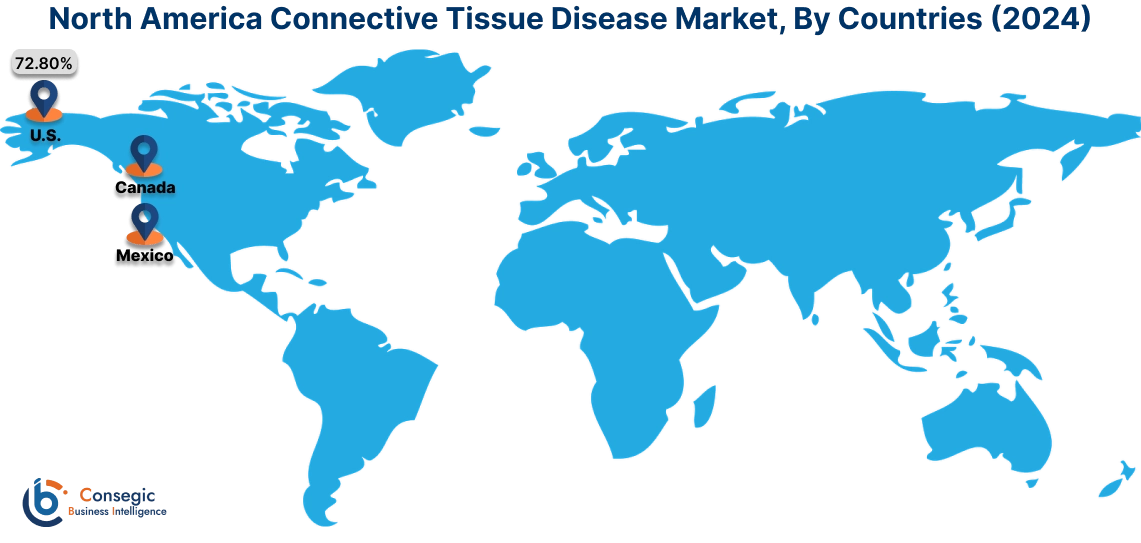

In 2024, North America was valued at USD 8,508.48 Million and is expected to reach USD 12,854.82 Million in 2032. In North America, the U.S. accounted for the highest share of 72.80% during the base year of 2024. North America holds a significant share in the global connective tissue disease market, driven by advanced healthcare infrastructure, high awareness about autoimmune and connective tissue disorders, and increasing prevalence of diseases such as rheumatoid arthritis, lupus, and scleroderma. The U.S. dominates the region with strong investments in research and development, widespread availability of biologics and advanced therapies, and robust diagnostic capabilities. As per the connective tissue disease market analysis, Canada contributes to the rising adoption of early diagnostic tools and expanding access to biologic treatments for managing connective tissue diseases. However, the high cost of therapies and disparities in access to specialized care may pose challenges.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 6.0% over the forecast period. The connective tissue disease market analysis is fueled by rising awareness of autoimmune disorders, improving healthcare infrastructure, and increasing adoption of advanced therapies in China, India, and Japan. China dominates the region with a growing demand for biologics and disease-modifying antirheumatic drugs (DMARDs) to manage diseases like lupus and rheumatoid arthritis. India’s expanding healthcare sector supports trends for cost-effective treatments, particularly for managing scleroderma and Sjögren’s syndrome. Japan emphasizes precision medicine and innovative therapies, leveraging its strong pharmaceutical industry and focus on early diagnosis. However, limited awareness in rural areas and affordability challenges may hinder connective tissue disease market expansion in some parts of the region.

Europe is a prominent market for connective tissue diseases, supported by a growing aging population, increasing prevalence of autoimmune disorders, and robust healthcare systems. Countries like Germany, France, and the UK are key contributors. Germany leads with advanced diagnostic facilities and a focus on personalized medicine for autoimmune diseases. France emphasizes public health initiatives to improve access to biologics and corticosteroids for managing connective tissue disorders. The UK is witnessing increasing adoption of research-driven therapies, including immunomodulators and targeted biologics. However, long waiting times and budget constraints in public healthcare systems may limit timely access to treatment.

The Middle East & Africa region is witnessing steady growth in the connective tissue disease market, driven by increasing investments in healthcare infrastructure and the rising prevalence of autoimmune disorders. Countries like Saudi Arabia and the UAE are adopting advanced diagnostic tools and biological therapies for managing diseases like systemic lupus erythematosus (SLE) and rheumatoid arthritis. In Africa regional analysis, South Africa is emerging as a key market, focusing on improving access to affordable medications and raising awareness about connective tissue disorders through public health initiatives. However, limited healthcare infrastructure in many parts of the region may restrict broader market development.

Latin America is an emerging market for connective tissue disease treatments, with Brazil and Mexico leading the region. Brazil’s growing healthcare sector and increasing prevalence of autoimmune diseases drive trends for advanced diagnostics and biological therapies. Mexico focuses on expanding access to DMARDs and biologics for managing rheumatoid arthritis and lupus. The region is also investing in awareness programs and collaborations with international healthcare organizations to enhance care for connective tissue diseases. However, economic instability and inconsistent healthcare infrastructure may pose challenges to market growth in smaller economies.

Top Key Players and Market Share Insights:

The connective tissue disease market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the connective tissue disease market. Key players in the connective tissue disease industry include -

- Pfizer Inc. (United States)

- Novartis AG (Switzerland)

- Johnson & Johnson (United States)

- AbbVie Inc. (United States)

- Amgen Inc. (United States)

- Hoffmann-La Roche AG (Switzerland)

- Sanofi S.A. (France)

- Bristol Myers Squibb (United States)

- Eli Lilly and Company (United States)

- GlaxoSmithKline plc (United Kingdom)

Recent Industry Developments:

Approvals:

- In May 2024, the FDA approved subcutaneous belimumab for pediatric patients aged 5 years and older with systemic lupus erythematosus (SLE), expanding treatment options for younger populations.

- In April 2024, the U.S. FDA granted Fast Track Designation to Telitacicept, developed by RemeGen Co., Ltd., for treating Primary Sjögren's Syndrome, potentially accelerating its development and review process.

Connective Tissue Disease Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 39,663.12 Million |

| CAGR (2025-2032) | 5.6% |

| By Type |

|

| By Diagnosis |

|

| By Treatment |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected size of the Connective Tissue Disease Market by 2032? +

Connective Tissue Disease Market size is estimated to reach over USD 39,663.12 Million by 2032 from a value of USD 25650.48 Million in 2024 and is projected to grow by USD 26,629.86 Million in 2025, growing at a CAGR of 5.6% from 2025 to 2032.

What drives the growth of the Connective Tissue Disease Market? +

Key growth drivers include the rising prevalence of autoimmune disorders like lupus and rheumatoid arthritis, advancements in biological therapies, and increasing awareness about early diagnosis and treatment options for chronic conditions.

What are the major challenges in this market? +

Limited awareness about connective tissue diseases and delayed diagnosis due to non-specific symptoms pose significant challenges, particularly in underserved regions with insufficient healthcare infrastructure.

Which segment dominates the market by type? +

The Systemic Lupus Erythematosus (SLE) segment holds the largest share due to its prevalence and the demand for advanced diagnostic and therapeutic solutions.

Which segment is expected to grow the fastest? +

The Dermatomyositis segment is anticipated to register the fastest CAGR, driven by advancements in targeted therapies and growing awareness among healthcare providers and patients.