- Summary

- Table Of Content

- Methodology

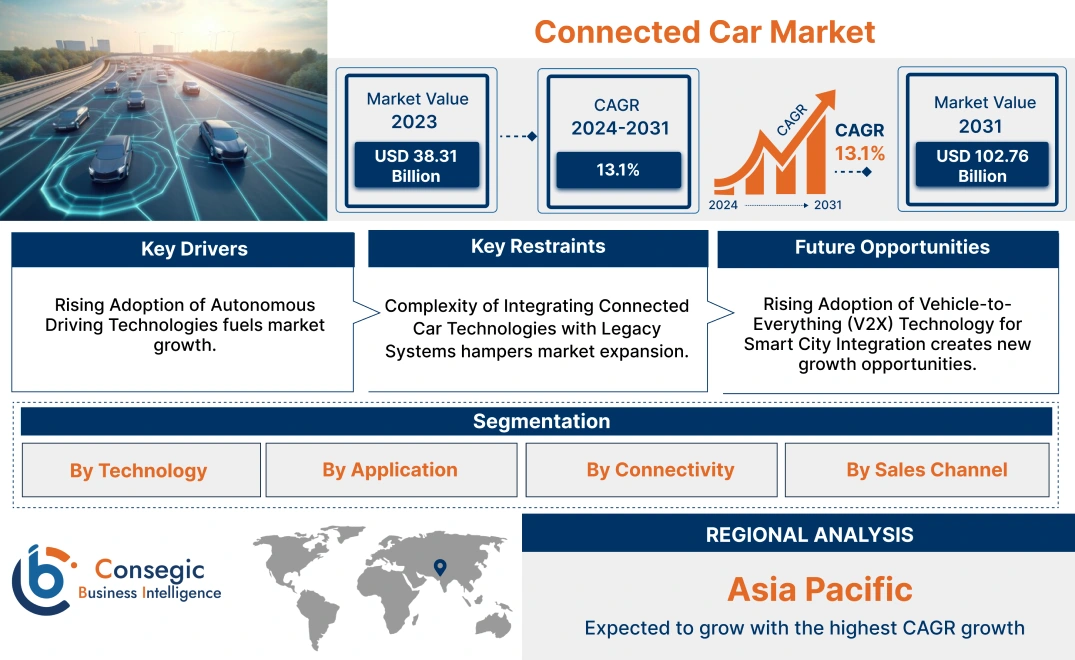

Connected Car Market Size:

Connected Car Market size is estimated to reach over USD 102.76 Billion by 2031 from a value of USD 38.31 Billion in 2023 and is projected to grow by USD 42.65 Billion in 2024, growing at a CAGR of 13.1% from 2024 to 2031.

Connected Car Market Scope & Overview:

Connected cars are vehicles equipped with internet access and advanced communication systems that allow real-time data exchange between the vehicle, its surroundings, and the driver. These cars utilize sensors, software, and cloud connectivity to offer features like navigation, entertainment, vehicle-to-vehicle (V2V) communication, and vehicle-to-everything (V2X) communication. Connected car technology enhances the driving experience by providing features such as real-time traffic updates, remote diagnostics, and advanced safety measures, improving both convenience and vehicle performance.

The increasing demand for enhanced driving experiences, coupled with advancements in automotive technology and the growing adoption of the Internet of Things (IoT), is driving the development of the connected car market. This market progress is further supported by regulatory initiatives promoting vehicle safety and the integration of advanced driver assistance systems (ADAS). The rise of autonomous vehicles and electric vehicles is also contributing to the increased adoption of connected car solutions.

Key end-users of connected car technology include automotive manufacturers, fleet operators, and mobility service providers. As the automotive industry focuses on developing smart, safe, and efficient vehicles, the need for connected car technology is expected to grow, driven by the need for enhanced safety, better user experiences, and seamless connectivity.

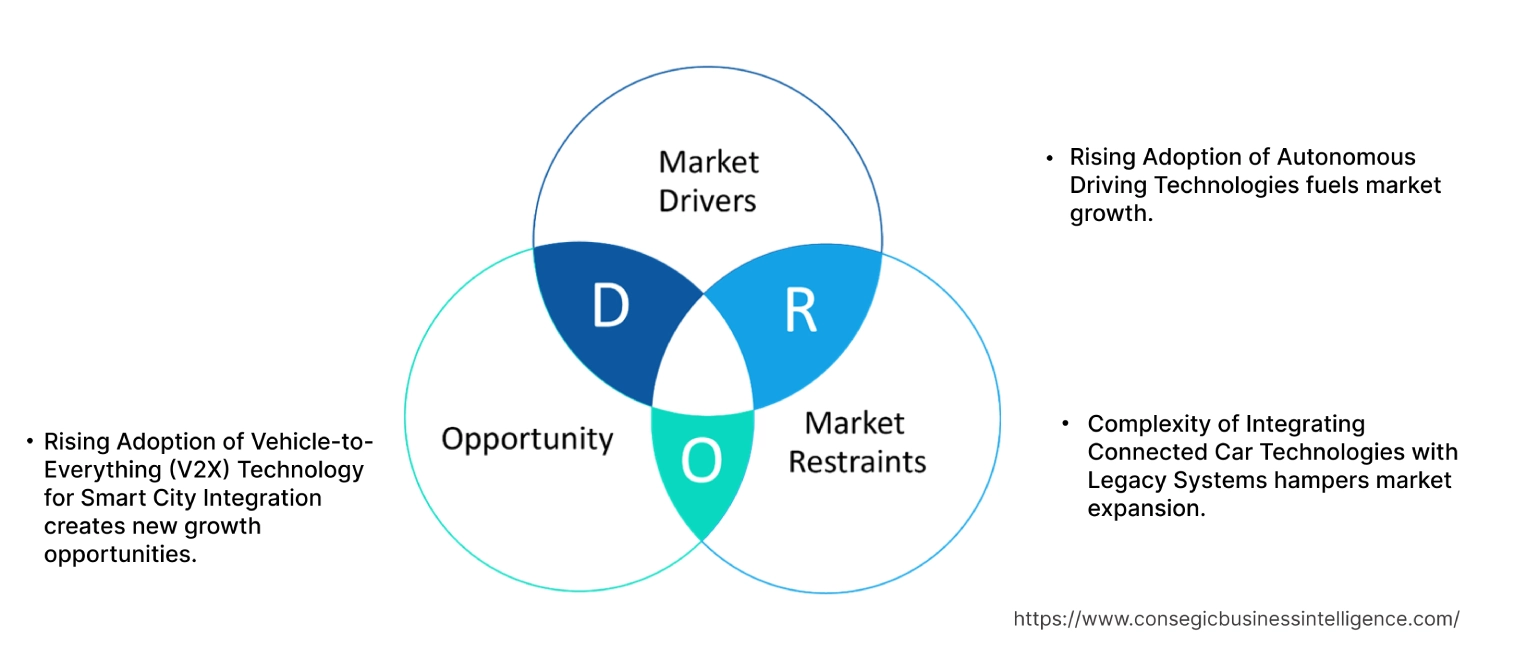

Connected Car Market Dynamics - (DRO) :

Key Drivers:

Rising Adoption of Autonomous Driving Technologies fuels market growth.

The increasing adoption of autonomous driving technologies is a significant driver in the connected car market. As the automotive industry progresses toward higher levels of vehicle autonomy (Level 3 and above), the requirement for robust connectivity solutions has intensified. Autonomous vehicles rely on real-time data from various sources, including sensors, cameras, radar systems, and V2X communication, to make informed driving decisions. High-speed, low-latency networks are crucial for enabling real-time decision-making, enhancing safety, and optimizing vehicle performance. The shift toward autonomous driving is pushing automakers and technology providers to develop advanced connectivity platforms that support seamless data transmission between vehicles, infrastructure, and cloud services. This trend is expected to accelerate as regulatory bodies in key markets, such as the U.S. and Europe, introduce frameworks to support the deployment of autonomous vehicles, further driving the connected car market growth.

Key Restraints :

Complexity of Integrating Connected Car Technologies with Legacy Systems hampers market expansion.

The integration of connected car technologies with existing legacy automotive systems poses a significant constraint for automakers. A large portion of the vehicles currently in use were not originally engineered for connectivity, creating complexities when attempting to retrofit modern connected features. This difficulty is further exacerbated by the need to seamlessly integrate new software and hardware components into established vehicle platforms without compromising safety, performance, or regulatory compliance. The substantial costs and technical hurdles involved in this integration process often hinder the pace of adoption, especially for smaller automakers and companies with constrained R&D budgets. Thus, the limited ability to implement advanced connected car technologies at scale, hinders the connected car market demand.

Future Opportunities :

Rising Adoption of Vehicle-to-Everything (V2X) Technology for Smart City Integration creates new growth opportunities.

The increasing adoption of Vehicle-to-Everything (V2X) technology in the context of smart city initiatives offers a substantial opportunity for the connected car market. V2X technology, encompassing Vehicle-to-Infrastructure (V2I), Vehicle-to-Vehicle (V2V), and Vehicle-to-Pedestrian (V2P) communication, is essential for creating safer, more efficient urban mobility systems. Smart cities are incorporating V2X-enabled traffic management systems to optimize traffic flow, reduce congestion, and improve road safety. For instance, V2I communication allows connected vehicles to interact with traffic signals and road infrastructure, enabling adaptive traffic control and real-time navigation updates. The deployment of V2X technology aligns with government initiatives focused on reducing urban traffic congestion and emissions, making it a critical component of future urban mobility solutions. As more cities invest in smart infrastructure, the demand for connected vehicles equipped with V2X capabilities is expected to rise, driving connected car market opportunities.

Connected Car Market Segmental Analysis :

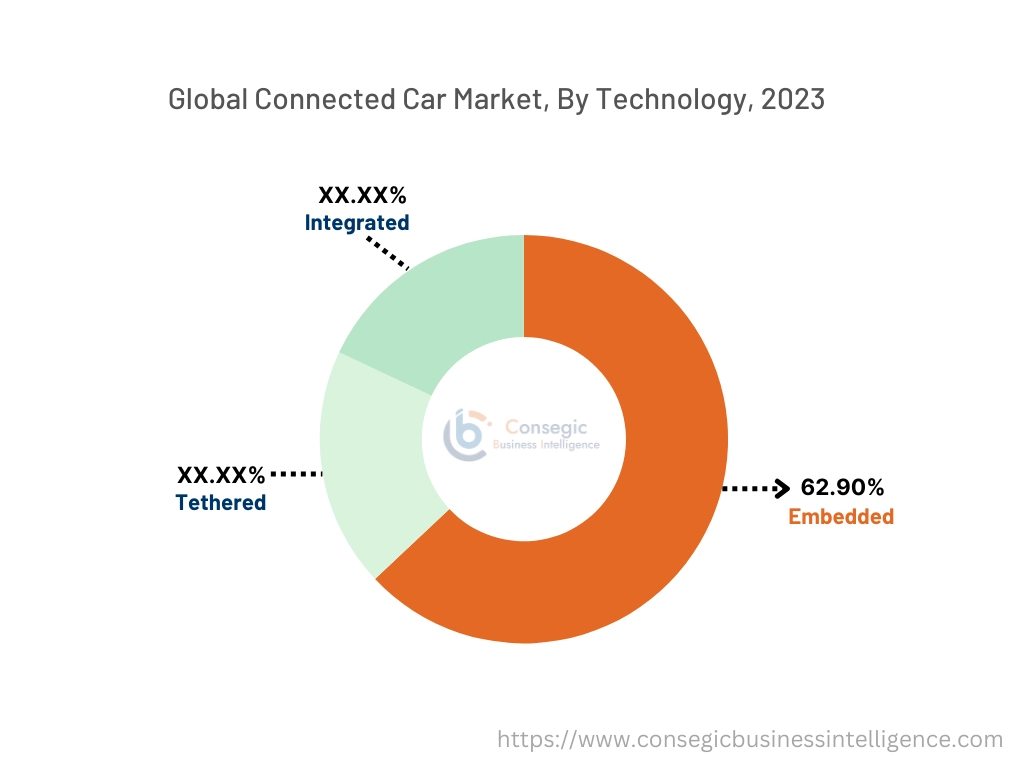

By Technology:

Based on technology, the connected car market is segmented into embedded, tethered, and integrated systems.

The embedded segment accounted for the largest revenue of 62.90% in 2023.

- Embedded systems are integrated directly by OEMs, providing reliable, factory-installed connectivity solutions.

- These systems are designed for enhanced safety features, real-time diagnostics, and seamless network integration.

- Regulatory mandates like eCall in Europe have driven the adoption of embedded systems in connected vehicles.

- The evolution of 5G technology is further enhancing the capabilities of embedded systems, supporting their dominance in the market.

- Embedded systems lead the market due to their seamless integration and compliance with regulatory requirements, making them the preferred choice for OEMs.

- As per segmental trends analysis, the embedded systems segment boosts the connected car market expansion.

The integrated segment is anticipated to register the fastest CAGR during the forecast period.

- Integrated systems connect users' smartphones to the vehicle's infotainment system, allowing access to various apps and services.

- These systems are popular for their flexibility, leveraging existing mobile connectivity without the need for additional data plans.

- The growing adoption of platforms like Apple CarPlay and Android Auto is driving the rapid development of integrated systems.

- Consumer demand for a personalized, connected experience in vehicles is contributing to the increased adoption of integrated systems.

- Integrated systems are expected to grow rapidly due to their user-friendly features and enhanced connectivity, aligning with consumer preferences.

- Therefore, as per the connected car market analysis, the integrated segment boosts the market progress.

By Application:

Based on application, the market is segmented into navigation, infotainment, telematics, safety & security, and others.

The infotainment segment accounted for the largest revenue share of the total connected car market share in 2023.

- Infotainment systems combine entertainment and information features, offering services such as music streaming, navigation, and internet browsing.

- The increasing requirement for a seamless digital experience in vehicles is driving the adoption of infotainment systems.

- Infotainment has become a standard feature in new vehicles, enhancing user experience and serving as a differentiator for automakers.

- Advanced voice recognition and AI-driven assistants integrated into infotainment systems are further fueling the segment's progress.

- Infotainment leads the market due to rising consumer needs for enhanced in-car connectivity and entertainment features.

- Therefore, as per the segmental trends analysis, the infotainment segment boosts the connected car market expansion.

The telematics segment is anticipated to register the fastest CAGR during the forecast period.

- Telematics systems provide vehicle connectivity solutions like fleet management, vehicle tracking, and emergency services.

- Increasing adoption in both passenger and commercial vehicles for real-time data and safety enhancements is driving this segment.

- Regulatory requirements for emergency response systems are further propelling the need for telematics solutions.

- The integration of telematics with V2X communication technologies is boosting its growth in connected car applications.

- Telematics is expected to grow rapidly, driven by rising requirements for real-time vehicle data and regulatory compliance.

- Therefore, as per the segmental trends analysis, the telematics segment boosts the market progression.

By Connectivity:

Based on connectivity, the market is segmented into vehicle-to-vehicle (V2V), vehicle-to-infrastructure (V2I), and vehicle-to-everything (V2X).

The vehicle-to-everything (V2X) segment accounted for the largest revenue share in 2023.

- V2X connectivity includes communication between vehicles, infrastructure, pedestrians, and other entities.

- It is critical for enabling advanced driver assistance systems (ADAS) and autonomous driving features.

- Deployment of 5G networks supports V2X with low latency and high bandwidth for efficient data transmission.

- Increasing smart city projects and traffic management systems are driving the adoption of V2X technologies.

- V2X dominates the market due to its comprehensive communication capabilities, essential for ADAS and autonomous driving.

- Therefore, due to the versatility of V2X to provide several features it boosts the market demand.

The vehicle-to-infrastructure (V2I) segment is anticipated to register the fastest CAGR during the forecast period.

- V2I focuses on communication between vehicles and roadside infrastructure like traffic signals and sensors.

- It improves traffic flow, reduces congestion, and enhances road safety through real-time data exchange.

- Growing investment in intelligent transportation systems is driving the need for V2I connectivity solutions.

- As urban areas develop smart traffic management initiatives, the adoption of V2I technologies is expected to increase significantly.

- V2I is set to grow rapidly, supported by the development of smart transportation infrastructure and increasing investments in road safety.

- Therefore, the vehicle-to-infrastructure (V2I) segment fuels the market development.

By Sales Channel:

Based on the sales channel, the connected car market is segmented into OEM (Original Equipment Manufacturer) sales and aftermarket.

The OEM sales segment accounted for the largest revenue share in 2023.

- OEM sales include vehicles with pre-installed connected features directly from the manufacturer.

- These vehicles come with factory-integrated systems for infotainment, telematics, navigation, and safety, providing seamless connectivity and advanced features.

- OEMs have a strong focus on delivering comprehensive, integrated solutions that cater to consumer needs for high-quality, reliable connectivity.

- The increasing trend of connected and autonomous vehicles, along with the regulatory push for enhanced safety features, is driving OEM sales.

- Direct sales through authorized dealerships also contribute to the dominance of OEM sales, as dealerships offer tailored financing options and personalized services.

- The OEM sales channel leads the market, driven by its ability to provide factory-installed, high-quality connected solutions, meeting the growing requirements for advanced in-car connectivity.

- Therefore, as per the segmental trends analysis, the OEM sales segment boosts the market demand.

The aftermarket segment is anticipated to register the fastest CAGR during the forecast period.

- The aftermarket includes the sale of connected car solutions and upgrades, such as infotainment systems, telematics devices, and connectivity modules, for vehicles that were not originally equipped with these features.

- Increasing consumer interest in retrofitting existing vehicles with advanced connectivity features is driving growth in the aftermarket segment.

- Independent retailers, specialty stores, and online platforms offer a wide variety of aftermarket products, providing consumers with flexible and cost-effective upgrade options.

- The rising popularity of plug-and-play devices and smartphone-based connectivity applications is further boosting the adoption of aftermarket solutions.

- The availability of a wide range of products and the trend towards enhancing vehicle connectivity without purchasing new cars are contributing to the rapid growth of the aftermarket segment.

- The aftermarket segment is expected to grow rapidly, driven by the demand for flexible, cost-effective solutions for upgrading connectivity in older vehicles.

- Therefore, as per the connected car market trends, the aftermarket segment boosts the market progression.

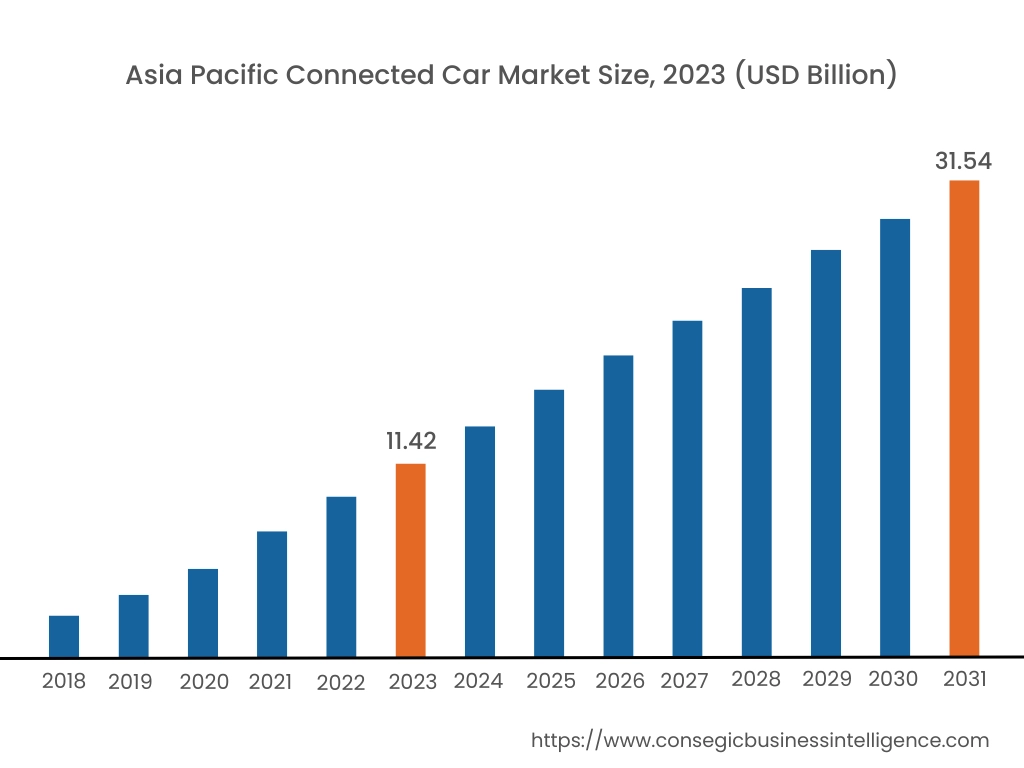

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

Asia Pacific region was valued at USD 11.42 Billion in 2023. Moreover, it is projected to grow by USD 12.75 Billion in 2024 and reach over USD 31.54 Billion by 2031. Out of which China accounted for 29.4% share in 2023. Asia-Pacific is witnessing rapid progress in the connected car market, driven by increasing automotive production, rising disposable incomes, and rapid urbanization in countries like China, Japan, and India. The growing requirement for enhanced in-car connectivity, navigation services, and real-time traffic information contributes to market progression. Government initiatives supporting smart city projects and the development of 5G infrastructure further bolster market growth.

North America is estimated to reach over USD 36.17 Billion by 2031 from a value of USD 13.39 Billion in 2023 and is projected to grow by USD 14.91 Billion in 2024. This region holds a substantial share of the connected car market, primarily due to a well-established automotive industry and high consumer adoption rates of advanced technologies. The United States, in particular, has a significant market presence, with major automotive manufacturers and tech companies investing heavily in connected vehicle technologies. The demand for features such as in-car infotainment, telematics, and advanced driver-assistance systems (ADAS) propels market growth.

Europe represents a significant portion of the global connected car market, with countries like Germany, the UK, and France leading in terms of adoption and innovation. The region benefits from strong government support for smart transportation initiatives and stringent safety regulations, which drive the integration of connected technologies in vehicles. The focus on reducing emissions and enhancing road safety further accelerates the adoption of connected car solutions.

The Middle East & Africa region shows promising potential in the connected car market, particularly in countries like the UAE, Saudi Arabia, and South Africa. Increasing investments in smart infrastructure, a growing automotive market, and a tech-savvy population drive the need for connected vehicles. The expanding tourism sector, particularly in the UAE, where high-quality transportation services are offered, further supports market development.

Latin America is an emerging market for connected cars, with Brazil and Mexico being the primary growth drivers. The rising adoption of smartphones, improving internet connectivity, and increasing focus on enhancing road safety contribute to the market's development. Government initiatives aimed at modernizing transportation infrastructure and promoting the adoption of advanced automotive technologies support market progress.

Top Key Players & Market Share Insights:

The Connected car market is highly competitive with major players providing connected car services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global connected car market. Key players in the connected car industry include –

- Continental AG (Germany)

- Robert Bosch GmbH (Germany)

- Harman International (USA)

- Airbiquity Inc. (USA)

- Visteon Corporation (USA)

- Denso Corporation (Japan)

- Tesla, Inc. (USA)

- General Motors Company (USA)

- Qualcomm Technologies, Inc. (USA)

- AT&T Inc. (USA)

Recent Industry Developments :

Partnerships & Collaborations:

- In October 2024, Kia India partnered with Airtel Business to introduce the Kia Connect 2.0 experience, enhancing in-car connectivity for customers. Airtel's IoT solutions will power Kia's connected car features, providing a seamless and secure network experience. This collaboration enables advanced telematics, real-time updates, and better safety features for Kia's vehicles, ensuring an improved user experience for customers.

- In September 2024, Samsung Electronics partnered with Hyundai Motor and Kia to expand the SmartThings ecosystem into software-defined vehicles (SDVs). This collaboration will integrate SmartThings into Hyundai and Kia cars, allowing seamless control of connected home devices from the vehicle. It also enhances in-car experiences by offering real-time data, enabling drivers to manage home appliances and receive updates about their surroundings. This initiative is part of Samsung's broader push to build an interconnected smart living ecosystem.

- In April 2024, HARMAN Automotive and Tata Motors expanded their decade-long partnership by introducing the HARMAN Ignite platform in Tata passenger vehicles. This platform enables a suite of connected services, enhancing the in-car experience with features like real-time vehicle diagnostics, over-the-air updates, and a customizable interface for drivers. The collaboration aims to bring more advanced and intuitive connectivity solutions to Tata's vehicles, marking a significant step in their shared commitment to innovation.

Product Launch:

- In April 2024, Panasonic launched its Cirrus platform which enhances roadway intelligence through two-way communication between vehicles and traffic operators. The platform provides real-time data insights, helping operators make informed decisions to improve traffic flow and safety. It supports connected vehicle ecosystems, offering critical information such as road conditions and traffic incidents, and enables seamless updates to drivers. This version strengthens the capability to manage traffic efficiently, improving overall roadway infrastructure.

Connected Car Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 102.76 Billion |

| CAGR (2024-2031) | 13.1% |

| By Technology |

|

| By Application |

|

| By Connectivity |

|

| By Sales Channel |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the connected car market? +

Connected Car Market size is estimated to reach over USD 102.76 Billion by 2031 from a value of USD 38.31 Billion in 2023 and is projected to grow by USD 42.65 Billion in 2024, growing at a CAGR of 13.1% from 2024 to 2031.

What specific segmentation details are covered in the Connected Car Market report? +

The connected car market report includes segmentation details for technology, application, connectivity, sales channel, and region.

Which is the fastest-growing segment in the connectivity type in the connected car market? +

According to the analysis, vehicle-to-infrastructure (VTI) is the fastest-growing segment in the connected car market due to its ability to reduce congestion and road safety.

Who are the major players in the connected car Market? +

The key players in the connected car market are Continental AG (Germany), Robert Bosch GmbH (Germany), Harman International (USA), Airbiquity Inc. (USA), Visteon Corporation (USA), Denso Corporation (Japan), Tesla, Inc. (USA), General Motors Company (USA), Qualcomm Technologies, Inc. (USA) and AT&T Inc. (USA).