- Summary

- Table Of Content

- Methodology

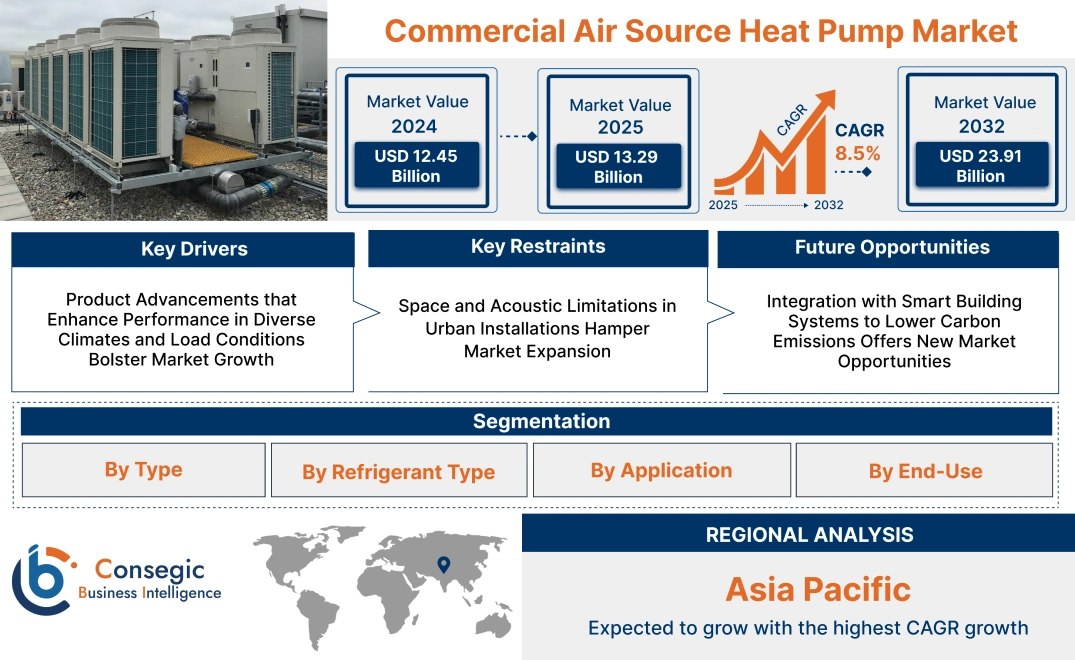

Commercial Air Source Heat Pump Market Size:

Commercial Air Source Heat Pump Market size is estimated to reach over USD 23.91 Billion by 2032 from a value of USD 12.45 Billion in 2024 and is projected to grow by USD 13.29 Billion in 2025, growing at a CAGR of 8.5% from 2025 to 2032.

Commercial Air Source Heat Pump Market Scope & Overview:

A commercial air source heat pump is a high-efficiency HVAC solution to extract thermal energy from ambient air for heating and cooling purposes in large-scale facilities. Designed for offices, retail centers, educational institutions, and hospitality spaces, it supports centralized climate control with minimal mechanical complexity.

These systems incorporate variable-speed compressors, smart defrost cycles, and programmable controls to ensure reliable operation across varying load demands. Available in split and packaged configurations, they work well with existing ductwork or hydronic systems.

Their main benefits include low operating noise, simplified maintenance, and consistent indoor temperature regulation. The system delivers both heating and cooling from a single unit, eliminating the need for separate equipment and streamlining installation. Moreover, commercial air source heat pump solutions support zoned control and building automation compatibility, making them suitable for modern infrastructure focused on occupant comfort, system efficiency, and reduced lifecycle costs.

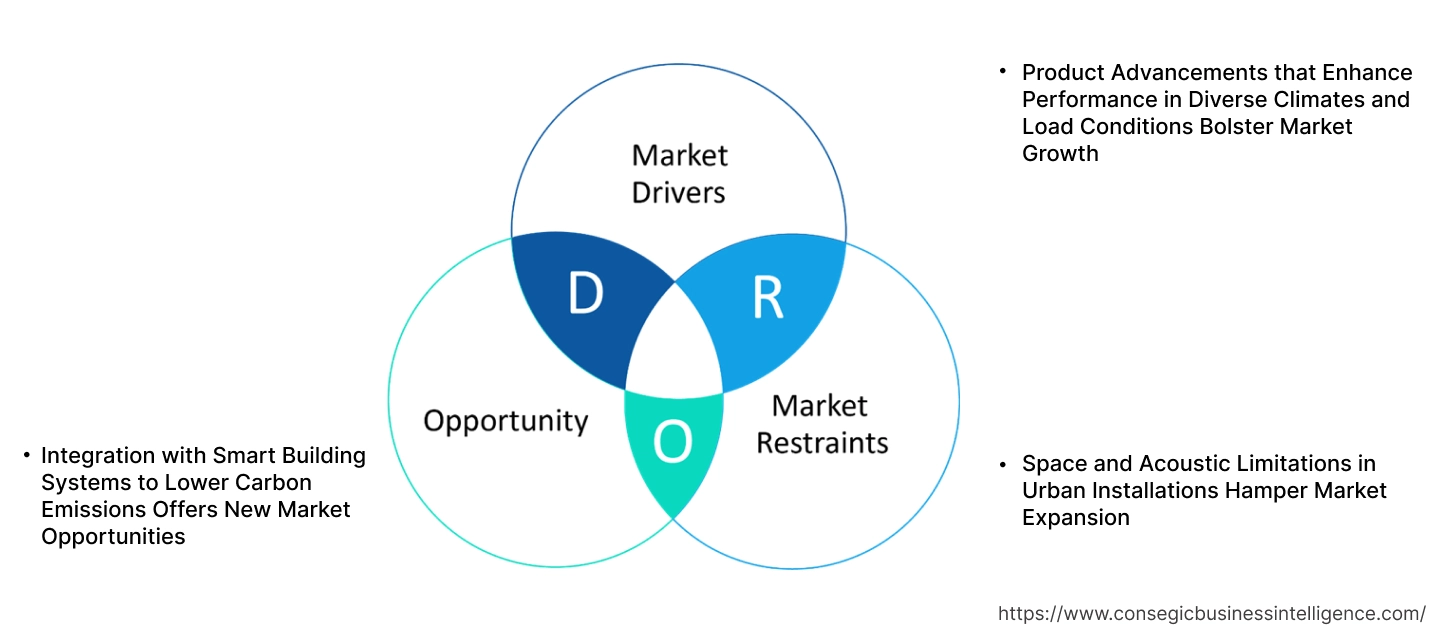

Commercial Air Source Heat Pump Market Dynamics - (DRO) :

Key Drivers:

Product Advancements that Enhance Performance in Diverse Climates and Load Conditions Bolster Market Growth

Manufacturers are introducing next-generation commercial air source heat pumps equipped with advanced components such as variable-speed compressors, vapor injection systems, and adaptive defrost controls. These innovations improve performance under fluctuating load conditions and deliver efficient heating in sub-zero temperatures. Enhanced seasonal coefficients of performance (SCOP) make these systems possible across a wider geographic range, including cold climate regions. The flexibility to operate under extreme weather conditions while maintaining a comfortable indoor temperature supports broader commercial adoption. These systems also offer better modulation, reduced energy use, and quieter operation, making them suitable for sensitive commercial settings.

- For instance, in February 2025, Carrier launched its first high-temperature air source heat pump for commercial and residential purposes, the AquaSnap® 61AQ. The heat pump operates using R-290, a natural refrigerant with nearly-zero Global Warming Potential (GWP). It has been optimized for this refrigerant and delivers high-temperature heating up to 75°C at outdoor temperatures of -7°C and operates efficiently in extreme conditions of -25°C. Moreover, it exceeds Ecodesign efficiency standards by up to 30%.

As building operators seek dependable and efficient heating and cooling solutions in varying climatic conditions, demand for adaptive HVAC technologies is increasing. This shift toward climate-resilient, performance-optimized systems is driving sustained commercial air source heat pump market expansion.

Key Restraints:

Space and Acoustic Limitations in Urban Installations Hamper Market Expansion

Installing commercial air source heat pumps in dense urban environments presents practical challenges. Large-capacity units require significant outdoor space for heat exchangers and airflow clearance, which is often limited on rooftops or building exteriors in crowded cityscapes. Additionally, noise generated by fans and compressors during high-load operation exceeds permissible limits, especially in mixed-use zones near schools or adjacent to residential buildings. These constraints hinder installations in locations where physical footprint and acoustic impact must be tightly managed. While compact and noise-reduced models exist, their capacity often falls short of larger building requirements. In such scenarios, building owners delay adoption or opt for alternative systems with greater design flexibility. Thus, despite growing demand for sustainable HVAC in urban areas, these limitations remain a barrier to commercial air source heat pump market growth.

Future Opportunities :

Integration with Smart Building Systems to Lower Carbon Emissions Offers New Market Opportunities

As commercial buildings shift toward net-zero targets, smart HVAC integration is becoming essential. Commercial air source heat pumps that interface with building management systems (BMS) enable operators to regulate indoor climate dynamically, monitor performance remotely, and participate in demand response programs. These smart integrations optimize load scheduling, reduce peak energy usage, and provide data-driven insights for energy conservation. Advanced control algorithms also enhance user comfort while supporting carbon reduction goals. In markets where building decarbonization incentives are tied to energy performance metrics, intelligent HVAC systems are gaining preference. Necessity is increasing across office buildings, campuses, and hospitality sectors that prioritize emissions accountability and operational efficiency.

- For instance, in November 2024, Wondrwall introduced a new air source heat pump integrated with its proprietary AI-powered Home Energy Management System (HEMS). Wondrwall Heat Pump enables low-carbon heating efficiency, reduces energy consumption and lowers running costs for homeowners. It features adaptive start/stop controls along with automatic adjustment of flow temperatures based on occupancy, weather patterns and the home’s thermal performance. Furthermore, the company opened the Wondrwall platform to all heat pump manufacturers to benefit from improved efficiencies. While this is for residential purposes, it opens up avenues for potential commercial application developments.

The convergence of digital control and electrified HVAC systems is creating strong commercial air source heat pump market opportunities fueled by both performance growth and sustainability mandates.

Commercial Air Source Heat Pump Market Segmental Analysis :

By Type:

Based on type, the market is divided into air-to-air heat pumps and air-to-water heat pumps.

The air-to-air heat pumps segment accounted for the largest commercial air source heat pump market share in 2024.

- Air-to-air systems transfer thermal energy from outside air to indoor air, offering both heating and cooling functionality in commercial buildings.

- These systems are widely used in retrofit projects and small to medium-sized office and retail applications due to ease of installation and zoning capability.

- They support ducted and ductless formats, making them versatile for modern HVAC configurations.

- As per commercial air source heat pump market analysis, their popularity is driven by cost-efficiency and dual-mode operation.

The air-to-water heat pumps segment is projected to register the fastest CAGR during the forecast period.

- Air-to-water systems extract ambient heat and transfer it into hydronic systems used for underfloor heating, radiators, and domestic hot water.

- Their integration with low-temperature heating networks and hybrid systems is accelerating adoption in large-scale commercial infrastructure.

- These pumps provide higher energy performance in colder climates when paired with thermal storage.

- According to commercial air source heat pump market trends, air-to-water units are seeing rapid uptake in green building developments and LEED-certified structures.

By Refrigerant Type:

Based on refrigerant type, the commercial air source heat pump market is segmented into R410A, R32, CO₂, Propane (R290), and others.

The R410A segment held the largest revenue share in 2024.

- R410A is a common refrigerant in commercial heat pumps due to its strong thermodynamic performance and global availability.

- It is used extensively in packaged rooftop systems and variable refrigerant flow (VRF) installations.

- Despite its high global warming potential (GWP), legacy infrastructure and equipment compatibility support its continued deployment.

- As per commercial air source heat pump market analysis, this segment remains dominant until replacement refrigerants scale economically.

The R32 segment is projected to witness the fastest CAGR.

- R32 offers better heat transfer performance and lower GWP than R410A, aligning with environmental compliance regulations.

- It is increasingly adopted in split systems and medium-capacity commercial units.

- OEMs are transitioning to R32 systems as part of their product decarbonization strategies.

- For instance, in January 2025, Clivet launched new air source heat pumps, Large EV PL, for commercial buildings. The heat pump operates on R32 refrigerant and inverter rotary/scroll compressors. Additionally, it is capable of variable speed control with a capacity range of 44 kW to 238 kW, a seasonal coefficient of performance (SCOP) of 4.17 and a seasonal energy efficiency ratio (SEER) of 4.65.

- Commercial air source heat pump market trends indicate that regional climate policies in Europe and Asia-Pacific are accelerating the switch to low-GWP refrigerants.

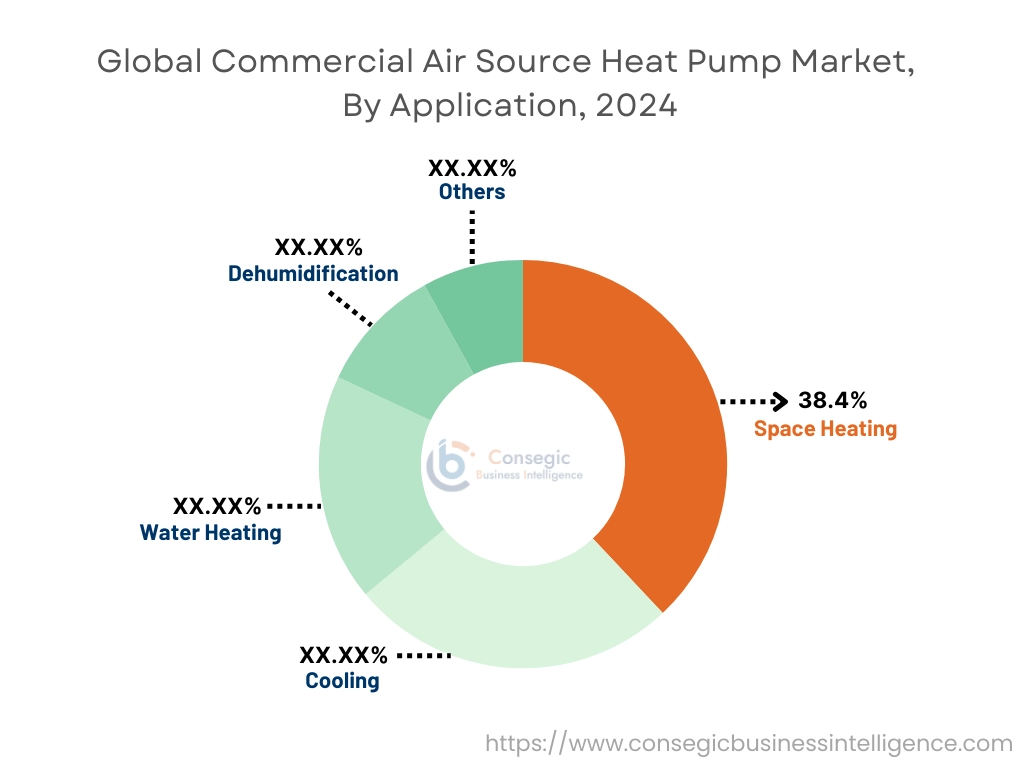

By Application:

Based on application, the market is categorized into space heating, cooling, water heating, dehumidification, and others.

The space heating segment accounted for the largest commercial air source heat pump market share of 38.4% in 2024.

- Space heating is a critical function in cold regions, especially for offices, educational campuses, and healthcare facilities.

- Heat pumps offer efficient and consistent heating, replacing fossil-fuel-based boilers and reducing operational costs.

- They can be integrated with building automation systems for improved control and zone management.

- Commercial air source heat pump market demand for heating is reinforced by carbon neutrality targets and the push for electrification in buildings.

The water heating segment is projected to grow at the fastest CAGR.

- Commercial water heating is essential in hotels, hospitals, and food service industries where the hot water requirement is continuous.

- Air-to-water heat pumps with storage tanks are increasingly replacing electric resistance and gas water heaters.

- High efficiency and lower energy bills contribute to increased adoption, especially in areas with renewable electricity sources.

- Hence, water heating systems are integral to net-zero energy strategies across commercial properties, which drives commercial air source heat pump market growth.

By End-Use:

Based on end-use, the market is segmented into office buildings, healthcare facilities, educational institutions, retail stores, hospitality, and others.

The office buildings segment held the largest revenue share in 2024.

- Office environments benefit from heat pumps’ zoned control, energy efficiency, and ability to deliver both heating and cooling.

- Renovation of old HVAC systems and mandates for green certification are driving installations in commercial office blocks.

- Systems are integrated with variable-speed fans and smart thermostats to maximize comfort and efficiency.

- Thus, the commercial air source heat pump market demand is bolstered by HVAC modernization across corporate campuses and coworking spaces.

The hospitality segment is projected to register the fastest CAGR.

- Hotels and resorts require continuous space conditioning and water heating, making heat pumps ideal for efficient, year-round operation.

- Quiet operation, compact design, and support for smart building management systems make heat pumps ideal for guest comfort.

- The segment benefits from industry-wide sustainability goals and investment in green-certified building infrastructure.

- Commercial air source heat pump market expansion is accelerated by hospitality brands adopting heat pumps to align with ESG reporting requirements.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

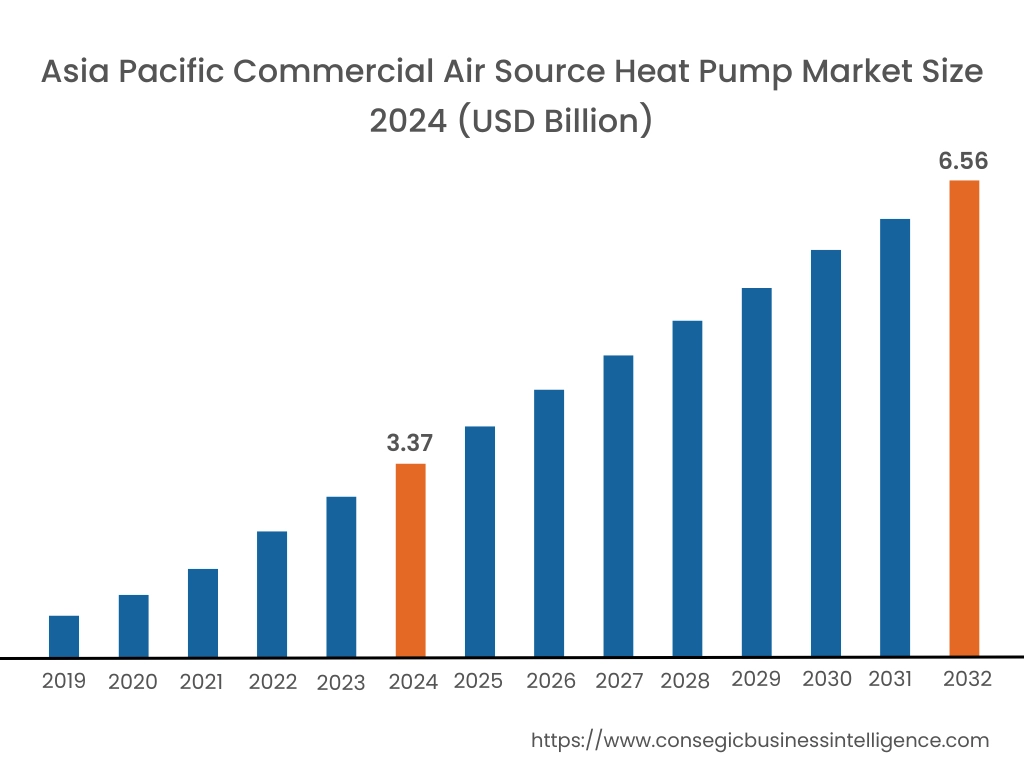

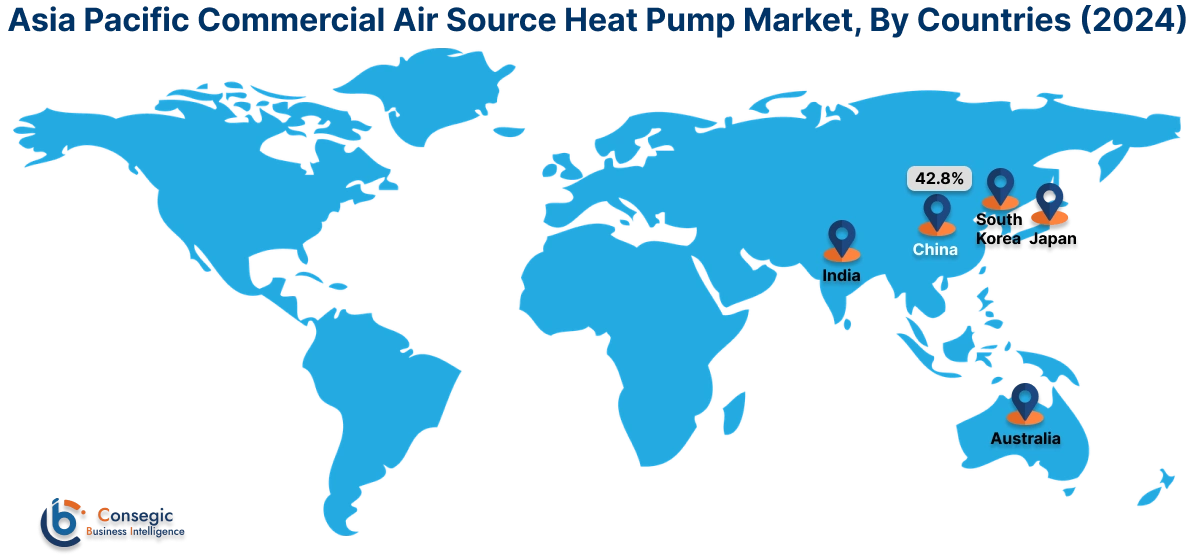

Asia Pacific region was valued at USD 3.37 Billion in 2024. Moreover, it is projected to grow by USD 3.60 Billion in 2025 and reach over USD 6.56 Billion by 2032. Out of this, China accounted for the maximum revenue share of 42.8%. Asia-Pacific is experiencing rapid growth, with widespread adoption in China, Japan, South Korea, and Australia. In China, air source heat pump systems are gaining traction in commercial buildings, hospitality complexes, and educational institutions as part of national energy-efficiency reforms and clean heating transitions. Japan and South Korea continue to innovate with compact, high-efficiency units adapted to space-constrained urban landscapes. Market analysis also reveals that Australia is scaling adoption through decarbonization strategies in commercial construction, particularly in high-performance office spaces and retail centers. The region's strong manufacturing capacity, combined with rising environmental awareness, is accelerating adoption across a broad range of verticals.

North America is estimated to reach over USD 7.96 Billion by 2032 from a value of USD 4.14 Billion in 2024 and is projected to grow by USD 4.42 Billion in 2025. North America is witnessing consistent adoption of air source heat pump systems, particularly in the United States and Canada where commercial buildings, schools, and public infrastructure projects are shifting toward electrified heating and cooling solutions. Market analysis indicates that rising utility costs and electrification incentives are encouraging the transition from gas-fired HVAC systems to variable-speed air source heat pumps. The adoption of dual-source units and cold-climate-optimized technologies is increasing in regions with extended heating seasons. Growth in this region is supported by carbon reduction initiatives, utility rebate programs, and performance-based building codes targeting net-zero energy usage.

Europe remains a leading market for energy-efficient HVAC systems due to ambitious emissions targets and evolving building regulations. Countries such as Germany, France, the UK, and the Netherlands are actively retrofitting commercial properties and municipal buildings with low-carbon heating and cooling systems. Market analysis shows increased deployment of inverter-based air source systems that comply with energy labeling requirements and offer low-noise operation in densely populated urban environments. Furthermore, the integration of renewable electricity sources and the implementation of district-scale heating strategies in locations using these heat pumps offer potential avenues for growth.

Latin America is an emerging market, with increasing interest in sustainable HVAC systems across Brazil, Mexico, and Chile. Adoption is primarily seen in commercial offices, healthcare facilities, and hospitality sectors in urban areas where utility infrastructure supports electric heating solutions. Market analysis points to rising need for cost-effective, low-maintenance systems that offer both cooling and heating capabilities in regions with moderate climate variation. Public and private initiatives to modernize building energy infrastructure are expected to contribute to steady growth. The commercial air source heat pump market opportunity in this region lies in expanding awareness, training local professionals, and offering systems designed for regional grid conditions and environmental goals.

The Middle East and Africa are gradually incorporating air source heat pump technology, particularly in regions with growing demand for sustainable cooling and heating in commercial facilities. In countries such as the UAE, Saudi Arabia, and South Africa, commercial development projects are integrating air source systems into green building designs and energy-efficient retrofits. Market analysis indicates that the potential for hybrid systems combining air source heat pumps with solar and thermal storage is being explored in high-performance commercial campuses. Though adoption remains limited, government-backed sustainability initiatives and high ambient cooling loads are expected to foster market expansion in the coming years.

Top Key Players and Market Share Insights:

The commercial air source heat pump market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global commercial air source heat pump market. Key players in the commercial air source heat pump industry include -

- Daikin Industries Ltd. (Japan)

- Mitsubishi Electric Corporation (Japan)

- Panasonic Holdings Corporation (Japan)

- Glen Dimplex Group (Ireland)

- Guangdong PHNIX Eco-Energy Solution Ltd. (China)

- LG Electronics Inc. (South Korea)

- Samsung Electronics Co., Ltd. (South Korea)

- Bosch Thermotechnology GmbH (Germany)

- Stiebel Eltron GmbH & Co. KG (Germany)

- Clivet S.p.A. (Italy)

Recent Industry Developments :

Product Launches:

- In March 2024, Aira launched the new Aira Heat Pump for residential heating. This heat pump operates using a smart app and a thermostat. Being a smart appliance, it learns the users’ hot water consumption patterns for precise heating, reducing heating costs and carbon emissions.

Commercial Air Source Heat Pump Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 23.91 Billion |

| CAGR (2025-2032) | 8.5% |

| By Type |

|

| By Refrigerant Type |

|

| By Application |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Commercial Air Source Heat Pump Market? +

Commercial Air Source Heat Pump Market size is estimated to reach over USD 23.91 Billion by 2032 from a value of USD 12.45 Billion in 2024 and is projected to grow by USD 13.29 Billion in 2025, growing at a CAGR of 8.5% from 2025 to 2032.

What specific segmentation details are covered in the Commercial Air Source Heat Pump Market report? +

The Commercial Air Source Heat Pump market report includes specific segmentation details for type, refrigerant type, application and end-use.

What are the end-use of the Commercial Air Source Heat Pump Market? +

The end-use of the Commercial Air Source Heat Pump Market are office buildings, healthcare facilities, educational institutions, retail stores, hospitality, and others.

Who are the major players in the Commercial Air Source Heat Pump Market? +

The key participants in the Commercial Air Source Heat Pump market are Daikin Industries, Ltd. (Japan), Mitsubishi Electric Corporation (Japan), Panasonic Holdings Corporation (Japan), LG Electronics Inc. (South Korea), Samsung Electronics Co., Ltd. (South Korea), Bosch Thermotechnology GmbH (Germany), Stiebel Eltron GmbH & Co. KG (Germany), Clivet S.p.A. (Italy), Glen Dimplex Group (Ireland) and Guangdong PHNIX Eco-Energy Solution Ltd. (China).