- Summary

- Table Of Content

- Methodology

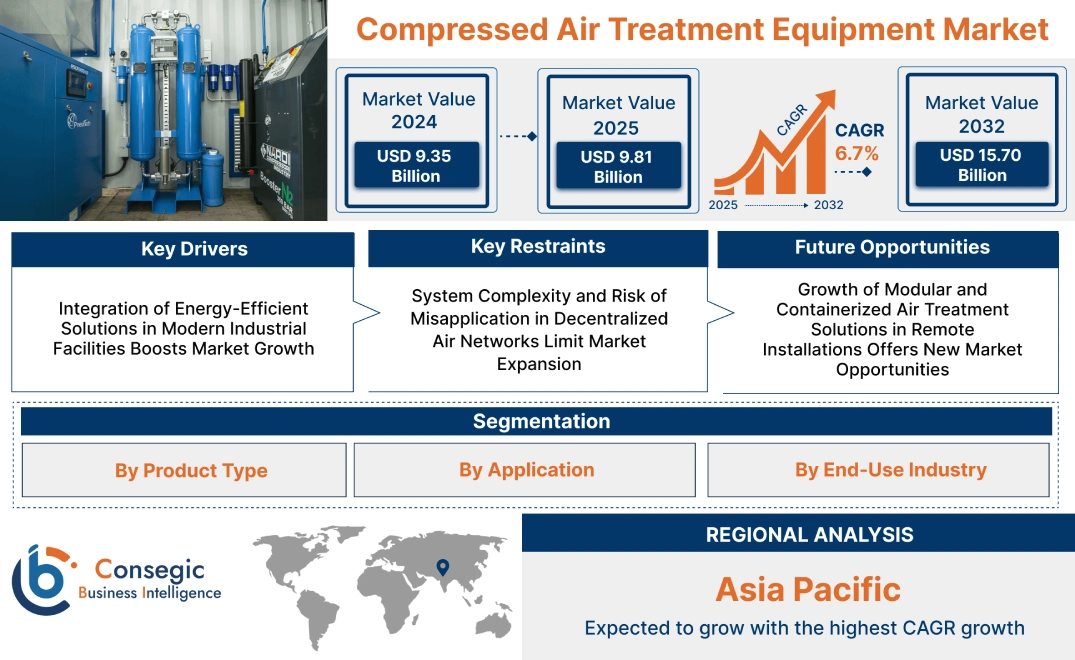

Compressed Air Treatment Equipment Market Size:

Compressed Air Treatment Equipment Market size is estimated to reach over USD 15.70 Billion by 2032 from a value of USD 9.35 Billion in 2024 and is projected to grow by USD 9.81 Billion in 2025, growing at a CAGR of 6.7% from 2025 to 2032.

Compressed Air Treatment Equipment Market Scope & Overview:

Compressed air treatment equipment is used to remove contaminants such as moisture, oil, and particulates from compressed air systems, ensuring clean, dry air for industrial and commercial applications. This equipment includes filters, dryers, separators, and drain valves, each designed to protect sensitive machinery, improve efficiency, and maintain process integrity.

Key features include high filtration precision, corrosion resistance, and integration with automated monitoring systems. These systems ensure consistent air quality, lower maintenance costs, and prolong the lifespan of downstream equipment. The modular design enables scalability and customization to meet various operational requirements across diverse industries.

Manufacturers, food processors, automotive plants, and pharmaceutical facilities utilize these solutions to meet regulatory standards and optimize performance. Their reliability in critical environments and compatibility with various compressor systems support smooth operations and minimal downtime, making them essential in maintaining production quality and protecting pneumatic instruments and systems.

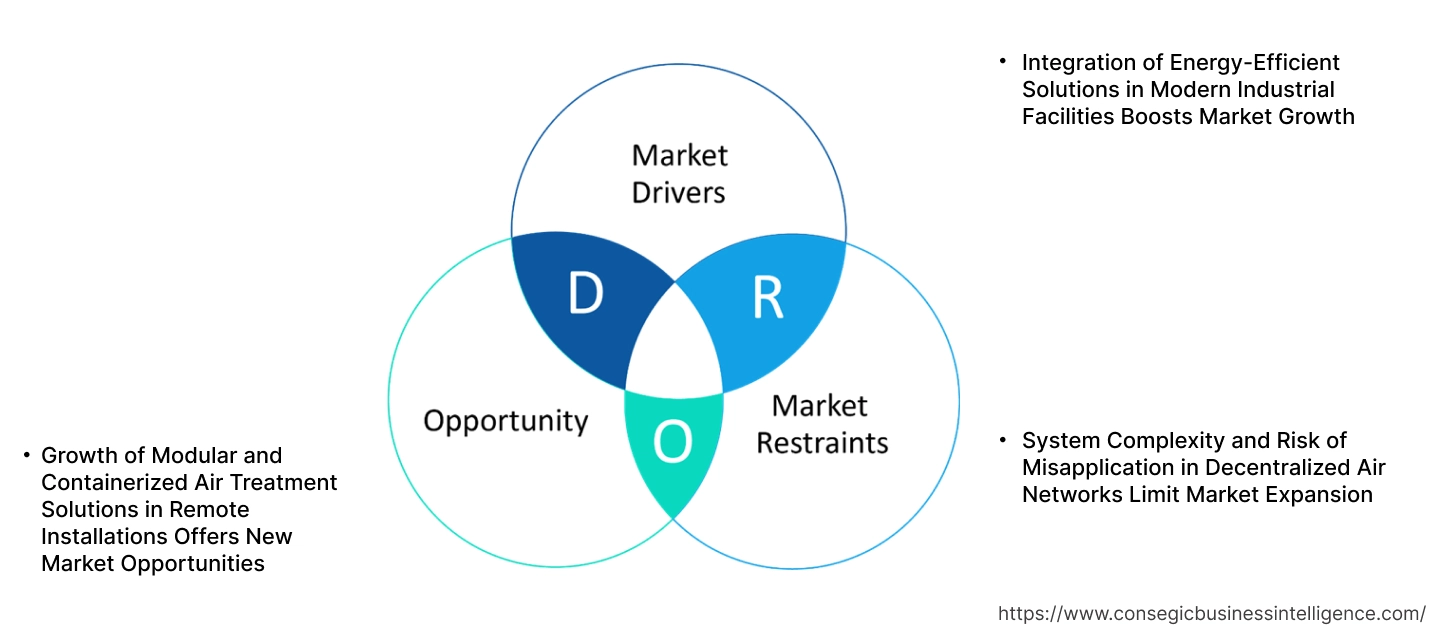

Compressed Air Treatment Equipment Market Dynamics - (DRO) :

Key Drivers:

Integration of Energy-Efficient Solutions in Modern Industrial Facilities Boosts Market Growth

Industrial operators are increasingly focused on lowering energy consumption and reducing the total cost of ownership across compressed air systems. Energy-efficient innovations such as variable speed drives, dew point-dependent dryer controls, and integrated heat recovery modules are being widely implemented. These technologies optimize performance under fluctuating load conditions, reduce power draw, and support carbon reduction goals aligned with ISO 50001 frameworks. In facilities where compressed air accounts for a substantial portion of energy use, adopting high-efficiency treatment systems significantly improves operational economics. Manufacturers are also integrating advanced controls to ensure precise moisture removal without over-drying, further improving energy utilization. This trend is especially prominent in sectors like automotive, metal fabrication, and electronics, where continuous uptime and performance reliability are essential. The alignment of air treatment with corporate sustainability mandates is fueling equipment upgrades and driving compressed air system modernization.

- For instance, in 2022, O’Neill Industrial announced a €150 million investment for a new filtration manufacturing facility in collaboration with Tandem Project Management. This net-zero factory aims to balance its carbon footprint by reducing greenhouse gas emissions through cutting-edge energy efficiency measures, the integration of renewable energy, and carbon offsetting initiatives by implementing a highly efficient, sustainable compressed air system. The design was conducted as per the EU Energy Performance of Buildings Directive and the Energy Efficiency Directives, ensuring that the installation met the highest standards for energy conservation.

Thus, these advancements are contributing to the compressed air treatment equipment market expansion.

Key Restraints:

System Complexity and Risk of Misapplication in Decentralized Air Networks Limit Market Expansion

Large manufacturing plants often operate multiple air supply zones, each with distinct pressure and moisture control requirements. Integrating air treatment systems into decentralized networks presents engineering challenges due to fluctuating demand profiles, pressure drops, and ambient condition variability. If components such as filters, dryers, or separators are improperly sized or installed without system-wide analysis, the result is inconsistent air quality, reduced tool efficiency, and preventable maintenance costs. Operators lacking specialized expertise in this equipment frequently misconfigure it, leading to suboptimal performance. Additionally, facility managers may underestimate the importance of treating air close to the point of use, resulting in contamination risks and premature equipment wear. This operational complexity discourages investment, especially in older plants or cost-sensitive segments. The absence of a standardized system planning and limited technical guidance restricts effective deployment, acting as a barrier to compressed air treatment equipment market growth.

Future Opportunities :

Growth of Modular and Containerized Air Treatment Solutions in Remote Installations Offers New Market Opportunities

Remote industrial operations such as mining, infrastructure development, and oilfield services require reliable compressed air systems that are compact, easily deployable, and low-maintenance. Modular and containerized air treatment solutions are designed for these off-grid or mobile applications, offering pre-assembled units with integrated filtration, drying, and control systems. These solutions reduce installation time, minimize the need for skilled on-site technicians, and ensure stable performance under variable environmental conditions. Their transportable design allows easy relocation between job sites, enhancing utility across temporary or project-based operations. As remote construction and energy exploration activities increase globally, the need for self-contained and adaptable air treatment systems is rising. These units are also being adopted in military logistics, disaster relief operations, and offshore platforms, where space and reliability are critical. The expanding utility of these systems across harsh and space-constrained environments is unlocking compressed air treatment equipment market opportunities driven by both demand and growth.

Compressed Air Treatment Equipment Market Segmental Analysis :

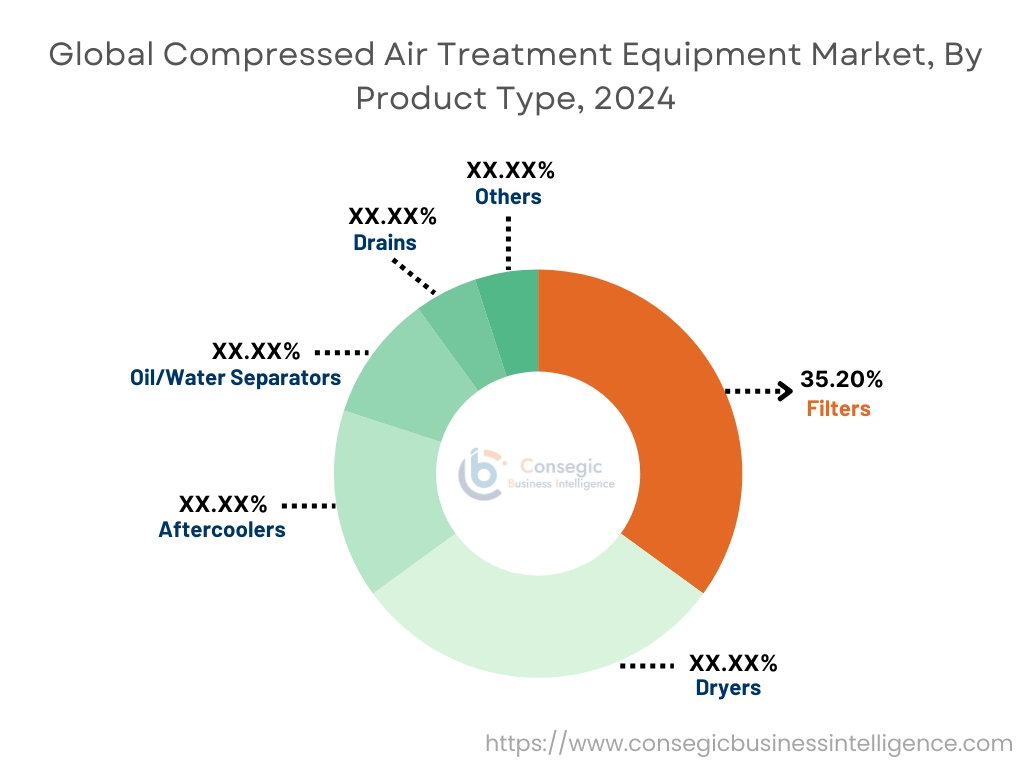

By Product Type:

Based on product type, the compressed air treatment equipment market is segmented into filters (particulate filter/pre-filter, coalescing filter/oil removal, activated carbon filter, filtered centrifugal separator, and others), dryers (refrigerated, desiccant, membrane), aftercoolers, oil/water separators, drains, and others.

The filters segment accounted for the largest compressed air treatment equipment market share of 35.2% in 2024.

- Coalescing filters and particulate pre-filters are essential in removing solid particles, oil aerosols, and water from compressed air, ensuring equipment longevity and product quality.

- Activated carbon filters further eliminate vapors and odors, especially in food, beverage, and pharmaceutical applications.

- Compressed air treatment equipment market analysis indicates strong replacement cycles and increased OEM integration of modular filtration units.

- The steady industrialization across developing economies sustains high filter need in assembly lines and critical manufacturing environments.

The dryers segment is projected to exhibit the fastest CAGR during the forecast period.

- Refrigerated dryers are commonly used across general-purpose industrial environments, while desiccant and membrane dryers are preferred in cleanroom, pharmaceutical, and instrumentation applications.

- Market trends highlight increased adoption of energy-efficient dryers compliant with ISO 8573 standards.

- Membrane-based technologies are seeing growth due to their compact footprint and ability to function without external power, driving requirement in mobile and remote installations.

- The rising need to minimize air moisture to protect sensitive downstream systems propels this segment’s contribution to compressed air treatment equipment market growth.

By Application:

Based on application, the market is segmented into plant air, instrument air, process air, breathing air, and others.

The plant air segment held the largest market share in 2024.

- It serves general industrial tasks including powering pneumatic tools, machinery, and cleaning operations.

- The ubiquity of plant air systems in discrete and process manufacturing sustains long-term volume consumption of treatment components.

- Compressed air treatment equipment market analysis shows that air quality classifications for plant operations continue to be upgraded, supporting stable product demand.

- Consistent retrofitting and system expansions further bolster the relevance of this segment.

The breathing air segment is projected to grow at the fastest CAGR during the forecast period.

- Applications in healthcare, pharmaceuticals, confined-space entry, and fire safety require purified, oil-free, and contaminant-free compressed air.

- Regulatory compliance with standards like OSHA and NFPA for breathable air accelerates specialized treatment equipment adoption.

- Compressed air treatment equipment market trends point to increasing demand for high-purity air systems in medical isolation wards and emergency response facilities.

- Furthermore, this segment is also driven by innovations in filtration and carbon absorption for personal protection systems.

By End-Use Industry:

Based on end-use industry, the compressed air treatment equipment market is segmented into manufacturing, food & beverage, pharmaceuticals, healthcare, chemicals & petrochemicals, energy & power, automotive, textile, aerospace & defense, electronics & semiconductors, and others.

Manufacturing emerged as the leading compressed air treatment equipment market share by revenue in 2024.

- Compressed air is vital to automation, pneumatic actuation, and cleaning systems across assembly lines.

- The shift toward lean manufacturing and predictive maintenance increases the emphasis on treated air systems.

- The market demand is reinforced by continuous industrial development across Asia-Pacific and Latin America.

- As per compressed air treatment equipment market trends, industrial players are investing in performance-optimized filtration and drying modules to reduce downtimes and energy waste.

The electronics & semiconductors segment is expected to experience the fastest CAGR.

- Ultra-clean air is essential in electronics manufacturing to avoid product defects and contamination.

- The rise of chip fabrication facilities and cleanroom expansions in the U.S., Taiwan, and South Korea fuels this segment.

- Segmental trends emphasize the need for membrane and desiccant dryers, coalescing filters, and zero-loss condensate drains in this domain.

- Precision airflow and moisture control contribute to segmental acceleration and long-term compressed air treatment equipment market expansion.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

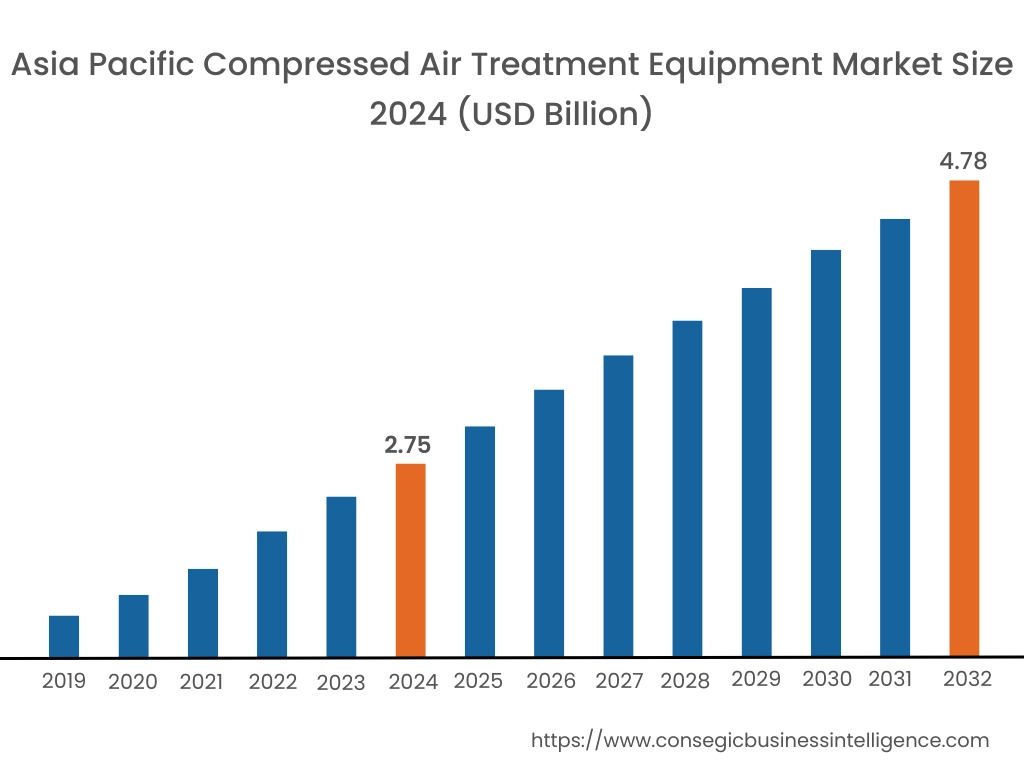

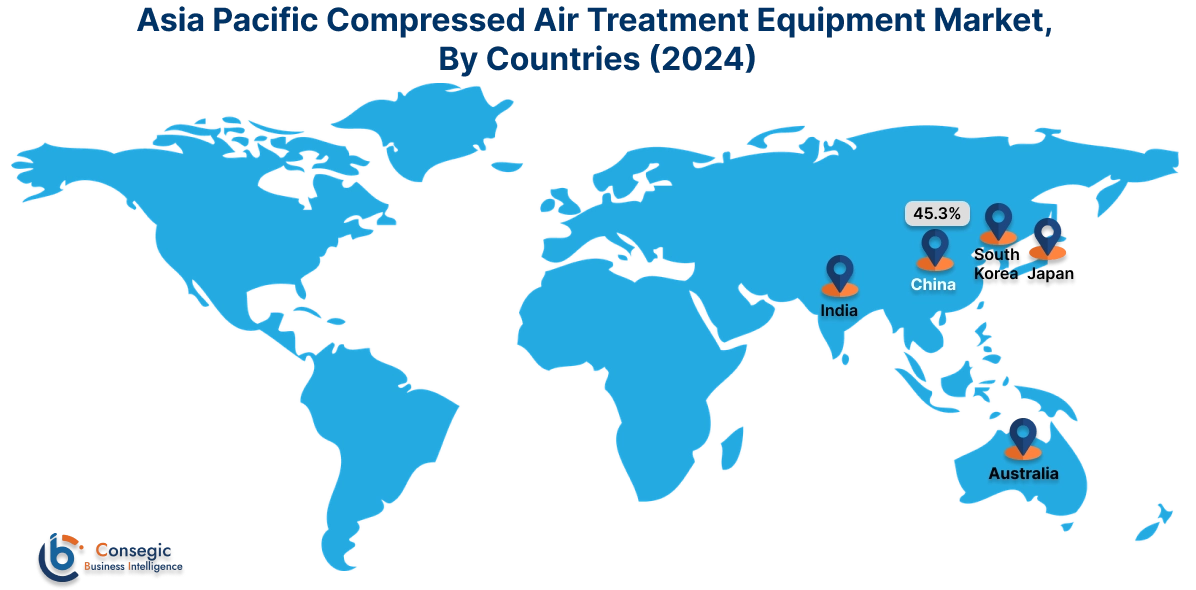

Asia Pacific region was valued at USD 2.75 Billion in 2024. Moreover, it is projected to grow by USD 2.90 Billion in 2025 and reach over USD 4.78 Billion by 2032. Out of this, China accounted for the maximum revenue share of 45.3%. Asia-Pacific is witnessing rapid growth in the compressed air treatment equipment industry, propelled by rapid industrialization, rising manufacturing output, and expansion of sectors such as semiconductors, textiles, and consumer electronics. China, India, Japan, and South Korea are undergoing robust infrastructure growth, increasing the need for clean and dry compressed air across facilities. Analysis highlights that localized production of cost-effective units and increasing government focus on industrial safety and environmental compliance are driving regional adoption. Additionally, expanding awareness of equipment longevity and energy-saving advantages among mid-sized manufacturers is accelerating requirement in both domestic and export-driven sectors.

North America is estimated to reach over USD 5.09 Billion by 2032 from a value of USD 3.10 Billion in 2024 and is projected to grow by USD 3.25 Billion in 2025. North America holds a significant share of the market, driven by its established industrial base and strict air quality regulations across sectors like pharmaceuticals, automotive, and aerospace. The United States and Canada exhibit high adoption of filtration, drying, and separation technologies due to stringent standards governing equipment efficiency and end-product quality. Analysis suggests that demand in this region is further reinforced by the growing emphasis on energy efficiency and predictive maintenance in factory automation. Additionally, the integration of smart monitoring systems in air treatment infrastructure presents a strong compressed air treatment equipment market opportunity for advanced technology providers.

Europe demonstrates a mature yet innovation-focused market landscape. Countries such as Germany, France, and Italy prioritize clean compressed air in electronics, food packaging, and chemical processing. Regional adoption is heavily guided by EU directives and ISO standards that emphasize environmental sustainability and safety compliance. Market analysis indicates that demand here is increasingly leaning toward compact, modular systems and solutions that support carbon-neutral operations. Moreover, retrofitting of aging industrial infrastructure with energy-saving equipment continues to generate sustained market activity, especially in Central and Western Europe.

Latin America presents a developing market with growing adoption in emerging manufacturing hubs across Brazil, Mexico, and Argentina. Industrial growth in food processing, mining, and automotive assembly lines is creating steady compressed air treatment equipment market demand, although price sensitivity remains a notable factor. Regional analysis indicates that while large-scale facilities are increasingly investing in quality air treatment solutions, smaller operations rely on basic filtration units. Opportunities lie in educating end users on the long-term operational benefits of advanced air treatment systems, particularly those that improve energy efficiency and reduce downtime.

The Middle East and Africa region is in the early stages of market expansion but is steadily gaining traction. The need is closely tied to the rise of petrochemical facilities, power generation plants, and infrastructure projects in countries like the UAE, Saudi Arabia, and South Africa. Industrial diversification strategies and environmental policies are encouraging investment in cleaner and more efficient plant operations. According to the analysis, the limited awareness of lifecycle cost savings and inconsistent maintenance practices present both challenges and opportunities. However, increasing collaborations between international vendors and local distributors are expected to enhance equipment penetration across high-growth sectors.

Top Key Players and Market Share Insights:

The compressed air treatment equipment market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global compressed air treatment equipment market. Key players in the compressed air treatment equipment industry include -

- Atlas Copco AB (Sweden)

- BOGE Kompressoren Otto Boge GmbH & Co. KG (Germany)

- BEKO Technologies GmbH (Germany)

- Elgi Equipments Limited (India)

- Chicago Pneumatic (USA)

- Kaeser Kompressoren SE (Germany)

- Ingersoll Rand Inc. (USA)

- Donaldson Company, Inc. (USA)

- Parker-Hannifin Corporation (USA)

- MANN+HUMMEL GmbH (Germany)

Recent Industry Developments :

Product Launches:

- In March 2025, SAF-Holland launched ApolloSDx, an air treatment system for heavy-duty vehicle applications. It removes water vapor, moisture, oil particles, and other contaminants efficiently from the compressed air generated by the truck’s compressor before it enters the air brake reservoirs. This product enables the company to set a new standard in air treatment, ensuring enhanced durability and reliability for vehicle applications requiring superior air-drying performance.

- In January 2025, Emerson launched the AVENTICSTM DS1 Dew Point Sensor, an industrial sensor to monitor dew point, temperature, humidity levels and quality of compressed air and other non-corrosive gases in real time from a single device.

Acquisitions:

- In January 2025, Atlas Copco Group completed the acquisition of Trident Pneumatics Pvt. Ltd, an Indian manufacturer of compressed air treatment and on-site gas generation. This acquisition enables Atlas Copco to expand their presence in the Indian market and strengthen their offerings.

Compressed Air Treatment Equipment Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 15.70 Billion |

| CAGR (2025-2032) | 6.7% |

| By Product Type |

|

| By Application |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Compressed Air Treatment Equipment Market? +

Compressed Air Treatment Equipment Market size is estimated to reach over USD 15.70 Billion by 2032 from a value of USD 9.35 Billion in 2024 and is projected to grow by USD 9.81 Billion in 2025, growing at a CAGR of 6.7% from 2025 to 2032.

What specific segmentation details are covered in the Compressed Air Treatment Equipment Market report? +

The Compressed Air Treatment Equipment market report includes specific segmentation details for product type, application and end-use industry.

What are the end-use industries in the Compressed Air Treatment Equipment Market? +

The end-use industries of the Compressed Air Treatment Equipment Market are manufacturing, food & beverage, pharmaceuticals, healthcare, chemicals & petrochemicals, energy & power, automotive, textile, aerospace & defense, electronics & semiconductors and others.

Who are the major players in the Compressed Air Treatment Equipment Market? +

The key participants in the Compressed Air Treatment Equipment market are Atlas Copco AB (Sweden), BOGE Kompressoren Otto Boge GmbH & Co. KG (Germany), Kaeser Kompressoren SE (Germany), Ingersoll Rand Inc. (USA), Donaldson Company, Inc. (USA), Parker-Hannifin Corporation (USA), MANN+HUMMEL GmbH (Germany), BEKO Technologies GmbH (Germany), Elgi Equipments Limited (India), Chicago Pneumatic (USA).